BNZ economists say the Government is "dead set" on curtailing soaring house prices and "will almost certainly win in the end".

In a detailed commentary on the housing changes announced by the Government this week, BNZ's head of research Stephen Toplis says the Government had been saying for some time it wanted to curtail rising prices - but prices just kept soaring.

"So, it should come as no surprise that their patience has now been exhausted and a full attack on prices is now under way."

Toplis says whether or not the measures announced this week have the desired impact or not "is neither here nor there".

"The fact of the matter is the Government will do what it takes. If this set of policies fails then more will be introduced until such time that house price inflation abates (or even prices fall). The Government is, in large part, staking its credibility on this and cannot be seen to fail."

Other economists have also raised the possibility of falling prices.

The Government has, Toplis says, now "fully exposed its intention" to moderate house price inflation.

"It will almost certainly win in the end. We have been saying this for some time now, and will repeat our warning, that investing in houses is not a one way bet."

'House price inflation zero - at best'

He says the government will not be happy unless house price growth falls below income growth.

"...So it is reasonable to assume house price inflation will fall to near zero, at best, in the not too distant future."

The risk, he says, is that no government, or central bank, has ever been able to fine tune an asset market - so the balance of risk is that a decent correction in prices occurs.

"For all but new purchasers this matters little as it will simply reverse some of the exceptional capital gain we have seen over the recent past. The possibility of a substantial correction is multiplied if we are right with our potential [housing] oversupply diagnosis and if the recently announced measures have a substantial negative impact on sentiment. House prices would come under significant pressure if everyone headed for the exit at the same time."

On that potential oversupply of houses, Toplis says in the period prior to the arrival of Covid-19, growth in new houses was not keeping up with population growth so an already stretched market was becoming more stretched.

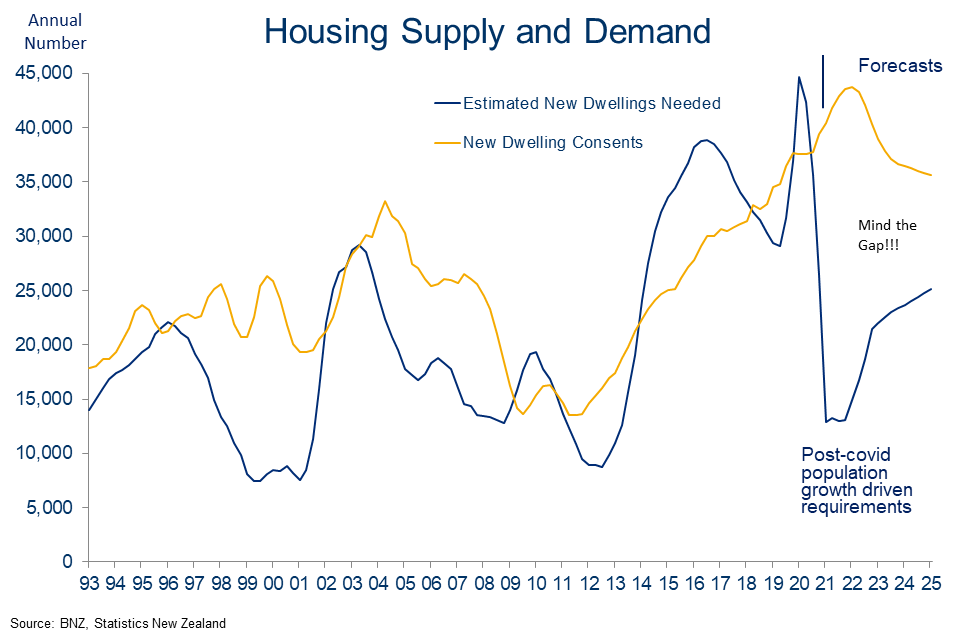

"But over the last twelve months we have been building far more houses than are needed to cope with the population’s expansion. Indeed, right here and now, we are probably building one new dwelling for every one person increase in population. This is clearly not sustainable."

Toplis says the BNZ economists' forecasts suggest the country will continue to build more houses than we need to cope with population growth for some time.

"Consequently, we will be chewing into that housing shortage rapidly even without the measures the government has just announced.

"Our forecast profile suggests that to reach some form of equilibrium, either residential construction needs to be weaker than we expect or population growth much stronger. And the natural clearing mechanism for the market would be a drop in prices."

'Purely for capital gain'

In terms of the likely falling returns to investors following the introduction of these Government measures, Toplis says many investors have been investing purely for the purposes of capital gain.

"That capital gain will now be reduced to the extent the bright-line test might apply and the net cost of providing accommodation will rise given the reduced deductibility of interest rate costs. All other things being equal, this will initially push up rents and/or reduce the supply of rental accommodation.

"What happens to the rents and the costs of construction feeds directly into the CPI [inflation].

"We think that in this respect inflation will probably be higher and, hence, heighten the possibility that the Reserve Bank might tighten monetary policy. However, house price inflation is a major driver of the Reserve Bank’s private consumption forecasts. If house prices are lower than they otherwise would be, the RBNZ’s models will produce lower GDP growth and lower pressure on capacity than previously and, hence, less need for tighter policy.

"Financial markets seem to have focused on the latter by pricing in later rate hikes and a consequentially lower NZD. Balance of risk says this is the right thing to do but we still caution that the economy’s inflationary pulse, both domestically and internationally, is growing and we still think the next move in rates will be up, potentially sooner and more aggressively than many believe.

"This won’t help the housing market either."

237 Comments

About time

... so far , they're just tinkering around the edges ... very little to address the three drivers of house price rises : easy credit , unfettered immigration , slack of supply .... very slack on addressing the supply side of the equation ...

It's so much easier & more popular to blame and to kick the crap out of investors ....

Why not do both? /s

.. nothing more fun than publicly booting the snot out of landlords ... it's a hoot ...

But ... it doesn't actually help increase house supply ...

..if it lowers prices and swaps out landlords with fhb's then that's progress - and i'd wager that's gonna happen. Supply issues will take longer.

No point increasing supply when 4 out of 10 house are being grabbed by speculators.

The two largest drags on the socioeconomic well-being of this country: housing and migration - plenty of perverse incentives within both systems for a handful of players to make short-term gains at the expense of vulnerable individuals.

Time for drastic changes to both!

Advisor

What is your source of the 4 out of 10 houses are being currently grabbed by "speculators"?

RBNZ mortgage data indicates investors accounting for 16 to 17% of mortgages over the past six months.

If supply is not to be increased then were are we going to put the numerous "homeless" currently in motels?

Yes, good to see investors discouraged and FHB encouraged but that is not creating a single additional house in urgent need.

You, like many on this this site need to see the housing and renting issues as being more than FHB and increasing rents - unfortunately the "homeless" don't contribute to this site.

Where do you get those figures? Investor lending has been sitting at about 25%? See yesterday’s lending data.

Albert

RBNZ

https://www.rbnz.govt.nz/statistics/c31

Columns U and X for number which your refer to - not % of value of houses as often used but misleading.

New mortgage data but will be most house sales and reflective of trend.

Your 25% is still well short of your initial claim of 40%.

Also big difference between investors and speculators - I think speculators would be likely well under 10%.

Cheers

All the investors are now worried and media is playing along to support their cause.

here is a link to a story published on Stuff.co.nz. Owners are crying foul, when they have an investment property, that they have rented to their parents who get money from the government. Very smart. Government subsidy is paying their rent/mortgage for an investment property. Now they have to top up a bit because of change in rules and they are not happy.

