Summary of key points: -

- Will the up and down Kiwi dollar trading pattern keep repeating?

- Oil prices lower and the US dollar lower as the Iranian war runs its course

The NZ dollar finally broke out above its previous resistance point at 0.5920 this last week. The next major level to climb above is 0.6000, which the NZD/USD exchange rate has not traded above since mid-February, just before the Iranian war started.

Over the last five years, the Kiwi dollar has remained below its long-term downtrend line that has remained in place since the peak of 0.7400 in February 2021 (refer to the chart below). An appreciation of the NZ dollar above 0.6000 over coming weeks will break above that downtrend/resistance line. Such a decisive break-out may well encourage short-sold NZD position holders that it is no longer that smart to be speculating that the NZD will depreciate. The punters are more likely to buy the Kiwi from there, reversing their spec positions from short-sold NZD to long-NZD. The converging wedge formation in the chart indicates a buying support for the NZD at 0.5700, and it is recently bounced off that level.

A further potential source of speculative NZ dollar buying is our Trans-Tasman cousins who aggressively sold the NZD against the AUD over recent months as the interest rate differential between the two currencies swung massively in the AUD’s favour. Looking ahead, that interest rate gap between NZ and Australia is likely to close up as the RBA in Australia end their monetary tightening cycle and the RBNZ need to adjust the OCR from super-loose at 2.25% to somewhere nearer neutral at 3.50%. From here, the NZD/AUD cross-rate punters are more likely to be closing down their short-sold NZD positions against the AUD, than adding to them i.e. independent NZD buying.

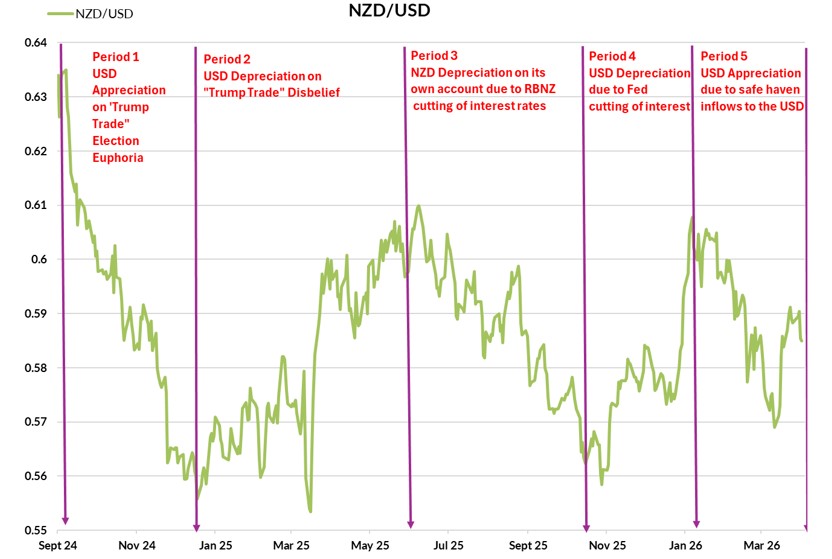

A reflection back on the numerous up and down NZD/USD exchange rate movements over the last 20 months since September 2024 reveals five distinct periods, two upwards and three downwards: -

Period 1. The NZD depreciated through November and December 2024 against the stronger USD from the level of 0.6350 in October 2024. The USD appreciated on the “Trump Trade” US election euphoria.

Period 2. The NZD appreciated from a low of 0.5550 in mid-January 2025 to 0.6100 by June 2025. The USD depreciated on the unwinding of the Trump Trades and disbelief on the tariffs i.e. the “Sell America” FX trade at the time.

Period 3. The NZD depreciated on its own account from June 2025 to November 2025 as the RBNZ made successive OCR interest rate cuts to 2.25%. NZ interest rates well below the US rates hurt the NZD.

Period 4. The NZD appreciated from 0.5600 in November 2025 to above 0.6000 in early February 2026 as the US Federal Reserve cut US interest rates and NZ economic data improved i.e. the export-led economic recovery that we were banging on about last year.

Period 5. The NZ depreciated in March 2026 to a low of 0.5700 in the face of a stronger USD on safe have inflows as a result of the increased geopolitical risk on the commencement of the Iranian war. At 0.5980 today, the Kiwi dollar has already largely recovered that lost ground to the USD.

As we look forward, what we may conclude is that the bouts of US dollar appreciation due to Trump decisions on tariffs and attacking Iran are unlikely to repeat, as Trump’s Republican Party faces serious losses in political power at this November’s mid-term Congressional elections. Trump and the Republicans will need to focus on fixing damaging domestic economic issues such as household affordability to shore up any political support. Major economic or geo-political initiatives or changes are unlikely over coming months; therefore, risk events that boost the US dollar’s value are not likely to occur. Currency traders and hedge funds will therefore likely return to underlying economic fundamentals and changing interest rate differentials as reasons to buy or sell any particular currency.

As the global foreign exchange market environment transforms from reactive to shocks/risk events and start to be driven by economic and investment changes, undervalued currencies such as the Japanese Yen and the Kiwi dollar should attract renewed attention.

