Summary of key points: -

- USD and AUD movements drive the Kiwi dollar to the bottom of its trading range

- Fed turning point edges closer

- Another heroic call from the Reserve Bank of Australia

USD and AUD movements drive the Kiwi dollar to the bottom of its trading range

A continuation of the dominant US dollar influence over NZD/USD exchange rate movements has seen the Kiwi dollar pushed, once again, down to the lower end of its established 0.6000 to 0.6400 trading range since February.

From trading just above 0.6400 on 14 July, the NZD/USD has depreciated 5.1% to a low of 0.6060 last week. Over the same time period the overall USD Dixy Currency Index has appreciated 3.3% from 99.20 on 14 July to a high of 102.45 last week. The latest USD gains coming about as many FX market participants see the next US Federal Reserve (“Fed”) meeting on 20 September as being a “live” meeting for another 0.25% increase in their official interest rates. Whether the Fed lifts rates again, or not, (as always) “depends on the evolving economic data”.

Over and above the USD appreciation of recent weeks, the Aussie dollar was hammered down last week following the Reserve Bank of Australia (“RBA”) delivering a more dovish than expected statement on monetary policy, inflation, and the Australian economy. The RBA yet again leaving their official interest rate unchanged at 4.10%. The end result was the AUD/USD exchange rate plunging two cents (3.0%) from 0.6730 before the Tuesday 1st August RBA meeting to a low of 0.6530 two days later on Thursday 3rd August. The Kiwi mirroring the AUD/USD decrease, dropping nearly two cents over those same two days from 0.6230 to the 0.6060 low.

Therefore, in forming the arguments and probabilities for the NZD/USD outlook from here, how the USD and AUD currencies respond to the emerging economic data in the US and Australia respectively, holds the key for the Kiwi dollar direction. The rest of this report addresses those issues.

Upcoming local New Zealand economic data releases that may only have a peripheral impact on the Kiwi dollar include:-

- 16 August: RBNZ Monetary Policy Statement (no change to current stance).

- 8 September: NZ Government pre-election update on their fiscal deficit position (how big is the fiscal hole?).

- 21 September: GDP growth for the June quarter (0.50% expansion expected).

The Fed turning point edges closer

To convince the Fed Governors that US inflation risks are much reduced and they can stop hiking interest rates, it was thought that it would take more than one month’s weaker employment data to allay their “tight labour market/increasing wages” fears. A month ago, the June Non-farm Payrolls jobs increase was less than expected at 209,000. Last Friday’s July jobs increase at 187,000 was also less than prior forecasts. The evidence is certainly gathering that the US labour market is finally softening and with that inflation risks decreasing.

As it is with inflation, it always pays to analyse the component parts of employment growth to understand the trends and form a view on future trends. Over the last three months most of the jobs growth in the US economy has been healthcare and Government workers. The big private sector industries of construction, retail, manufacturing, and hospitality/leisure are flat or contracting. Worker numbers in the US healthcare sector have now increased to above 2019 pre-pandemic levels, so it is difficult to see their job increases continuing over coming months.

US inflation numbers for July are released this week on Friday 11th August. Consensus forecasts are for a 0.20% increase in prices over the month, which will marginally increase the annual inflation rate from 3.00% to 3.10%. The wildcard in the numbers will be whether we see significant decreases in the rents/shelter component part as the 12-month time lag in this data turns from lease renewals being higher, to being lower. A surprise inflation result below +0.20% would certainly be fuel for the USD market bears i.e. a weaker USD.

We believe that there will be enough evidence of softer economic data in front of the Fed by 20 September that they will halt their interest rate increases. That official confirmation will be seen as a major turning point lower for US market interest rates and the US dollar value. The FX markets will start to price this probability into the USD value well ahead of the 20 September meeting.

