Summary of key points: -

- Hallelujah! – the RBNZ finally recognise the sticky domestic inflation problem

- Mixed messages from Fed members, however the economic data will determine the US dollar’s fate

It was another episode of the “Shock and Orr!” drama series last week with the Reserve Bank of New Zealand (“RBNZ”) yet again wrong-footing both the economic pundits and financial markets with a surprise “hawkish” monetary policy statement. Widely expected interest cuts this year (never the view of this commentator) have been shunted right off the table by the RBNZ as they belatedly recognise the problem with continuing high inflation from domestic sources that are not interest rate sensitive. In explicitly singling out local government rates, rents, insurance and building costs as the inflation culprits, the RBNZ have finally done their homework on the component parts of domestic non-tradable inflation to see the problem, rather than just relying on their macro-economic model. Readers will understand this column has been banging on about the permanent nature of continuous price increases from the public sector in New Zealand for many months. That price setting behaviour has none of the discipline that competition ensures occurs in the private sector. It is reassuring that the RBNZ now understand the reasons why it is proving difficult to reduce inflation from 4.00% to 2.00%. However, it is certainly worrisome that it has taken them so long to highlight the root causes. Not that the higher interest rates/tighter monetary policy would have changed any of the behaviour of the public-sector price setters. A tighter control on Government legislation and regulation to ensure changes are not inflationary is what is required. However, the previous Labour Government and even the RBNZ themselves have been very lax on that front. If the RBNZ are carrying out their job as the guardians of price stability they should have a duty to “call-out” potential causes of inflation emanating from the public sector. Unfortunately, they will tell you that their mandate does not go that far.

The local interest rate market were misguidedly pricing-in interest rate cuts before the end of 2024 based on the forecasts from bank economists that a contracting economy will automatically cause unemployment to increase, and that would automatically (through the demand transmission mechanism in the economy) cause aggregate demand to decrease, therefore pulling inflation down. Yet again, the economic theory has proven to be far removed from the reality of sticky inflation lasting for longer for the reasons outlined above. However, a bouquet to the RBNZ for finally fronting up to that reality and delivering a justifiably hawkish statement that the markets did not expect.

However, the RBNZ have also earned a brickbat for some weirdly confusing and wishy-washy signalling to the markets. The forward interest rate track the RBNZ published in the statement confirmed a higher and prolonged profile for the OCR. That is normally interpreted as a message that further tightening in monetary policy is required. However, they contemplated increasing the OCR, but in the end decided against that. In the subsequent media conference, the RBNZ Chief Economist Paul Conway attempted to explain that the forward interest rate track is purely a mechanistic output of their macro-economic model and is derived from what level of interest rates are required to deliver their inflation forecasts. Mr Conway went on to say that the market should not read too much into that interest rate forward track as subsequent economic data results and other uncertainties could change it. He also suggested that the RBNZ could publish alternative future interest rate movement scenarios under alternative economic developments. All a bit messy in terms of clear signalling of their intentions to the markets and the wider economy. If the RBNZ do not want the markets to over-react to a higher interest rate track in their statement, then do not publish the interest rate track in the first place.

The net/net conclusion from this classic Governor Orr “blindsiding of the markets” event is that the RBNZ have underestimated ongoing inflationary pressures, they have not had interest rates and/or the currency value high enough and therefore they are threatening even tighter policy for longer, some 18 months after commencing the tightening cycle. The result is that the lagged and negative impact of tight monetary policy on the economy is extended for even longer than what most contemplated. Our column has warned of this likely scenario for several months now, so it comes as no great surprise.

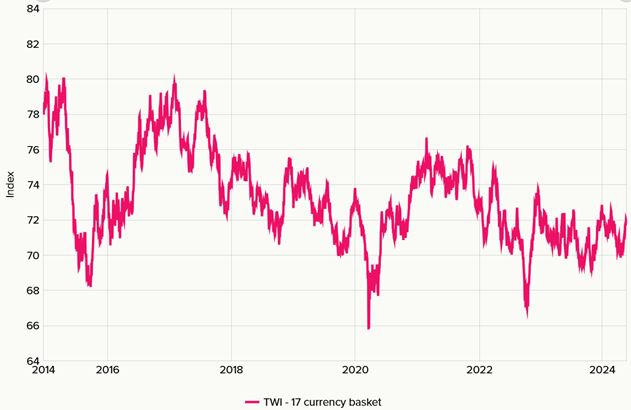

The implications for the NZD/USD exchange rate is that likely lower US inflation, interest rates and US dollar value over coming months will be in stark contrast to NZ interest rates being “higher for longer” over the remainder of 2024. Therefore, the renewed vigour of the RBNZ to push inflation down with a tighter monetary policy is certainly NZ dollar positive on its own accord. The initial FX market reaction was to buy the Kiwi dollar on the surprise change in the RBNZ’s stance, the NZD/USD rate jumping from 0.6100 to 0.6145 on the day. It has settled at 0.6125 over recent days, outperforming other currencies against a marginally stronger USD. Overall, the NZ dollar has recovered back to 72.00 on the Trade Weighted Index (“TWI”) from below 70.00 two weeks ago (refer chart below). Arguably, the TWI must be nearer 75 or 76 to be consistent with having negative tradable inflation to offset the permanently high non-tradable inflation to achieve the RBNZ 1.00% to 3.00% inflation target band.

