Summary of key points: -

- Anticipated downward correction in the Kiwi dollar proving to be elusive

- Will the October hex hurt the Kiwi dollar this year?

- Chinese Yuan strengthens on positive economic data

Anticipated downward correction in the Kiwi dollar proving to be elusive

Given the speed of the NZD/USD rate climb in an almost straight-line trajectory upwards from 0.6000 to 0.6700 over the winter months of June, July and August, it was the expectation of this column that the Kiwi dollar was due for a sizeable correction back downwards before it could appreciate further to above 0.7000 in early 2021. The price action to date has seen that anticipated market correction prove to be elusive.

The reasons for the NZD/USD just pushing on higher to almost 0.6800 over this last week have been varied, most defying sensible rationale and logic. However, such words often play no role in currency markets!

When the Aussies released their GDP figures for the June quarter a few weeks back the 7% contraction in the economy caused the AUD to depreciate more than one cent against the USD.

When it was announced last week that New Zealand’s economic activity had decreased by a larger 12.2% over the same three-month period, it would be a fair assumption that the NZ dollar FX market reaction would also be just as negative.

The fact that the Kiwi dollar did the opposite and traded higher on the day, can be explained by two short-term but influential Kiwi positive factors: -

- Speculative position-taking in the NZD/USD rate going into the GDP economic release must have been short-sold NZD and when the -12.2% result was not quite as bad as the Government Treasury had forecast at -16%, the punters rapidly bought back the NZD to square up their positions.

- At 1.30pm in the afternoon of Thursday 17 September, Australian jobs numbers came out considerably stronger at +111,000 new jobs against prior consensus forecasts of -35,000. The AUD shot up again the USD and the NZD followed.

Whilst the GDP figures did not spark the forecast pullback against the USD, the subsequent failure of the NZD/USD rate to hold on to gains to near 0.6800 in currency market trading on Friday 18th September is maybe telling us that in the short-term FX traders are not all that keen to be buying the Kiwi at such lofty heights.

In addition, the above two factors that drove the Kiwi dollar up were very short-term in nature, temporary and therefore not long-lasting positives. The rate has corrected back to 0.6760 as US equities markets sold off ahead of last weekend.

Whilst there is no clear evidence yet that US equities are going to move downwards on large-scale profit-taking from the spectacular gains since March, the higher volatility and day-to-day wobbles in market sentiment are displaying a much higher level of uncertainty about future direction in share investors’ combined minds. US equity markets potentially heading south in the run up to the 3 November Presidential election still stand as the one remaining factor that will cause a correction down in the NZD/USD rate to the 0.6500/0.6400 region.

Will the October hex hurt the Kiwi dollar this year?

Whether history repeats for the Kiwi dollar over the next month in the lead up to the New Zealand general election on Saturday 17th October remains to be seen. Over each of the last three years the Kiwi dollar has depreciated against the USD in the September/October period.

- After the 23 September 2017 election of the Labour Coalition government, the Kiwi dollar depreciated five cents from above 0.7300 to 0.6800 by early December 2017. Uncertainty about the economic policies of the “accidental” Ardern Government being one negative for the Kiwi at the time (The Government only formed after Winston Peters’ NZ First Party leveraged the Labour Party the most to get their policies accepted).

- In September/October 2018, the NZD/USD rate was pushed lower from 0.6700 to 0.6400 as the Trump Administration ramped up the tariffs on the Chinese. The escalating trade war causing the USD to strengthen on global FX markets and the Kiwi weakened as trade protectionism is never good news for the NZ economy.

- In September/October 2019, the Kiwi dollar again depreciated by more than three cents from 0.6600 to lows of 0.6300 following the surprise 0.50% cut to the OCR by the RBNZ. The economy did not fall into a hole as the RBNZ were expecting in late 2019 and by January 2020 the NZD/USD rate was back up to 0.6700.

Given that track-record of recent years, any currency speculators currently holding long-NZD positions are more likely to close-down their open positions and become NZD sellers in doing so. The possibility for our election result to be a lot closer run thing than current political opinion polls would suggest, adds to the intrigue and potential FX market uncertainty.