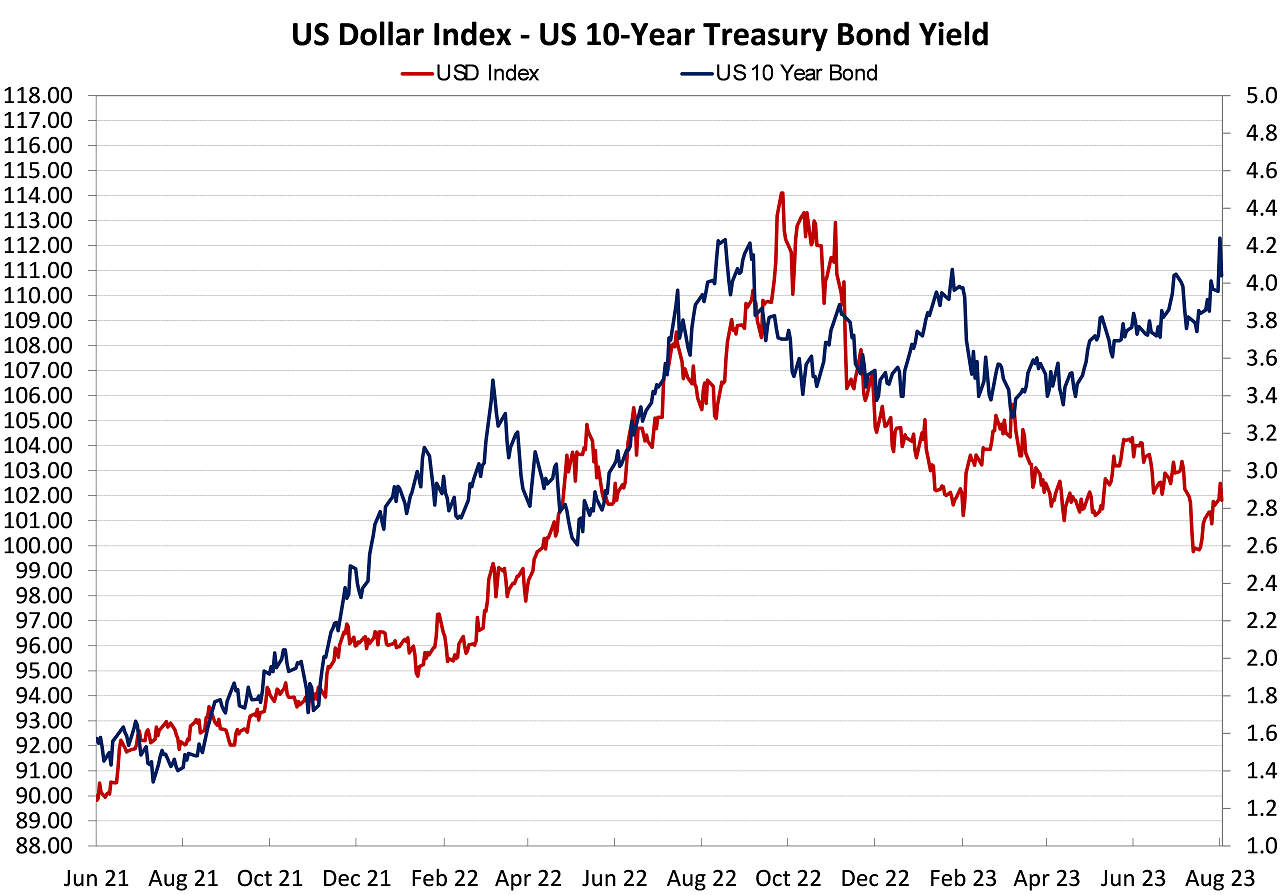

The gains by the US dollar in recent weeks have been aided by rising US bond yields. Despite the lower inflation outcomes and now softer jobs numbers, bonds have been heavily sold (yields higher) due to the increased supply coming into the market from the US Government. There has been a massive increase in the issuance of new bonds since the debt ceiling deal was struck in June. US 10-year Treasury Bond yields climbed to 4.24% last week, however in a “key-day reversal” movement, the yield plunged to 4.04% on Friday night’s softer than expected jobs numbers. It has also been reported that Warren Buffet’s Berkshire Hathaway were buying bonds last week at the yields above 4.00%. Why wouldn’t they be doing that with US inflation heading to 2.00%, the “real” 2.00% return above inflation is the highest seen for many years.

The chart below confirms that the two previous spikes higher in the 10-year bond yields to above 4.00% (in August 2022 and January 2022) proved to be short-lived. The current spike higher is also not expected to last long. Lower bond yields over coming weeks/months back to the 3.50% area will be negative for the US dollar value. The recent gains by the USD (red line on chart, left hand axis) in February to 105 and June to 104 is showing a pattern of peaking-out at lower levels. The latest USD gain to 102.45 last week could not be sustained and the USD is lower to 101.80 following Friday’s softer jobs data.

