Summary of key points: -

- Trump’s poll ratings at home will end the war before anything else

- Are migration numbers and house prices influencing the NZ dollar value?

- Play it again Sam! – Will the Kiwi dollar follow the Aussie dollar playbook?

Trump’s poll ratings at home will end the war before anything else

US President, Donald Trump measures his success in improving the US economy for the masses based on the share market going up, interest rates going down and gasoline prices also going down (remember “drill baby, drill!”). Since he started the Iranian war with the Israeli’s four weeks ago, all three so-called economic indicators are going the wrong way for him. Trump states that this is a small price to pay for riding the world of a rogue, nuclear threat power. The problem for Trump is that unless he ends the war within a few weeks, his political runway at home runs out. He surely understands the risk of becoming a “lame duck” President for the last two years of his term if the Republicans lose the House of Representatives and the Senate at the November mid-term elections.

Therefore, the two real determinants of the timing of the war ending (and oil, US dollar and interest rate prices reversing) and Trump declaring a “victory” are: -

- Ships passing through the Strait of Hormuz without threat of Iranian attacks. How and when the Americans achieve this remains unknown. The FX, bond, currency and oil markets backed up the bus last Friday when a Chinese ship was refused free passage through the Strait.

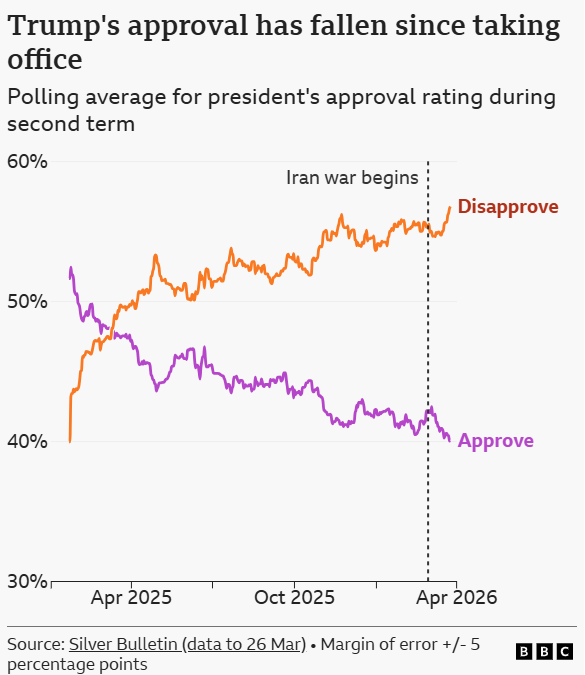

- Further deterioration in Trump’s own approval rating by the American public forcing him to terminate the war sooner rather than later (Iranian regime change or not). As the chart below displays, Trump’s latest approval rating has dropped to 40%. Independent voters are now also turning against Trump, in addition to the Democrat voters. A further reduction to below 40% would force Trump to end the war for his own domestic political reasons.

Outside of these two “market changing” eventualities, all the markets are increasingly skeptical towards Trump’s ever-changing two-day, four-day and now 1o-day ultimatums to some illusory Iranian Government leaders. Over the next eight days, until the expiry of the latest 10-day ultimatum for the Iranians by 6th April, Trump has to stop the Israeli’s bombing and agree a deal with the Iranians that allows safe and free passage through the Strait of Hormuz. It seems a tall order. Trump’s track record of succeeding with ultimatums has not worked too well in the Ukrainian/Russian war and therefore the markets are currently ascribing a low probability of it working here. However, that situation can change quickly as no-one really knows what is going on inside Iran and it would not be surprising to this writer that the Iranian military and Government suddenly capitulate without warning.

