-

Summary of key points: -

- Trans-Atlantic capital flows likely to shift the EUR/USD exchange rate dial

- Interest rate differentials likely to shift the NZD/USD dial as well

Trans-Atlantic capital flows likely to shift the EUR/USD exchange rate dial

The movement of capital across borders can have a profound impact on exchange rate values. Direct capital flows will pour into an economy that offers attractive investment opportunities, often related to the mining of resources or they have substantially lower energy/manufacturing costs. Lower taxation rate jurisdictions use to be another major reason for cross-border flows being attracted into a particular economy. Free-floating currencies will appreciate if there is large and permanent foreign capital inflows.

Equity portfolio investment flows will be attracted to sharemarkets that are considered undervalued relative to the outlook for the economy the listed companies are operating in. If the target sharemarket and economy have a currency that is considered undervalued (compared to its historical trading ranges), then that will be an added incentive to make the cross-border investment. If enough external investors are attracted into the target market with large amounts of money concentrated into a particular point in time, then it is inevitable that the currency value will be pushed up as the funds are converted into the local currency. Off course, the opposite occurs as well when the foreign investors all decide to exit at once, the local currency value will be smashed downwards by the selling pressure.

It is not just equities fund managers switching their investment portfolios around the globe that impact exchange rate values, fixed interest fund managers also diversify their risk by buying Government and Corporate bonds in many countries. The bond fund managers will be attracted into a particular country’s bonds if both the underlying interest rate and the margins (credit spreads) are at elevated levels and are expected to move downwards. The inflation rate reducing sharply in the future would be one reason why the interest rates in that target economy would move lower. The difference between the interest rates prevailing in the investor’s home market and the interest rate levels in the target external market will also drive bond fund managers to switch their money from one market to another.

For all the reasons cited above it is therefore no surprise that the EUR/USD exchange rate is closely correlated to the differential between US and European 10-year Government bond yields. Fund managers domiciled in Europe will weight their bond portfolios more heavily to the US bond market if US interest rates are well above European interest rate levels. The European fund managers will also be calculating on receiving an added bonus of FX revaluation gains as the US dollar appreciates against the Euro over the time period they are invested in the US market. When the US bond market no longer offers a yield return pick-up compared to European bond yields, the European fund managers will bring their funds back home to Europe. If they are sitting on large FX gains from their US investments because the USD appreciated against the EUR over the period they will even more incentivised to sell their US bonds and sell the USD proceeds as well.