Another heroic call from the Reserve Bank of Australia

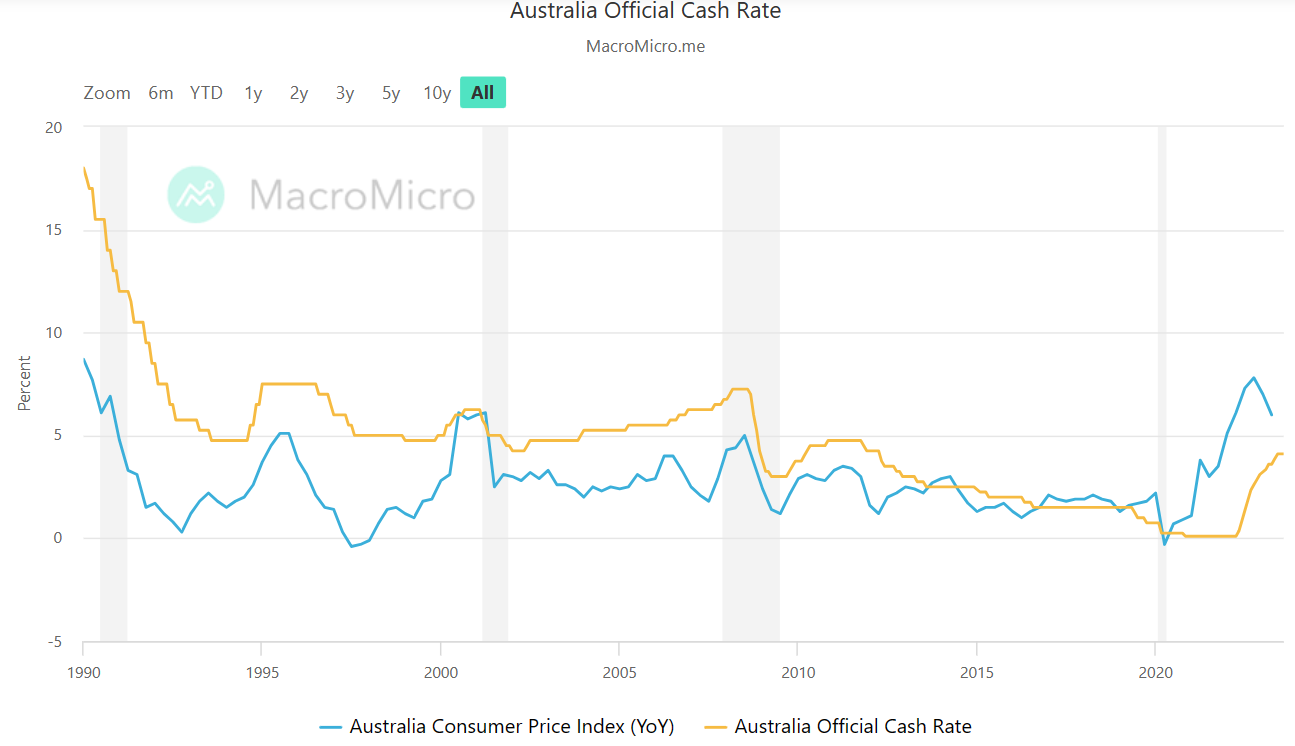

Over the first seven months of this year the RBA have delivered a succession of inconsistent U-turns with monetary policy and interest rate decisions. Last week’s pause and accompanying dovish statement was another example. The FX market were not expecting an interest rate increase last week; however the RBA now seem more worried about causing an economic recession than forcing inflation lower. The RBA’s complacent and ponderous approach to reducing the stubbornly high inflation seems to be based on believing that an interest rate of 4.10% is sufficient to slow the economy, reduce wage settlements and therefore push inflation back down. They appear to be in their own dreamland when compared to interest rates in the US, NZ, the UK and Canada all being above 5.00% with inflation rates similar or lower than Australia’s.

At some point not to far away the RBA will wake up to their mistakes with monetary policy management and increase their interest rates to closer to 5.00%. The new RBA Governor, Michelle Bullock starts on 15 September, and she is expected to bring a harder line on controlling inflation. Ms Bullock will be well aware that the longer it takes for the RBA to get inflation back down, the greater the financial pain on Australian households. Extending the monetary tightening process out as the RBA have been doing to date, lengthens the period of pain. As the Fed and the RBNZ have demonstrated, rapid interest rate increases to higher levels is the most effective method to reduce that period of pain from high inflation.

Just why the RBA currently think the Australian economy is so different to the rest of the world on this stuff beggar’s belief.

The chart below compares Australian interest rates against their inflation rate. Previous RBA monetary tightening cycles to bring inflation down in 1995, 2001, 2008 and 2012 all required interest rates to be well above the inflation rate. Why is this cycle so different that 4.10% interest rates will do the job? To be fair, the current increase in interest rates from 0.00% to 4.00% is the largest and most rapid. However, the question is whether the still relatively low level of 4.00% interest rates will change the economy and price-setting behaviour to bring inflation down. Evidence from history and other countries would suggest not. There is only upside for the AUD from here as the RBA rectify their mistake and are forced to hike interest rates again.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

3 Comments

The belief that the Fed must do something is very ingrained. How about the Fed does nothing at all and we let economies find their own levels of equilibrium.

Trouble is, with fiat currency it’s intrinsic value is zero. Left to their own devices markets will find that value, (we will end up with hyperinflation)

NZD going sub 60c. Soon.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.