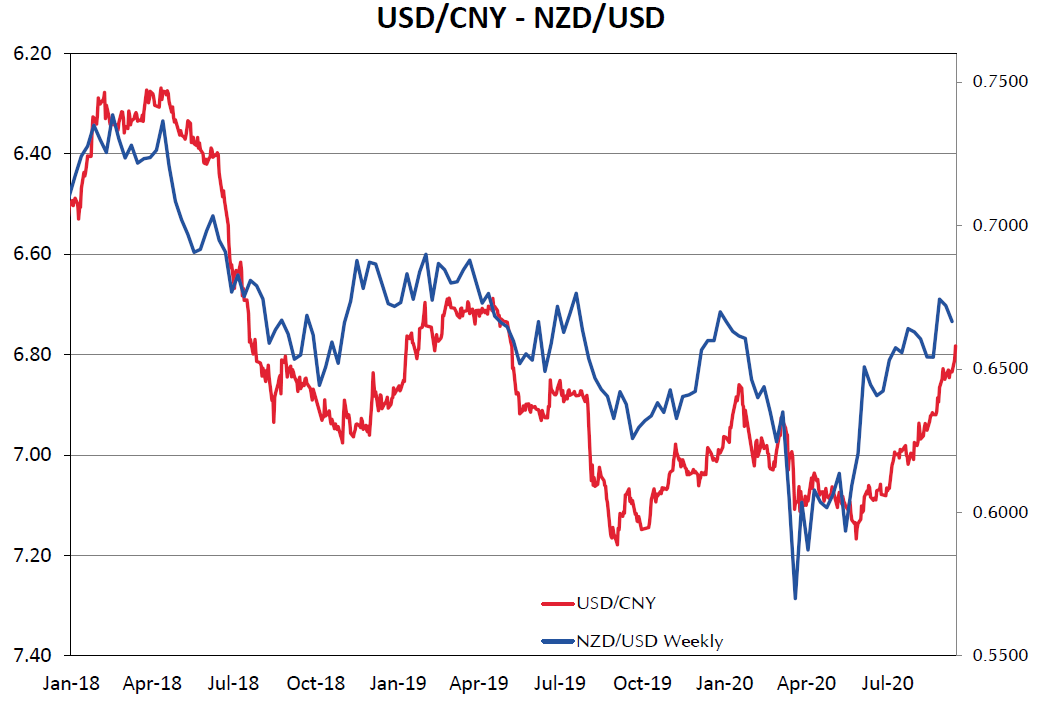

Chinese Yuan strengthens on positive economic data

We have held a consistent and often repeated viewpoint since April of this year that the Chinese economy would recover from the Covid-19 pandemic disruption a lot earlier and stronger than anyone else.

As the New Zealand and Australian economies are highly dependent upon China, we would also recover earlier and faster than the Europeans and the US. As a result of these economic linkages we forecast the NZD to appreciate from the lows below 0.6000 back in April. The scenario has played out as anticipated with recent Chinese economic data for manufacturing, industrial production and retail sales all proving that their economy has returned to normal activity levels. Whilst a managed and controlled currency, the Chinese Yuan has strengthened (as we forecast it would) against the USD from 7.15 in May to 6.77 today.

As the chart below depicts, NZD/USD movements remain closely correlated to USD/CNY changes.

Stronger than anticipated Chinese demand for steel (fiscal stimulus via infrastructure construction, a la GFC 2010) over recent months has spiralled iron ore prices from US$100/tonne to US$135/tonne.

The AUD/USD exchange rate has followed the higher iron ore prices upwards (and the NZD has followed the AUD). We have previously witnessed the Chinese importers going crazy to buy large volumes of raw materials supplies before the price moves up on them, only to then see them become over-stocked with inventory and the prices subsequently collapsing as they stop buying for a few months. The iron ore price rise of recent months feels a lot like this; therefore a sharp iron ore price pullback would not be a surprise from here, resulting in a lower AUD and NZD over coming weeks.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

3 Comments

https://www.tradingview.com/x/EzA4ygC0/

Also have a very interesting rising wedge pattern that looks like it wants to break down imo.

I'm not sure why you are looking at USDNZD. AUDNZD has shown our devaluation va our primary trading partner, likewise CNYNZD has not seen a material change.

There are so many interference's by governments around the world propping up the economies/stock market through asset purchases, short term stimulus infusions that are now running out, unprecedented US bond and ETF govt. purchases that have to stop at some point. Expect interest rates to be held low for many years so countries can attempt to pay down their debt...or are countries going to do a trump and figure paying ones debts is not an important or necessary thing anymore?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.