The NZD/USD exchange rate has been stuck in a rut between 0.5820 and 0.5980 over the last month as the Iranian war continues to dominate global currency movements. As the risk increases and then recedes surrounding whether Donald Trump will recommence the bombing of Iran, or not, the Kiwi dollar is fluctuating within the relatively narrow trading range. Foreign exchange markets are responding to the daily news of Trump’s alternating threats and concessions; however, the impact on FX rates is reducing over time as the war has dragged on.

Latest reports (Sunday morning NZT) from the Financial Times in London is that Iran and the US are closing in on a 60-day extension to the ceasefire to establish a framework for nuclear talks. The agreement would include a gradual reopening of the Strait of Hormuz and an unfreezing of Tehran’s overseas assets.

Time will tell. In the meantime, the conclusion is an impasse until market risk sentiment goes one of two ways: -

- Trump starts bombing Iran again as the latest peace talk proposal fails, in which case oil prices shift higher, the USD strengthens and the NZD/USD rate decreases.

- A peace deal is struck, oil prices collapse and the USD follows oil prices downwards. Under this scenario, the NZD/USD exchange rate pops above 0.6000 again.

Given the current impasse, we see twelve factors as likely to influence the NZD/USD exchange rate direction over the next few months: -

- Oil and currency markets react to one of the two scenarios outlined above: It is very binary in the short-term as the US dollar value is now correlated with the movement in oil prices. Higher oil prices for longer increases the probability of second round inflation increases in the US and therefore the Federal Reserve will hike interest rates, which is USD positive. Alternatively, a sharp decrease in the oil price increases the probability again of the Fed returning to interest rate cuts later this year, USD negative.

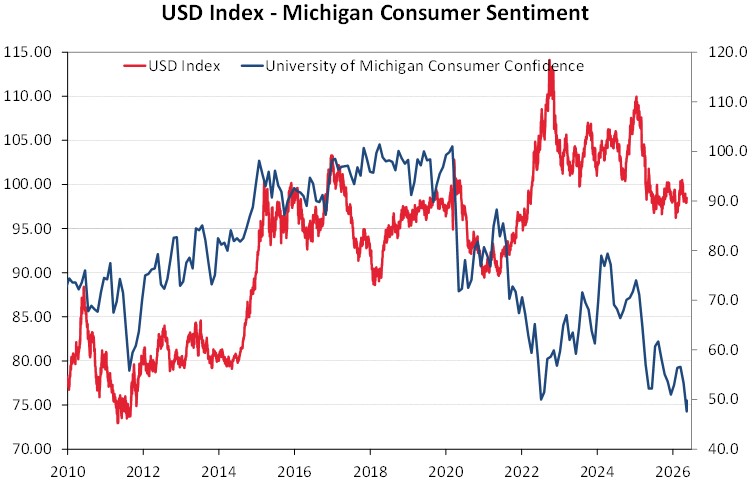

- Trends in US economic data: Underlying economic indicators such as employment, retail sales, industrial production and PMI manufacturing/services surveys have generally printed more positive than prior forecasts over recent months. There is no doubt that the construction of new data centres for the AI boom is driving positive business investment numbers in the US. However, the flipside to that more positive story is the continuing plunge in consumer sentiment with the University of Michigan survey diving to new record lows of 44. 8 this month. Coupled with major problems in the US home construction industry and the untrustworthy nature of the Non-Farm Payroll jobs data, the conclusion must still be that US GDP growth will disappoint on the weaker side in 2026. If consumers ultimately drive the US economy, the outlook cannot be positive for GDP growth or the US dollar value over the coming period (see first chart below).

- Will new Fed Chair, Kevin Warsh be positive or negative for the US dollar? President Trump’s alarming inconsistency has once again been laid bare for all to see. Just a few weeks ago he was calling then Fed Chair, Jerome Powell a “knucklehead” for not lowering interest rates. Two days ago, at Kevin Warsh’s swearing-in as the new Fed Chair, Trump was trumpeting that Mr Warsh would act independently and told him to “just do your own thing and do a great job”. No pressure on Kevin then. Kevin Warsh intends to reform the Fed; however, we do not know whether this allows him more influence to cut interest rates even though inflation remains above the 2.00% target. The first media conference for Mr Warsh after the next Fed meeting on 17th June will be closely watched by the forex markets for indications of where the new Chair stands on the dove to hawk spectrum for monetary policy management. Any tendency towards the dovish side will be USD negative.

- The evolving RBNZ monetary policy stance: There are a number of strong arguments as to why Governor Anna Breman should pre-empt rising inflation with an early interest rate hike at the RBNZ meeting tomorrow. The main one being that you only make the inflation control job harder if you wait. Therefore. act sooner rather than later as changes to monetary policy settings take nine to 12 months to have any impact. The argument against interest rate increases at this time is that it is still too soon to measure whether the oil price shock will feed into increases in other prices and wages. At this point, we still favour holding off on interest rate increases until August/September. However, the RBNZ would be justified in delivering a sterner message about price setting behaviour, otherwise interest rate increases will be coming. In reality, the forward interest rate market has already tightened monetary conditions with two-year wholesale swap interest rates now trading at 3.57%. We expect the RBNZ statement to be neutral for the Kiwi dollar at this point, but successive interest rate hikes in three months’ time to catch up to market pricing will be NZD positive.

