FOMO is back.

ANZ economists say there now appears to be an element of the fear of missing out (FOMO) driving the housing market, based on an assumption that house prices will keep increasing.

In the bank's latest ANZ Property Focus, ANZ chief economist Sharon Zollner, senior economist Liz Kendall and senior strategist David Croy are forecasting that house prices will actually fall 4% in 2021, before recovering, but concede this is a smaller and later fall than they earlier expected.

For now, though, there's FOMO, a dynamic that "has the potential to contribute to frothiness in the market that ultimately cannot be sustained – adding to financial stability risks", they say.

"The fact is, history – especially further back than the past few decades – tells us that house prices do indeed fall from time to time and that the market can turn very quickly."

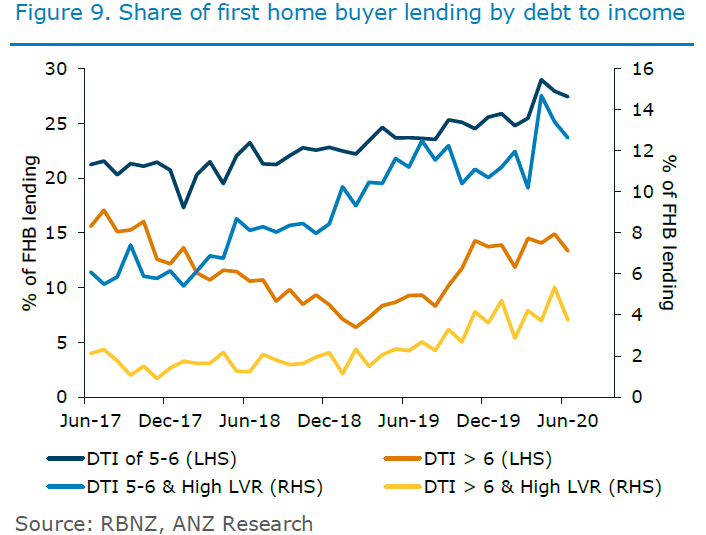

They say expectations that interest rates will remain low are encouraging borrowers to enter the market with debt levels that are high relative to their incomes, even if deposits are decent.

"We have seen first home buyer activity increase, and those buyers are more likely to be in vulnerable debt-to-income categories, even if their equity positions are good. Indeed, there has been an upward trend in the share of buyers in riskier debt-to-income buckets over the past year."

The economists say "exuberance", if it continues, could contribute to a more pronounced housing cycle, "adding to risks that the housing market has further to fall if it eventually turns".

"This risk is accentuated to the extent that buyers who are entering the market have high debt-to-income ratios, making them more vulnerable to income strains. Income strains are a typical pressure point for the housing market in a recession."

Good equity positions (low LVRs) make it less likely that homeowners will go into negative equity if house prices fall, they say.

"But if someone’s income dries up, then they may not be able to service their mortgage, no matter how low mortgage rates might seem right now.

"In the extreme, this can lead to significant financial hardship, fire sales and nasty feedback loops between house prices, spending and credit supply."

Debt levels are high

The economists note that house prices and household debt levels are already very high in New Zealand, making the market vulnerable to a "disorderly correction" at some point.

"This isn’t a new risk by any means, but an outright housing boom in a recession would certainly up the ante.

They say housing affordability is a serious social and economic problem in New Zealand that requires some mix of lower prices and/or enormously higher incomes to resolve.

"Seeing prices drift lower as a result of more supply, weaker population pressures or adjusting regulation would be socially desirable, even if it would come at a cost to existing homeowners.

"But triggering a demand-choking painful correction in house prices would most certainly not be a win.

"To be clear, it is not our expectation that such a painful correction in house prices will occur, but the risk is there, and increased speculative behaviour that could expose borrowers to income strains adds to it."

Housing market 'out of step'

They point out that unemployment looks set to rise, even if by less than previously expected, and some households will face more challenging times ahead.

"As such, we are becoming concerned that the housing market appears to be increasingly moving out of step with fundamentals, like rents and incomes – particularly given our expectations for where those fundamentals are headed."

Therefore, they say looking forward, they expect that the economic recovery will stagnate, that closed border impacts will become more evident, and that income strains will increase – and ripple well beyond low-income earners.

"It is our view that these effects will see some wobbles emerging in the housing market as we enter 2021, even as mortgage rates move lower.

"Our current assumption is that we see another strong quarter to finish the year, but that house prices will fall 4% next year, before recovering. This is a smaller, later fall than our previous forecasts.

"Of course, the outlook is highly uncertain and the strength in the housing market to date has surprised us.

"It is possible that further declines in mortgage rates have a more potent effect than we assume and the housing party goes on longer.

