Summary of key points: -

- What the Bank of Japan currency intervention on the Yen may mean for the Kiwi dollar

- A divided Fed: however, still too early to predict their next move

- What will more RBNZ transparency mean for the market?

The Japanese Finance Minister, Ms Satsuki Katayama provided plenty of warning to the markets last week that Japan was prepared to take decisive action against excessive Yen currency volatility. It was not just jawboning words to stop the Yen depreciation above 160 to the US dollar, the Bank of Japan followed through with direct intervention in the FX markets, buying Yen, selling USD. It was the first time that Japan has stepped into the markets in nearly two years and the first time under new Prime Minister Ms Sanae Takichi. Time will tell whether the intervention to turn the tide on the weakening Yen will be successful. In a classic FX intervention playbook move, the Bank of Japan timed their Yen buying ahead of public holidays for Golden Week, hoping that the normally lower market liquidity will provide more “bang for the buck” and extend USD/JPY movements. The Yen immediately strengthened from 160.70 to 155.50 on Thursday 30th April, the largest single day drop since December 2022. The purpose of the intervention is to burn off the currency speculators who have been selling Yen against the USD since the Iranian war started two months ago. Following the initial intervention action last Thursday afternoon, Japan’s top currency diplomat, Mr Atsushi Mimura was quick to warn the markets that they would act again if necessary and that Japan was working closely with the US on the intervention.

Our observation is that short-term FX market interventions will not be successful in driving the USD/JPY exchange rate significantly lower by itself, unless it is accompanied by a tightening of monetary policy by the Bank of Japan to further close up the interest rate differential between Japan and the US. Current estimates are that the Bank of Japan is preparing to lift their official interest rate from 0.75% to 1.00% in June. The Bank of Japan has become very slow at raising interest rates over the last six months as the Prime Minister was against such increases, stating that there were other ways of controlling inflation. PM Takichi is yet to announce what those alternative methods might be!

After reaching 155.50 on Thursday, the Yen has bounced back somewhat to close the week at 157.00. On the expectation that the FX markets will start to progressively price-in Japanese interest rate hikes, the Yen should advance to 150 and below as the short-Yen speculative position holders close down their trades by buying Yen. In an additional significant development in Japanese financial and investment markets, their 10-year Government Bond yield has increased to 2.50%, the highest level since February 1999. Soaring crude oil prices, coupled with a weaker Yen currency value, is combining to send Japanese inflation sharply higher, and this is what is scaring participants in their bond market. US 10-year bond yields are currently 4.37%, therefore the differential between Japanese and US bonds has closed up further to less than 2.00%. The chart below confirms the close historical correlation between the USD/JPY exchange rate and the gap between US and Japanese 10-year bond yields. The current dislocation between the two series has the Yen remaining weaker at 157.00, however the bond differential points to Japanese investment house returning funds home from the US as the substantially lower interest rate gap does not justify taking the FX risk to continue to invest in US bonds. The Yen strengthens as the investment houses buy Yen, sell USD to repatriate funds home from the US markets. It has seemed inevitable for some time now that the USD/JPY rate would follow the bond differential lower, maybe it just needed a catalyst to start the Yen buying and that has now occurred with the Japanese intervention.

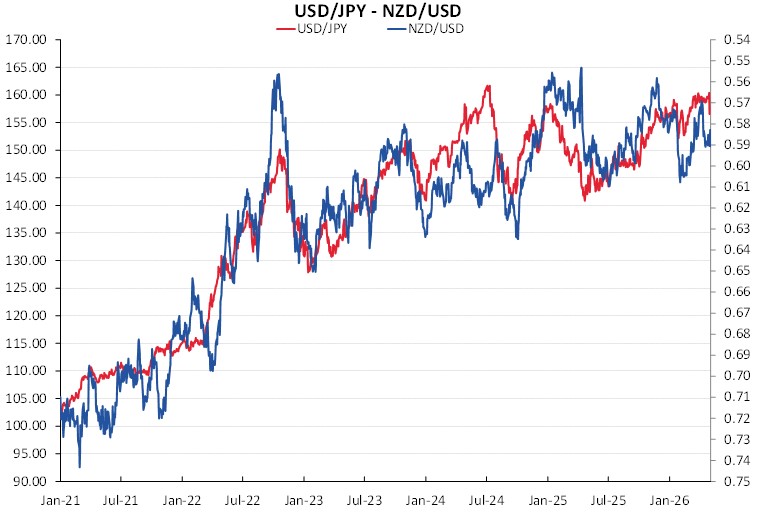

The tight correlation between the USD/JPY exchange rate and the NZD/USD exchange rate continues. One good reason why the Kiwi dollar has not been sold below 0.5500 over recent years when NZ interest rates have been well below US interest rates, is because the Yen has been halted from weakening above 160.00. The Japanese Yen is the dominant freely traded currency in the Asian region, given the dependency of our economy on China, Australia and Asia is makes sense that our currency is closely aligned to the Japanese Yen. When the Yen does catch up to the bond differential and appreciate to 140 and lower against the USD, it will move faster than the Kiwi dollar, resulting in the NZD/JPY cross-rate downshifting from the current 92.50 to closer to 85.00.