Shame on Stuff.co.nz to publish these hopeless stories and stroke false alarms.

https://www.stuff.co.nz/life-style/homed/latest/124652371/family-that-b…

Yes, i don't think they realize how they come accross. I mean, its nice that they bought a home for their parents. But they've also managed to arrange things so that the taxpayer is helping them buy an asset which, being in Northland, has no doubt gained a lot in value since they bought it. There's a very good chance that the extra they pay in tax is less than the accommodation supplement, which while in their parents name, effectively goes straight into their pockets.

FamilyGuy...so that is two fewer houses that our own people could be living in rather than be holed up in a motel for years or living in a garage or even a car. And why? Because we took pity on an extended Sth African family and allowed them to come here and fill two of our houses. Maybe they witnessed a shooting or two, maybe in real life or maybe just on a TV screen. Who knows and to be blunt who really cares. What is important is the divisive message this sends to kiwis on the lower (financial) rungs of our society. They see foreigners living in homes while there is no home for them in their place of birth. It shows them that nobody cares about them and that they will never have the opportunity to be a real part of an inclusive society.

South Africans are great people, they love a beer, a laugh and the rugby and cricket, it's not personal, but it is completely unacceptable that we are housing these people while our own citizens remain homeless.

There's been a lot of crocodile tears in the last couple of days, they are just trying to make their case heard and for once try to look like the loosing party, when in reality it is exactly the opposite. Get ready for a campaign against the government from now on, who should crack down on usury and speculation and make it clear this type of unproductive and parasitic behaviour is not allowed in this country.

I never claimed 40%, I'm just relaying information published by interest yesterday

... agreed ... the 3 magic words in this House Price Emergency are " supply , supply , supply ! " ...

According to the BNZ, they have actually been doing well getting housing supply kicked into gear recently

""But over the last twelve months we have been building far more houses than are needed to cope with the population’s expansion. Indeed, right here and now, we are probably building one new dwelling for every one person increase in population. This is clearly not sustainable."

Toplis says the BNZ economists' forecasts suggest the country will continue to build more houses than we need to cope with population growth for some time."

But look at what is being built - Trade Me is starting to become awash with unsold townhouses. We will see an oversupply of apartments and terraced houses. I think traditional "family" homes on 500sqm+ will hold in value as no one is building them anywhere close to the main centres.

True, but if you're a FHB, thats great! Not everyone needs or wants a large section with some very expensive (per SQM) grass on it.

I agree, I reckon Flatbush in Auckland could be the canary in the coal mine if things head south

If you have driven through that area recently? And have you ever experienced how differently developments of any scale (small or large) in Europe look and work for families? I am not surprised that even naive and not very discerning customers in New Zealand see no value in those cardbox boxes squeezed onto section after section in flatbush. Let alone being able to raise finance for whats being asked for price wise...

Labour have done much more to address the problem in 4 years than National did in 9 years, it was 9 years wasted under National.

Removing the investors interest "wealth subsidy" was a fantastic move, one National would never contemplate having the guts to do

Hmmm however investors are more agile than Governments......

Incidentally in discussions with landlords tenant's can expect a 10 % rent increase .......

Yeah but like what was reported in the NZ Herald today, investors have been raising rent over the last year quite a lot, while interest rates costs to them have got substantially lower.

So what does that tell you?

Either they are very greedy, which some of them are, or that a lot of them shouldn't even be in the property market, and are pushing up prices way to high, and paying too much, off the back of knowing in the past they could get ridiculous write off's of their losses at the end of the year.

Pricing home owners out of the market because they couldn't compete due to not being able to claim back losses.

Someone had to have to guts to end it, finally a government has ended that rort.

oh, in my incidental discussions with other tenants, most also are on 1 year fixed terms to start with. Thats probably due to both letting agencies needing a nice annual racket, and landlords requiring some security of income to make the highly levered mortgage payments! I just cant wait to see overleveraged landlords professional service falling apart the minute rules change to make it about professional returns instead of speculation on capital value. Should also add that looking at moving again in 7-8 months if landlord would ask for more rent. Except this time, I expect a much better selection to choose from than just 6 months ago. I started looking to follow market in city fringe areas and it certainly looks much easier already than the few months after first lockdown. And this is for someone who also got affected by the housing insanity because of a separation. Very few actually give this issue any thought either. It is not only first home buyers that are seriously struggling with house price issues.

Are you a landlord yourself? I think you just admitted to price fixing. But don’t worry, as you are a mum or pop I’m sure its ok.

You forgot demand from investors, >20% of demand according to who's buying property.

Really? I never seen so many new houses pop up in my area than what has in the last few years, it seems to me home building work is going gangbusters.

I think I heard they are training 50,000 more apprentices, they are doing everything right in my book, removing the interest deductions was a masterstroke.

100% better effort than Nationals no effort at all on the problem, and just try to pretend the problem doesn't exist.

Sorry accidentally reported

Exactly right, not a fan of taxpayer money going to subsidize some of NZ's most wealthy people, all the while making it hard for average people to afford a house.

Well, if BNZ is right - all that is needed now are rent controls.

I suggest universal rent controls to produce a weekly rent maxima under the formula [(GV/1000) +/- X%] - the value of 'X' set to bring lower quartile properties on an area basis (the same areas as covered by tenancy.govt.nz) back to 30% of median household income (before tax) for that region.

#rentcontrolnow.

"BNZ economists say the government is "dead set" on curtailing soaring house prices and "will almost certainly win in the end".

Great. Go for it and keep going, all the way. These are just the first timid steps, and much more has to be done. Now is the time to change monetary policy too.

We need a managed, progressive but significant decrease in house prices. Better be bold and have the housing Ponzi deflated now, than experiencing a catastrophic collapse later on.

Perhaps if Labour had supported the revamp of the RMA National wanted, the situation re supply may not have become so dire.

.. if memory serves they twice blocked the Gnats from RMA reform .... it'd be easier to go back to a simple Town & Country Planning Act , and rebuild it from there up ...

Lets not even try and pretend National cares about any housing crisis or the majority of New Zealanders. Their interest in reforming the rma was solely for greed and to change the rules to benefit themselves and their mates. Key in 2014 - "There is no housing crisis in New Zealand"

Yes lets not forget that that National had 9 years to sort out the housing crisis that they largely created through growing a property false economy, selling NZ off as fast as possible to foreign buyers and speculators. One of their major policies last election was to swing the gates fully open and remove the Foreign Buyers Ban.

"It's a supply issue" - says landlord with 140 tenants.

(not even joking: https://www.stuff.co.nz/life-style/homed/housing-affordability/12462342… )

So blind he can't see that he could supply a full day of the country's demand if he sold all his properties

And the displaced would live were? - A motel/Tent - changing ownership does not change occupancy although there is anecdotal evidence that rented properties house more people than owner occupiers especially FHB's which are largely couples.

In the houses vacated by the purchasers. Almost zero sum

https://d39d3mj7qio96p.cloudfront.net/media/documents/ER22_The_New_Zeal…

Page 25 of the attached suggests the following. The occupancy rates on rented properties are higher because the families renting tend to be bigger. Don't get caught up in the idea that every rental is filled to the brim of "Flat mates" and that one flat mate misses out when a greedy FHB leaves the bedrooms empty.

Household size

Larger households were more likely to be renting than were smaller households, though two-person

households were least likely to rent overall, followed by four-person households; one and threeperson households were roughly as likely to rent as five-person households (see Figure 5). For all

households with six people or more, more than half of households were renting.

If he sold them all to FHB that's potentially another 140 tenants on the street.

Many renters simply dont have the deposits or income to support the purchase of a home.

See the ASB survey which suggests things have been improving but many account holders live week to week.

Other than those living at home, you do know what a FHB was before they became a FHB?

A foreigner living overseas, Returning expat or living in employer provided accomodation (army, navy, season worker, etc, working on a fishing vessel)? Why do you ask? Most will likely come from parental dwellings.

