- Well-timed Japanese Yen intervention lifts the Kiwi dollar

- One-way USD bets in FX markets under fresh scrutiny

- Extreme and excessive conditions everywhere you look

- Domestic inflation has been out of control for 16 years

Well-timed Japanese Yen intervention lifts the Kiwi dollar

You have to hand it to the currency market specialists at the Bank of Japan, they picked their time to intervene in the USD/JPY forex market superbly and adriotley reversed the Yen’s direction on Friday 21st October. The Japanese Yen has been under enormous selling pressure from speculative one-way bets that the Yen would continue to weaken as the authorities refuse to raise their interest rates. As the interest rate differential widened with the rapid increases in US interest rates, Yen speculators were rewarded with a massive forward point benefit when selling the Yen against the USD. The plummeting Yen value to above 150 against the USD for the first time since 1990 in sleepy afternoon New York trading last Friday was the cue for the Bank of Japan to act with large-scale intervention, buying the Yen in the open market. They caught the market napping with the USD/JPY exchange rate immediately reversing from 151.95 to 146.30, before settling to 147.65 by the market close. The direct market intervention could not have come as any surprise to FX market participants, the Japanese authorities had been threatening further action recently following their US$20 billion of Yen buying intervention during September.

The Kiwi and Aussie dollars were instant beneficiaries from the Japanese market intervention to sell the USD, the NZD/USD rate lifting from the day’s low of 0.5600 to 0.5770. The poorly performing Australian dollar attracting even more bids and appreciated 180 points from 0.6210 to 0.6390. Short-term intervention by a central bank to buy their own currency to prevent further depreciation is only effective if there are sufficient USD reserves to sell and the speculators are sufficiently frightened-off to go play somewhere else. Time will tell whether the Japanese currency market intervention is the catalyst that turns the tide on the US dollar’s relentless appreciation against all currencies this year. However, the one-way bet is no longer safe and secure for the FX punters and this is a significant change in currency market conditions. Off course, at the end of the day, relative economic performance and monetary/fiscal policies the drive investment/capital flows inwards and outwards will determine longer-term currency values.

One-way USD bets in FX markets under fresh scrutiny

The Kiwi’s dollar’s whippy price action against the USD over the last four weeks, repeatedly moving up and back between 0.5550 and 0.5800 may be signaling significantly increased uncertainty in the minds of the currency speculators who have sold the Kiwi dollar along with many other currencies against the rampant USD over recent months. Such zig-zag movements, up and down, at the end of long-running and clear trend often signifies a turning point in direction. The currency market players holding short-sold NZD positions will be concerned at the resistance and support building up at the lower bound in the 0.5500’s. However, there has not yet been a convincing event or change with the US dollar itself to attract larger scale NZD buying/USD selling to push the Kiwi back above 0.5800 to 0.6000. The likely event that will cause a more permeant change of direction for the NZD/USD rate is the US Federal Reserve hinting that they have tightened their monetary policy enough to bring inflation back down. Up until very recently all the Federal Reserve members where consistently singing from the same song-sheet that US interest rates need to go “higher for longer” to combat inflation. However, the US dollar also lost some value in the markets last Friday when a Wall Street Journal media story suggested that there was a growing debate within the Fed as to the appropriate future pace of interest rate increases from here. The Fed members will be observing the same dramatically weaker data in the US housing market in September that the markets are also witnessing.

Over recent weeks we have highlighted the importance of trends in the US residential real estate market as holding the key to inflation reducing and therefore the Fed pausing and pivoting on their tight monetary policy stance. The plunge in new build and existing house sales activity levels is leading to falling house prices, which ultimately leads to lower rents (“shelter” in their CPI measure). Six months ago it was sharp increases in oil, commodity, supply chain/freight, micro-chip and food prices that pushed US inflation up to 8.50% from 3.00%. Today, all those prcies are reducing. The largest cause of US inflation is now the shelter component. In last week’s report we outlined the considerable time-lag with these housing cost adjustments due to the archiac CPI inflation calculation method. Some Fed members are now quite rightly questioning the need for the continuing tight policy stance when they observe that current rising shelter prices will ultimately reverse and fall.