Recognising the risks

"But there is also the possibility that increased income strains, reduced population pressures, and a shift in expectations lead to a more abrupt adjustment in house prices than incorporated in our central forecast."

The economists say that policymakers will be "cognisant of the risks on both sides".

If, however, the market continues to run hot and macro-prudential policy is deemed necessary, the obvious response would be to reinstate LVR restrictions, which were lifted in May, at least for 12 months.

The economists say that responding to the situation with broader tools, like the 'counter-cyclical capital buffer', could risk choking non-housing lending though, so not all macro-prudential policy options would be deemed appropriate.

"The RBNZ plans to review whether to reinstate LVR restrictions in March next year. The case would be particularly clear if there was a surge in low-deposit lending between now and then. But implementing LVRs isn’t the only option, and it may not be effective or indeed the best response.

"High debt-to-income ratios (like high LVRs) can be a significant source of vulnerability in a downturn, and risks tentatively appear to be building in this area.

'A case could be made for DTIs'

"The RBNZ does not currently have a mandate to implement debt-to-income (DTI) restrictions, but its macro-prudential policy powers are currently under review as part of The Reserve Bank Act Review.

"A case could be made for expanding the RBNZ’s powers to include these sorts of tools should they be required in the future, even if they are not needed any time soon.

"But it’s political, because DTIs make it harder for first home buyers to get on the ladder."

Broader policies, the economists say, are also needed to address our long-term housing affordability challenge, like adjustments to regulations limiting land supply and building, and ensuring that population flows are sustainable (once the border opens) given limited home building capacity and infrastructure. Such policies can help from a financial stability perspective too.

"Lack of responsiveness of housing supply and huge swings in population can lead to house prices becoming unaffordable, but can also lead to more exaggerated house price cycles overall. There are no easy answers, but doing nothing isn’t a solution either."

55 Comments

ANZ will happily sell your house at mortgagee auction when you cant make payments in the future.

Buyer beware. If you over pay and cant afford it take your short back and sides haircut with good graces when the economy goes bad.

They won't sell your house before they have charged 100k of collection and legal fees... best to not go there

Ton of investors cashed up sitting waiting on the sidelines should that occur. Don't think we'll see many distressed sales personally. But let's see in 6 months...

With stimulus chances are low but it depends on unemployment numbers. If big enough they will struggle to pay the rent and so called investors in houses (speculators is a better term) will not be getting rents to pay rates and insurance even. You can see pockets of this now in NZ I think.

I believe rental market problems are happening in Wellington central now. A stat I have also been following is rentals available in Wellington (excluding outer areas Porirua, Lower Hutt, Upper Hutt and Kapiti Coast and Wairarapa) there are 605 houses / apartments for rent. https://www.trademe.co.nz/a/property/residential/rent/wellington/wellin…

Friends of mine down there cannot rent properties that are usually always rented. The lack of foreign students and lack of tourists for Air BnB looks to be impacting. Lots in the 605 have not been rented for 6 months.

Speaking to friends and family in NZ they all seem to be completely possessed by the idea that it doesn't matter how much you have to borrow anymore because prices will only ever go up until the end of time.

It reminds me a lot of the mentality at the peak of the last crypto bubble. All caution thrown to the wind.

This certainly seems to be the case. I missed out on a very average house in Auckland yesterday, CV 720, needed work, body corp, sold for 1.1 mill. I get the impression the guy who bought it would happily have gone higher.

The interest rates and removal of LVRs ( plus the seemingly vindicated "you cannot lose in NZ houses") are making things very hard, and dangerous.

What were you prepared to pay?

Ideally 850, but I was prepared to go to 900 as I'm fed up looking.

Send the Reserve Bank an email thanking them for screwing you over.

Same, every time when I catch up with friends, housing is the topic being talked most. My friend's colleagues also talk about house market all the time. I'd agree with you that kiwis are now possessed with housing market right now thanks to our governments and RBNZ.

We really have nothing else. Our property market is worth over $1T, whereas our sharemarket is worth $180B. It's the only way the majority of the country has built their wealth. Not through business, not through innovation, through buying a house and existing. Where else in the world are older teachers and nurses multi-millionaires? (no offence). I'm a homeowner, but believe the market needs to come crashing down so we can reset and normalise our unhealthy obsession for property. But RBNZ and the Govt won't let that happen as it's, unfortunately, our most important asset class for economic stability.

Pretty boring and one dimensional people!

[ removed ]

Just noticed that ASB have recently slashed margin lending on many blue chip NZX50 companies. Don't think they have done this before. They must be worried about the possibility of big drops.

[ removed ]

… for those who don't own a house and don't have a mortgage

If it's really end up like what you've said, Yvil, our economy is in a very messy situation. I'd recommend you sell your houses and take your money to another country if you can...