Mixed messages from Fed members, however the economic data will determine the US dollar’s fate

There has been a barrage of speeches from both voting and non-voting members of the Federal Reserve’s FOMC committee over this last week. Most are painting a picture of US interest rates needing to be held at the 5.50% restrictive rate for a bit longer yet as they gain more confidence that inflation will recommence its track lower to 2.00%, having stalled above 3.00% over the first three months of 2024. The tone of the Fed member’s views has certainly been more on the hawkish side of the stance projected by Governor Powell at the last Fed meeting, wherein he ruled out any further interest rate increases and could see cuts this year if the economic data printed as they expected. We have previously stated that the Fed members will need more than one month’s worth of softer inflation and employment data (April numbers were below forecast for both) to have sufficient evidence to make the decision to cut their official Fed Funds interest rate.

The US interest rate and FX markets await the May and June inflation and jobs figures with high expectation, as if they are also softer following April figures, the signal to buy bonds (in expectation of lower interest rates) and to sell the US dollar will be a strong one. Upcoming US inflation and employment data releases are as follows: -

- Friday 31 May: PCE Inflation Price Index for April (+0.20% forecast for the month = 2.60% annual).

- Friday 7 June: Non-Farm Payrolls (new jobs) for May (a softer 150,000 increase is forecast).

- Wednesday 12 June: CPI Inflation for May (current annual headline rate to 30 April is 3.40%).

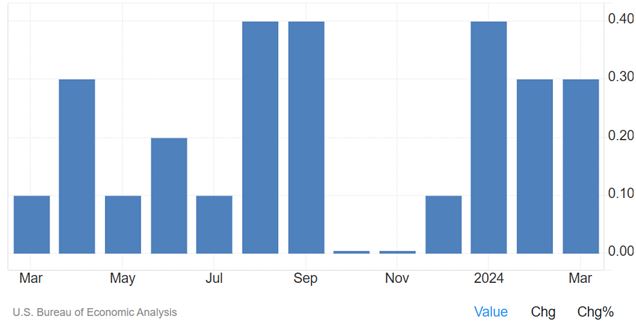

As can be seen by the chart below, the monthly PCE inflation increases in 2023 were very low through the May to July period, therefore the current annual PCE rate of inflation will stay stable at 2.60% over coming months. When the larger monthly 0.40% increases in August and September 2023 drop out of the calculations, the annual PCE rate should hit the Fed target of 2.00%. However, Governor Powell has stated on several occasions that they will not wait until the actual inflation rate is 2.00% before they commence to cut interest rates. The markets are pricing a 60% probability of a 0.25% cut by the Fed in mid-September, however if the inflation and jobs data is weaker in May and June, an earlier cut at the 31 July Fed meeting should not be ruled out. If that occurred, the US dollar would depreciate.

US PCE Inflation – Monthly Change %

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

8 Comments

In explicitly singling out local government rates, rents, insurance and building costs as the inflation culprits, the RBNZ have finally done their homework on the component parts of domestic non-tradable inflation to see the problem, rather than just relying on their macro-economic model. Readers will understand this column has been banging on about the permanent nature of continuous price increases from the public sector in New Zealand for many months.

Only one of those four main culprits is in the public sector, so it looks like the private sector is as much if not more to blame for the sticky inflation.

In NZ "local inflation" has been a problem for years - hidden by imported deflation. If the NZRB is only just recognising this issue then they need a dont come monday card

And nothing in their report to show that they have any clue as to what changes in the macro environment will be required before they change OCR

I despair - an omnipotent RB thats clueless, Govts that cant make tough choices, bureaucrats that huiey instead of doey and a public that still thinks the Govt will/should provide to meet their needs what ever they happen to be

Correct but it doesn't suit Roger's narrative.

"As can be seen by the chart below, the monthly PCE inflation increases in 2023 were very low through the May to July period, therefore the current annual PCE rate of inflation will stay stable at 2.60% over coming months."

Staying stable would be a good result. The risk is that May-Jul 2024 leads to increases back towards 3% YOY.

"When the larger monthly 0.40% increases in August and September 2023 drop out of the calculations, the annual PCE rate should hit the Fed target of 2.00%. "

There is already a cumulative 1.1% from Oct 2023-Mar 2024. It is going to need six months of 0.15% MOM on average to hit 2%, compared to recent months of 0.3%-0.4% MOM. The cumulative 1% over Jan - Mar 2024 could delay getting to the 2% target a bit further as the very low Oct-Dec 2023 are replaced with Oct-Dec 2024 actuals.

Left-wing councils like Nelson could care less about feeding inflation, but continue on their merry way with lavish spending on grand projects that are not essential.

Some of the council rates increase is due to delayed effects of inflation as contractors roll off fixed prices on rates set in 2020.

Will the Central Bank's cash rate still be 5.50% when they open up and let the public keep their cash there? (CBDC).

There is little to nothing RBNZ can do about non-tradeable inflation. They can't stop Councils putting up rates by 10%+.

So, the RBNZ slams down harder on tradeable inflation to compensate, screwing the economy harder than needed and dumping more people on the dole queue.

Central govt is too incompetent to address the other inflation issues which it mainly owns.

Council rates - monopoly - Central govt issue - Central govt needs to sort out its funding arrangements with local govt. It could start with paying rates on central govt land to remove the subsidy it enjoys.

Rents - Central govt issue. Unsustainable immigration rate & not enough houses built

Insurance - Weather & crime related but also an oligopoly. There's not much competition now. The crime issue is a central govt issue. Neoliberal policies in NZ since the 1980's have decimated the poor and reduced social cohesion.

Building costs - Oligopoly & Central govt issue. Unsustainable immigration rate means pressure on house build prices & the building supplies oligopoly hasn't been addressed.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.