A divided Fed: however, still too early to predict their next move

The US Federal Reserve left interest rates unchanged and their meeting last week, they also left the wording in their statement unchanged, which meant that the “additional adjustment” forward guidance for likely further cuts to interest rates remained. Three voting FOMC members dissented and voted against retaining that forward guidance wording. There was no surprise in seeing who the three dissenters were. Predictably, they were three renowned “hawks” on the voting committee, namely, Ms Lorie Logan, Ms Beth Hammack and Mr Neel Kashkari. Fed watchers would single these three members out as consistently warning about rising inflation and the need the tighten monetary policy further from the already moderately restrictive level of 3.50% - 3.75%. Eight members voted to retain the easing bias, with Trump’s man, Stephen Miran again voting for interest rate cuts. Fed Chairman, Jerome Powell is not getting the full consensus on interest rate decisions that he has always strived for. It is a very difficult time for all central bankers as no-one knows how long the Iranian war will last and oil prices remain high. The message from Chair Powell is that is still too early to state that the war and energy shock will only be a temporary spike up in inflation, which the Fed can “look through”, or will a prolonged continuation of the war mean that inflation increases are more permanent and therefore interest rates need to be increased. The US short-term interest rate markets are no longer pricing-in cuts by the Fed this year, however they are not (at this stage) pricing interest rate hikes either. The waiting game continues for the Fed.

Chair Powell has apparently upset Trump’s henchmen by stating that he will stay on as a normal member of the Fed for an undefined period after Kevin Warsh takes over from him as Chairman on 15th May. Trump was hoping that Powell would resign his position (he has two years to run on his term as a governor) and allow a new Trump appointee who will favour lower interest rates. Jerome Powell states that want to see the Trump legal cases against the Fed through to closure, before deciding if he will stay or go. There is more to play out in this little stoush, as Trump will struggle to legally fire Mr Powell. The markets worry about Powell acting as a “shadow chair” in the committee, still influencing Fed decisions as a normal voting member in 2026 and 2027.

The Fed has some tricky decisions coming up. If they do not cut interest rates they could send the US economy into recession. If they cut interest rates and resultant stronger economic activity keeps inflation well above 2,00%, they are outside their mandate.

What we observe currently is that there are conflicting and mixed messages of how well the US economy in travelling in early 2026: -

- Core CPI and PCE inflation results (excluding food and energy) over the first three months of the year have been in line with consensus forecasts with the tariff related price increase of 12 months ago starting to roll out of the annual inflation numbers and shelter (rents) still declining. If the war ends within the next few weeks, the Fed will still be cutting interest rates this year and that is negative for the US dollar value

- The labour markets is hard to read as to its true state, as the immigration policies of the Trump regime has reduced the supply of labour. The reduced supply numbers have matched the reduced demand, leaving the unemployment rate stable. However, the AI revolution is causing large worker layoffs at software and technology companies. Going on recent wild volatility in the monthly results, this week’s Non-Fram Payrolls jobs data is more than likely going to be far weaker than the 75,000 to 95,000 increase being forecasted. Hiring intentions in the recent ISM Manufacturing survey were particularly weak, collapsing to 46.4, well below forecasts of 49.0.

- The annualised GDP growth in the March quarter at +2.00% was marginally below consensus forecasts. Increased business investment in data centres to support the AI revolution dominated the GDP figures. Consumer spending increased at a slower +1.60% pace. Imports increased more than exports, the opposite of what Trump’s tariff policies are designed to do!

- A new report from credit reporting company TransUnion states that the “K-shaped” US economy is becoming more pronounced. Higher income households are increasingly better off with equity investment portfolios doing well, whilst lower income households are falling further behind. The report states that a large segment of consumers is facing higher costs and rising debt burdens. The gap between the rich and poor is widening. The bifurcated consumer economy in the US is arguably Trump’s greatest risk for how the votes go in the mid-term elections in November.