Agreed the entire system is propped up by the RBNZ & Government and we all know they will keep doing this... sooo give me a good reason why house prices are going to go down all of a sudden???

Well, there may come a point where younger generations no longer put up with being second class citizens. They have borne the brunt of Covid - greater unemployment, reduced opportunities, and not even the silver lining of lower rents and house prices. I wouldn't like to be a landlord when the under 30s start getting really pissed off about the way things have played out.

In a Prisoner's Dilemma way it may make sense for younger Kiwis to just give up on keeping COVID out and welcome it in to New Zealand instead of making sacrifices only to be screwed over the by the older generations and their out of control Reserve Bank. They might crash everything, but be little worse off than otherwise.

We need to start throwing them a bone rather than only transferring wealth upward to older, wealthier asset owners.

I cry myself to sleep every night because of my lack of bank profit donations.

Tears of joy

Hmm, you'd think so. But... it's more likely Kiwis would read a sharemarket crash as further evidence that property is the only decent investment around.

Yes, I was thinking the same... will the stock market contagion spread into housing? It’ll definitely make banks nervous given mark to market

But, but, but removing LVR's was done to increase financial stability! Clearly that has "worked" (which in RBNZ language means the opposite).

So exactly what I complained about when I sent angry letters to the RBNZ is coming to pass (financial system instability). Will they reverse the removal of LVRs? Apparently not until next year. Bascand and Orr have to go, they have done the opposite of their mandate by removing LVRs.

They are accountable to the fish and chip shop lady at the end of the day but she was elected on a cult of personality not on a deep understanding of macroeconomics.

Hugs and state houses and hairbrained shared ownership schemes and easier access to debt for tiny dogboxes are totally going to solve the problem you see.

BL that attitude also prevailed during the 1920s in the USA

Until 1929

The big crash may hit in 2029

They are right so far though.

My logic using reason and mathematics doesn't seem to explain how prices could conceivably keep increasing.

But they always do.

Why? It's simply a function of interest rates and available credit.

The interest bearing component on a 100k loan 15 years ago at 10% is ~the same as a 500k loan now.

What I find inconceivable is the cheapness of money now. A 65 year old retiring now would have expected ~50k pretax income on deposits. Ha good luck now.

Sure. Except we are now at zero.

How do they keep increasing from here?

Well it's been said and used quite a few times before - they go negative.

Interest rates have been dropping in NZ for a long time now, from what I can see, people are buying houses more or less entirely on the weekly payments, sod the principal. A house at 800k 18 months ago when rates were 4.5% would be about 750/week. Now at 2.5% you can spend 1000000 and your still better off per week at about 730. Then the LVR has been reduced and the penalty interest is very low now so you can borrow the 1 million with your deposit for 800k and still pay the same per week.... For now....

It seems the FOMO is a vendor thing these days as much as it is happening with hordes of stupid money motivated by the removal of LVR restrictions which are likely to be gone pretty soon.

Markets get driven by sentiment

Hi David,

Return of FOMO has been created by RBNZ (not just by lowering interest rate, which had to for economt) and got real high when Asian (sorry for using the word but feel strongly) looking deputy governor came out in media to bat for rising house price.

His words were that rising housing prices are very good for the economy and we will do everything to support it AND it is at that time, when many including FHB realized that if RBNZ wants the ponzi to continue than who is going to stop them.

House prices have been steady after lockdown but actually took off last month when RBNZ officers went around town attending media conferences in favour of rising house price.

You can check that June/July though was high but not what has been created by RBNZ to hide their limitation by artificially inflating house price from already high price for short term gain.

Question is that if everyone is aware of the FOMO being created than what it is been done to calm it. It is RBNZ who should come out to calm but it is they who have instigared it, so to expect from them to act is stupidity. When RBNZ is the only agency (government turning blind eye as it suits them) who can bring some sense to tbe market (not crash) but their priority is to hide theur limitation and failure of the agency behind the housing euphoria.

Mr Orrrrrr by his action (or no action) is only delaying the inevitable and more the delay Bigger the disastor.

Specuvestors all firing before new LVRs arrive. The lucky offloading to the not so lucky (time will tell). All ways you look at it it seems mad unless inflation is about to make everything twice the price.

Perhaps it is.

Nothing new, RBNZ to support speculators will announce giving everyone enough time (window opportunity) to ramp up the ponzi.

Should ask Mr Err, When had fear of house price came out with announcement to protect with immediate effect and NOW when price is getting out of control, why the delay.

Should act now to protect many FHB who under FOMO are stretching to buy now specially with 5% deposit as possible of them ending with negative equity and the blame should be government and Mr ErrrrrOrr.

