Summary of key points: -

- Does the building of a wall ever work?

- The things that the economists did not see coming

Over the last two years the Governor of the Reserve Bank of New Zealand (RBNZ), Adrian Orr has expressed and actioned a consistent view that a lower NZ dollar currency value will enable him to achieve the RBNZ ‘s objectives of stable inflation around 2% pa and higher employment levels through stronger economic growth.

The one-sided view is as strong post-Covid as it generally was before the world changed in March.

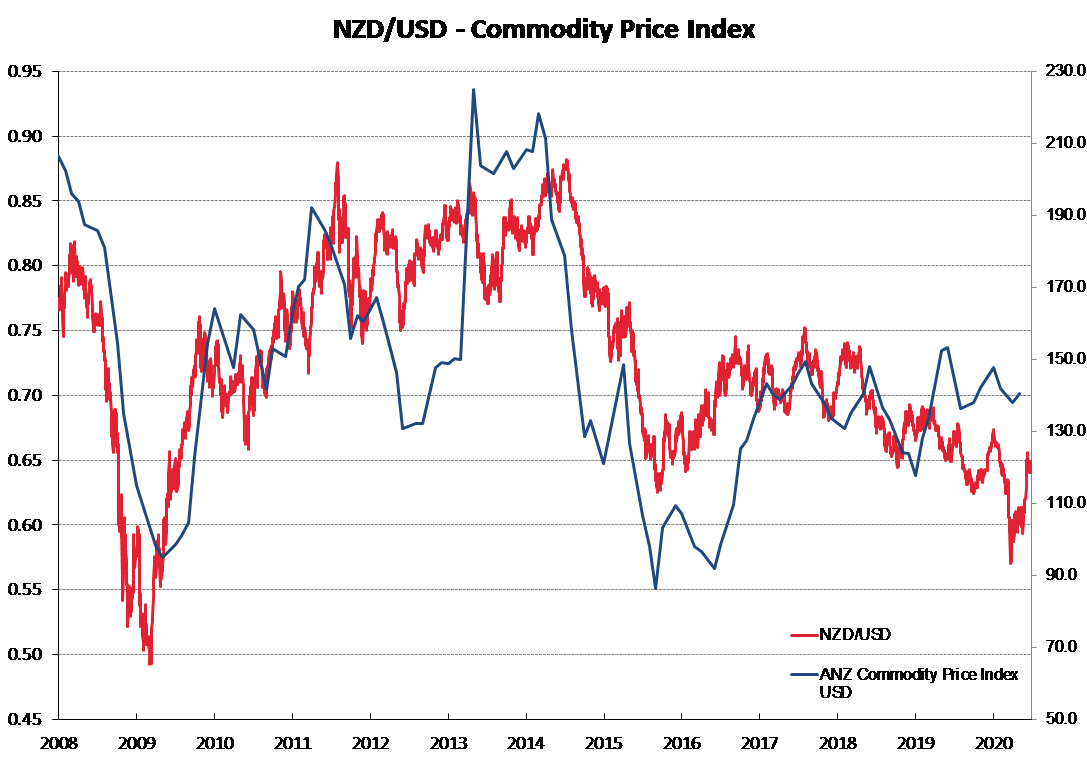

My column has well documented the results in the foreign exchange market of Governor Orr talking down the Kiwi dollar. The immediate FX market reaction is to sell the Kiwi as the RBNZ have some power to enforce a lower value through cutting interest rates, or now increasing quantitative easing. However, the Orr-inspired dips in the NZD/USD exchange rate are never too long-lasting and other greater forces in the markets soon return the Kiwi to the prior levels. Whilst the USD itself was strong on global FX markets through 2018 and 2019 due to higher interest rates than other currencies (also safe-haven USD buying due to the trade wars) and the Aussie dollar was under downward pressure due to lower interest rates, no-one questioned or challenged the RBNZ currency view as the NZD was trending down anyway.

Ahead of last week’s RBNZ Monetary Policy Review it was again widely expected that Adrian would take the opportunity to jawbone the Kiwi dollar down. He did not fail to deliver with: “The appreciation of New Zealand’s exchange rate has placed further pressure on export earnings.” However, the normal one to two cent plunge in the Kiwi following such statements has been much reduced on this occasion.

