Summary of key points: -

- Considerable resistance preventing the Kiwi breaking above 0.6600

- Currency speculators finally unwind short-sold NZD positions

Considerable resistance preventing the Kiwi breaking above 0.6600

At trading just under the 0.6600 level the NZD/USD exchange rate has arrived at a key cross-road juncture for its future direction.

Can it make immediate further gains above 0.6600 on the back of a weaker US dollar on global FX markets?

Or, is the more likely scenario a pullback or correction to 0.6400/0.6300 following the sharp appreciation to 0.6600 from the 0.6000 area over the last two months?

The answer hinges around how the FX markets interpret the following influencing factors and forces on the Kiwi dollar’s value: -

- The failure of the Kiwi dollar to appreciate last week when whole milk powder dairy commodity prices jumped up a staggering 14% to US$3,208/MT, indicated that the speculative interest in the currency was at a low point and no-one was interested to buy the Kiwi at a rate so close to the major technical/chart resistance point at 0.6600. In typical market conditions the Kiwi would have appreciated by up to one cent on such positive commodity price news. The absence of NZD buying on such good news was instructive, and this factor favours the pullback scenario.

- The continuing gains of listed technology stocks in US equity markets has many pundits dumbfounded about the sustainability of the recovery rally since April. The Kiwi dollar is always vulnerable to equities markets selling off and the investment world going into the “risk-off” mode. The continuing equity markets gains cannot be based on the US economy having a rapid recovery from Covid-19, as many states now consider slowing their business re-openings as the virus still spreads in the southern states. On a risk/reward balance question, the selling of equities from current levels on profit-taking would seem a higher probability than further gains. The position of US equities also supports the Kiwi pullback case.

- The Kiwi dollar has significantly out-performed the AUD against the USD over recent weeks, propelling the NZD/AUD cross-rate from 0.9240 to 0.9440 over the past month. The AUD/USD rate has pulled back from 0.7000 on several occasions as AUD buying volumes dry up on the Covid-29 second wave forcing Melbourne back into lockdown and the deteriorating diplomatic/trading relationship between Australia and their major trading partner, China. You would be hard-pressed to claim that the NZ economy is performing well ahead of Australia at this point, therefore the sharply higher NZD/AUD cross rate above 0.9400 does not seem sustainable. Profit-taking by speculators who have purchased Kiwi/sold Aussie over recent weeks, would suggest a lower NZD/AUD cross-rate and thus a lower NZD/USD rate over the short-term.

- NZ inflation data for the June quarter to be released on Thursday 16th July would on the surface suggest a weaker Kiwi dollar with consumer prices forecast to decrease by 0.4% following the higher than expected 0.8% increase in the March quarter (reducing the annual inflation rate from 2.5% to 1.6%). The RBNZ are forecasting a 0.8% drop in prices over the June quarter, however lead indicators for inflation suggest the deflation will not be as large as that. Petrol pump prices decreased approximately 10% from the March quarter to the June quarter. The transport group (which fuel prices are a part of) has a high 15% weighting in the inflation index, therefore fuel price reductions will force a negative number. The question is whether increases in food prices, rents and other non-tradable prices will offset the fuel price deflation and result in the CPI outcome being smaller than the consensus forecast of -0.4%. What we do know about current and future inflation is that technology/communication prices which have reduced materially over the last 10 years and thus generated the overall low inflation, are no longer reducing in price like they once did. (Chorus are not gaining many friends with their latest fibre network price increases). A June quarter CPI figure less the -0.4% on Thursday seems more likely than not, thus positive for the Kiwi dollar.

- The NZD/USD exchange rate has consistently remained below the downtrend line that has run from the highs of 0.8700 in 2014. It will require a major NZ-specific positive event to force the Kiwi up through the current intersection at 0.6600 and break out of the downtrend. It is difficult to see that major positive over coming months up to the General Election in September. After that, a culmination of factors should cause the break upwards.

The conclusion from the above positives and negatives for the Kiwi over the short-term is that a short-term pullback to lower levels has the stronger argument. Add on financial market speculation that the RBNZ will increase quantitative easing policies further at their next statement on 12th August, the scales tip in favour of seeing 0.6400 before we see 0.6700.

However, my central thematic of a weaker US dollar against all currencies on global FX markets over the medium term still points to the NZD/USD exchange rate climbing to around 0.7000 in early 2021. Local USD exporters should not lose sight of this financial risk (nothing to do with NZ).