Most first home buys are renters, you are likely to be in your thirties when you have saved enough for a deposit or are on a high enough salary to service a mortgage in Auckland.

Someone who has sufficient deposit and can service a mortgage - not all renters as you may suggest.

Sadly there's many who rent who will never be in that position. There's 22000 odd on the state house list alone.

Mate you sound like the NZ Initiative. Did you buy your calculator from them ?

Which would do what, exactly? His houses aren't empty. Selling them wouldn't be creating new supply. Are the existing tenants supposed to move out? Where do they go? If the existing tenants stay, you haven't achieved anything, just changed the ownership.

Now what this guy could / should be doing, is using his equity to build more houses and actually help the supply problem. With the government's proposals that new builds are allowed to deduct mortgage interest costs and existing houses aren't, then I imagine it's likely he will set about doing this.

Edit: Snap!

hmm, still can solve monopoly issue I guess? At the moment, he owns probably between 40-50 properties. He could easily monopoly the market depends where these properties are. If he sells these houses to FBHs or lower leveraged investors, the rent prices for these properties will match market value more.

Building new is a bad idea. If you end up needing to exit the market you’ll have to sell at a loss because whoever buys the property off you can’t expense their interest cost. This means the property will be worth less to them than it is to you. Also how long is a new build new? When does the exception stop applying?

Yeah, It's laughable that landlord came out and give his views on this. He could've talked about any other issues, but instead, he chose to talk about supply issue.

COH

Pity more on this site didn't talk about supply issues - one of the key house price drivers, rent drivers and also currently resulting in a considerable social issue. A need to look beyond self-interest.

Printer8

I would love to see more discussion on supply issues too. Personally, I don't think just building more houses will solve the supply issue. At least not for short term, we would be lucky if the supply can catch up within 5 years. Part of the reason is that most FHBs are already locked out of the property market because of the housing price. The extra supplies would most likely be snapped up by investors. Not even mention about our far lagged behind infrastructure development. So something has to be done from the demand side. A lot of things can happen in 5 years. We can't afford to let a hard correction happen.

COH

Agreed.

Personally after KiwiBuild I am not confident in Governments announcement. It seems a significant part is providing local councils with capital for infrastructure development and at best this is going to very time consuming.

One landlord kicking out a tenant family and selling to a FHB is desirable - but the net affect is not addressing one additional home for those currently in motel units.

If investors greatly outnumber FHB's, it's not a supply issue. Build-to-rent instead build-to-live-in is the issue.

Yay, someone talking rent controls in MSM - and MSM even printing it!

Until the govt solves the issue of supply and allow other better options for folks to invest their savings, I don't see it happening - especially with all the large amounts of liquidity being pumped into Global economies.

- If cash is left in the bank, it's accruing less than 1% interest. No one will accept those yields.

- No international travel, therefore can't spend savings on travel.

- Not everyone wants to spend their money on domestic goods/purchaes (i.e. luxury items, etc.).

- Not everyone wants to invest in an all-time high stock market.

So where does a sound investor put their money to get a good yield?

In an all-time high property market? The everything bubble

The government's changes have effectively reduced the yield on an Auckland rental property to that of a term deposit, kind of making it no longer worth it considering the risk involved.

Zach...good isn't it. Now more FHBs might actually be able to achieve their hopes and dreams and if that comes at a cost to investors then that is just an added bonus.

Yes, believe it or not, I think it is good. I was able to give my wife a very good reason not to buy which was a great relief. If even I, a long time so called spruiker here, was aghast and concerned at what was happening that must tell us something.

Zach... I have been married for 15 years and have never had a joint account or shared money with a partner (although I do pay all the bills). It saves time spent debating (educating them on) financial decisions. And that way I can lose thousands of dollars in a card game and not feel any guilt about half of it being her money. And she can send as much of her money to her Mum and buy as many pairs of shoes as she wants without annoying me. Never understood why more couple do not have separate money.

Kids?

Two kids, and I pay everything for them too. But the upshot of that is I have been in my new house for a year and still don't know how to use the oven, washing machine or turn on the dishwasher. It is a good trade off. And I have the NZs insanely investor friendly rules and tax laws to thank for my lazy, comfy lifestyle. Time to stop this country producing any more me. People should have to work for a living.

Haha at least you're not delusional.

Thai wife?

ER...Yes. One of the few foreigners, I think, who managed to marry an educated Bangkok Thai from a well off family. Luckily for NZ her parents, sister and "brother" (Thai boyfriend) don't all want to migrate here as well. I think it was you I sent a reply to about Kurt's son doing some (monkey) business with my wife in Thailand? If it was you, thanks, you brought back some great memories of The Oriental and especially of Kurt. Best place I ever worked. If NZ had people with his skills running the place we wouldn't be in this housing mess. Kurt is a real champion of the poor (and was a big red shirt supporter), another thing we shared in common.

Karl. Thais are very good at playing the long game. A Cambo lady sets out to secure your mobile phone, a Thai lady sets out to get her hands on your house. I have an Asian wife and the in-laws seem to enjoy talking about my life expectancy.

KK...yes I know. I have been with my wife 20 years and when we moved to NZ I contemplated asking her to sign a pre nup but felt after 20 years it would have been a bit rough. Although I pay the bills, the only money I have ever given her family was for my wedding as is tradition. None of her family have ever asked for anything and regularly buy stuff for my kids. Her Mum used to bring dinner for me and the family several times a week and never accepted money. I used to borrow their cars. My wife worked at London School of Medicine in Bangkok and was paid in pounds. She earnt a lot but I don't even know how much. I only became aware she was paid in pounds when Brexit happened and the pound crashed.

I have seen enough of other Westerner/Asian relationships to know I have been exceptionally lucky. My two best mates have literally lost millions to their (multiple) Asian partners. The Thais are in a class of their own for charming money from us. The money goes from the Western man to the Thai girlfriend to the "brother" (Thai boyfriend/husband) and then to a different, younger Thai girl. Amazing Thailand. The advice I give anybody looking for love in SEA; pay by the hour. But good luck to you Keith. The odd person does beat the odds. Just be careful of "food poisoning " and "jumping " off Thai balconies.

Karl at the moment I am in the fortunate position that my wife's future net worth increases the longer I am alive. I'm receiving a private pension which is more than how much the household expenditure would reduce if I was taken out. I tell my wife I am worth more to her alive than not. And congrats on beating the odds on the thai honey trap. You can argue you made your own luck.

Just curious how your Bangkok Thai wife copes in New Plymouth. I ask this because mine (yep, I also have a Thai wife from Bangkok) finds Napier much too quiet and boring. We actually considered New Plymouth and went there for a couple of days and a look around when we first moved back to NZ but eventually settled on Napier.

Most Thais find the Anglo Saxon lifestyle boring. I knew many Thai women in London who had married English husbands. They mostly found the idea of going to work coming home cooking dinner and then watching the telly a dull lifestyle. Thailand was much more socialising, snacking and laughing

KK.. true Keith. Also a number of these women do come from, shall we say exciting occupations, back in Thailand so they must find it extra boring. Imagine moving from Pattaya to Wanganui for example. Often Thais have the impression that foreign countries are a paradise and then get back somewhere like the UK, into a very small, cold home, a husband away working all the time, no spare money, nothing to do and awful food. Not to mention, often a way older husband they share little in common with and I can see why most relationships do not last.

Karl the lousy UK food thing is overstated. There is far more variety in Tesco than Countdown and cheap restaurant food is far better in the UK than here. The exception is most fish and chip shops in the UK remain dreadful. The way older husband thing has played out to there now being a significant number of Thai widows in the UK sitting in 100% mortgage free houses. They are looking for new husbands but can spot gold-diggers a mile off. I dated one for a while and but we always ended up in my house as she was confident her late husbands ghost was still loitering in her/his house. The girls in Pattaya only cook if they really want to. So cheap to eat outside. It is a shock when they move to the west and discover no one eats out every day.

