Summary of key points: -

- Two good reasons as to why the FX markets, in buying up the USD, have misread the Fed

- Aussie dollar pulls back, however retains its yield advantage

In the world of foreign exchange market commentary and forecast you need to possess a liberal dose of contrition and humility!

Over recent weeks we have proffered the strong view that the Iran/US war would end sooner rather than later, the WTI oil price would plummet as a result to below US$70.00/barrel and the US dollar would follow the oil price lower (based on US inflation reversing back downwards as fast as it went up in March and April and therefore US short-term interest rates moving lower). We were correct on the first two assertions, however unfortunately the US dollar did not depreciate in line with our expectation. Hence the contrition and humility (for the short-term anyway!). In fact, the opposite occurred, with the US dollar appreciating from 98.00 to a high of 101.45 on its Dixy Index last week when the US financial markets interpreted Kevin Warsh’s first Fed meeting as Chairman as a “hawkish” pivot to increasing US interest rates.

Time will tell, however our opinion is that the FX markets have interpreted the messaging from the Fed incorrectly, and the US dollar will not sustain this latest bout of strength that has driven the NZD/USD rate to new lows of 0.5640. The immediate reaction by US short-term interest rate markets to the Fed’s statement last week was to re-price two-year Treasury Bonds sharply higher from 4.00% before the statement to 4.23% afterwards. Tellingly, the interest rate markets have already started to have second thoughts about the Fed raising interest rates later this year. Over the last seven days the two-year Treasury Bond yield has reversed back downwards to 4.09%. The currency markets have not yet followed that lead by selling the US dollar lower; however, we can expect that the FX markets will follow and also unwind the recent USD gains.

There are two very good reasons as to why the Fed will not be increasing interest rates over coming months and could well revert back to the earlier signaled cuts.

Reason 1: The majority of the 12 voting members of the Fed remain biased to lower interest rates

The interest rate and foreign exchange markets largely react and adjust pricing according to the headlines flashing across their screens. The media headlines from Kevin Warsh’s first meeting as Chair was that it was a hawkish pivot in monetary policy because he was very stringent on stating that the Fed was committed to returning the US annual inflation rate to the 2.00% target. There was nothing new in that statement, former Chair Jerome Powell has consistently stated that same commitment over recent years.

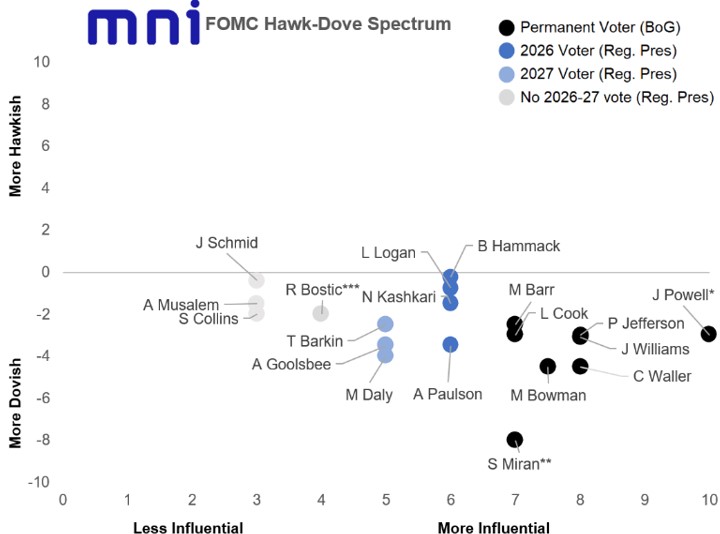

However, delving into the detail and examining the weeds of where the current 12 voting and seven non-voting members of the Fed sit on the spectrum between doves and hawks reveals that the majority of the voting members favour stable to lower interest rates (doves), not hikes (hawks).

- 12 voting members: Doves include Miran, Waller, Bowman, Jefferson, Paulson, Cook, Powell, Williams and Barr (9), whereas there are only three hawks, namely; Kashkari, Logan and Hammack.

- 7 non-voting member: Doves include only Daly, whereas the remaining six members are all hawks, namely; Collins, Goolsbee, Bostic, Musalem, Barkin and Schmid. Their hawkish views do not count for much as they have no vote on interest rate changes.

- New Chair, Kevin Warsh, did not enter his own growth, inflation and interest rate forecast (dot-plot) at the last meeting, however he would be regarded is more in the hawkish camp.