Currency speculators finally unwind short-sold NZD positions

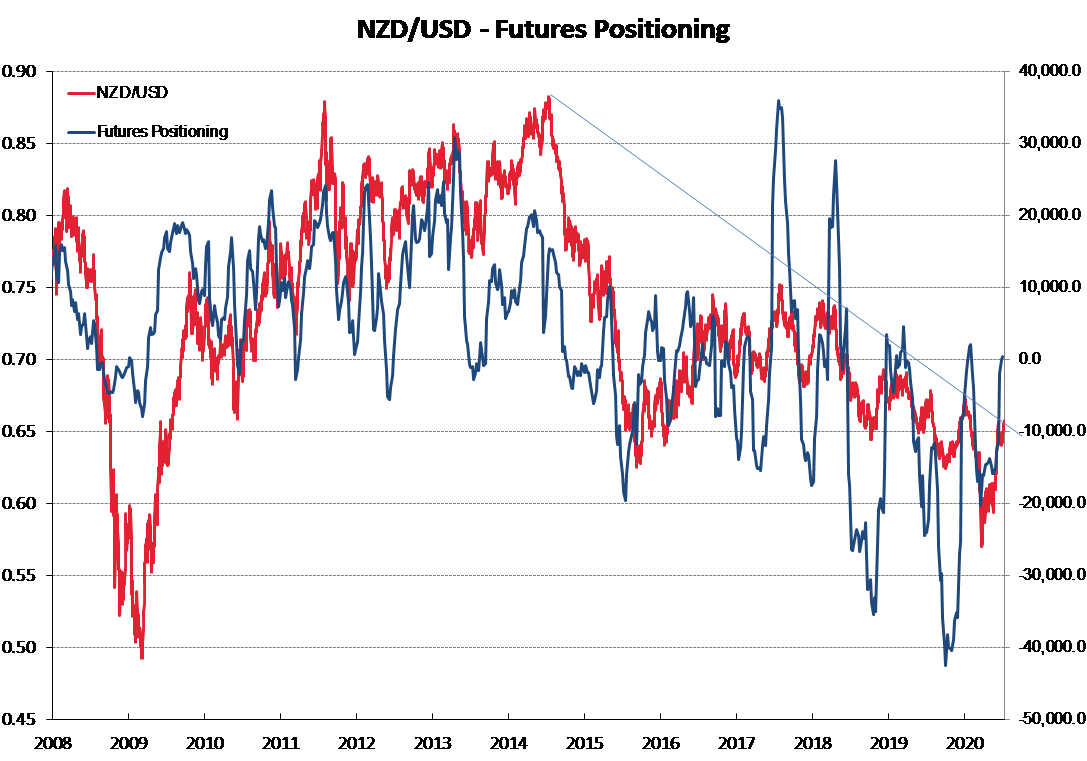

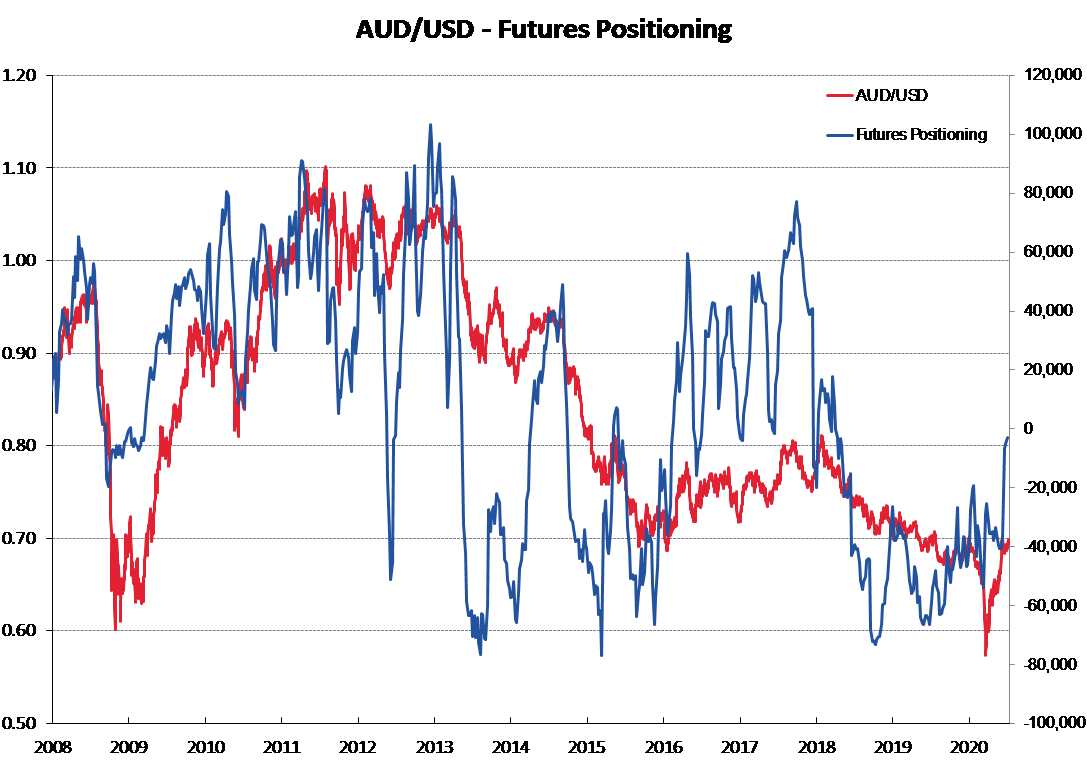

The inevitable unwinding of short sold NZD and short sold AUD speculative positions always stood out as a factor to cause both currencies to rebound upwards from their oversold positions in March/April. Latest data from US currency futures markets (refer charts below) confirms that the punters have finally bitten the bullet and reduced their short-sold positions to a neutral zero.

The hedging behaviour of local fund managers also has an influence on the Kiwi dollar’s market movements. Local investors in global equity funds would expect that their NZD returns are protected somewhat when equities indices fall, and the Kiwi dollar falls in tandem i.e. they would not expect their fund manager to have NZD/USD hedging in place. Fund managers who hastily reduced NZD hedges in March/April have been forced to re-instate those hedges as the Kiwi has rebounded. The sudden reversal in hedging behaviour has contributed to recent Kiwi dollar gains. The FX hedging policies of fund managers are disclosed in their SIPO and Product Disclosure Statement documents, however few investors would read such detail. Many fund managers maintain hedging between 50% and 100%, others favour the 0% to 100% flexibility.

Foreign investor interest in New Zealand’s bond and share markets remains robust and this provides external and impartial evidence that they are not negative on the NZ economy and thus currency value compared to other international investment destinations they could select.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

3 Comments

We are at that Pivotal Point from which we could advance in either direction!

Flashback:

Dealing room – 7 am Monday, after a week of the senior dealers having been belted from pillar to post; the weekend filled with chart analysis; stats analysis; news feeds; tidal chart pattern – all of it.

“So. What do we do? Buy or Sell?’

Silence.

