Summary of key points: -

- The “quick end to the war” scenario appears more likely than alternatives

- New Zealand capital inflows to exceed capital outflows

- The “lost art” of context, perspective and relativity on NZ short-term interest rates

As the Iranian war moves into its ninth week, foreign exchange markets are still not reflecting a serious risk of the global economy falling into a major slump as a result of the oil price shock. The US dollar would be a lot stronger today if that risk was considered a high one. The US dollar appreciated to above 100.00 on its Dixy Index in early March when the hostilities started, however there has been no further conviction from the USD buyers that the safe haven capital flows into the USD will continue. As the ceasefires have been extended in recent weeks, the US dollar has weakened when there looks likely to be diplomatic progress on the peace talks and then strengthened again on the Trump threats and counter threats around the Strait of Hormuz. The pullback in the USD value to around the 98.00 level has allowed the Kiwi dollar to recover from 0.5700 to 0.5900. However, further NZ dollar gains to 0.6000 and above will not be achievable until there is a clear-cut diplomatic resolution to the conflict, a re-opening of the Strait of Hormuz and WTI crude oil prices returning to below US$80.00barrel. The risk of the NZD/USD exchange rate moving the other way to lower levels on an escalation of the war is now reduced compared to a few weeks ago.

Despite the on-gain and off-again posturing over this last week for a second round of peace talks in Islamabad, the scenario of a relative quick end to the conflict and oil prices dropping appears to have a higher probability of occurrence than the alternative pessimistic scenario of a prolonged stalemate, oil prices remaining high and the global economy tumbling into recession. It is somewhat surprising that local bank economists, in slashing their New Zealand GDP growth forecast for this year from +3.00% to nearer +1.00%, seem to be rating the latter scenario as the more highly probable. The sharply lower GDP growth forecasts appear to be a knee-jerk over-reaction to us. As we have stated on several previous occasions, Trump does not have the political runway at home to allow this war to continue for too much longer. His attempt to open the Strait of Hormuz appears stalled currently, however no-one really knows the true state of Iran’s military capability at this point in time to prevent the Strait from re-opening.

Should the relatively quick end to the war scenario eventuate over coming days/weeks, the negative impact on New Zealand and global economic growth will be nowhere near as bad as most have been factoring into their more pessimistic forecasts. Consumer and business confidence will rapidly bounce back from recent plunges across all economies, resulting in GDP growth in 2026 only being 0.25% to 0.50% below what it otherwise would have been. As we witnessed with the stronger S&P Global Manufacturing PMI surveys last week in the US, Australia and Euroland, it is by no means a forgone conclusion that economic growth is decimated from what might prove to be a relatively short-term oil shock.

Most currency market commentators are expecting a rapid return to a “risk-on” investor sentiment mode, if and when a diplomatic peace deal is reached. The NZ dollar and the Aussie dollar stand to make further gains in this scenari0. Beyond that immediate FX market reaction to an end to the war, the direction of interest rates in the US, Australia and New Zealand will return as the principal drivers of currency values in this part of the world. Outside of the oil impact on petrol/gasoline prices, underlying inflationary pressure remain higher in New Zealand and Australia than what they do in the US. Last week’s CPI inflation data in NZ for the March quarter reminded us all as to the stickiness and stubbornness of “administered prices” in the New Zealand economy with non-tradable inflation remaining above 3.00%. Excessive Government spending and wage increases in Australia are making it extremely difficult for the Reserve Bank of Australia to get inflation under control (even before the war started). The interest rate markets have pulled back the pricing of Fed cuts to interest rates this year to just one 0.25% reduction, however that could change quickly if jobs data in the US continues to print on the weaker side. The big technology and software companies in the US are laying-off thousands of workers as the AI revolution expands. Expect Chair Jerome Powell and the Federal Reserve to be much more circumspect around the state of the US labour market as this weeks’ Fed meeting on Thursday morning (NZT).

