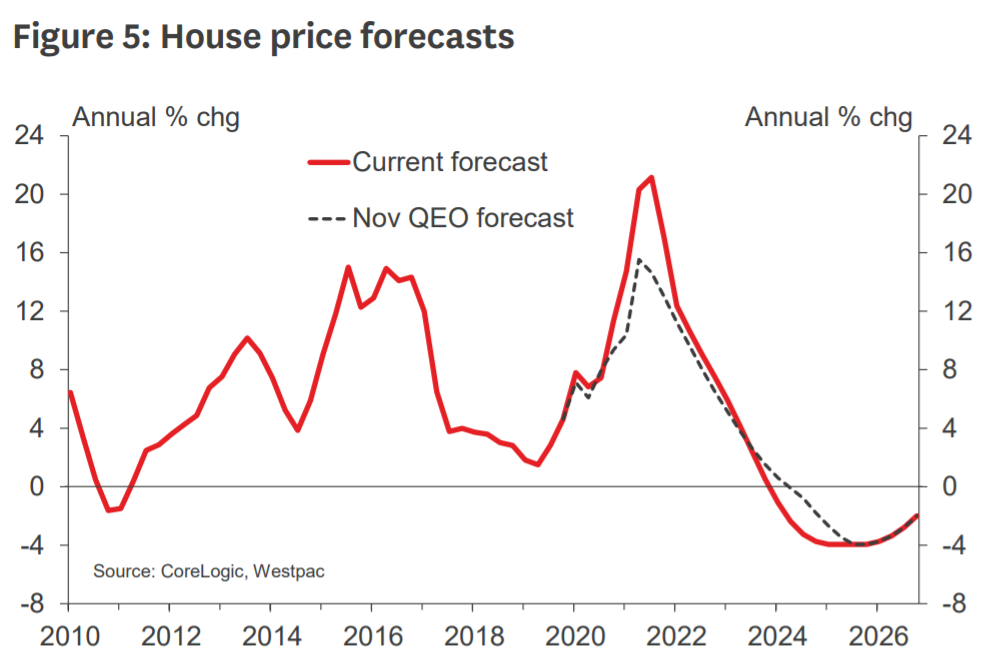

Westpac economists see the heat staying on in the housing market this year and 17% gains in house prices - but eventually the market will turn negative, with price falls by 2024.

Another cautionary note, is that the economists see some possibility the Government might limit the deductibility of interest for investors.

In the bank's latest quarterly Economic Overview Westpac chief economist Dominick Stephens says the housing market has heated up "much as we warned".

Stephens says a 17% rise in prices this year will be a very strong pace compared to history, but implicitly actually a slowdown from the current monthly pace.

"We believe that mortgage rates have reached their lows for this cycle, with long-term interest rates now starting to head higher as global economic sentiment improves.

"The impact will become greater as the prospect of OCR hikes draws closer; we expect house price inflation to turn negative by 2024."

Stephens notes that rising house prices have rapidly become a social and political flashpoint, with the Government pledging to take “bold action” on both housing demand and supply.

"We regard the options as limited. The Reserve Bank’s tightening of loan-to-value restrictions will have some dampening effect on prices, but historically it has been a small one."

He notes that the Government has ruled out many of the options regarding the tax treatment of property, such as a capital gains tax.

"However, one remaining possibility is to limit the deductibility of interest for property investors, which could have an impact on prices depending on how it was applied. We regard this as a downside risk to our house price forecast."

He reiterated the point the Westpac economists have made previously that with housing supply, the ground has already shifted. The construction sector turned out to be one of the surprise stars of 2020, and with dwelling consents soaring to new multi-decade highs, there is a strong pipeline of work for 2021 as well.

"This building boom is coming at a time when population growth has plunged to its lowest rate in a decade. Net migration has been close to zero since Covid-19 struck, a far cry from the 70,000 net migrants the country received in 2019. This means that the severe housing shortages that have been dogging New Zealand for years are now rapidly eroding. By our estimates, housing shortages will continue to shrink even after migration resumes, because today’s level of construction activity is so much higher than what is needed to keep pace with population growth even in a normal year.

