Summary of key points: -

- RBNZ dealing with a tricky, two-speed economy

- Only a matter of time before global investors recognise stellar Australian economic performance

RBNZ dealing with a tricky, two speed economy

Whether the Reserve Bank of New Zealand (RBNZ) deliver fully or partially to prior market expectations in their monetary policy statement this Wednesday afternoon will determine near-term NZ dollar direction.

The pattern over the last 18 months has been that the FX markets only react very briefly to these RBNZ statements on the economy, monetary conditions and their intentions with interest rates.

The US dollar side of the NZD/USD currency pair has absolutely dominated the Kiwi dollar’s movements against the USD since the plunge/reversal to and from 0.5500 in March/April/May 2020. Local factors have very rarely had an influence and if they have it is just caused temporary blips up and down in the NZD/USD rate.

It appears that the RBNZ will need to be more aggressive on their monetary tightening intentions than the markets are expecting in order to cause a more significant and permanent NZD appreciation.

A higher NZD value brings down imported/tradable inflation earlier.

Certainly on the conditions currently in the economy with sharply higher inflation and a very low unemployment rate, the RBNZ have all the prerequisites in place to act decisively and boldly.

The justification for a 0.50% increase in the OCR to 1.25% seems to be there. As the financial markets have only priced in a 40% chance of this happening, the Kiwi dollar would jump upwards 1 to 1.5 cents on a 0.50% OCR increase.

A decision to lift by 0.25%, however, with a clear signal that they will go harder if inflation looks like it is remaining well above their target, would also be positive for the Kiwi dollar in its own right.

The challenge the RBNZ have in balancing out all the pro’s and cons for a more hawkish/aggressive tightening of monetary policy is that they are facing a tricky, two-speed NZ economy, with risks of collateral damage and un-intended consequences both ways.

The domestic economy is already showing signs of slowing abruptly under the weight of:-

- Many people being afraid to go out of their homes due to the rapid Omicron spread.

- House prices no longer increasing, reducing the “wealth effect” on consumer spending.

- Sharply higher mortgage interest rates for those re-fixing.

- Squeezed household budgets from food and fuel price increases not matched by wages increases.

- Much tougher credit/lending conditions from the banks.

- The hospitality and retail sectors being hit hard by all of the above, as well as high staff absenteeism due to shambles caused by the Government with the availability of RAT tests.

On the other hand, the export economy continues to perform strongly (thank god!) due to higher commodity prices and strong global demand for what we export. Exporters do face difficulties with worker shortages and supply chain/shipping disruptions, however overall most are seeking to expand production if they can.

Typically, an aggressive tightening of monetary policy would shove the NZ dollar higher and that would reduce competitiveness/output in the export sector and slow overall GDP growth (one of the objectives of the monetary tightening).

The RBNZ need to be aware as to what degree the exporters are forward hedged against any NZD appreciation. If the RBNZ is still doing their regular business visits to exporting companies around provincial New Zealand they would be getting the clear message that USD, EUR, JPY and GBP exporters are currently highly hedged against adverse currency risk (some out to two and three years forward). Therefore, an appreciation of the NZ dollar over the next six to 12 months would not negatively impact activity levels and growth in the export economy. Even the AUD exporters are price competitive and profitable at a now lower 0.9300 NZD/AUD cross-rate.

The RBNZ need to take the lead from the Federal Reserve in the US and “look through” the short-term negative impacts of the Omicron strain on the economy and aggressively tighten monetary policy to deal with rampant inflation that has already got away on them. In New Zealand’s case, the challenge is more difficult as we have recent imported tradable inflation overlaid on top of already high domestic/non-tradable inflation that has been ignored and not addressed for 10 years.