The diagram below confirms the disparity between the majority dovish voting members in 2026 and 2027 and the more hawkish non-voting members.

Reason 2: US inflation is about to follow oil prices sharply lower

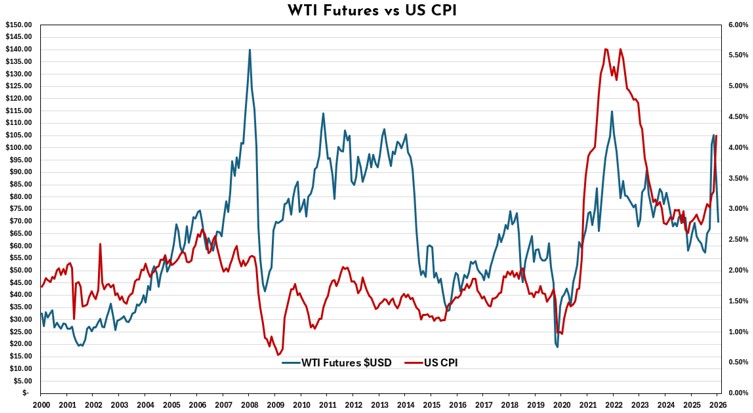

Unsurprisingly, there is a close “causation” relationship between WTI oil prices and the US inflation rate. The dramatic 36% reversal in oil prices from US$108.00/barrel in mid-May to US$69.20/barrel today is about to send the US annual headline inflation rate down from the current 4.20% level to nearer 2.50% over coming months. The direct impact of oil prices on US inflation, both up and down, means that it is highly unlikely the Fed will need to lift interest rates to reduce the inflation rate. It will happen automatically by itself as monthly CPI inflation results over coming months turn negative and replace the 0.30% monthly increases of 12 months ago (pulling the annual rate of inflation sharply lower).

The chart below plots the US annual CPI inflation rate against WTI oil prices over the last 26 years. The significant and rapid decreases in the oil price (blue line in the chart) in 2009, 2015, 2020, 2023 and over the last month in 2026 have all resulted in subsequent sharp reductions in the US CPI inflation rate (red line in the chart).

- 2009 GFC: Immediate, sent inflation to 0.50%

- 2015: Inflation reduced to 1.25%

- 2020 Covid: Inflation dropped from 2.00% to 1.00%

- 2023: Assisted the high inflation at 5.50% to reduce to 2.50%.

Note that over the 2009 to 2014 period rising oil prices did not push US inflation up, because the US was importing large dollops of deflation from China (lower goods prices) over those years.

The conclusion from the above analysis is that FX markets, who have bought the US dollar higher to 101.20 over the last two weeks, will very soon have to reassess their positioning due to the Fed not increasing interest rates and inflation reducing sharply on its own accord. Based on the USD reversing lower over coming weeks/months, the current spike downwards in the NZD/USD exchange rate to 0.5640 should prove to be as short-lived as the previous dips below 0.5700 in recent years.

Aussie dollar pulls back, however retains its yield advantage

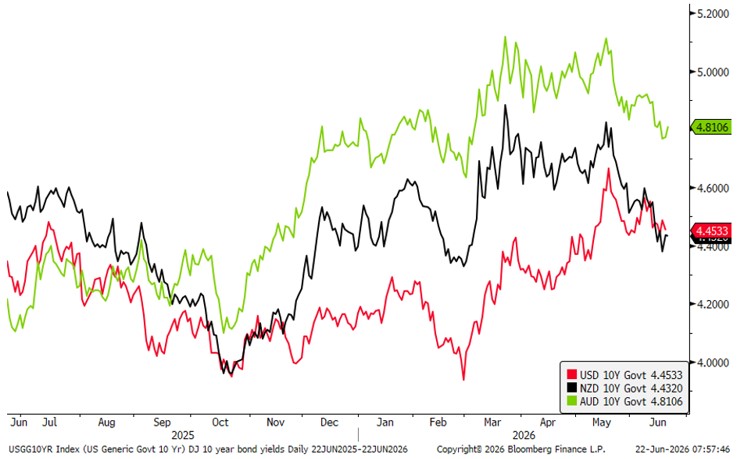

The Australian dollar has corrected back three and a half cents to 0.6900, from its highs of 0.7260 reached in mid-May, against the stronger US dollar over recent weeks. However, it still retains a yield advantage over US interest rates, even though US interest rates have increased in reaction to Kevin Warsh’s first meeting as the new Federal Reserve Chairman. Australian 10-year Government Bond yields currently trade at 4.81%, still 0.36% above US 10-year Treasury Bonds at 4.45% (refer to the first chart below). Global bond investors seeking diversification away from the US economy and the US dollar are still attracted to the yield enhancement that Australian bonds offer. The Australian bond market is not yet convinced that the Reserve Bank of Australia (“RBA”) is done with hikes in short-term interest rates as they tighten monetary policy to rein in inflation which is well above their target.