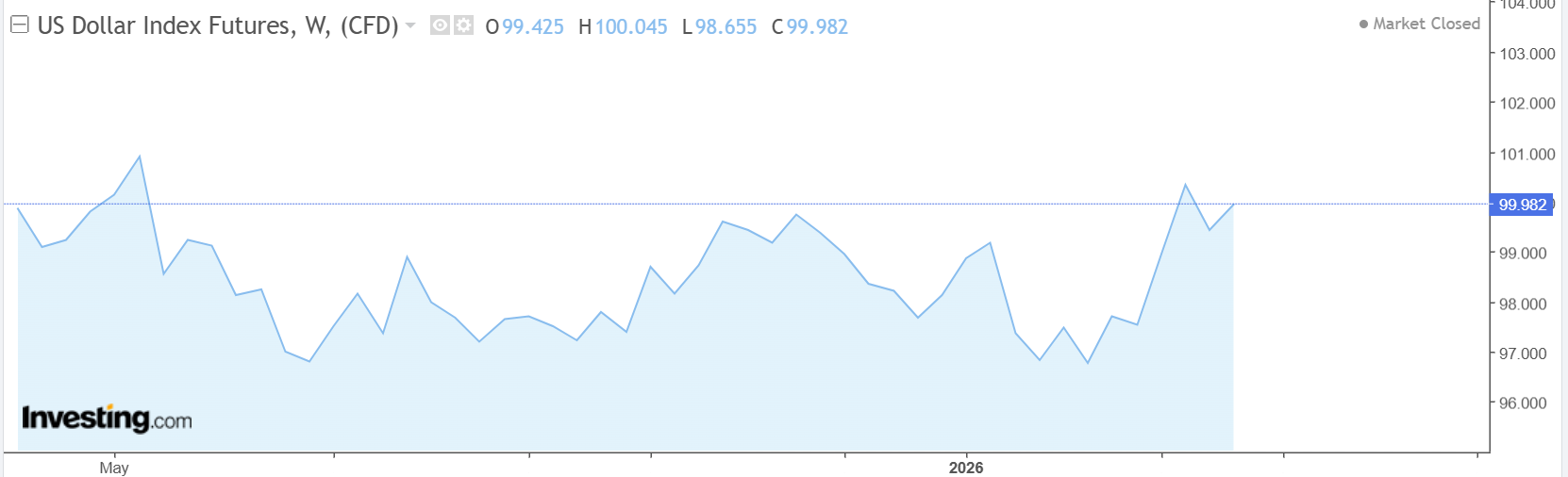

What we do know, is that the oil price will continue to race up and down on every new piece of military, diplomatic or Trump news. It does seem that the latest sell off in the WTI oil price to US$99.60/barrel is pricing-in a worst-case scenario of Trump getting to the end of his 10-day ultimatum period with no further progress and the missiles into Iran recommence. The USD Dixy Currency Index has appreciated again to 100.00, following the oil price higher. As a consequence of the latest bout of USD strength, the NZD/USD exchange rate has been forced to return to the bottom of its trading range at 0.5750. The USD has encountered considerable resistance from trading above 100.00 over the last 10 months, therefore it would need something like an oil tanker being sunk by the Iranians in the Strait of Hormuz to engender further strong USD buying.

Are migration numbers and house prices influencing the NZ dollar value?

Many factors influence the direction and level of the NZD/USD exchange rate at any point in time. Some factors will dominate for a time and then reduce as global and local conditions change. Not necessarily in strict order, we would list the following factors as the key influencers: -

- General USD movements against the major currencies.

- Interest rate differentials – “carry trades” appreciating the NZD when NZ interest rates are above those of the US (and vice versa).

- Strong correlation to the AUD/USD movements – reduced when the Trans-Tasman interest rate differential is wide, as it is currently.

- Central bank decisions with monetary policy to control inflation – particularly the RBNZ.

- Relative economic performance (GDP growth, Balance of Payments Current A/c Deficit, Budget Deficits, credit rating etc).

- Export commodity prices – once dominated, currently off the radar.

- Performance of the Chinese Yuan and the Chinese economy – our largest export partner.

- Inwards and outwards capital flows – incorporating net migration and NZ house prices.

We examine and run commentary on the first seven factors on a regular basis, attempting to determine the strength of influence of each factor to explain NZD/USD movements.