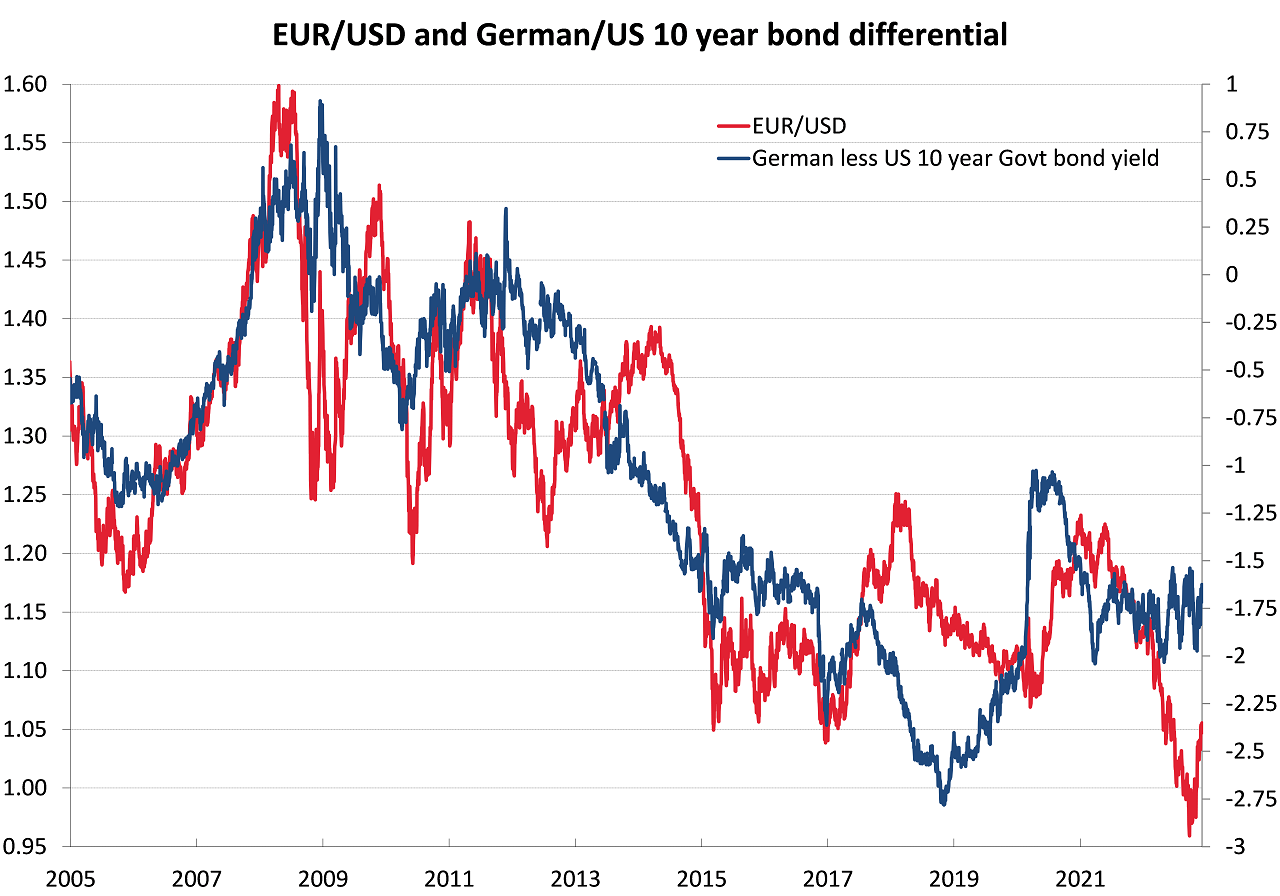

The chart below plots the EUR/USD exchange rate against the differential between US and German 10-year Government bond yields (right hand side axis – German yields less US yields). In the 2009 to 2011 period German and US 10-year bond yields were at the same level. Over the subsequent eight years until 2019, US bond yields increased to be 2.60% above German bond yields. European fund managers were attracted to the higher US yields and as a consequence of those Europe to US capital flows, the USD strengthened against the Euro from $1.4000 in 2011 to the $1.1000 area by 2019.

US fund managers invested in European bonds would have sold out of those bonds and shifted their funds back home as the US yields were so much higher.

Today, the bond yield differential is 1.65% with US 10-year yields at 3.58% and German 10-year Bunds at 1.93%. The writer’s strong view is that over the next six to nine months US bond yields will reduce further to 3.00% as the US Federal Reserve pause and pivot on monetary policy due to US inflation decreasing from 7.00% to 3.00% as fast as it went up to 7.00% over the first nine months of this year. The Federal Reserve is nearing the end of its monetary tightening cycle; however the Europeans are only just getting started with theirs. The European inflation rate is above 10.00% and the European Central Bank (“ECB”) has been very slow to raise their short-term interest rates due to Russian/Ukraine war causing an energy crisis, therefore damage to the European economy. However, events have moved on in Europe with gas prices plummeting over recent months as alternative sources are found to the Russian Nordstream pipeline. The European economy has not performed as poorly as everyone had feared three of four months ago. Therefore, the ECB can now more aggressively tighten monetary policy by jacking their interest rates higher and they have a long way to go. As a result, German bond yields seem likely to increase to at least 2.50%, if not closer to 3.00%.

The US/German bond yield differential going forward is therefore set to reduce from the current 1.65% to say 0.50%. (i.e. the blue line on the chart moving up from -1.65% to -0.50%, right had axis). The change in the bond yield differential will entice European bond managers to bring their funds home from the US, selling USD and buying EUR in doing so.

If the historical relationship/correlation holds, the EUR/USD exchange rate will not be staying at $1.0500, the capital flows back to Europe could force it all the way back up to $1.3500. Over the course of the next 12 months even if the EUR/USD rate only increases to $1.2500 (weaker USD), it would result in the NZD/USD exchange rate appreciating to above 0.7500.