Support us by going ad-free. Find out more.

We contimue to hold the opinion that the current massive and highly leveraged “long USD” positions in the FX marketplace built up over the last six to nine months will all reverse when the makets are convinced that the Fed is nearing a “pause” date. That date may be a lot closer (i.e. before the end of the year) than what most currently believe. The time of year is also critical here, US hedge funds and investment banks typically close-down their open positions and profitable trades, taking the cash profits before their 31 December financial year-end and Christmas holiday period. The failure of the USD Dixy index to follow US 10-year bond yields higher over this last week may be an early sign that the conviction from the speculators that the US dollar will continue to strengthen may be wavering. The argument against the US dollar reversing to a weaker trend in 2023 is that the US dollar always stays strong when the world economy is in recession. The counter to that argument is that the currently over-valued US dollar is a big cause of the financial and economic problems for the rest of the world (higher inflation due to currency weakness). A reversal of the US dollar’s appreciation would be a release valve for the global ecomomy and it reduces the probability of a damaging recession.

Extreme and excessive conditions everywhere you look

The Japanese have been prepared to take extreme and excessive measures with the FX intervention to help their economy. It seems we are seeing many other “extreme and excessive” geo-political, economic, and financial/investment market situations around the globe currently that is rendering decision-making difficult for businesses, investors, and governments alike: -

- The extraordinary mess that is the UK economy, economic policy, and political leadership.

- The US Federal Reserve’s belated and aggressive monetary tightening that is causing chaos around the world to the point that some African countries cannot afford to import grain to feed their population as their currencies have depreciated so far.

- The extreme Covid-Zero policy in China is damaging their economy and that of their trading partners. China’s September quarter GDP growth numbers were due for release last Tuesday. They will not be too good, and they do not release the unwelcome news in the middle of their Communist Party Congress!

- The energy crisis in Europe has caused extreme decisions to go back to coal and nuclear as energy sources. The Green environmentalists in Europe are seemingly happy to waiver from the cause if it means they keep warm in their homes this winter!

- The Reserve Bank of Australia are off on another one of their tangents to everyone else on monetary policy. They may be right with their now slower pace of interest rate increases; in which case the NZD/AUD cross-rate continues higher to 0.9200/0.9300. Or, they may have it wrong again and be forced into another policy U-turn. Under this scenario the NZD/USD cross-rate would return to 0.8900.

- Here in New Zealand, the current Government leadership seems prepared to sacrifice food production and damage our largest industry to claim a “world first” in climate change policy. Cattle and sheep have farted and burped methane into the atmosphere forever, so how could they be the cause of the increased man-made carbon emissions that have caused the climate change since 1990?

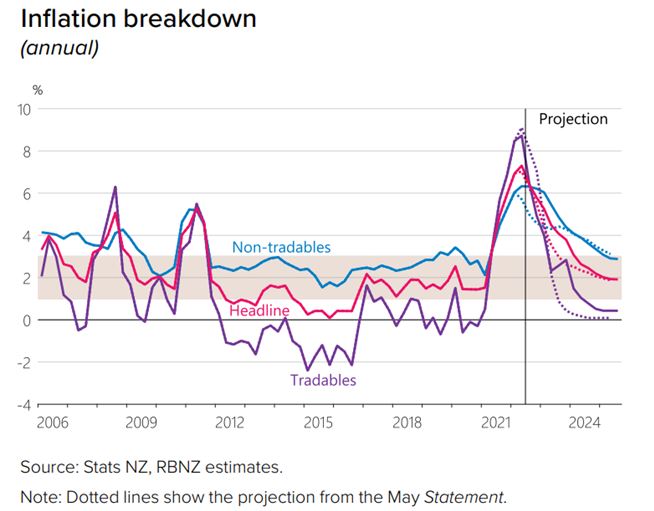

Domestic inflation has been out of control for 16 years

The vociferous calls for an independent enquiry into the management of monetary policy through the Covid era by the Reserve Bank of New Zealand are barking up the wrong tree. Sure, the RBNZ (in hindsight) went too far with money printing and cheap loans to the banks in 2020 and 2021 and we are now paying the price with tight monetary policy to contain the resultant inflation. However, those were judgment calls that had to be made in a very uncertain environment, therefore there is not a lot to be gained from questioning their decisions well after the fact.