Off course, there will be new shocks/risk events ahead that we do not yet know about. However, they are impossible to forecast in advance and therefore cannot be factored into any assessment for future exchange rate direction. What we do know is about is relative economic performance and relative interest rates, which at the end of the day, will drive realignment of currency values as the weight of investment and speculative flows force different exchange rate pricing.

Oil prices lower and the US dollar lower as the Iranian war runs its course

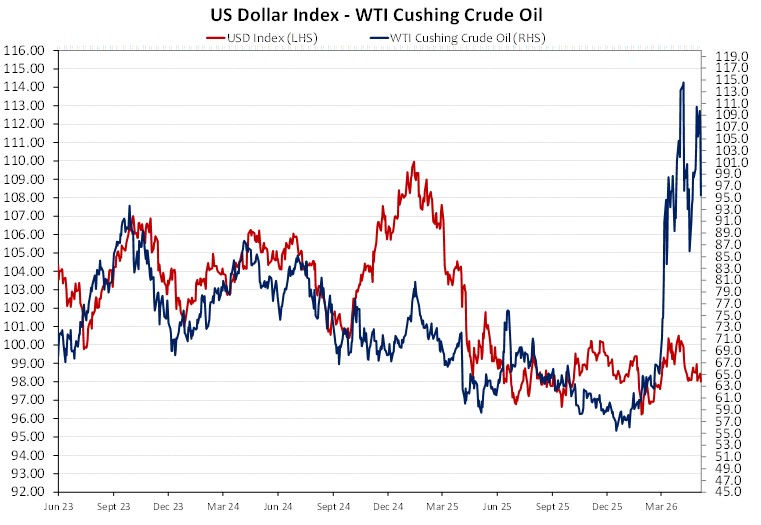

Developments in the Iranian war remain pivotal for the US dollar currency value as the foreign exchange markets continue to buy the USD on any escalation of the war and sell the USD on de-escalation. Should a peace deal be struck between the Americans and the Iranians and the Strait of Hormuz is re-opened, we would have to expect the WTI oil price to plunge to the sub-US$70/barrel area where it was trading before the war started. It will not be the oil producers selling oil futures contracts, but large hedge funds unwinding their “long-oil” speculative positions taken out when the war started.

Over recent years, the WTI oil price has become positively correlated to the US dollar value (refer to the chart below) as the US become a net oil exporter. Trump may think that the US having more of an influence over the global oil markets than the Arabs is positive for the US economy, however it may prove to be negative for the US dollar value. The war in nearing its inevitable end (in our view), however Trump’s own flip-floppy positioning is probably making it harder to secure a peace deal to end the conflict, that he so desperately needs. Whilst it may take several months for the global oil supply situation to normalise once the Strait is re-opened, the oil market price reaction to lower levels will be immediate as the speculators sell out of their contracts on the risk disappearing.

It has to be expected that the Chinese are playing a pivotal role behind the scenes to get the Iranians to agree to the current US proposal to end the war. The week ahead may well hold the key on these global geo-political developments with Trump visiting Premier Xi Jinping in Beijing on 14 and 15 May.

As geo-political factors come to an end as the driver of US dollar direction, the markets will focus back on trends in the US economy. The media headlines last Friday were that the US Non-Farm payroll jobs increase had beaten expectations two months in a row (March and April). The accompanying economic commentary was that the US labour market was in good shape, and this would make it harder for the Federal Reserve to cut interest rates this year, given the inflation increases. However, it was very instructive as to how the bond and FX markets reacted to the 115,000 increase in jobs in April. Typically, a stronger than forecast jobs increase would send bond yields higher and the USD higher. Contrary to expectations, US 10-year bond yields decreased on Friday to 4.36% (down from 4.45% over the full week) and the US dollar depreciated on the Dixy Index from 98.15 to close at 97.80 (down from 98.43 over the week). Clearly, the bond and FX markets do not trust the accuracy of the monthly-announced Non-Farm Payrolls data as fairly reflecting the true situation with employment trends in the US economy. The second employment survey of households was much weaker and is not prone to the large subsequent downward revisions in jobs increases that the Non-Farm Payrolls survey of business establishments is notorious for.

Released alongside the jobs data last Friday was the University of Michigan Consumer Sentiment survey for May. It was again weaker than forecast at 48.2 (down from 49.8 in April). It appeared that the bond and FX markets see softer consumer demand as a more up to date barometer on the direction of the US economy. It is not positive as households struggle with affordability issues, mostly related to the increase in gasoline prices. The financial markets will be looking to the US April core inflation figures this Tuesday for an indication on underlying inflation direction away from the oil price impact. Consensus forecasts are for core inflation to increase by 0.30% for the month.

The Euro made further advances against the USD last week as the prospects increased of the Ukraine/Russian war ending, following a three-day cease fire agreement. The EUR/USD exchange rate lifted to $1.1790. A return of the Euro to above $1.2000 will be positive for the Kiwi dollar.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.