As the currency markets look beyond the war and the resultant energy crisis, the rapid closing up of the interest rate differential between New Zealand and the US remains standing as the most significant influence on the NZD/USD exchange rate going forward.

New Zealand capital inflows to exceed capital outflows

Following a very long hiatus when New Zealand was very much “off the radar” for foreign investors, it does seem that the worm is finally turning to significant foreign capital investment flows returning to New Zealand again. However, according to the local media, the New Zealand economy has been relegated to the basket case mode again as the oil shock has destroyed the economic recovery and Moodey’s have downgraded our credit rating.

The woe of economic misery that the local media seem to take enjoyment in peddling out every day is a world away from the reality of the many positives for the NZ economy that foreign investors are starting to recognise.

The Moody’s credit rating adjustment to “negative watch” was not a downgrade and not all that surprising as Fitch had already moved to that position given the massive increase in Government debt the current Government inherited from Jacinda and Grant.

Unfortunately, the uncertainty and costs associated with Trump’s tariffs last year, adverse weather events and the Middel East conflict this year has postponed the timing of when the Government’s books will return to surplus and start to reduce debt ratios. The NZ dollar did not react whatsoever to the Moody’s statement; therefore, it was of no surprise, and the risk of an actual credit rating downgrade appears remote given the fantastic export commodity prices the economy is currently benefitting from.

Recent announcements support the view that we will see significant foreign direct investment returning: -

- The Government’s refreshed direct investment visa scheme, the Active Investor Plus “Golden” visa is exceeding expectations with NZD1.5 billion already invested in funds and businesses, with a further NZD2.4 billion in the approval pipeline. Allowing the investors to own a house in New Zealand has stimulated the interest from the US, Germany and China.

- The Overseas Investment Act has been streamlined for fast-track approvals, removing one of the previous stumbling blocks of long, drawn out approvals. The Invest New Zealand Agency is now also up and running, targeting deals between NZD100 million and NZD1 billion.

- The Free Trade Agreement with India is currently being signed, aiming for NZD35 billion of direct foreign investment from India. Whilst many are sceptical as to whether this will happen, it should be remembered just how large the Indian economy is compared to New Zealand. The FTA with China in 2008 was a gamebreaker for the New Zealand economy leading to the “rock star” performance years from 2012 to 2019. Then Indian FTA has the potential to benefit our economy in a similar way.

- An Australian company, Victorian Hydrogen plans a NZD3 billion plant near Invercargill to use lignite (brown coal) to manufacture urea fertiliser. Whilst we currently produce some urea locally in Taranaki, the bulk is imported. The proven technology is already being used in Arica.

- With the NZ foreign tourism industry back to pre-Covid full noise, offshore hotel investors/chains are again eyeing opportunities in New Zealand. Global brands such as JW Marriott and Moxy have recently entered or expanded in the NZ market.

- The opportunity to use New Zealand’s renewable “green” electricity (from hydro not fossil fuels) to power data centres for the AI revolution is already underway. Microsoft, Amazon AWS, Datagrid and CDC are investing in local facilities.

The net result of the foreign investment inflows is demand for NZ dollars exceeding supply and it is always these large capital flows on the margin that determine exchange rate shifts.

The “lost art” of context, perspective and relativity on NZ short-term interest rates

A recent bank economic commentary stated that the Reserve Bank of New Zealand “(RBNZ”) would be “reckless” to increase the OCR this year as that one act would do untold damage to the economy. Their argument was that increasing the OCR from its present level of 2.25% to 3.00% would hurt mortgage and business borrowers to such an extent that the economy would be driven back into recession. It is doubtful whether the bank received too many supporters with that view, because as financial market participants correctly observe, forward market pricing for 90-day interest rates is already substantially higher with the two-year wholesale market swap interest rate at 3.45% currently. The two-year home mortgage lending rates are priced off the interest rate swap curve. The OCR being lifted by the RBNZ from 2.25% to 3.00% may not change that two-year swap interest rate as it has already priced-in such an expected increase. In lifting the OCR to 3.00%, if the RBNZ also stated that inflationary expectations had increased and further monetary tightening may be necessary, the two-year swap interest rate would be justified is rising further towards 4.00%.