The NZD/USD rate was trading at 0.6500 before the 2pm release last Wednesday, dropped to 0.6410 by the next morning, but follow-through selling did not eventuate and it has since recovered to 0.6430. The muted response is like the boy who cried “wolf”, sing the alarm too many times that something bad is about to happen (and it doesn’t), pretty soon the punters just do not believe you. The RBNZ’s currency jawboning has lost its potency as a monetary tool or aid due to over-use.

The RBNZ’s justification for desiring a lower NZD value now seems to be that exporters are experiencing lower profit margins because the NZD/USD rate is trading at 0.6500.

The RBNZ conclusion ignores currency hedging policies and programmes that all medium to large NZ exporting companies implement and manage.

My observation currently is that our manufacturing exporters are very well hedged forward for two to three years at exchange rates between 0.6500 and 0.6000. They are profitable at these levels; however, they see the risk of a weaker US dollar on the global stage (nothing to do with NZ) potentially pushing the NZD/USD rate to 0.7000 or 0.7500. If that happened, the hedging protects business profitability and thus investment and jobs.

Primary industry commodity exporters (dairy, meat, logs, horticulture) generally do not hedge so far forward as the commodity price is more linked to the NZD/USD exchange rate (thus offsetting NZD appreciation somewhat).

Previous RBNZ Governors, such as Dr Alan Bollard always took a keen interest in the level of exporter hedging as it is was important for the RBNZ to factor this into their economic modelling. I am not so sure the current regime at the RBNZ is regularly visiting the larger exporters in provincial New Zealand to glean this important information.

Drawing an artificial line in the sand at a particular price level in the world of currencies is ultimately an ineffective strategy for anyone, including the RBNZ.

The RBNZ Governor may want to build a wall to keep the Kiwi dollar lower, (H)Adrian’s Wall?. However, like the 120 AD Roman wall across England, it was doubtful that it was that effective in keeping out invading armies and rebellious incursions. Donald Trump’s wall on the US/Mexican border has been just as ill-conceived and is really all about political propaganda to scare Americans that the Mexicans were taking their jobs. The reality is that Mexicans are required to do the largely agricultural work that most Americans are too lazy or physically incapable of doing.

Local USD exporters have found to their cost in years past that they should not rely on the RBNZ to always keep the NZ dollar value at a low level. The risk is on the other side of the currency pairing, the USD, and the RBNZ cannot control that.

The things that the economists did not see coming

More doom and gloom forecasts for the state of the future global economy from the OECD and IMF over recent weeks, however readers would be right to question the application of the normal “cause and effect” economic principles going into these projections in the current environment.

A number of current trends occurring in the New Zealand economy do not fit the conventional wisdom that we are headed for a deep recession/depression: -

- Return of the Kiwi diaspora – Last year it was estimated that one million ex-pat Kiwis were living and working overseas. The coronavirus pandemic has caused thousands to return home over recent months and that trend is set to continue. The returnees are seeking to rent and buy houses and are effectively replacing the previous demand in the property market from new immigrants. Dire predictions of plummeting house prices may prove to be widely inaccurate.

- Rising sharemarkets – The rapid rebound appears to be more and more sustainable as excess cash around the world needs to find a home that provides some return. Equity markets continue to look forward to improved economic conditions and thus improved listed company profits/valuations. Equities may be disconnected to current economic conditions, but that does not guarantee an imminent plunge.

- Booming food exports – Volumes and prices are up and exporters have had the opportunity in March to lock into great NZD/USD exchange rates below 0.6000. RBNZ forecasts of falling export commodity prices due to weaker global demand are looking a bit sick.

- CBD office ghost towns – Lockdown and working from home has convinced many professional and financial services companies (banks, insurance, CA firms etc) that employees no longer need to spend hours commuting to central city office towers. Related economic activity for restaurants, café and bars is rapidly re-locating to the suburbs, exactly what happened in Christchurch after the earthquakes. Office property as an investment asset class has major problems. The economic activity has not disappeared, just occurring at a different location. Let’s hope employers appropriately compensate workers for the cost of the home office, computers, electricity, internet etc.

- Money flow and plumbing issues with the banks – Government injections of emergency cash into the economy have been much more effective through the IRD than through the banks. The banks have tightened their credit criteria; however, business firms are very reluctant to increase debt levels despite the base interest cost being very low. Listed companies are preferring to raise new capital (and being very successful) as it is more attractive to the investors than bank deposits.

