Summary of key points: -

- Another blockbuster US jobs increase

- Will the RBNZ push-back against market interest rate pricing?

- What is really driving US dollar movements?

The year started just over three months ago with the US interest rate markets pricing-in five x 0.25% (1.25%) of cuts for this year as the Fed pivoted in late 2023 on monetary policy settings. Today, the markets are only pricing in just two x 0.25% (0.50%) cuts over the remainder of the year and the probability of the first cut being in June has now dropped to below 50%.

What has changed so dramatically with the US economy over this three-month period to cause such a sudden reversal in expectation and sentiment by the markets?

Two major factors are behind the change: -

- The number of new jobs being added by the economy has increased significantly above all forecasts. Last Friday’s Non-Farm Payrolls increase of 303,00 for March was the fourth monthly blowout in a row. Prior consensus forecasts were for a 200,000 lift. A stronger than expected labour market pushes wages and inflation upwards - so the economic theory goes.

- Oil prices (WTI) have increased 24% from US$70/barrel on 1 January 2024 to US$86.70/barrel today, making it a lot harder for annual inflation to reduce over the “last mile” from the current 3.00% to the Federal Reserve’s target of 2.00%.

Whilst the interest rate markets are riled by these fresh inflationary pressures, the evidence that the Fed are suddenly about to change tact from their stated intention of three x 0.25% interest rate cuts this year, is not so strong.

In the foreign exchange markets the US dollar, as would be expected, appreciated strongly when the higher jobs data was released last Friday. However, the immediate USD gains from 104.00 to 104.46 on the USD Dixy Index proved to be short-lived. Accompanying the jobs data was the Average Hourly Earnings (wages) measure which increased 0.30% for the month of March, reducing the annual wages increase to 4.10% (the lowest level since mid-2021). The USD value reversed back to 104.04 as the markets realised that the robust growth in jobs was not necessarily transferring into higher wage pressures and inflation. The NZD/USD exchange rate briefly dipped to 0.5985 during the day, however it subsequently recovered to 0.6020 when the USD fell back. What has become clear in the US economy over recent months is that higher immigration inflows is increasing the supply of labour and therefore not causing wages to increase. Robust jobs growth without upwards pressure on wages is evidence of a stronger, non-inflationary GDP growth, which is why US equity markets rallied higher again last Friday (despite bond yields increasing). The second measure of US employment is the Household Survey, it recorded a significant surge of employed people in March of 498,000, following large losses over the preceding three months. More than half of those employment increases in March were part-time jobs. As has been the case for most of the last 12 months, the increase in new jobs was in the healthcare and government sectors.

The FX and interest rate markets will now be focused on this week’s (Wednesday April 10) US CPI inflation reading for March. Another 0.30% monthly increase is expected, reducing the annual rate of inflation from 3.40% to 3.20%. Of particular interest will be the impact of higher crude oil prices on gasoline prices at the pump and airfares, as well as the much delayed (but material) reductions in rents/housing costs. Attention will then turn to the Fed meeting on May 1st and whether they see the stronger jobs trend feeding into elevated inflation risks, or not?

Will the RBNZ push-back against market interest rate pricing?

At their last Monetary Policy Statement in late February, the RBNZ stated that they did not anticipate cutting interest rates until early 2025 as the inflation rate remains significantly above their 1.00% to 3.00% target band. Despite that clear message, over recent weeks the local interest rate market has moved to price-in two to three 0.25% cuts this year, commencing in August. The markets, following bank economist deliberations, are convinced that a contracting economy will automatically and dramatically reduce inflation over coming months. If only it was that simple!

The RBNZ have a choice with their interest rate review statement this Wednesday at 2pm, either push-back against the market pricing as being premature or not comment at all on current market pricing. Should they choose the latter route it would be taken as a tacit endorsement of current market pricing of much earlier interest rate decreases – a complete turnaround in the RBNZ’s position over the last 30 days. The NZ dollar would depreciate on its own account if the RBNZ select the second route. A clear statement from Governor Adrian Orr that the interest rate market is too far ahead of itself with current pricing would be Kiwi dollar positive.

Evidence in favour of the RBNZ pushing back is the fact that oil prices are higher, and the NZD/USD exchange rate is lower since their last inflation forecast just over a month ago. The RBNZ forecast for inflation for the March quarter (released Wednesday 17th April) is an increase of 0.40%, reducing the annual inflation rate from 4.70% at the end of December 2023 to 3.80% at the end of March 2024. Current consensus forecasts are for an increase of 0.90% for the March quarter, which will result in an only minor fall in the annual rate of inflation from 4.70% to 4.30%. There is no evidence yet that the rampant price increases coming out of the public sector over recent years has suddenly stopped because the Government has changed. If the Luxon Coalition Government were really serious about reducing inflation (as they say they are) they would have implemented a pricing freeze on all Government departments and entities. They have not done so, and therefore the high wage increases in the public sector continue to feed through into all sorts of price increases on to the average NZ household. Domestic non-tradable inflation continues at its “sticky-high” rate of increase in New Zealand, the market economists and interest rate markets have lost sight of this fact.