In thinking that a 0.75% increase in the OCR from 2.25% to 3.00% would be a reckless tightening of monetary policy that makes all our lives total misery, the bank economist seems to have lost all perspective, context and relativity as to what is a low interest rate and what is a high interest rate for the New Zealand economy. In our view, adjusting the OCR from 2.25% to 3.00% is merely unwinding the “super-loose” monetary settings put in place late last year and bringing the monetary settings back to a more neutral point i.e. easing off a bit on the accelerator, however certainly not putting the foot anywhere near the brake pedal.

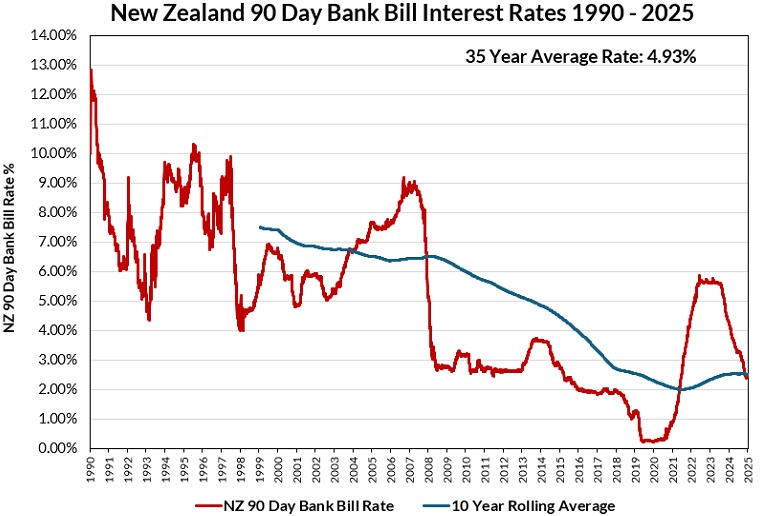

An interest rate lesson from history is warranted.

The chart below plots the 90-day bank bill interest rate over the last 35 years. The steady decline in the 10-year rolling average interest rate from above 6.00% in 2008 to 2.00% in 2021 can be attributable to two economic phenomena that are unlikely to be repeated (famous last words!): -

- 2010 to 2020 being a period when we imported substantial and sustained goods deflation from China, resulting in record low inflation and historically low short-term interest rates.

- 2020 to 2022 Covid years where the RBNZ Governor Adrian Orr’s “no regrets” monetary loosening went to historical and world record extremes.

Excluding the above two economic “anomalies” that distort where normal or neutral OCR interest rates might work for the NZ economy, leads us to a conclusion that a 3.00% to 3.50% OCR (or 90-day interest rate) represents a neutral interest rate zone that achieves the right balance between borrowers and savers. If inflation averages the RBNZ mid-point target of 2.00% in the long run, a 3.50% base interest rate delivers the right incentives and motivations for both borrowing and saving/investment decision makers in the economy.

As the RBNZ stated at their last OCR review, should the higher headline inflation rate over coming months (from the oil price shock) cause an increase in long-term inflationary expectations and higher wages, they will need to adjust monetary policy away from the current “super-loose” setting to somewhere near to neutral or slightly above neutral. Whether they are forced to hike interest rates in this fashion depends entirely on how long the Iranian war lasts and oil shipments are disrupted. In the post deflation/Covid era a realistic assessment, in our view, as to what is tight monetary policy (higher interest rates) and what is loose monetary policy (lower interest rates) is summarised in the following table: -