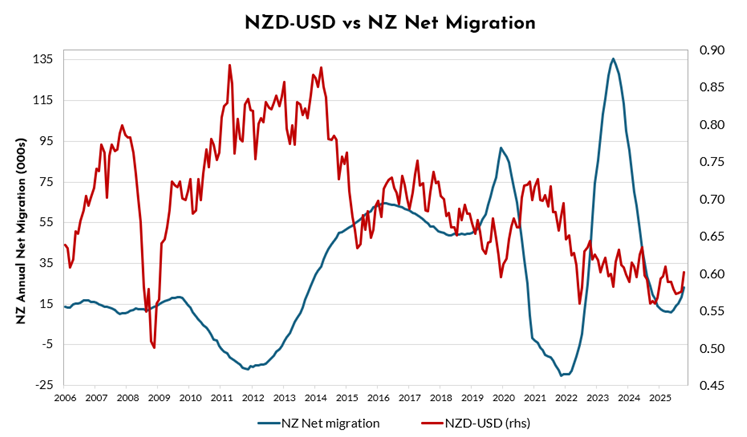

The argument goes that strong inwards migration into New Zealand not only brings the immigrant’s funds into the Kiwi dollar, it is also a reflection of the strength of the economy and its ability to attract new immigrants. Therefore, increased net migration is positive for the Kiwi dollar (and vice versa).

Unfortunately, our immigration policies over the years have been changeable and inconsistent, causing large swings in the numbers for net migration. As the chart below shows, other factors have been more determinant on NZD/USD exchange rate movements over the last 20 years than net migration numbers. The significant increase in net migration in 2022/2023 did not cause any NZ dollar appreciation. Likewise, the sharp drop off in net migration in 2024/2025 was not a factor pushing the NZ dollar down.

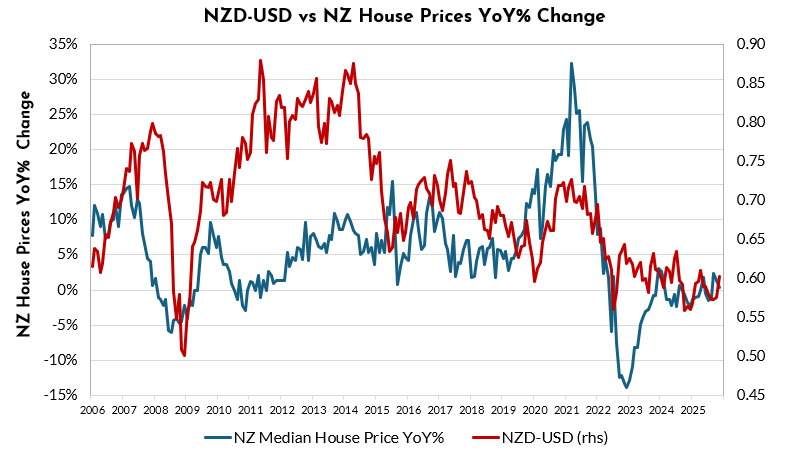

The influence of local house prices over the NZD/USD exchange rate movements is a little more interesting. This argument goes that rising house prices (for whatever reason) causes higher general inflation as the “wealth effect” drives higher consumer spending, as house owners believe they have more money as the equity level in their house increases. The RBNZ tightens monetary policy to bring inflation down, interest rates increase and that in turn attracts funds into the Kiwi dollar on “carry trades”. House prices reduce when the economy goes into recession and unemployment rises. In recent years the recessionary periods have been largely caused by RBNZ monetary tightening. The recessions and lower house prices eventually cause a loosening in monetary policy, lower interest rates and a lower NZ dollar value.

There has been a loose connection between the rise and fall of house prices and the Kiwi dollar since 2019. Currently, house price movements are flat, and the NZD/USD rate has been stuck between 0.5700 and 0.6200 for quite sometime.