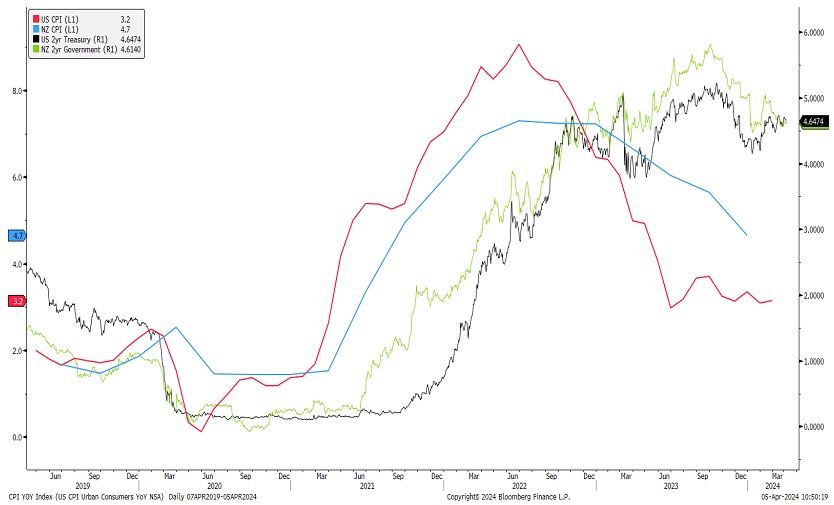

The chart below plots annual inflation rates (left-hand axis) in New Zealand (blue line) and the US of A (red line) against the respective two-year Government Bond interest rates (right-hand axis).

The New Zealand two-year interest rates (green line) closely tracks US interest rates (black line), however typically at a margin above the US rate. Today the NZ and US two-year interest rates are equal at 4.75%. Both central banks have their official interest rates set at 5.50%, therefore both interest rate markets are pricing near to three x 0.25% cuts this year. The stark difference is that New Zealand’s annual inflation rate at 4.70% is significantly higher than the US inflation rate which will be 3.20% to the end of March. The aggressive NZ interest rate market pricing is based on the premise that our annual inflation rate will plunge over coming months to below 3.00% to match the US inflation rate.

The current US interest rate market pricing is the exact opposite, their markets in pricing the two-year interest rate at 4.75% must be convinced that US inflation is going no lower and will increase sharply over coming months. Both interest rate markets seem unlikely to be correct.

Based on evidence emerging over coming months that US inflation continues to fall to the 2.00% Fed target, the US two-year interest rate is likely to be totally re-rated from 4.75% to closer to 4.00%. The NZ two-year interest rate is more likely to remain stable as the RBNZ push-back against earlier interest rate cuts. The widening of the interest rate gap back in favour of New Zealand will lead to a lift in the NZD/USD exchange rate from current levels.

What is really driving US dollar movements?

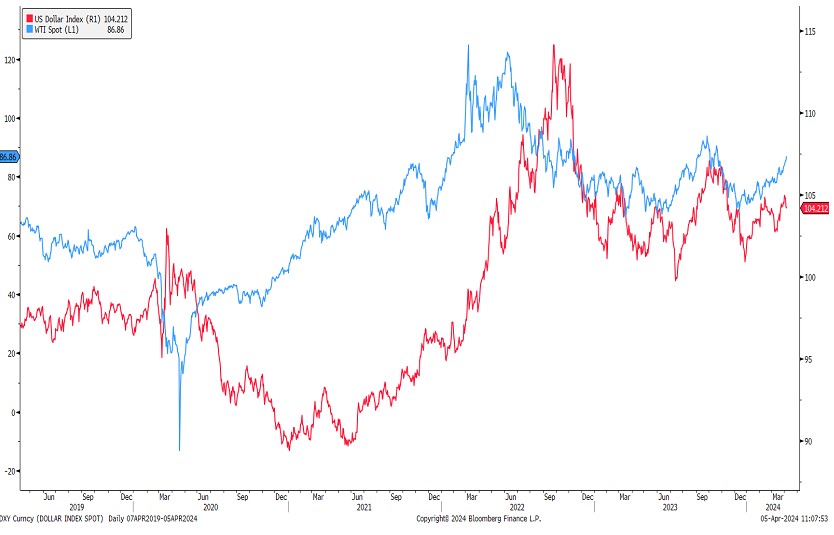

Currency market convention for many years has been that the US dollar value moves inversely to crude oil prices. The economic and market rationale being that Europe and Japan need stronger currencies in periods of oil price increases (priced in USD) so that imported oil costs in EUR and JPY terms remain stable. Therefore, historically the USD depreciated when oil prices increased. Over recent years, the inverse correlation relationship has been blown out of the water. The US dollar (USD Index red line, right-hand axis in the chart below) has closely followed oil prices (blue line) up and down since 2020. Higher oil prices increase US inflation and interest rates is how the FX markets are currently seeing it. Middle-East tensions and bombed Russian oil refineries are currently hitting the supply side of oil. The higher oil prices will stimulate more supply from the non-OPEC producers and that may well halt the current price climb. The level of oil inventories held in the US play a significant role in the supply/demand equation that drives the oil price. Over recent weeks, US inventories have been increasing again, also suggesting that oil price increase (and the USD) may be running out of steam.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

3 Comments

Thank you Roger Kerr for the excellent analysis.

Please stop this perpetual adoration Mrs Kerr.

I always look for your take Roger. With the flooding in the Urals another Russian refinery is out for the present. As well I see the Russians are looking for an increase in payments from Malaysia and others.

I think New Zealand is going to be hurting on the inflation front for much longer. I suspect we are going to have a rerun of the 1970's.

The US dollar has also been tracked by Bitcoin which I am just observing for that one I can't plumb.

Gold rising makes sense. Especially if you're Turkish and have 67% inflation.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.