"We expect to see rent inflation easing within a year. And this erosion of housing shortages is one reason that we expect house price inflation to start gradually cooling from later in 2021."

In terms of the economy in general, Stephens says GDP may have been strong recently, but the Westpac economics team thinks the “summer without tourists” will cause a decline of 0.7% over the six months to March.

Additionally they estimate that disruptions to global supply chains will cause inflation to spike to 2.5% by June this year, but that it will drop all the way back to 0.8% by June 2022.

"That’s partly because supply chains will normalise and partly because we anticipate a big lift in the exchange rate, to 78 cents against the USD."

The economists expect moderate growth in household incomes this year.

"Labour market indicators point to further growth in jobs, but we expect wage growth to remain subdued this year. Solid agricultural prices will also provide a boost to rural incomes. Fiscal support to households has moved away from direct transfers, and is now coming through more in the form of rising public sector employment."

This is some of the key points:

- The “summer without tourists” will cause a GDP decline of 0.7% over the six months to March.

- Inflation will reach 2.5% by June, but will drop back to 0.8% by June 2022.

- The exchange rate will rise to 78 cents against the USD.

- The OCR will remain at 0.25% until early-2024.

- The housing shortages that have long dogged New Zealand are now rapidly receding thanks to booming construction activity and low population growth.

88 Comments

I basically switch off on these bank economist viewpoints these days.

However, I would say that 17% increase in prices this year, and no increase in the OCR till 2024, don't seem credible scenarios.

Do you think it's more credible that OCR increases sooner, or later than 2024? Just out of interest.

Definitely sooner, in mid 2022.

But, not by much. Perhaps only to 0.5 or 0.75 max by end of 2022.

The one caveat is if there is a global financial crisis. But he hasn't stated that. No increases till 2024 seems to be his base position.

I hear you, not credible and also not impossible.

Agree it's not *impossible*

In 3 months (end of 2020), house prices in tauranga rose over 10 percent and many other cities over 6 percent... !!! The speculators will be loading up right now to take advantage Comparatively to orksland other cities are cheap so this will help propel them up. And yes it depends what happens in orksland to calculate the overall figure. Personally i am very happy if prices do not rise, strong rises are too destabilizing

Fritz, so do you think house prices will rise by more or less than 17% ?

See below Yvil, 5-10%.

Fritz

"I basically switch off" when I see posters such as yourself making predictions. :)

Actually I have substantiated if you care to read.

In summary:

- political unacceptability of high house price inflation will stir actions that will dampen price increases

- reduced stimulus from RBNZ will do same

- however, favourable market factors will still mean solid house price gains this year

Do you disagree with any of that, and if so why.

agree Fritz - Westpac is way out of line with what every other economist is predicting and this economist also predicted 15-20% decreases in April 2020 - which again was way more than other economists.

The other reason why they wont increase by that much is 17% would represent to a first home buyer another 25-40K (depending on the region) in deposit needed just to get into the market, for the average first home buyer this is at least 1-2 years savings. As a number of economists have already said (including corelogic and REINZ) the market will cool when the first home buyers reach their maximum borrowing capacity and the deposit becomes too large - at 150K-200K for a 20% deposit in NZ- I'd say we are very close to that tipping point.

Good point.

Unless the govt implements more support for first home buyers- eg doubling the Homestart grant, more widespread 95% loans to FHB, increasing the price caps and eligibility of Homestart grants

Yeah, but I don't know if that would boost prices *much*, if there is a house price cap. It limits the ability of FHBs to bid up prices

But who would want a 95% loan at these prices? The compound interest would be staggering

Unless the govt implements more support for first home buyers- eg doubling the Homestart grant, more widespread 95% loans to FHB, increasing the price caps and eligibility of Homestart grants

The higher prices also mean higher equity if you already own a property. Bearing in mind that borrowing against an existing property is using leverage, the amount you can borrow to purchase will increase even more than the valuation increase in your existing property (assuming the new investment property is cheaper than your existing one, which would be usual). That's part of how this bubble works.