Interest rate differentials likely to shift the NZD/USD dial as well

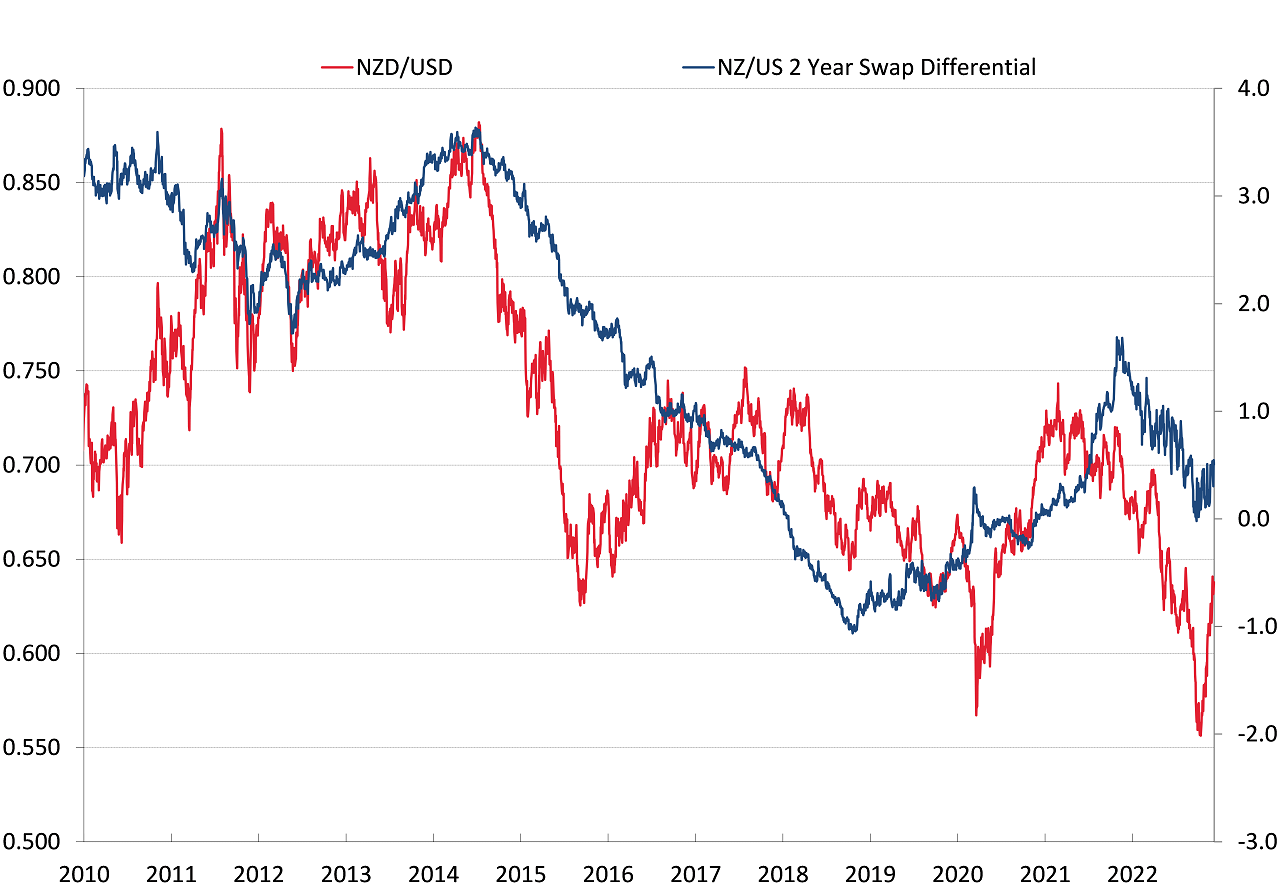

Over recent years the NZD/USD exchange rate has dislocated itself from being highly correlated to US:NZ interest rate differentials. Currently, the gap between New Zealand and US 2-year swap interest rates is only 0.67% (NZ = 5.31% and US = 4.64%). US macro funds and hedge funds have had no reason to play in the Kiwi dollar to get a yield return pick-up. However, looking forward into 2023 a highly likely scenario is New Zealand interest rates staying higher for longer as the RBNZ combat the pesky wage-push inflation problem (largely caused by Government employment and immigration policies). Whereas in the US of A, their 2-year interest rate is primed to reduce to the 3.00% to 3.50% area as the Fed eventually cut their interest rates as the economy weakens and inflation is back down.

The 2-year swap interest rate differential is therefore set to increase to 1.80% to 2.00% (the blue line on the chart below moving higher). Another strong reason why the Kiwi dollar will not be staying at 0.6400 in 2023, it will potentially move back to the previous 0.7000 to 0.7500 trading range.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.