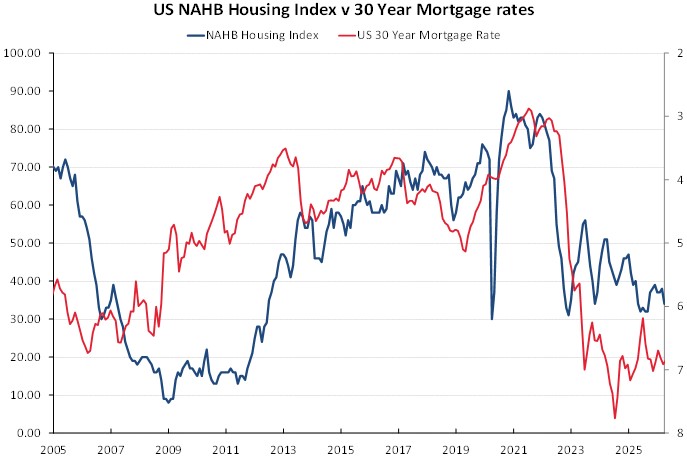

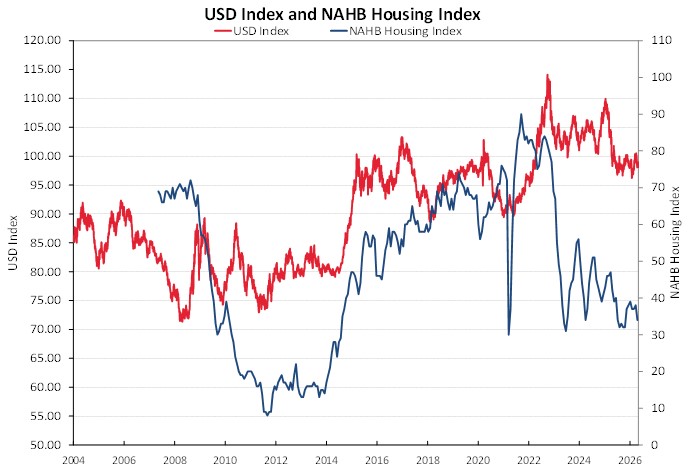

- The yield on 30-year Treasury Bonds has increased to record highs of 5.00%, pushing the fixed interest rate for new build mortgages to over 7.00%. Homeowners cannot afford to pay 7.00%, therefore new house building activity in the US (NAHB Housing Index) is very weak, as the following two charts confirm. The housing market is not the whole economy; however, the sector has major problems.

What will more RBNZ transparency mean for the market?

The NZD/USD exchange rate is proving to be more resilient than what most would have expected in the face of the Iranian war and the energy crisis. The Kiwi dollar returned to 0.5900 by the end of last week, following a spike lower mid-week to 0.5820 when the USD appreciated on Trump’s latest rejection of Iranian peace proposals. Subsequently, the USD has eased off to 98.00 on the Dixy Index again as currency traders do not want to be long-USD’s if and when a peace deal is agreed. We retain the view that the USD will depreciate if and when a deal is agreed between the US and Iran and the Strait of Hormuz reopens. The resultant decrease in oil prices will pull the USD Index downwards. The NZD/USD has encountered stiff resistance at the 0.5925 level over the last three weeks and has been unable to hold onto gains above that point. The Reserve Bank of Australia will be lifting their interest rates again to 4.35% this Tuesday. Depending on the accompanying commentary from Chair Michele Bullock, the AUD could be expected to make further gains if the messaging is that the tightening bias with monetary policy remains. The expected Australian dollar gains over this coming week could well drag the Kiwi dollar higher to break above the 0.5925 barrier.

The Reserve Bank of New Zealand has announced new measures on its operation of monetary policy to provide greater transparency, accountability and responsibility. There will now be public attribution of individual votes and views within the Monetary Policy Committee when consensus on interest rate decision is not reached. It will be disclosed how named individual members voted. Individual members of the committee will be encouraged to make their own public speeches and espouse their own views on the economy, inflation, interest rates and monetary policy settings/strategy. The financial markets have generally welcomed the new openness; however, whether it leads to enhanced management of monetary policy remains to be seen.

One potential downside that has been identified is that individual external members of the Monetary Policy Committee may refrain from committing to strong views on the direction of the economy and interest rates. If they consistently get it wrong, their own reputations and careers could be adversely impacted. In which case, no-one will stick their neck out too much and the financial markets are no better informed! Given that here in New Zealand we have a consistent bias to appointing academics to the Monetary Policy Committee, it would seem we are not going to have a Beth Hammack or Stephen Miran rocking the boat with firmly held and controversial economic views. The new Monetary Policy Committee at the Reserve Bank of Australia is not dominated by academics, instead they have bankers, private sector economists, trade unionists and businesspeople.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.