Summary of key points: -

- Three dips and recoveries for the Kiwi dollar since mid-December

- NZD/AUD cross-rate oversold at 0.9250?

- It is rare for the NZD/USD rate to deviate from general USD movements

Three dips and recoveries for the Kiwi dollar since mid-December

Events and trends in global financial and investment markets are shaping up to be quite different in 2023 that what was experienced in 2022. Last year we saw “one-way” US dollar strength for the first nine months due to the war, sharply higher inflation and the Fed. That was followed by a reasonably rapid US dollar sell-off over the last three months as the markets realised that US inflation had already peaked, oil prices had dropped to pre-war levels and the Fed had arguably tightened too hard. Last year was one of big FX price movement cycles due to those events and developments. Unless there is another global shock or risk event like the Russian invasion of the Ukraine, this year is unlikely to see the big price cycles of 2022 repeated. However, FX market volatility from unexpected economic and geo-political events will still occur, presenting both dangers and opportunities to those with FX risks.

After climbing impressively to 0.6500 in mid-December against the USD, the Kiwi dollar has been very much in a corrective phase over this last month. Whilst the wild unseasonably summer weather across much of New Zealand has not been conducive to swimming in the sea, rivers and lakes, the Kiwi dollar has itself had three dips over the period. The mini-sell-offs in the NZD/USD exchange rate down to 0.6250 on three separate occasions since 22 December have largely been due to bursts of selling in US equity markets. The “risk-on” and “risk-off” sentiment modes from equity investors remain as dominant short-term drivers of the NZD/USD exchange rate direction. The Kiwi dollar correlation to the Dow Jones Index continues to be close. Equity investors have been selling shares on reports that the Fed are not yet done on interest rate hikes and also on weaker corporate earnings. The same investors (or traders?) have been buying the market on data that points to a US economic slowdown and therefore interest rates decreasing. The Kiwi dollar has been buffeted around by this whiplashing equity market sentiment.

Local USD exporters with FX orders placed with their bankers down to 0.6250 over the holiday period would have had all of them triggered and therefore restored their hedging profile to policy maximums for the risks that lay ahead.

Whilst the December Non-Farm Payrolls jobs result of a 233,000 increase released last Friday would suggest a continuing strong US labour market (therefore continuing inflation risks according to the Fed), the markets instead focussed entirely on the accompanying average hourly earnings wages data. The annual wages measure declined to +4.60% in December, significantly below prior consensus forecasts of a 5.00% increase, therefore pointing to a softening in the labour market. On this news over one day’s trading on Friday, equities rallied 700 points on the DJI, 10-year bond yields dropped from 3.75% to 3.56%, the USD Dixy Index depreciated from 105.36 to 103.64 and the NZD/USD reversed back upwards one cent to 0.6350.

In the short-term, further Kiwi dollar gains back towards 0.6500 are anticipated as the USD continues to weaken on global FX markets and the markets look ahead to the local CPI inflation result for the December quarter on Wednesday 25th January. Forecasts are for a 1.90% increase for the quarter, which will lift the annual inflation rate from 7.20% to 7.70%. The historical inflation data will keep the pressure on the RBNZ to maintain their tight monetary policy stance at their next meeting on 1st February. New Zealand’s higher short-term interest rates still stand out as a positive for the Kiwi dollar over the first half of 2023 as “carry-trade” investors are attracted into the Kiwi.

NZD/AUD cross-rate oversold at 0.9250?

The 10 cent fall in the NZD against the AUD from 0.9700 in October 2021 to 0.8750 in October 2022 was due to the FX markets pricing ahead the fact that the Reserve Bank of Australia (“RBA”) would eventually be forced to increase their interest rates and therefore the interest rate differential between the two currencies would reduce. However, since October 2022, the reverse situation has developed, with the RBNZ belatedly tightening monetary policy harder as wage-push inflation is embedded-in, whilst the RBA is seemingly now on a “go slow” monetary policy tangent. The NZD/AUD cross-rate therefore raced back up to 0.9500 in mid-December as the interest rate differential again widened out in the NZD’s favour.