| Monetary Policy setting |

90-day Interest rate ranges |

|

| T2 | Super Tight | 4.50% to 5.50% |

| T1 | Tight | 3.50% to 4.50% |

| N | Neutral | 3.00% to 3.50% |

| L1 | Loose | 2.50% to 3.50% |

| L2 | Super Loose | 1.50% to 2.50% |

It has to be said that over the last 35 years the RBNZ’s inflation targeting and management of monetary policy has been successful in structurally reducing New Zealand’s interest rate levels. Unfortunately, abrupt swings in policy settings from super loose (2020/2021) to super tight (2023/2024) and back to touching super loose gain (2025) has caused a volatility and uncertainty that has not been good for the economy. Maintaining stable interest rates at the neutral range would serve the economy with more certainty and confidence. In the historical context, a 3.50% OCR is not a high interest rate that is restrictive on the economy. As has been proven in recent years, New Zealander’s tend to embark on speculative property binges if money is too cheap. They then moan incessantly when the monetary medicine has to be delivered to bring the resultant inflation down.

Holding local interest rates at levels below those of the US and Australia over recent years has pushed the NZ dollar value lower than otherwise would be the case, and through higher import costs this has contributed to some of the inflation challenges the RBNZ now faces.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

6 Comments

- "The Free Trade Agreement with India is currently being signed, aiming for NZD35 billion of direct foreign investment from India. Whilst many are sceptical as to whether this will happen, it should be remembered just how large the Indian economy is compared to New Zealand. The FTA with China in 2008 was a gamebreaker for the New Zealand economy leading to the “rock star” performance years from 2012 to 2019. Then Indian FTA has the potential to benefit our economy in a similar way."

You appear to have that backwards...the investment requirement is the other way.

Yes, you re correct, there is no requirement for India to invest in NZ. I suspect. I suspect just had a senior moment.

To compare the India FTA with the China NZ FTA is to misunderstand the huge market complementarity that existed between NZ and China. The India FTA will be more modest in its outcomes.

Bit of feedback from Food & Hospitality Asia 2026, where Aotearoa had its first pavilion since 2018, was that all the propositions fit well within the food service channel like 5-star hotels that have a high proportion of Western guests. Compare that to Bel’s Laughing Cow processed cheese, which is starting to find favor in China. Simple things like understanding that the cheese market is essentially sweet means Laughing Cow cream cheese cubes are now positioned as sweet snacks, not as traditional savory cheese.

Two things

First off, Jarrod Kerr (the Kiwibank economist alluded to in the article) is a broken clock crying for lower interest rates since he had a platform to cry on. He's not worth listening to as he's never presented another perspective; on the contrary - listen to any of his discourses in 2019 and you'll know what he says now. Good rebuttal though

Secondly, I think the author severely underestimates the IRGC appetite for inflicting pain to the US. MSM is only now waking up to the reality that the negotiations are driven by IRGC, and what drives IRGC is fundamentalism, not rationalism

We've been in the chemonomics phase of the conflict for some time now, and will be here for a while. Trump can have all the appetite in the world - this is not how asymmetric warfare works

Trump has the mightiest legacy army in the world, best equipped to deal with a similar army, but poorer. He doesn't have an army to shield the insurance industry's confidence from droves of drones launched from trunks of 1980s Hiluxes hidden in caves, and that's what he needs

Interesting times ahead, but I wouldn't be as optimistic as the Occidental markets are about the conclusion of a standoff which is dictated by fundamentalists from another world with nothing but appetite to inflict pain on the US. These analysts seem to apply their own mindset to the world view of a different, antagonistic culture. The result won't look prettier than how Vietnam turned out to be vs how the Americans expected it to go

The 3rd para resounds. The IRGC were formed in 1979 and developed for exactly the circumstances Iran is experiencing today. Furthermore the assassination of the political hierarchy has cemented the IRGC’ s position as the actual power holders. In a way it has been an involuntary coup d’etat, precipitated by the USA and Israel. The IRGC are not the negotiating types and by now they will have realised that there ain’t going to be any land force willing to even test their mettle and it would not be too far fetched to think, that they find that slightly disappointing.

'Loose' encompasses 'neutral' according to your table. Fyi

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.