Orr may have to leave New Zealand after this.

He won't be welcome at restaurants and cafes, as Rod Petricevic found after he screwed people over financially: http://www.stuff.co.nz/business/money/3106541/Angry-investors-rough-up-…

Powers that be may be stupid but I think they're aware it's impossible to increase rates and inflation with debt the way it is now. So negative interest rates may be the only way to go. However I recently put it out there that I don't think we'll go negative. So what does that leave... low rates and returns scraping along the bottom for years and maybe a few other policy changes to try and slow (not stop) house prices.

Agent: Here's a house built 50 years ago, the current owners paid $400k for it back in 2010 and have done very little to it and in fact it's in worse condition than when they bought it...this beauty can be all yours for $1.2m Buyer: Wait...$1.2m now and it's in worse condition? What possibly can validate a 3x price tag for a worse product? Agent: That person over there is willing to pay $1.19m.

Congrats RBNZ. You have given banks the ability put the average punter into ever increasing amounts of debt.

The Agent is asking you are you a greater fool than that person over there?

That is why its best to minimize talking to agents and do your own due diligence.

I prefer they don't speak when I look at property.

Generally when their lips are moving they are lying much like Politicians.

They'll tut-tut at younger folk and pretend it was all through their own hard work that they deserve that wealth transfer.

"The RBNZ plans to review whether to reinstate LVR restrictions in March next year."

Jeez, don't rush it Adrian!

Offers over $469k for a 2 bed 80 sqm 1985 "Keith Hay" home in Masterton. Sold for $240k in 2017.

https://www.92hillcrestst.com/?fbclid=IwAR29AA7GYB2bS34PKySCHndbVXXM6hm…

Thank goodness for Labour's Foreign Buyers Ban to take the heat out of the housing market !

Exactly. It's good ole local 'ma and pa' that's the problem. So how can we get a NZ 'ma and pa' property "investor" buyer ban?

Cough TAX Cough.

Stopping the banks allowing investors to leverage capital in residential property to buy more residential property would really be the only way. But that could only come from the RBNZ, and given their track record, it is unlikely to happen.

Given that a high percentage of house purchases are straight-to-rental, a property tax to disincentive landlords from buying up so many would only cause rents to rise as they seek to recoup the tax.

Possibly having a property cap for investors that would force landlords to diverge themselves of a portion of their portfolio could have an affect, but again, if they see their revenue shrinking they will increase rents to compensate.

KiwiBuild could have worked, if it hadn't been hijacked by developers looking to make a quick buck. But something like that is needed. A residential building boom, similar to the 60's (I assume, given the high number of 60's properties that appear. Or was it in the 40's?)

There was that news reporter who was a FHB, and lost out on a property, but overheard the winning bidder mention "don't really need the house. got plenty already", and it's that level of greed and selfishness that just winds me up.

Those Chinese sounding names.

This is now just to hard to fix. Perhaps and end of the world scenario might help lower prices, wooops just tried Covid and it had the opposite effect. Perhaps a Civil War in the USA post November 4th 2020 might have the required ripple effect ? Honestly the NZ property market is as bullet proof as you could possibly get, its left me almost speechless. Listings in Tauranga totally static and are so low its not funny. It must get to the point where the majority of listings are either total rubbish (as this is an ideal time to offload during a panic ) or just overpriced.

The RBNZ & govt are clever enough to hide the RE inflation from the normal CPI report, recently it's not even meeting their 1-3 percent bands, which means? they must reduce more OCR/preferably in negative and provide more stimulus. The more stimulus? the more it can be siphoned quickly on the way of rental & mortgage payment towards inflated housing. so, this is a win-win solution with our only way of F.I.R.E economy. This is the way it should be. Peoples productivity, are all being put into leash.. to work harder, smarter, longer hours, no kids etc. to cope with the stimulus/incentive that being put as a 'roof'.. to have that.. you must do those - The unknown questions right now into 2021? is those real producers, will they have to hike their price of milk, rice, bread, egg, petrol, public transportation, healthcare med cost etc. as well? to balance the delta between the RE rise.

And yet they just offered me half a million backed to a fairly modest single salary.

I just wish these bank economists would STFU. Take their careful manicured economo- speak and shove it.

It's just tedious now.

Pass the remote.

I used to have respect bankers. Remember when the local bank manager was a well respected member of the community? Now this form of capitalism has turned them into the equivalent of dodgy used car sales people. Selling cheap debt for a living.

Investors leverage on stuff not built yet is driving froth and frenzy, not FHB.

They are clearing out the stuff developers wanted to get shot of off the plan and all.

Now that is dissipating the market is "clearing" and sales will be slowing from here on in

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.