ER...Yes my wife does miss Thailand especially her family, friends and her good job. We have early teenage kids and we both moved back here because Bangkok is not a place to raise kids IMO and as you know, in Thai culture everything revolves around the kids. My wife spends a ton of time on social media and video calls with family so I guess that helps. She runs for hours every day and has just started a FT job so has no real friends here at all. There is quite a big Asian community here now with some Thais and Thai restaurants. My grandmother was from Napier and from what I saw it is not dissimilar to NP.

I think most Thais struggle to come to terms with the quiet boring lifestyle of a NZ town when they are used to the hussle and bustle of Bangkok. I can understand that as I do too. Being away from friends and especially family hangs heavy on most. And if we are brutally honest most Thai wives get sick of us as well. My wife will no doubt be pleased to see the back of me once I have the jab and bugger off to Vegas for a few months and leave her in peace. If you do decide on a change I would recommend NP. It is a beautiful place with friendly people. Good luck.

Thanks for the thoughts and the perspective. We'll probably move back to Bangkok at some point. Just got a few projects to work through here first and then we'll look at the logistics of getting back there. A couple of years away until that happens, at a guess.

Are their hopes and dreams actually to own a house, or simply participate in capital gains? I wonder how many desperate FHB's will consider renting to be fine once they see a sharp correction

"Until the govt solves the issue of supply" you say, then you list things related to demand. It's a demand issue, pure and simple, as the rest of your comment points it out. There are enough houses for everyone currently in NZ.

... there are not enough houses ... only Ashley Church peddles that malarkey .... we've allowed 300 000 of net immigration to NZ in the past decade ... not built anywhere near enough new houses to cope with this influx ...

Unfortunately the 2018 census made a total balls up of getting useful information on household density and ownership.

Shortage calculations rest on estimates of household density because people divide the pop of NZ or Auckland by the estimated persons per household , which varies hugely by suburb and by demography. use 3 people per hh and you get an entirely different shortage figure than if you use 2.3.

When people come out with shortage figs, they rarely explain where they got them or the method used.

Mike

A count of "homeless" in motels is a good start.

Gummy..build the extra homes we need. Have them ready for our migrants and then ONLY THEN allow them the privilege of coming here. You do not start to dig the hangi pit after all the guests have arrived!

Condition of visa - build a house to live in. LOL

Whatwillhappen...Not a joke, A great idea. And build it outside Auckland. Or if we have too many visa applicants build two or three houses to live here. And with 8 billion people in the world surely we can find single essential workers without dependent children or parents wanting to join them in NZ. We should accept migrants strictly on terms that benefit NZ to the fullest degree (with the exception of 1500 refugees as per our UN obligations, which will likely be at least 150 000 PA if Jacinda becomes UN Sec General).

Absolutely. Every single one of those relates to an inability to accept low yields, rather than anything related to the physical supply of housing.

Most of buyers these days wont be able to pay cash, that means they will take more mortgage. This means they will need a good cash flow to service the mortgage. The list you've made above doesn't require people to take debt. Most people will still need to consider whether it's worth to take more mortgage or not.

Put your money in low fees index funds, this provides a hedge against inflation & a small ROI. Or invest in commercial property. Let residential houses become homes for NZ families again.

Good question. 1% TD interest doesn't work.

Is risk-free profit a human right?

There are actual physical resource limits; what if the world can't 'afford' to promise you, or anyone else, an ever-growing share of those resources?

No risk-free profit isn't a human right. I've taken risks and saved, saved very hard indeed and gone without a lot. I have never owned a rental, but have worked hard to pay off my mortgage and put enough in the bank to supplement my retirement. These days, the interest earned has helped towards things like dental bills, medical insurance, car repairs, not champagne or meals out.

Great post 7jai, if only there were more intelligent posts like yours and less "screw that people that are not like me" posts

Gross yields are typically 2-4% in Auckland, so not great but yes better than TDs.

But net benefits will be significantly affected by this week's changes. Although not for new builds, which is good

What a terrible post. You seem to forget that housing in New Zealand's main purpose is to HOUSE people. Its not the stock market. 60% of New Zealanders believe the housing crisis is the most important issue facing New Zealand, so the rightly, the government is responding to that concern.

An Investors "right" to speculate on the housing market doesn't supercede the basic human right to safe and affordable housing.

Such a selfish point of view Miguel!!!

Just kidding, but there are people on this site who really think that the idea to provide the working class with the hope that they might one day own their own home is selfish and based in jealousy.

Not just 'working class'. Also increasingly middle class.

Mom & Dads...

A business. This is the point. Growing the productive sector. If this is too risky for you then accept the fact that you will not make money from your money.

The risk, he says is that no government, or central bank, has ever been able to fine tune an asset market so the balance of risk is that a decent correction in prices occurs..

Unrestrained bank lending for non-GDP qualifying residential property speculation, to the few, inevitably gives way to bursting asset bubbles.

What defines a bubble is that investors drive valuations higher without simultaneously adjusting expectations for returns lower. That is, investors extrapolate past returns based on price behavior, even though those expectations are inconsistent with the returns that would equate price with discounted cash flows. The defining feature of a bubble is inconsistency between expected returns based on price behavior and expected returns based on valuations.

“As long as investors focus on year-to-year returns and not discounted cash flow calculations, the bubble can continue to grow in self-reinforcing fashion. Investors anticipate a high return, and the price behavior reinforces the expectation. The true long-term return becomes increasingly detached from the long-term return imagined by investors, and the bubble component accounts for an increasingly large proportion of the total price.” Link

Why was the state regulator absent or otherwise pre-occupied?

I commend the Government for finally actually doing something. More needs to be done, but finally its a start. I think they've striked the right balance as Property Industry furious, people on the left say they could go further so seems to be a good start.

Its a good step in the right direction. Realistically the problem needs to tackled though several sets of initiatives over 10 or so years. To do everything at once will crash the market.

The market needs to be crashed.

The best deal is when both the seller and the buyer feel like they've been mugged.

Looking at the respective area under the curve one could argue that new dwelling consents have outpaced new dwellings needed significantly over that time period?

Makes for a refreshing break from 'pillaging the next three decades of our children's earnings as they try to establish a life of their own', don't you think?

When I see them remove interst only loans on buying existing houses (not new builds) and remove the ability to use equity buying another house I'll believe it.

Until then. Meh.

Action by Government was appropriate in everyone's interest.

Besides affordability issues, current price increases were unsustainable posing increasing risk not only to housing but the wider economy. It was apparent that the market was not going to act as a brake and RBNZ seemingly has not so far taken action other than LVRs due to their priorities.

I think most can live with a flat market and even some minor correction and to most a lack of capital gain in the short to medium should not have been unexpected.

For FHB it is primarily about a home, not an investment.

For investors it should always be about yield and being cash flow positive, so even with loss of tax advantage, their return should still be positive.

I have no sympathy for negatively geared speculators who were relying on capital gains - their motive was simply speculative and in this case it hasn't paid off.

P8...if things get bad and some of the speculators go under it isn't a big problem. Many of the richest 1% have been bankrupted before so if any of these people have genuine business talent they will bounce back from bankruptcy by being profitable and productive in a real (non harmful) business that does not suck the life blood out of the poor people of NZ.

What happened yesterday is exactly why I have been warning about diversification, leverage, prudence and and overconfidence in peoples ability to predict the future especially when those predictions are solely based on what happened in the last (tiny time frame of) 40 years.