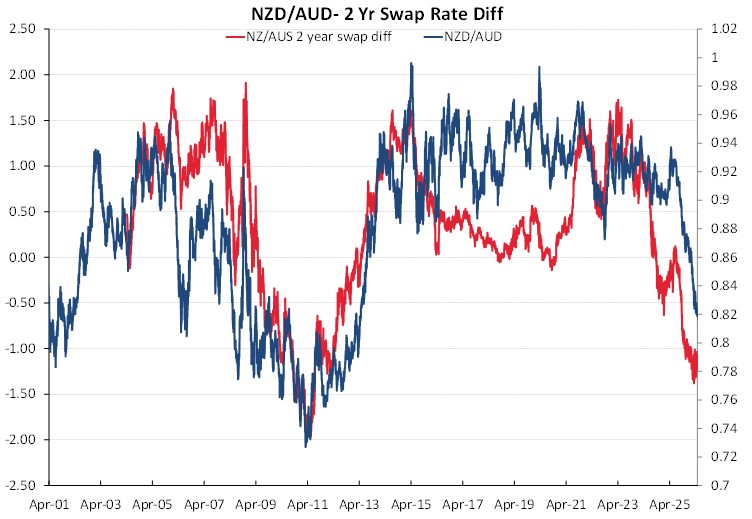

- Closing interest rate differentials to the US and Australia: Arguably the strongest influence on NZD/USD exchange rate direction. NZ interest rates being well below both US and Australian interest rates over recent years has kept the Kiwi dollar at the bottom end of its longer-term cyclical range. However, that negative is drawing to a close, as on a forward looking basis there is the real prospect of NZ hiking interest rates and the US cutting interest rates later this year. The two-year swap interest rate differential is on track to shift from negative to positive i.e. NZ interest rate once again above US interest rates. Given the close correlation between interest rate differentials and the Kiwi dollar, that change can only be increasingly positive for the NZD as independent buying of the Kiwi emerges.

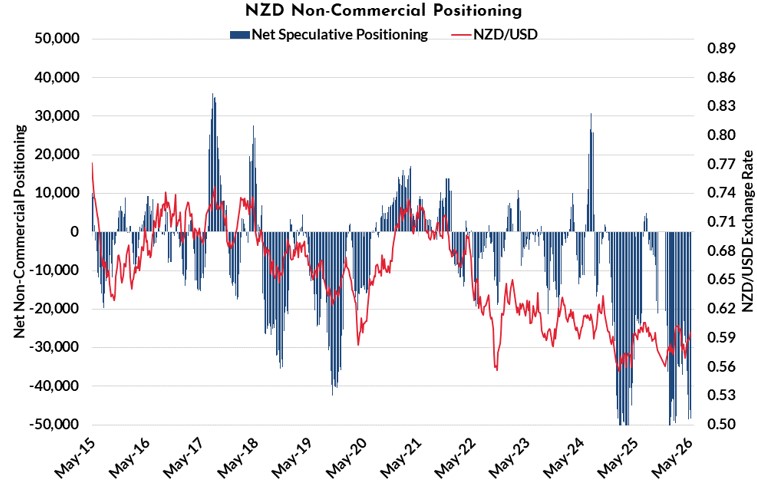

- Speculative FX market positioning set to change: The second chart below confirms that the currency speculators are still prepared to hold “short-sold” NZ dollar positions in expectation of future NZD depreciation. As NZ short-term interest rates are still below those of the US, the punters are paid the forward points to sell the Kiwi. As we have already witnessed with the AUD/USD currency positioning, the change from short-sold AUD to going long AUD is rapid when the interest rate differential switches the other way. We have not seen any sign of the short-sold NZD punters switching position yet. However, it cannot be too far away, particularly if Middle East events send the oil price and USD lower, the resultant NZD buying lifting the NZD/USD rate above 0.6000.

- Renewed issuance of Kauri NZD denominated bonds: When there is new and increasing investor interest in these NZD denominated bonds issued by offshore borrowers, it is generally a positive sign for the Kiwi dollar. We have not seen much activity in this bond market for a few years, but suddenly there is a flurry on new issues. The World Bank issued a NZD1.3 billion, 7-year bond in April, quickly followed up by the Asian Development Bank also issuing a NZD1.3 billion bond. Last week, Rentenbank increased the size of its new issue from an initial NZD300m to NZD800m, indicating some serious demand from investors. If the pricing continues to work for both the issuers and investors, we may well see many more issues coming to the market. According to RBNZ records, 25% of issued Kauri bonds are held by foreign investors. The foreign investors have to buy NZD’s to buy the bonds. If not anything else, it is a sign of renewed confidence in the NZ economy and the NZD from offshore players.