For your info P8, and for others, I am not going to engage in ad hominem stuff anymore.

I am keeping it to debating the issue, not denigrating the person.

Fritz

Don't get touchy.

The issue is that you outright dismiss all bank economists and then put yourself up as the font of all knowledge and accurate predictions. :)

That's not true and again I am not going to engage in that.

So, what do you disagree with me on and why? Let's engage in that rather than put downs.

fritz

I don't necessarily disagree with you on your prediction - in fact since late last October I have posted that I see a cooling of the market this year due to affordability issues and increasing impact of bank and RBNZ LVRs. Like you, I see some increase and possibly some minor correction as RBNZ will not want to see a serve correction to undo their actions on simulating the economy through housing.

What gets up my nostril is that on this site is anonymous key board warriors simply rubbish bank economists outright and the RBNZ as a bunch of Wallys. My post was a light hearted dig at your posting along those lines.

Economics is not an exact science. All economic reports and forecasts making observations and drawing conclusions are simply an opinion on the factors at that time and of course those factors are for ever changing (a case in point is the current Auckland Covid situation and even Bloomfield doesn't know the extent of it). The astute and experienced person will consider the views of a variety sources and critically and along with other views come to their own conclusion - to "switch off" and outright dismiss bank economists and put one's self indicates at best a bit of naivety.

You may be interested that ANZ NZ Economic Update out today on REINZ results comments much along the same lines as you do:

"The market remains tight, but turnover in the market has started the year at much more normal levels. This moderation could see price pressures normalise in coming months. We expect to see a cooling in house price inflation in time as credit and affordability constraints bite, and the more moderate pulse in sales activity to start the year could signal the beginning of that. We will need to wait and see where the dust settles in the next couple of months".

There is no certainty (and the ANZ comment mentions this).

The astute home buyer or property investor will be looking at a range of opinions - not dismissing them - to come to their own conclusion.

So, yes, your conclusion has some validity worthy of consideration.

Printer8

You take credit for forecasting mass asset inflation as if you are an economic genius. Yet you never admit banks creating credit and central bank rate manipulation as the cause.

Ponzi

Sorry son, I don't have the foggiest of where you are coming from. A strange weird post.

I am not currently forecasting mass asset inflation nor not acknowledging that RBNZ has had a role. Quite the opposite actually.

Dominic hasn’t got the best track record and is constantly “updating” his forecasts when he gets it wrong.

Awesome

Well said, ignoring trolling is we can do since reports won't be taken into account by the admins.

I have been often guilty of ad hominem. I am not playing that game anymore.

Others can play it if they like.

bank economists horizon is at most 1.5yrs, and do not understand how global political environment drive economy.

So prices to fall this year?

Don't expect any OCR change unless the rest of the world change first.

Mr Orr's favourite come back is 'We're just following global best practise'

Generally agree with that... nz has been a leader in raising interest rates in 2012 but had to back down and that was under wheeler I recall not orr. Orr has the complexity of the new mandate that requires maximum sustainable employment which for nz means a low not high exchange rate. Equivalent to pissing into a strong wind

We are told the Govt is going to do ‘something’ Stephen’s suggest removing deductibility of interest.

Question for readers....what’s your call...or rather, what else is there. Bright line extension, first home buyer grants? Go.

Equity tax - https://www.top.org.nz/property_tax

Fortunately this government isn't quite that misguided!

Would be pleasantly surprised if it turned out to be a Stamp Duty like Aussie and I hear England have. However back on planet earth.. I am betting yet another non-announcement

That didn't work so it's all a bit pointless. It is a revenue raising tool, not contributing to controlling house price inflation. It penalises everyday punters.