Yesterdays announcements are a good start, but they are only a start. We have won round one of a ten round fight. The RBNZ MUST announce a stop to interest only loans as they slant the playing field away from FHBs and hugely increase the risk to our banking system and even our whole financial system. We also need to see some measures to peg rent rises to wage rises so the poor are not the ones most negatively impacted again. And the LVRs that will be in effect in May must remain for years to come and prohibitive tax on unoccupied houses and Air B n Bs in urban areas needs to be introduced.

And of course, mass immigration, which remains a huge barrier to providing houses at affordable prices and rents must be completely overhauled.

If these measures are undertaken, by the end of round ten, all judges will declare that we have won by unanimous decision.

karl

I agree with your sentiment, however supply is a considerable issue and all things that you suggest and Government action are going to cool the market but are not going to provide one more single house in the short term.

Currently, figures released the other day show that here in the HB house prices are up 30% and the drivers are low interest rates and a housing shortage with 1500 to 1700 "homeless" (over one percent of our population) are in motel units. Rent freezes, banning interest only loans etc may be needed but it is still not going to address a key underlying issue of supply.

Although the issue of supply may be severe here in HB, we are not unique.

We aren't out of the woods yet simply by tampering with price factors.

P8.. I agree that pegging rent rises to wage rises and banning interest only loans will not increase supply. I would love to see us build mega houses, enough for everyone (immigrants and all) but I just do not think we can do it. It would be very very difficult if not impossible. So pegging rent and banning interest only need to happen to get more FHBs into their own home and if they were done it would.

However, freeing up unoccupied homes and Air B n Bs (in urban areas through prohibitive sin taxes) would certainly increase supply. How much is debatable but it would help and where is the harm? And the elephant in the room is immigration. If we could go back in time and take measures to ensure our immigration had not exceeded, say 10 000 PA then can't you see that there would be enough homes for kiwis and our people would not need to live in motels, cars and garages? Mass immigration has meant we have allowed our population to increase by 50% in the last 30 years and each and every one of those 2 million people makes it more difficult to address the supply side of things.

We can't, of course, go back in time and fix our mistakes but we need to learn from them and not repeat them.

Well said P8

Why do any media outlets even bother to print the rubbish that spews forth from groups like the NZPIF. Some of the twisted garbage that has come from them in the last 24 hours (and amazingly been given space in the MSM) makes groups like One Roof seem balanced and rational. If they insist on printing this rubbish, please at least label it as advertising. Joseph Goebbels would be proud.

the loudest voices are the most interesting, I'd say. But I do find it frustrating that they won't match the investor commentary with something at least neutral or potentially anti-investor. There has to be some massive echo chambers of investors yelling at each other at the moment where they don't realize that some significant % of NZ just wants lower prices, and wants the investor game to be harder.

Simon... there are many, including me, that would take the other (sensible humane) side and write about their views for nothing. I would probably pay $10K to debate Ashley on the property crisis on national TV.

Karl S - are you related to Joe - (Stalin or Biden)? either would be proud of you.

Rumpole..totally a-political old chap. I might even have less respect for Biden (esp if you lump him with Harris) than for Trump, although it is a close call. And Stalin was a far bigger villain than Hitler, although of course you are anti-semetic if you point out that fact. Why do you not spend the time (trying to) sensibly refute my points rather than make childish insinuations? Judging by your posts you are far too grown up (I am going with over 75) to revert to that. Please post something of substance or go back to your reruns of Coro.

Karl - The political aspect is the historical facts and they remain facts that you may prefer to ignore or dispute. I respect your opinion and hope you are right as it will benefit me more than a repeat of history but right now my money is on a repeat as global debt is beyond repayment - even NZ which is well placed compared to others is borrowing $128 Million a day - https://www.debtclock.nz - which is $45 Billion a year. I may not live long enough to see a final result but with age comes experience and judgement, if you are right I will be delighted for you to me you told me so and i can treat you to a beer to celebrate, if I am right your generation will be the one paying the bill. I do wish you well for at least being interested enough to express an opinion.

rumpole... not sure exactly what you mean about historical facts but I also wish you the best. For the record I am not young either (over 50) and also agree that our QE and debt will be our downfall. I am very negative about it, but that is another topic. I just hope the (so called) experts know what they are doing. I started to read the (most popular) book on MMT recently but it is so boring and hard to understand that I gave up but will make the effort at some stage. Interesting times and good to hear everyones opinions.

A bit of maths. if prices have risen 17% pa for last year in Auckland and then fall 17%, how much in value terms, have they in fact fallen over the period it takes from the beginning of that 12m to when they have (if they do) fallen 17%??

A quick stab: 17% up if median in Auckland a year ago was $930k = 1.088m

17% down from there would be: 1.088 - 17% = $903k

This is highly improbable and even 10% unlikely. If it is a drop of 10% then that only take price median in Auckland back to $979k

Interest rate rises are only thing that will do anything to prices.

Also, how long are we told that this price drop will take?

Best guess remains that prices will continue to rise til year end, but that rise will. moderate per quarter.

Meanwhile sales as a % of stock will continue to fall as prices unaffordable

I notice NO political is prepared to actually state what they consider affordable price for a house for a median earner in Auckland or NZ in general.

In terms of DTI, NOT payments as a % of income, drop in which is now ending.

I do find it amusing to see quite Right wing folk slagging a Labour government for not solving supply issue.

Oil way of gov doing so, is for IT to build the houses needed and commandeer the land to put them on.

is this really what loyal readers of interest want??

I do. But not what I expect.

Gov remains resolutely non interventionist at sharp end I am afraid

Yes hilarious. National had a long time to address the supply side, and had very little to show for it. People slag Labour for working groups but Nats did it too, 2 or 3 reports of the Productivity Commission that were hardly acted on at all.

I don't want the government to build houses. They have proven to be grossly incompetent in that area (like most things they do).

What I expect is for them to do is stop artificially constraining what can be built and where to the extreme degree they do. Get quicker at consents or outsource the process. Zone land (if you must..) for more building.

Look at this shopping list of bureaucracy:

https://www.aucklandcouncil.govt.nz/building-and-consents/building-cons…

Sure it will affect house prices for a short time, but will up swing again, the next move the government will make AFTER the next election, A CAPITAL GAINS TAX on more than one property, they will find an excuse, then after the NEXT election, capital gains on certain family homes at a high value at FIRST, then the rest. WHAT they have always wanted for quite a while. This is will affect ALL home owners eventually

Good, it should have been applied to all homes equally from the very start.

Lots of taxes increasing. Not many (=none) taxes decreasing. Surely with all this new-found money from non-deductible interest there should be income tax cuts offered.

Toplis is a well known for his DGM bias and his scary views had somehow wane on me throughout the years.

However, any views that gives hope to FHBs are good isn't it?

Even the ex RBNZ governor had to tell him to toe his extreme views, https://www.nbr.co.nz/article/wheeler-calls-bnz-boss-rein-top-economist…

The only way to crash the market is to accept a major collateral damage with the common folk on the street as the expenditure.

The collateral damage of the status quo is the common folk on the street. Investors, who have been pillaging the future earnings of the country through spiking house values suddenly using them as human shields is a thing of beauty, it really is.

GV, "human shields", "pillaging" - listen to yourself! I am 100% in favour of bringing the housing market under control. I can split hairs over this Governments interventions but they have actually done something which has to be applauded. If we are to see more economic activity like this then we need to stop using spiteful and aggressive narratives that will just blunt the effectiveness of the message.

The government also needs to find a new home for people with savings to direct their dollars that will help not hurt the fabric of our society. KiwiSaver locks you in - shares are viable for some but not all of a retirement strategy. In the UK there were ISA's, TESA'a and other state backed investment opportunities that directed money into funds that supported constructive investment. NZ over serial governments has failed the part of the population that had savings and so our elected officials must collectively take some of the blame for allowing property to become the only show in town. Blaming people who have been left little choice of how to invest their money is disingenuous.