- Spectacular NZ export performance: Overseas merchandise trade (export and import) data for April released last week produced the largest monthly trade surplus ever recorded. April exports exceeded imports by NZD1.92 billion, more than double prior consensus forecasts of NZD0.90 billion. Exports were 12% higher than April last year. Despite current question marks about global GDP growth as a result of the oil shock, the outlook for our commodity exports still appears strong. Retail sales over the March quarter at a 0.90% increase were also double forecasts, mostly coming from regional New Zealand. It remain only a matter of time before the export boom starts to lift activity levels in underperforming Auckland economy. The credit rating agencies may have pressure on our Finance Minister, Nicola Willis to rein-in future fiscal deficits, however an actual rating downgrade for New Zealand does not seem likely with our export performance so strong. The budget this week will provide the numbers and pathway to the Government’s ultimate deficit and debt reduction. The export boom is net positive for the Kiwi dollar.

- Bank of Japan intervention in the Yen: Whilst it could be argued that the billions of USD’s spent by the Bank of Japan over recent times to stop the Yen depreciating any further has not been successful in turning the currency around, the 160.00 level to the USD has been defended and it has not traded above that point. If the USD falls on decreasing oil prices, the Yen is poised to make gains towards 150.00 as Japanese investment houses repatriate US Treasury Bond investments back to Japan. The NZD/USD is also closely correlated to USD/JPY movements, so the odds favour the Yen strengthening from here and the Kiwi dollar following that adjustment.

- Interest rate hikes in Asian economies: A number of the Asian economies (Malaysia, Philippines, Thailand, Singapore and Indonesia) have been hit badly by energy shortages and price increases due to their heavy reliance on oil imports from the Middle East. Their central banks are looking at interest rate increases to combat inflation, which will push some interest rates above those in the US and therefore strengthen their currency values. Asian manufacturing economies have US$1.3 trillion in Current A/c surpluses held in USD’s. There may be a large incentive for those Asian companies holding surplus cash in USD’s to bring it home to the higher interest yields. By contrast, Arab oil producers (one upon a time the petro-dollar kings) now only have $300 billion in Current A/c surpluses.

- Global equity markets: Any downward correction from the current bull run in chip, AI and technology stocks would stand as a negative for the NZD, as market risk sentiment would turn down. It is a brave person who would put a time frame on this happening anytime soon.

- The Aussie investment invasion is coming: With the NZD/AUD cross-rate at 0.8200, New Zealand assets are suddenly very cheap in the eyes of the Aussies. Do not be surprised to see a wave of Australian funds, private equity firms, property investors and companies seeking out opportunities in New Zealand as the returns stack up very well in AUD terms. The recent Australian budget hit baby boomer property investors hard with adverse tax changes, investments outside Australia may be starting to look attractive.

While not all of the factors listed above are outright positive for the Kiwi dollar, a good majority point to NZ dollar gains against the USD and AUD once the Iranian war is over and the oil shock comes to an end.

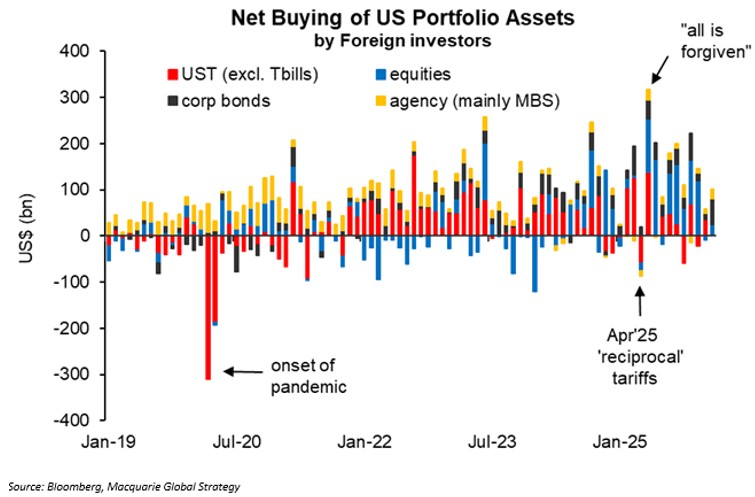

The final chart below plots foreign investment into US investment asset classes (portfolio assets). The striking feature of the shifting investment flows is that foreign investors have curtailed buying of US equities and Treasury Bonds over recent months. They are still buying the higher yielding corporate bonds and agency bonds, being mortgage backed securities (“MBS”). The US economy does not have sufficient domestic savings to funds their own increasing US Government debt. If the foreign investment flows are not coming in they are going to run into some problems. It is not positive for the US dollar value whichever way you look at it.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.