If the government removed interest deductibility like the Westpac economist suggests it would destroy the growing build-to-rent industry which is one of the supply solutions to the current rise in housing inflation expectations.

It might contribute to another big jump in rental rates as investors need to claw back the losses even harder. It would be yet another kick in the teeth to the average Ma and Pa investor (read voter) who already had their losses deferred, and property rights stripped, with added compliance and management costs added onto them. If Labour are stupid enough to go that way, they'll be electorally punished by centre voters.

I reckon they'll decree that a maximum of 60% of the purchase price borrowings will be tax deductable. (i.e. The deposit is non tax deductable) All to complement the 40% deposit. That'll bugger those using existing equity to raise the deposit.

I predict Westpacs prediction will be 99% inaccurate.

They predicted the house price would fall by 10~15% in the year 2020 due to the pandemic.

We would probably get a better forecast about the economy asking pretty much anyone else than these bank economists.

These guys are starting to sound like Harry Dent and Peter Schiff... Calling it but never happens... Will be correct eventually. How can they predict 2024..

Bank economists tell you what they want you to believe, not what they actually expect to happen. In the unlikely event that it does, however, they'll gladly take that as a sign of their brilliant prescience and foresight. In the far more likely event that they're wrong, they'll excuse themselves by blaming it on something which nobody could possibly have expected, shrug their shoulders, and move on to the next prediction.

PonziKiwi...The one thing rational people should be able to agree on. Property will not always continue to go up for ever and at some time in the future it is certain that there will be a very severe and long-lasting correction. And when this will happen nobody can predict with any certainty at all.

To me the only thing sillier than saying there will be a crash at this specific time in the future is saying there will never be a crash. Harry Dent and Schiff and the other precise (negative shock) predictors are knowledgeable but just looking for sensational click bait. The "never a crash in NZ" types like Ashley Church are just plain ignorant.

I can't argue with what Dent and Schiff say. But fundemantals are out the window. Church knows because banks will continue to create credit out of thin air for awhile yet.

Supply is an issue, but it's not *the* issue. The combination of low interest rates and fear of inflation is the issue.

Interest rates will follow whatever happens internationally, the RB doesn't really have a lot of power there unless they think the currency is seriously out of whack.

Fear of inflation is around because people see how much deficit spending is happening. That's only going to increase as we try to counteract the unpalatable outcomes of the low interest rates.

The only trigger for interest rate rises would be a currency collapse in a major economy. Central banks and the IMF will create an infinite amount of new money to prevent that situation.

So I see house prices rising slowly but steadily in a time of zero real growth for the foreseeable future. A kind of slow drowning. Stagflation, basically, because those who control the levers would rather drown slowly than risk a 'shock'.

totally agree - a slow drowning until something snaps

Interest rates cant rise

Asset prices cant fall

Everything & some will be thrown at it to starve off a crash

Lack of income growth means deficit spending to the moon

I imagine we will see Govt's increasingly "take over" bad loans in many sectors (not write them off) with much PR about its a temporary situation soon to be reversed when those good times roll up ...

Yeah. And we've already seen this story play out, in Japan and then in Europe. Stagnation in real terms, and debt that can grow infinitely so long as liquidity gets pumped in to any creaky joints in the machinery. I think this is the lesson they've learned from the GFC -- that what brings things down is a liquidity crunch. So just make sure that anyone who is demanding a debt be repaid gets their money, even if the actual counterparty is insolvent -- turn it into collective debt for the common good, to keep the wheels turning. And it kind of works, in the sense that Japan and the Eurozone are still functioning political and economic entities with reasonable living standards, mostly.

Yet there's an assumption that making exactly the same moves will have a different outcome in the Anglosphere. Tech, or something, never mind that all those tech dollars are only valuable insofar as they're eventually used to buy products in the real world. For now, it's a hasty rotation of capital out of some sectors (of industry and society) and into others, hoarding wealth in advance of the zero-growth economy.