"Little choice"? Using an app on the computer that lives in my pocket, I can buy, sell and trade in funds, shares, cryptos - you name it - all over the world. It has literally never been easier to invest money in anything but housing.

And yes, I will blame people who think they are entitled to tax-free gains underwritten by the government's extensive social programmes and then expecting my generation to pay insane amounts for dilapidated housing stock, dislocated from employment centres because those same people have managed to restrict development in their own suburbs to the point where the entire city is a congested mess.

Sorry, some of us have had enough of being told we didn't work hard enough, or we needed to put off having kids until later or perhaps at all if we wanted to own a house. The chickens are coming home to roost. Don't sit there and act like Kiwis had a gun put to their head and were forced to use high leverage to speculate in residential property.

Well said. The sheer entitlement is astonishing. Property investors have been creaming it courtesy of the government. Now that particular gravy train had been very slightly moderated, the government is supposed to provide some other avenue for investment? Bloody hell. I guess that kind of attitude is what happens when one generation gets used to having everything go their way at the expense of everyone else for so long.

Do you not agree harnessing the money that Kiwi's have saved in ventures that help society rather than hinder it is a good thing? A debate rather than a character assassination is what I was looking for.

Yes, its a good thing - but its a good thing that benefits one sector of society in particular, and a sector of society that, for decades, has been pushing the line 'whats good for us is good for society, so we need policy after policy that shovels more and more wealth our way'.

Its a question of priorities. There are plenty of good things the government could do that would benefit society in general, but particular individuals as well (like building state housing, for example). Providing investment opportunities for property investors upset that the goose that has given them golden eggs for a while has downgraded to silver is at the bottom of the list.

And if i sound angry, its because I am. For many people in my position, our experience of adulthood has been repeatedly being told that we can't have the things our predecessors have because its 'good for society' that education isnt free, that wages haven't budged in real terms for years, and that house prices kept spiralling up. Too bad we cant afford basic stable housing for our families - its more important 'for society' that boomers are able to put another holiday or a boat on the mortgage. Thats why the 'more handouts for the already wealthy - its good for society' argument cause (justifiable) irritation.

Points well made - I wish you and your family well going forward,

The investments you describe are not compatible with a balanced portfolio, as I mentioned, but I agree they are available. Again, you use language which is inflammatory and not constructive "I will blame people who think they are entitled to tax-free gains". I have a super annotation scheme that gives me a tax break on contributions, I can claim tax relief on the cost of leasing my car as it is through a business. I could go on. Tax incentives are in the fabric of our financial system and I have never felt entitled to them, just as investors in property are utilising a similar opportunity and I'm guessing also don't feel entitled. Blaming someone for taking advantage of any of these is naive.

Make an argument, back it up and be constructive. Opinion and blame get us no further forward to sorting this out. If you'd have said that you believe that the sale of second homes should be taxable and the new changes are overdue then we have a discussion on our hands. You are very hard to agree with even when we agree!

Sorry, indexed funds, shares and so on are not part of a balanced portfolio? How is having the country going all in on residential property, at the expense of low income earners and first home buyers better, in that regard?

And frankly, expecting people to be civil after the real, monetary and life-changing costs rampant speculation has had on people is rich. In years gone by, concerns about house prices escalating have been met with snark and derision about iPhones, avocados on toast, flat whites and other such ridiculous derisive commentary. Now the shoe is on the other hand and everyone has to be civil and constructive all of a sudden.

Common folk on the street are the "expenditure" of the situation as it is, basically traumatized from not being able to afford a home.

Can the government please get a deposit guarantee scheme in place before it goes attacking bank equity.

fatpat..aren't they trying to provide more security to the banking system by ensuring they hold more capital?

Is it just me or from my rudimentary calculations. About 22-25% has been wiped off the value of Auckland houses?

If the major driver of price growth has been investors. Does that mean the calculation to service the mortgage will recalibrate the values that can be lent? This is the main driver of value in the say low price to $950k / $1m even if before it wasn’t cashflow positive. Now it’s a big expense liability.

Thoughts?

I may be able to answer this soon. Last Saturday I visited the bank to get a pre approved mortgage value. I haven't received it yet. Will what I receive be different to what they suggested it would be on Saturday? I suspect so because my expenses would now be considerably increased. I reckon the figure will drop from 600k to around 450k that they are willing to lend.

Hi Zach, I think in the past you have posted something along the line of "should have listened to Yvil". Well if you care, by all means get your mortgage approval, then spend a lot of time looking for a house in the area you're interested in, don't rush. I think the stock of houses is about to increase which will give you choice, something a buyer hasn't had for a while. It'll allow you to negotiate, also something that has been very hard to do for buyers. Be patient and good luck!

Did you listen to yourself, Yvil? Have you bought some more investment properties in the last couple of years?

I agree with everything written here about pressures on the market but how it balances out is unclear. I believe current investors may be more circumspect than is forecast and may not "rush to market". The recent investors (1-3) years may well hang on for the BL test to be satisfied. Those 4-5 years since purchase are, I believe, the most likely to sell but may be comfortable sitting on a lot of equity and seeing how things play out as there is not immediate rush given the timeline fo the tax changes. Investors over 5 years may be very happy as interest on loans will be small and so the tax changes are less of a push factor for them. Certainly the re-opening of borders with immigration coming on line may be enough of a ? to stay in for now. It's pure speculation on my part.

There could well be more FHB's at sales now, some returning after getting fatigued by investors and the OCR is still very low which we know is a bottom line for spurring people to borrow.

The only thing I am confident about is that the number of investors at sales from here on in will be much lower. Will that curb interest enough for each property? You need only need two buyers to push up prices, the dollar doesn't mind if they are FHB's or investors.

I wonder if we will see a drop in sales, a big drop. Investors not selling in the numbers forecast and purchasers not buying because there is the risk of a correction and negative equity so a kind of stale mate. So very difficult to know.

If I were a recent purchaser I would definitely hang on to get past 5 years BLT AND to get the benefit of still being able to deduct part of interest payments in the short term - something the potential buyer would not have access to .

That would be dumb. The smart selling will start now to beat the downside risk.

I think true investor stock will fall - apartments, tiny town houses etc will tumble. People will consolidate and sell their rentals and pour that cash into upgrading their family home. Also a holiday home has lost attraction unless you are 100% certain you will keep it for ten years. I think quality family homes with some land (500sqm+) in good areas will hold their value or continue to increase.

JJS - you are right because you reflect human reaction and will create work for builders, do nothing to improve housing supply indeed it may decrease if house builders transfer to more profitable home improvements, As usual 99% of economists are wrong 99% of the time and socialist govts 100% - show me a successful prosperous and happy socialist state/population and I will vote Labour next time.

Have you been to Europe / Scandinavia?

Ha ha yeah, another right wing idiot. Most of the Scandanavian countries are successful and happy.

just for the sake of it. Hahaha another left wing idiot. Scandinavia has totally different historical back ground and culture. Different resources. Lot's of Scandinavia aren't so happy with leftist lunacy, not happy about immigration and the changes their society . See we can both be snarky and opinionated.

Nope.

The difference is I can lean on evidence, you can't.

Look at the recent 'happiness surveys pal, top 10 dominated by Scandanavian countries. They are pretty strong economies too.

And different culture has nothing to do with it. You equated left wing to misery. Wrong!

Go back to your right wing echo chamber.

They'll just go back to higher yield investment properties. This policy is going to screw renters.

BMM

Not sure how you arrived at 22-25% value of Auckland wiped off the market.

My thoughts?

I am watching and waiting to see.