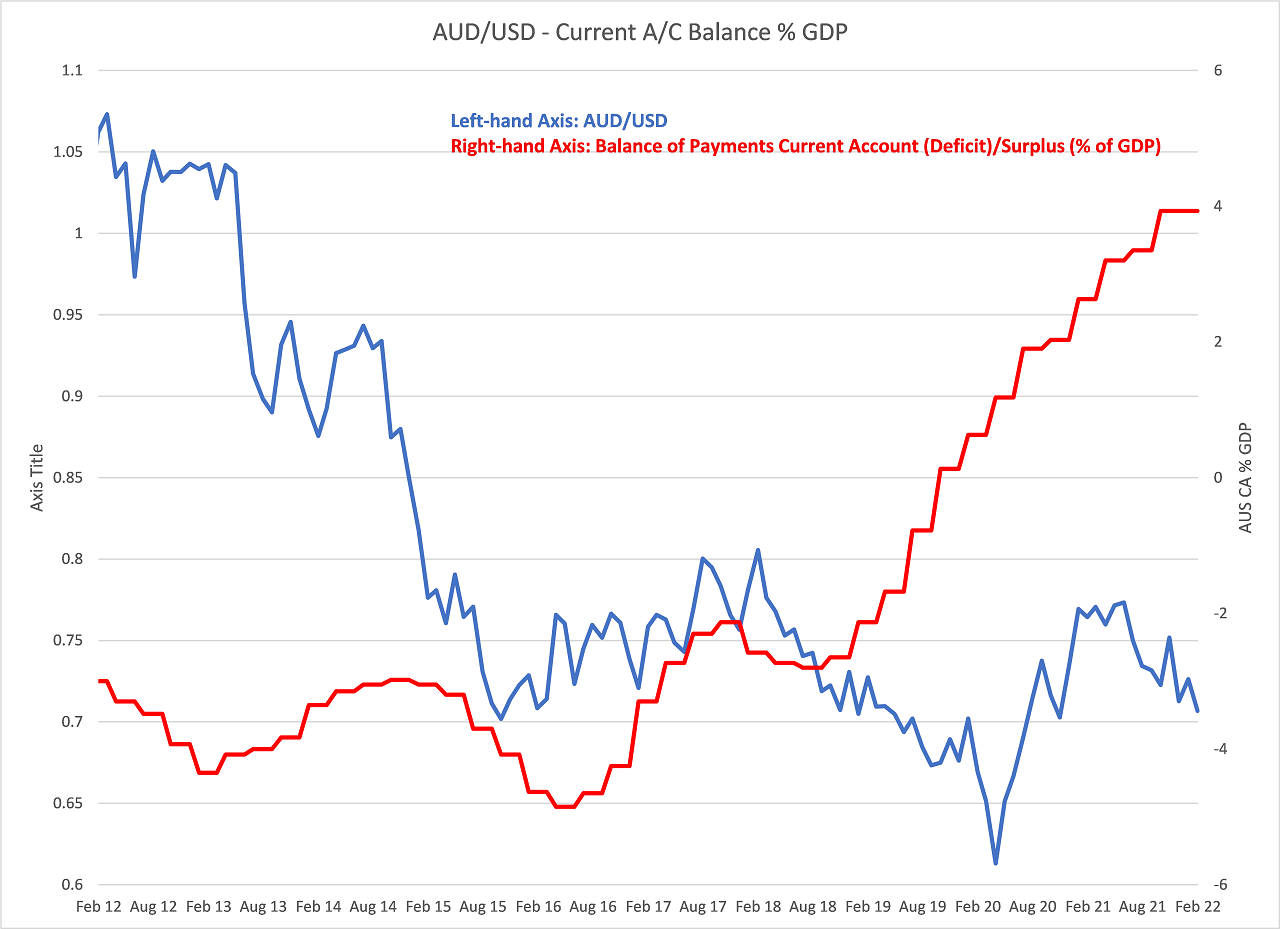

Only a matter of time before global investors recognise stellar Australian economic performance

Arguably more influential on NZD/USD currency movements than US and NZ economic changes/ trends, is the direction of the Australian dollar against the USD. Whilst the NZD/USD rates has been underperforming the AUD/USD rate of late (resulting in the sharply lower NZD/AUD cross-rate from 0.9700 to 0.9300), the market reality is that the Kiwi closely follows the Aussie in daily direction.

Over recent months since the USD started to move sideways against the Euro around $1.1300, the AUD has been unable attract serious buyers as the Reserve Bank of Australia (“RBA”) has continued with their monetary policy stance of not lifting their interest rates until they see clear evidence of wages increasing. The RBA monetary stance has held the AUD back for over 12 months now. For how much longer the RBA can defy what is happening in the rest of the world (except China) with the need to increase interest rates to combat inflation is a debatable point. Australian wage price index data for the December 2021 quarter is released on Wednesday 23rd February. A quarterly increase of 0.70% is forecast, anything above that will exert more pressure on the RBA to change their policy stance sooner rather than later. GDP growth figures for the December quarter a week later on Wednesday 2nd March should also be positive for the AUD.

The AUD appears poised for significant gains against the USD as soon as international FX market players receive the official signal from the RBA that their interest rates will be increasing along with everyone else. On any comparison of economic fundamentals, Australia is a stand-out for currency appreciation, with stronger GDP growth and massive Balance of Payments Current Account surpluses. The Australian resources/mining sector is booming again, awash with high cash and profits from higher commodity prices and the lower AUD/USD exchange rate.

With ScoMo’s Liberal/National Government trailing in the political opinion polls ahead of the May general election in Australia, political risk is likely to loom as a constraint on expected AUD appreciation (in the short-term at least). Global investors into Australia and the AUD would prefer a centre-right, pro-business government. However, a likely change to a Labour Government will not cause fundamental changes in economic policies or economic performance.

The AUD/USD exchange rate currently sits just under 0.7200. A move higher above 0.7400 breaks out of the downtrend line the AUD/USD has traded below for the last 12 months. Forecast eventual AUD gains to 0.7900 by the second half of the year would pull the NZD/USD rate up to 0.7400 (maintaining the current five cent gap between the two currencies against the USD).

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

4 Comments

The assumption of an ongoing five cent margin between NZ and AU in relation to the USD is a very big assumption - see the last sentence of Roger Kerr's post.

KeithW

Yes, although I would suggest any assumption of a future currency value is a big one 😊

With inflation running so high if RBNZ doesn’t raise OCR by .5 and other countries raise rates the NZD will tank making inflation even higher the sharks will be out and can take down NZD quickly. I can remember back in 2001 I was getting 3.3 NZD to 1 pound made everything cheap here.

That would seem very risky too in a world where an increasing number of people can work remotely for offshore companies too. Will make harder for local companies to attract skilled people if they can get paid far more - in NZ pesos - to work for a British or American company (for example).

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.