(double post, pls remove)

I will clarify why I think 17% house price increase will be wrong.

Because it's politically untenable.

Just as it seems it is politically untenable for prices to drop, it would be political suicide for Labour if prices rose anything near 17%.

I haven't given enough attention to the political dimension previously, and these economists clearly aren't.

The other reason I think it is unlikely is that the stimulus of cutting the OCR and money printing has stopped.

Yet, prices will increase because while the government has a lot of influence, it has far from total influence. I think they will increase somewhere between 5-10% this year.

Labour needs prices to drop, it is losing voters who have started to feel outraged by the lack of action and won't take long for other parties to capitalize on that. The only way these people can afford purchasing a home is for prices to go lower.

Fritz, I respectfully disagree. The (upwards) price volatility has been so much recently that 17% would barely register. NZ houses are like Tesla shares at this point -- they've detached from any conventional notion of value, so no price is startling.

Fair enough.

I just think that the political unacceptability of this will lead to govt action that prevents those kinds of increases.

Having said that, who knows with these clowns in charge?

They might do something that supercharges FHB demand...

I would have said the same thing this time last year though - that it would be politically untenable for house prices to go up 17%. They've gone up 19%. But I didn't trust Labour on this issue anyway, which is why I didn't vote for them for the first time in a long time last election. I don't think they actually want to solve this problem.

Yeah, I agree with a lot of that.

But...I do think they were stuck a bit between a rock and a hard place last year.

I don't see the same thing happening.

Why not? From my perspective, prices have been stupidly high (and increasing at stupid levels) for basically a decade now. It's ridiculous that the average price in Lower Hutt, for example, is $800k. It would be ridiculous if the average price were $1 million. Once you get to these levels of stupidity, you're into essentially decreasing marginal returns on stupidity - that is, things are already so ridiculous that massive rapid increases don't make things any more ridiculous. Bit like how Jeff Bezos is already so stupidly rich that an extra billion dollars doesn't really make much of a difference to how stupidly rich he is in the scheme of things.

There were good reasons for their actions last year, but with obvious housing inflation consequences.

It could happen again this year, granted, if we have multiple lockdowns lasting at least 1-2 weeks. If that happens, then one could see OCR cut to negative, and then once again all bets are off...

So I guess I should caveat my views as follows:

- very limited lockdowns: house price increases of 5-10%

- significant lockdowns, with OCR cut into negative territory: price increases could be higher

No, Labour will only pretend to care and make changes that only effect the peripheries.

Like Adrian Orr, they are able to tolerate stupid price increases if it keeps the economy looking rosy.

Its all about the optics!!!

So we are about to see the fastest ( and consecutive) years of growth in prices in percentage terms since 1995 and roaming moas.

I think 17 percent is about right.. But politically it will be a win for Labour! It will be spun as a booming economy and people have money to spend. Also half the population will love all the paper wealth! Govt definitely wants solid increases of sustained 15 percent gains year on year..

That would disenfranchise a large proprtion of their traditional voter base.

Fritz

Possibly.. But remember labour and green have solid support from inner city hypocritical urban liberals. Also identity politics locks in minorities regardless of economic conditions..

Yep that's a valid point. A big chunk of their fanbase are 'chardonnay socialists' who care more about virtue signaling than real gains in the lives of the downtrodden.

Still, I think Labour would still view price rises of 17% as highly problematic.

Pretty pointless going out to 2024, nobody got the last 6 months correct let alone years into the future. Certainly the next few months look clear and everyone can see it. Prices are only going one way unless there is a major change.

Can deduce that Mike Kirk and his chums don’t work at Westpac.

What chums?

This is not a conspiracy!

Meanwhile REINZ today shows that Dec-Jan sales fell 46% in Auckland.

Yes, in answer to the inevitable cries, they do ALWAYS fall in January compared to Dec.

But usual fall is in order of 27%.