This time last year many posters jumped in and were making dire predictions of 30 to 50% falls that proved to be not the case - in part because they didn't factor in RBNZ actions.

I was watching and waiting last year, and I'm doing the same again this year - although I wouldn't be too cocksure and put money on a significant capital gain :)

There is much uncertainty, for example:

- What is RBNZ is going to announce in May and for the same reasons they allowed house prices to inflate, they are not going to want to see them crash, and

- Just what will many investors going to do? I think that many are over estimating the numbers that will bail out as those who purchased more than five years ago will be getting very good yields on their initial investment and ride out short term market fluctuations and those who purchased in the last three years of so may be holding in there to see out the current Brightline requirements.

N.B. Yeah, RBNZ got it wrong last year expecting a 10% drop, but they weren't as extreme as the consensus on this site, and it is proof that even the experts don't always get it right even of they can influence the outcome.

Yes but those commentators at least jumped off the fence and made a prediction? It's fine to sit on the fence and take a "watching and waiting" approach but you can't then lambast people for actually giving their opinion on the direction of house prices that turn out to be incorrect.

Albert

I think that indicators (such as auction results) over the next few weeks or so and especially knowing what RBNZ actions are in response will provide some indication and a better basis for making a sound assessment for the future.

Anyone currently claiming what is going to happen to housing really is just guessing not knowing how the market or RBNZ will react - so yes, worth of being critical. As in many situations it is well worth standing back and assessing the situation rather than foolishly rushing in. A one-line unsubstantiated claim as was common last year really was guessing.

P.S. October 2020 I was posting that the then increases were not sustainable and that the market due to affordability issues was likely to be flattish from this year for sometime with possibility of some minor correction. I still stand by that at the moment, however I thought that the market would self-regulate itself rather than the Government having to step in.

That's a great graph summed up by what I have been saying for a while:

"But over the last twelve months we have been building far more houses than are needed to cope with the population’s expansion. Indeed, right here and now, we are probably building one new dwelling for every one person increase in population. This is clearly not sustainable."

It could have been that we were already going to see some over supply price drops, particularly if unconventional monetary policy wound up (which I think is highly unlikely). The distortions added by the government around COVID though have just injected money into a system that is designed to flow money into residential housing. Hence prices boomed.

It is possible we are in for a collapse of similar proportions given the pin prick Labour just gave the market, I guess time will tell...

Bloobles

Please review the graph - building consents and forecasts are not built houses and even if all the consents get built eventually as the industry appears to have a capacity of 25/30,000 a year even this may not be achieved more so if ex Landlords employ their capital and use ex house builders for more profitable home improvements.

I hope we have messaged our govt MP's and said well done....great start, now keep going. Nothing like feedback and an uplift in the polls to motivate our elected officials.

National still don't get it.

National are literally stuck in the 1990's. They have not changed with the times.

Labour have yet to move past 1972.

Agreed. I believe that the Reserve Bank needs to ban interest only loans (in May), but I feel better for young savers looking for homes. Well done.

EdwardD - I'm genuinely interested in why you have described interest only loans as being a significant factor. Would you mind replying I'd be grateful.

here's a video that shows why interest only loans allow investors to continue when the numbers don't dd up

"The Government is, in large part, staking its credibility on this and cannot be seen to fail."

Hilarious.

Unsurprisingly the Bank economist is now suddenly warning about "over construction" warning that "prices might fall". Jesus christ, that isn't something to "warn" about - it NEEDS to happen.

Not just because 70% of FHB require outside help to get together a deposit, but just to short-circuit the insane belief in NZ that prices can only go up, so just invest everything in property at any price - don't worry if the yield is negative, the capital gains will cover that.

The obvious risk is that an orderly decline becomes a disorderly one - but that is why we shouldn't have allowed an asset bubble to form in the first, not a justification for doing nothing now.

It's amazing how suddenly there's an oversupply. All it took for thousands of homes to appear was a proposed change to tax laws, who knew it was so easy?

To be fair, I rate Toplis much higher than most. Much more balanced than most.

Tony Alexander puts the end of interest tax deductibility for investors in perspective, the best way to look at it he says, is that basically the interest rate for investors has gone up by 30% (= the tax rate). So if an owner occupier borrows at say 2.49%, the same rate will cost the investor 3.24%. This allows a simple calculation for the investor to see if a purchase or even an existing investment is still worthwhile.

What about increased downside capital price risk?

The impact is quite negligible from the investment perspective within the context of the country's economy.

What about it Audaxes? Can you calculate it as accurately as T Alexander? No

Yvil...as a former property investor I was almost completely unconcerned with the month to month calculations. As long as you are able to pay the shortfall why would you pay any attention to it when each investment property is sometimes increasing by up to $100 000 in one month?

Karl, from your multiple previous landlord bashing comments, it's extremely hard to believe you were one of them

Yvil..I guess I am like the born again christian or the recovering alcoholic, always more vocal, pious and sanctimonious than everyone else about succumbing to life's evils. But in all seriousness, I really was a landlord for over 25 years. And having houses in Mt Roskill and BHB most of my tenants were Indian, which may also be hard to believe.

Indians in Mt Roskill? No way

Yvil - a very valid point, the concern must be however that by targeting one sector is vindictive and other sectors unpopular with this socialist Govt may be next. Another thought - if property rental is not a business then perhaps its a hobby so not taxable at all?

Rumpole..I do not think the Govt is targeting one sector out of vindictiveness. They are trying to create a system where the average person can afford a home in their place of birth. When something is doing so much damage to the fabric of society it needs to be targeted and it is nothing to do with being vindictive.

It will only take a slight flinch of sentiment change from the RBNZ for the retail banks to immediately add in 75 bps in rate increases.

The other thing that is in the back of my mind is - what if under the new calcs the banks can’t justify offering fixed rates to a mortgage holder.. imagine being stuck in floating rate purgatory.

BNZ economists say the Government is 'dead set' on curtailing house prices and will do what it takes - 'it will almost certainly win in the end'

Hi David,

1 : Will it be good or bad, if the government win in the end.

2 : Is it not, just shouting kicking - throwing Tantrums, fear Mongering to put pressure on government to stop it from taking any meaningful action like the pending action of DTI and on Interest Only Loan ( which is clear that is must to put brake on speculative funding and no one can deny it)

Wished FHB had such a strong representation lobbying as is evident from the voices that by just one action are so disturbed and frustrated.......they were no where to be seen or heard, when house prices rose by $100000 in a month - not to forget that even if house price we're to falls by 5% or 10% or even 15% - it will still end on a positive note on an annual basis by 20% or 30%.

'Toplis says many investors have been investing purely for the purposes of capital gain.'

Same people who use to say that in NZ most invest for yield and long term now confessing that fast and easy tax free capital was the reason.

Just a thought / fear that house price may stabilize or fall slightly is sending shivers to all.

Expose !

alittle, good/bad are personal emotions, what is good for one person is bad for another and vice versa. If you want to see things clearly, try to see how things actually are rather than how you'd like them to be according to your opinion of what is good or bad

Agree and that is what I wanted to know, What David feels - his perception.

Yvil.. but we can decide what we believe to be good or bad for our society as a whole right? I agree, not good or bad according to us personally but how we would like them because of the positive or negative effect on our country as a collective. And IMO, our decisions needs to be firmly based on what is good for the average, struggling young kiwi in the lower quartile with complete disregard for what is good for investors.

Well I have a different opinion to the one you just stated, perfect example

Yvil..fair enough. I have always supported the underdog. Unless it is Aussie in sport. I often even want the ABs to lose, again, unless it is against Aussie

"If this set of policies fails then more will be introduced

And in that one sentence lies a problem for all the "I'm gonna put my rent up 40%!" crowd.