What an independent enquiry into the RBNZ should focus on is their total failure to understand and address the root causes of the domestic (non-tradable) inflation over the last 16 years. The RBNZ are supposedly the guardians of the value of our savings and spending power by maintaining low inflation. Low tradable inflation and reducing technology/communication prices worked to disguise consistent domestic inflation that has averaged 3.20% pa over the last 16 years. Now that the tide has turned the other way with overseas-sourced tradable inflation, the emperor has been caught with his pants down. Excessive Government legislation, regulation and compliance costs have been passed on by the public sector to the consumer through the high non-tradable inflation. It is the RBNZ’s responsibility and accountability to stop such excessive pricing behavior at the top of the cliff, rather than just reactively changing monetary policy at the bottom of the cliff. By only being reactive to developments they have caused unnecessary volatility in the economy, interest rates and the exchange rate.

It is time someone stood up, asked the challenging questions, and demanded RBNZ accountability for a systemic monetary policy failure.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

10 Comments

What an excellent column! Yes, the current government's "climate change" policies will have severe repercussions for the NZ economy. Under the new legislation, another 700,000 hectares will be planted in pine forest, with much of this replacing beef and sheep farms which are a significant part of our export earners. Overseas investors will own these plantations and be subsidised by the NZ taxpayers, who will earn "carbon credits." How stupid can you get? Meanwhile, China continues building many new coal fired electricity generators, so that New Zealand's actions make no significant difference to so-called climate emissions.

Excellent analysis and insights thanks Roger. It does feel like groundhog day and by end of year we will see some new trends emerging. Demand side inflation pressures seem to be easing, I don't think the impact of Covid on supply side has been weighted enough. Regulatory pressure on non-tradeable inflation is also a big blind spot in the beltway political scene.

The Bank of Japan is forced to burn billions of $USD to temporarily protect the Yen, and this is... a sign of imminent Yen strength and $USD decline?

what?

Yep, wondered the same thing. Didn't appear to help much last time either.

Cattle and sheep have farted and burped methane into the atmosphere forever, so how could they be the cause of the increased man-made carbon emissions that have caused the climate change since 1990?

I tell you what Roger, let the engineers and scientists handle the climate stuff, and you stick to currency trading! About 5 minutes of informed research will give you the answer to your question. Maybe do that before spreading a narrative that is both misleading and dangerous.

It is indeed astonishing that this website still employs a climate change denier to offer us his 'views' on the subject, and it does the reputation of this site no favours at all. As was demonstrated during the covid crisis they were quick to remove the misinformation on that subject that mushroomed on here (correctly of course), but when it comes to misinformation on the biggest crisis of all? Abject inaction.........

Gosh, I'm glad you're not in charge of things whiner.

Jfoe - Agreed and well said.

Just like when Soros nuked the Bank of England in 1992 on Black Wednesday, speculators are about to nuke the Bank of Japan as seen again this morning on another intervention dip rebound. Contagion will spread through U.S treasuries, then its game over, no one is safe.

Japan’s exposure to US Treasury bonds is having a big impact on the JPY.

https://www.bloomberg.com/news/articles/2022-10-18/japan-s-treasuries-h…

US is successfully exporting some of its inflation to countries like China & Japan which own large volumes of US Treasury bonds.

USD has some protection as the world’s reserve currency. NZD is not protected to the same extent & will suffer much more from its excessive money printing.

How this will play out is unclear but there appears to be some downside for NZD as our trade deficit will struggle to reduce with slowing global / Chinese demand.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.