Recent economic data releases in Australia have produced a mixed set of results which have not settled the debate either way as to whether the RBA need to continue their interest rate increasing cycle or hold off at the current OCR interest rate at 4.35%.

The economic arguments for ending the interest rate hikes are as follows: -

- Plummeting oil prices will stop the increases in the inflation rate and start to pull the inflation rate back down again. The inflation rate in the month of May, released last Wednesday, was a decrease of 0.70%, well below consensus forecasts of -0.30%. The annual rate of inflation reducing from 4.20% to 4.00%, against expectations of another increase to 4.40%.

- House prices in Australia are no longer increasing and are starting to fall in Sydney and Melbourne as higher floating rate mortgage interest rates and changes to tax rules for residential property investors erodes confidence.

- Previously strong immigration inflows, which were providing a tailwind for the housing market and the economy, are slowing down. The political landscape in Australia is reflecting growing opposition to strong inwards migration.

- Consumer confidence is weakening with the Westpac Consumer Confidence Index dropping to 80.6 in June from 83.0 the previous month. The NAB Business Confidence measure has abruptly turned negative since the Iran/US war started in March.

The argument from some local Australian economists is that the RBA should continue with interest rate increases as they need to slowdown demand and wage increases in the economy to return inflation to the 2.50% from the current 4.00% level. Australia’s monthly employment data is notoriously volatile and unreliable as an indicator of economic conditions. In April, jobs unexpectedly decreased by 41,000, however the May numbers bounced back to an increase of 40,000 (albeit most of the increase was for part-time employment). The Unemployment rate has remained stable at 4.40%. The inflation figures for June are released on 29th July and the employment figures for June are released on 16th July. The RBA do not meet again until 11th of August, so the debate will continue over coming weeks as to whether the RBA need to increase interest rates further or signal that they have finished.

In the meantime, how the US dollar itself behaves and whether it now starts to follow US interest rates lower will be the determinant of AUD/USD exchange rate direction. Lower oil prices are arguably a negative for Australia’s mineral and energy export prices. Iron ore prices have slipped from US$111/tonne in May to currently trade at US$100/tonne.

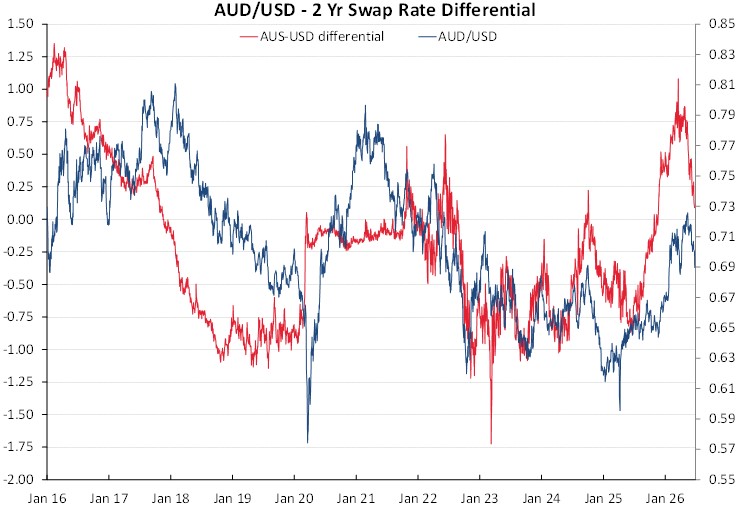

The second chart below confirms just how much US short-term interest rate increases over the last two weeks have reduced the favourable positive interest rate differential the Aussie dollar has enjoyed over the US since mid-2025. We expect that US two-year interest rates will decrease more rapidly than Australian two-year rates from here, therefore we would anticipate that the interest rate differential (red line in the chart) will start to move back upwards again and therefore act as a positive for the Australian dollar over coming months. A return of the US dollar to a depreciating path would certainly project the Australian dollar higher to the mid 0.7000’s as its yield advantage makes it stand out as a preferred destination for funds moving out of the USD.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.