Over the last three weeks since mid-December, the NZD/AUD cross-rate has completed another U-turn to drop to 0.9235 as the AUD has markedly out-performed the NZD against the USD in volatile FX market conditions. There has certainly been more favourable economic news for Australia over this period with China rending its ban and re-commencing coal imports from Australia. However, with the RBNZ about to re-emphasise the need for continuing tight monetary conditions against the more permanent wage-push inflation situation we have in New Zealand, it is hard to see the NZD/AUD cross-rate staying down at 0.9235 for very long.

Local AUD exporters who are not already hedged at policy maximum limits have another opportunity to load-up at 0.9235.

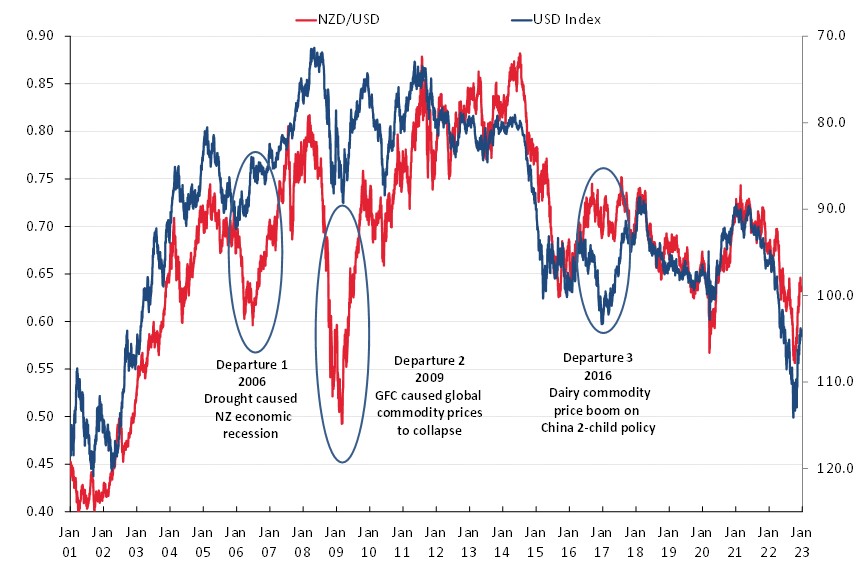

It is rare for the NZD/USD rate to deviate from general USD movements

Moving away from the short-term movements and forces on exchange rates, the start of a new year is always a good time to reflect back on the longer-term currency patterns and think about where the Kiwi dollar stands in a big picture sense.

The recurring theme of this market commentary piece over the last two years has been that the NZD/USD exchange rate movement have been totally driven by the USD side of the equation, nothing to do with NZ factors. Looking ahead into 2023 that USD dominance is likely to continue.

Over the last 20 years there have only been three occasions or periods when the NZD/USD exchange rate has deviated from, or departed from, general USD movements (as measured by the USD Dixy Index): -

- 2006: The NZ economy was diving into recession well ahead of the GFC due to a drought reducing agriculture/export production.

- 2009: The GFC caused global commodity prices to collapse, hitting the NZD very hard.

- 2016: The Kiwi dollar strengthened on rising dairy prices due to Chinese importers buying two-year’s supply all at once on the change away from the one-child family policy.

Since 2017, the NZD/USD rate has been in a lock-step correlation with the USD Index and there is nothing on the horizon to suggest that we will see extraordinary conditions or events to force another deviation.

Local companies with NZD/USD FX risks therefore must look to the US factors this year i.e. US inflation falling as fast as it went up in 2022 and the Fed being forced to pause and pivot on interest rate changes. We remain of the view that the USD depreciates to below 95.00 on the USD Dixy Index over coming months, resulting in a 0.7000 NZD/USD rate.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

4 Comments

Good to see talk of opportunities on interest.co.nz

Hort and arable guys are having a terrible season - will be interesting to see what sort of a dent that puts in the domestic picture given dairy and meat are also coming off recent highs pretty fast now ….. and forestry isn’t exactly pumping either. I’m sure the tourists will plug the gap 🫤 - but we haven’t seen mediocre commodity prices in conjunction with anything like our current levels of spending (imports) before - and given we’ve stopped with the volume and are all about the value these days - someone better hope we dig up some more value pretty quick.

I agree and think 0.70 NZD USD will happen. Lets see.

Roger that.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.