Large job layoffs in tourism, travel and some retail is inevitable and happening, however, how far the unemployment rate increases does depend on how quickly displaced workers re-deploy to industries were there is strong demand for labour. The dairy industry has 2000 job vacancies and so far they have only attracted 200 new workers into their fast-track training module.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

15 Comments

The property market is more complex than that. People are slowly returning with the quarantine limit. All the AirBnB and hotel owners are going to have to look at different or more diversified ways of generating income. Internal tourism appears to be starting to help but they may be used for longer term accommodation.

I noticed the number of houses in Wellington for sale in the $1m+ plus category has gone up a lot. Some really look like the owners dream home so the decision to sell is probably driven by loss of income. Those selling on the high end will either be looking for a lower cost home or a place to rent. This could place more pressure on the low end of the market assuming they can sell.

For exports we may have unintentionally ended up in the position for an export led recovery. Not the worst position to be in given the state of the global economy.

Current situation is filled with liquidity and many have made a small fortune out of it so is hard to ppredect what might happen once wage subsidy comes to an end and if unemployment rate is high more that 10% will adversly affect the housing market as the article abive is missing tge domino affect as not only Hospitality and Tourism along with some retails be affected but also no immigration /no International students will have advers affect.

Besides Tourist region particularly in South Island will be badly affected as no amount of domestic tourisn can replace international tourist.

Not to forget second wave as cannot be ruled out so any article/expert opinion is just a guess wirk or best calculated guess work as no one is able to undestand the role of excessive printinting by government and its overall affect.

The RBNZ should simply print its money and buy gold. Closest thing to a win-win free lunch in economics. If it works, you devalue the currency as you wanted. If it doesn't work, you get a free hard asset.

Every single dollar that the government spends is newly created on a computer keyboard at the Reserve Bank, only the NZ Government can create NZ Dollars.

Every single dollar that the government spends is newly created on a computer keyboard at the Reserve Bank, only the NZ Government can create NZ Dollars.

Money creation comes from commercial banks. This is the fundamental education NZers need.

https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/20…

Yes banks create credit (horizontal money) but only the government can create NZ currency (vertical money) which equates to commercial bank reserves and only the government can create net financial assets to finance private savings. Banks cannot create their own reserves or private sector net financial assets as the assets and liabilities they create cancel each other out. An explanation here of Sectoral Balances. https://gimms.org.uk/fact-sheets/sectoral-balances/

Yes

I would rather have the governments currency in my pocket rather than bank created credit money which I would have to pay interest on. When bank loans are repaid the money ceases to exist again, try saving that money.

The RBNZ should simply print its money and buy gold. Closest thing to a win-win free lunch in economics. If it works, you devalue the currency as you wanted. If it doesn't work, you get a free hard asset.

What about the scenario of carry trade? Was thinking about this if currencies all go into NIR territory. Borrowing in USD, NZD, etc and investing in gold and BTC.

Roger

Although there is still a high level of uncertainty remaining (e.g. locally the impact of removal of wage subsidies, the length of time before even some opening of our borders, and globally the extent of the increase in Covid) your comments are well worth noting.

The sudden escalation of the virus and even more sudden closing of our borders tend to - as in any shock - bring out a knee jerk extreme reaction.

Rather than expecting their early projections, I notice a number of respected economists now tending somewhat to slightly downgrade their earlier estimates on factors such as unemployment, fall in GDP, and housing. Your comments are consistent with this.

Personally I still feel a fairly high degree of uncertainty and am still still sitting, watching and waiting but not in a state of extreme fear.

NZD looks to be correlated to the confidence in the US share market at present. If that tanks again in the next few weeks, or months, and which there is a reasonable possibility, I don't see why the NZD won't be back in the .50's.

RBNZ talks NZD down, naive people believe and short NZD, NZD rips up, banksters win as they’ve taken the opposite trade of speculators.

Roger,

I have been a regular critic of your views on inflation, but I certainly agree with your critique of the RB's thinking on the exchange rate. Our $ is heavily traded globally and what the RB wants I largely irrelevant. To base our economic thinking on an ever lower $ is short-sighted. Companies like F&P H'Care which do almost all their business overseas and as you say, are well used to hedging. They do not base their business model on a falling NZ$, but on the competitiveness of their products.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.