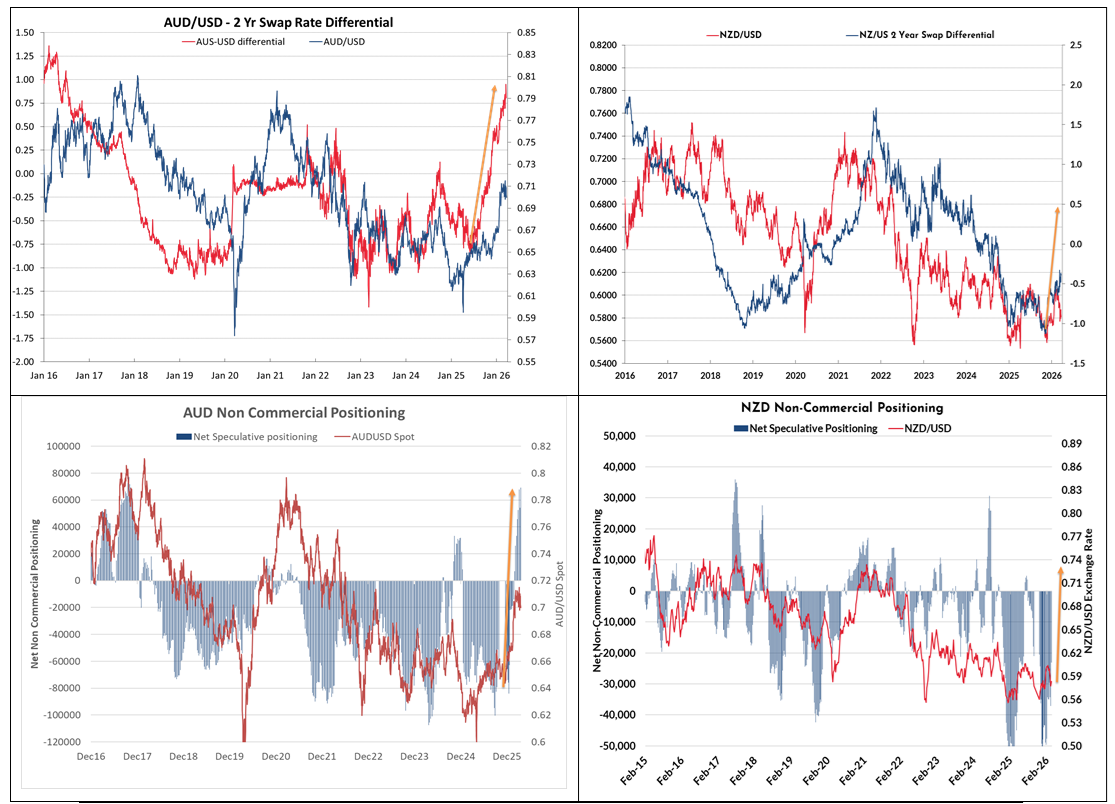

Play it again Sam! – Will the Kiwi dollar follow the Aussie dollar playbook?

The appreciation of the Australian dollar against the US dollar over recent months has been nothing short of spectacular. The sudden and dramatic change in the interest rate differential between Australian rates and US rates in late 2025/early 2026 (from -0.75% to +1.00% - red line in the top left chart below) drove the Aussie dollar up from 0.6400 to 0.7000 against the USD. The AUD “Non- Commercial Positioning” chart below on the left-hand side confirms how the AUD currency speculators shifted from being “short-sold” the AUD (blue bars) to today being 60,000 futures contracts “long-AUD”.

The open question for the future direction of the NZD against the USD is whether a change in the interest rate differential between New Zealand and the US will also stimulate similar NZ dollar gains on its own account? The NZD/USD charts against the interest rate differential and speculative positioning are on the right-hand side below. In November 2025, NZ two-year swap interest rates were 1.00% below those of the US. Today that gap has closed up to -0.40%. The Aussie dollar playbook would suggest that NZ interest rates have to move above US rates to change the speculative market positioning to buy the NZD aggressively. Under the “early end to the war” scenario it would be expected that US two-year swap rates will reverse their 0.50% climb to 4.00% over this last month of the war. New Zealand two-year swap rates might come down a little, however they will still price OCR increases this year. In contrast, the interest rate market pricing in the US would return to Fed interest rate cuts ahead. Both New Zealand and Australia have inflation rates above 3.00% pa. The RBA is arguably six months ahead of the RBNZ in tightening monetary policy (the Aussies did not have a minor recession in 2024). It does seem likely that the NZ dollar will follow the AUD playbook.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

1 Comments

I'm disappointed with the entrenched status quo position of this article, particularly in relation to immigration and housing. Tinkering while Rome burns.

Trump is a wild card. Whether midterm election results can stymie him or whether they will even be held is an open question -he may declare a wartime suspension to traditional election cycles (that he criticised Zalensky for invoking - consistency and integrity are not Trump strong points).

As far as the Iran war ending within the next month, the only possibility I can see goes along the lines of: (Trump) "I feel it in my bones it's time to pull out, I always wanted to be a wartime president. It's been great fun. Now I want to get back to the important stuff, like building the gilded ballroom". (Interviewer) "But what about the critical choke points in the Persian Gulf and Red Sea?" (Trump) "Oh well, not my problem really. This is my last term as President so I'm going to ensure I enjoy myself while it lasts".

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.