“Come on! We’re here to make money. Someone must have an idea?”

A hesitant, junior voice from the back of the room come forth with “Sell?”

All right!!! The room erupts with high fiving; fist slapping and heads off to the phones and terminal to Sell the guts out of the market! Someone had the confidence to express their opinion.

Tomorrow at 7 am we’ll know whether that squeaky voice was right or not.

Moral?

The market knows everything that we do, and it only takes the smallest of inputs to change the direction of the next movement. But speed and courage are sometimes two of the most important factors.

I think Roger has it wrong , the markets are not behaving in a rational manner , and are reacting to news rather than fundamentals .

Of course the markets are along reacting to stimulus packages ,and the wash up is something we have not seen yet

The fact is the US$ is not in a good space , and irrespective of the trend lines , we are in a much better space .

Covid will likely cause much more damage yet , and the damage will be to the US and EU as its industries are hammered .

We are still producing food ( which everyone needs) so we are in a sweet spot

I think Roger has it wrong too. The last graph on the page shows a structurally strong configuration.

Draw a line from March 23 low to 16 May low and extrapolate it to the outer extremities of the graph. This is the base line side of a possible right-angled triangle. The vertical side of the triangle I would start at 18 May upwards. Complete the triangle from that point and align it with 9 June peak, extending the line until you close the triangle. RULE; breakout must happen before 75% of triangle is complete. Breakout happened within these parameters on approximately 9 July. OBJECTIVE; the height of the triangle carried to the point of breakout is how high it will go. So 0.655 - 0.595 = .06c up to 0.715. Could be wrong, but until now it's looking good. If gold goes crazy, you will see the Kiwi gain - so that's a possible reason.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.