Go ahead....and see what happens next.

As we all learned as children:

"Don't poke it, and it won't bite you"

I've not put my rent up in the UK for almost 10 years. When I inquired about increasing rent I was reminded that there is a limit of up to 5% each year. Anyone who thinks about increasing 40% will raise interest from the tenancy tribunal. I'm sure government will introduce caps pretty soon. Other option of course is to kick out the tenant and then market 40% higher...good luck with that!

If the governments measures just end up screwing the young, renting-without-choice, study loan indebted population of NZ, what have they all got to look forward to or be grateful for from this government? It will be they who end up being forced to pay the landlord's lost tax deductions. And just where are they supposed to find that extra money?

But one thing is for sure, Ms $400,000-a year Jacinda, their memories will out-live your political career this time!

Haha. What a joke. This government/Reserve Bank's policies are mostly to blame for the recent price surge. They haven't got the guts or brains to solve the root of the problem. There's still a massive shortfall in housing. House prices will continue rising until there's an over supply of houses (not happening) or interest rates go up. The only limit to price growth will be whether incomes can support mortgage payments. People aren't just going to sell all their properties cheaply because there's a new tax. The profits and yields are still better and easier than nearly any other area of our economy. Some people actually renovate their houses to increase value rather than sitting on them too.

At the moment, artificial demand is as much of a problem as a lack of supply. This was a gutsy move by Labour (finally somebody grew the cojones!) that will remove a big chunk of investor demand. The genuine supply / demand dynamic hasn't changes since COVID - as you can see from the graph - in fact it looks like new supply is exceeding new genuine demand. Its just that thousands of Ma & Pa's have diverted their $ towards investment properties, and in doing so have utilized unfair advantages to outbid owner occupiers - in what universe is that a good thing?? Bravo Jacinda / Grant.

It's not gutsy at all. They're too fucking useless to build houses themselves so they've decided to go after people who already own property. Problem is it will only end up hurting renters.

How many Kiwibuild houses were we supposed to have by now, 30,000?

Sam..we needed to build about 40 000 extra houses just to house the 170K extra people who moved here in the 12 months prior to covid. So not even allowing for the kiwis in need of housing we just can't build enough to keep up with mass immigration.

Good identification of the underlying problem - too many migrants on top of natural population growth and insufficient capacity to build enough houses to accomodate plus restriction of land supply - solution reverse all especially land supply.

Problem is it will only end up hurting renters.

More crocodile tears please.

Ah yes, the typical landlord crybaby. Everything the govt does "will hurt renters". I dare you to raise the rent on all your properties! Good luck

I left Auckland to buy my first home only 6 months ago. I'm just a realist.

Everyone is a realist in their own mind.

They haven't got any idea what they're getting themselves into.

Who - over-leveraged property investors?

Headline : Full attack on house price.

Is it bad ?

Also is it full attack or part as still waiting to target cheap and easy money supplied to speculators through Interest only.

AND it highlights how big the ponzi is, as is so fragile that even by little....people who are involved in speculation are worried of not fall but crash that happens is a sign of hyper bubble.

will it ? more people than houses = high demand -- is supply increasing faster than population than demand - NO -- will demand continue to increase - yes borders will open immigration will restart -- people will want to live in their own homes and not share -- - and realistically we are nowhere near increasign supply to match existing demand -- target 100 000 extra in ten years above waht the market will build -- current result about 1100 in 3 1/2 years-

slow down rises maybe -- but only the infrastructure fund remotely addresses supply -- and although it sounds a big number -- who is going to build more houses and faster than we already are ? not impressive - and after a 100K rise in a month -- woo woo to the 5k increase in first home loan

All the same people saying house prices will go down now said the same thing with Covid. They were all wrong.

This is just scaremongering so government does not take other measures, which are in the pipeline just like Westpac bank threatening that will leave NZ.

Jacinda Arden will have to be very firm and show leadership qualities to not be influenced by biased vested interest.

Covid will go down..can you expand on that one please?

BNZ economists say the Government is 'dead set' on curtailing soaring house prices and will do what it takes - 'it will almost certainly win in the end'

BNZ economist says that government is trying on curtailing 10% rise on a monthly basis......IS HE COMPLAINING ......Reflects mindset of so called economist and also exposes, How they support and favour ponzi SO government has to be very careful with such economist and experts.

little, you missed out the last sentence from BNZ economist, which sums him up that for him rising house price / ponzi is good for the market.....

'.....still think the next move in rates will be up, potentially sooner and more aggressively than many believe.

"This won’t help the housing market either."

For average Kiwi and FHB, if what he mentions does happen and house price stabilise or fall will help and is good.

Can't see how those with giant loans facing rate increases is a good thing. Especially with falling equity.

It frustrates me that *Bank Economists* get so much traction in the media. These are paid spin doctors!! Let's hear from independent experts who are not directly or indirectly on the payroll of banks and corporate interests. Unfortunately there probably aren't any. This age of 'celebrity economists' is puke making, just talking heads who love the sound of their own voices being paid to postulate and waffle.

Can you name a few independent experts please

Paid experts that work for companies/banks that pay big $$$ for PR i.e. features in news articles, advertising etc. This is why you hear from them and not Joe Blogg expert down the street...

The graph can't be correct, the area beneath the yellow line but above the blue line is more than the reciprocal. My highschool calculus tells me there is no housing shortage!!!!

I guess not all BC's translate into houses but it must be high percent.

It is known that only action by rbnz on DTI and Interest Only Loan will have some affect :

https://www.stuff.co.nz/business/300261797/investors-might-pay-30-per-c…

"Smith said he expected the changes to slow house price growth but not cause an outright fall. But even a 20 per cent drop in house prices would only take the median back to where it was a year ago.

The Reserve Bank will report back in May on the potential introduction of debt-to-income ratios and limits on interest-only lending, which could make a significant difference to investor activity"

As usual readers don't look critically at what the actual words say.

What does "curtailing soaring house prices " actually mean? Does it mean that the rate of house price increases will be curtailed e.g. from 27% per annum to 15% per annum; or does it mean that prices will stay the same with no more increases; or does it mean that house prices will fall?

All we can deduce from the statement is that there will be an as yet unidentified negative effect on prices.

Well if we are to have any hope of lifting our fertility rate we need lower house prices and more people living in their own house. Who wants to start a family in a flatting renting situation, unless they have no option? Hoping we see a real significant correction here and further disincentives for specuvestors applied. A lot of people were claiming we would see lot of talk but no substance, but no; well done to Labour and their courage to do something. Let's hope we see the change in the market the average young NZer desperately needs.

As a side note I hear a lot of bellyaching on the radio about the new threshold only adding 650ish new houses in Auckland to the reach of FHBs, however this would be a rolling average would it not? So as a percentage of the bracket FHBs look in, would this not represent quite a decent increase percentage wise?

The plan is to import at least 100,000 people a year - so fertility rates are neither here nor there.

Anyone who questions the sense in bringing hundreds of thousands of people to a nation with a chronic housing crisis is Xenophobic, according to someone named Arthur Grimes.

Exactly right... my girlfriend and I (wont be getting married for that would put us further back on saving for a deposit) weve talked about this at a very deep level...

What is more important to us.. remain near all our jobs, our friends and her family here in auckland or move to a regional town and start again so we can have a child or two children - Its a bit of a gamble - will we resent our decision in order to be able to afford a stable home, have to start again with a new friendship group, any kind of child care will have to be supplied by the dollar not in kind by the grandparents - its a very sad situation but both of us being on very good wages, cannot make the money stack up to keep a mortgage alive in AK and have even a single child...

Its as much a shame for the would be grandparents that - yes you can have some grandchildren, but youll need to board a flight in order to visit them...