LVR and shortage of stock to sell is now taking effect.

And to those who mocked when I said 18th February was the "turn", are you still laughing?

Mike

House prices and the stock market will keep climbing. I don't argue with your sentiments but the market is rigged. Nobody is allowed to fail anymore. It will be proped up at all costs..

Hi

thanks for your comments.

Yes, it is rigged.

But sales will fall off, as will prices, but still probably be rising art 8% pa by mid year, so acceleration decelerating

The pool of greater fools is not infinite and it's already started to drain, you should know that given your nickname.

B21

When the banks fail courtesy of the fed and it's global franchises including Mr Orr and we have only one bank issuing digital currency then the game is over..

You cannot sell a house if its not for sale. Sales volume will be down because the market has gone nuts and there is no stock left. Almost down to 1/3 of the properties available in Tauranga compared to a year ago. Everything that is for sale is being snapped up, its manic out there. No way you would sell your house at present for the pure fun of it, you would need to be moving town because of work or some other major reason. Everyone is holding until Christmas.

1000 newly built houses coming out each month in Auckland alone. Add this to other houses on sale, which are in record numbers. Where's the shortage?

Galbraith said there are two types of economic forecasters. Those who don't know and those who don't know they don't know. I suspect Dominick Stevens falls into the latter category.

As a property investor, nothing scares me as much as the "one remaining possibility is to limit the deductibility of interest for property investors". Why is no one talking about this? The UK introduced this a few years ago and it crushed mum and dad investors. Would it be any different here?

What do we need to do to prepare?

Make a company that is in the business of money lending. Its loans (from the bank) are deductible because they are not investment property loans, lend yourself money from that business to buy your investment properties? It all just sounds like making work for accountants & lawyers whilst cutting out those who can’t afford them from the market.

The bank isn't going to lend the money without getting a mortgage over the house that you're going to purchase, so it will still be considered an investment property loan.

Crystal ball gazing but who knows, it would appear prices will be up not down or flat.

17 % would be a $2.5million paper gain for me but it's all irrelevant as I'm not selling anything anyway.

I have my properties for cashflow and capital security.

This can't go on forever ! or can it ?

DS doesn't caveat his opinions enough, this is foolish. There's still potentially a lot of volatile and unpredictable water to flow under the bridge.

We, in nz, are all set to repeat our own version of US induced 2008/09 GFC. And why not? If we are encouraged to own homes, affordability aside, at 1.99% cost of money, we are told is a no brainer. We are told prices will not drop as drops wont be permitted. We are all set to go.

A financial crisis will bring it all down, as it did in the USA in 08.

When, who knows? But I have been picking 2022 for a couple of years.

2022 would be a good pick. House prices will peak at Christmas and Covid-19 will still be a clear and present danger. Personally I don't think we will get on top of Covid-19, it has the ability to keep side stepping a vaccine. The financial system is broken, eventually everyone will see the Emperor standing there naked.

Some here might confirm that I have been saying that for a year or two :)

Everything goes in cycles, and typically there is a financial crisis every 8-10 years. We haven't had one since 08, and there seem to be a lot of vulnerabilities in the system right now.

I'd like to see continued capital gains for my own sake, but really I think there's so much risk of overshoot in building + overshoot in rentals. You're probably not wrong with 2022, gives 2021 a chance to work through the "sticky on the way down" phase.

People are taking on liabilities (debt) in the expectation of future gains. The real kicker is whether we continue to see a drop off in net migration numbers (there's a trend showing) and a steady run of building consents/CCC's.

600k rentals in the market are no good if only 550k households need a rental, may see Landlords start Dutch auctioning, will start with apartments.

How many foreign students have remained in NZ to see out the rest of their year's study, and are on their way home?

In all of this don't forget the wider world economy and where it is likely headed. For those interested 'Crazy days for money' is a good read. https://www.goldmoney.com/research/goldmoney-insights/crazy-days-for-mo…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.