Was it really little more than four months ago that we were anticipating (and got) another cut to the Official Cash Rate?

To say 'a lot has happened' since the November 26 OCR review is to not even come close. Suffice it to say, nobody's talking about rate cuts any more.

Since then we've had a new Reserve Bank (RBNZ) Governor - Anna Breman - come into the job. And she wouldn't be human if she hadn't wished for a somewhat quieter bedding-in period. Wholesale interest rates spiked late last year prompting banks to start raising mortgage rates. Then last month everything was turned upside down with a fuel crisis. Economists are forecasting 4% inflation for New Zealand by the middle of the year.

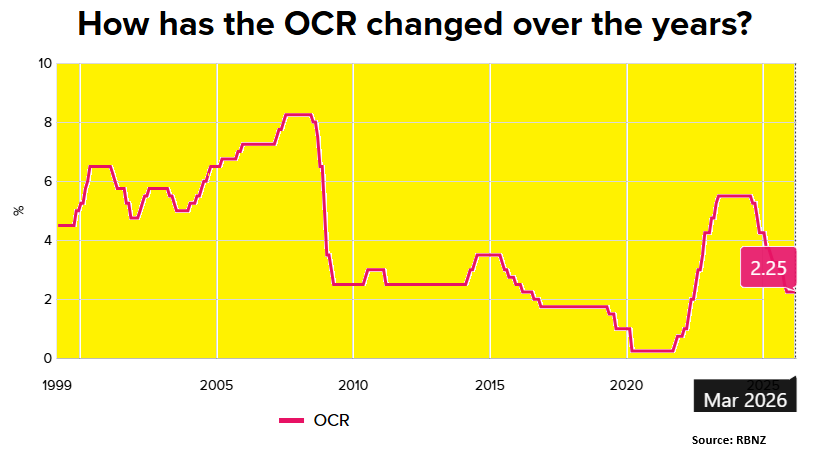

It's with this exotic background that the RBNZ's Monetary Policy Committee (MPC) will on Wednesday, April 8, make its latest pronouncement on the OCR. In such circumstances, it's strange to say that the 'easy' part of this decision is that the OCR WON'T be changed from the current 2.25%.

Beyond that, it all gets a lot harder - when it comes to 'guiding' the markets on what comes next. I mean, let's face it the MPC won't really know exactly itself.

I think Governor Breman has made an encouraging start in the role despite facing unexpectedly taxing conditions. She certainly would not have imagined needing to speak to the financial markets barely two weeks into the job in December in attempt to calm down wholesale interest rates that were spiking as the markets poorly digested the realisation that the November OCR cut would be the last in the foreseeable future.

And likewise, set down to deliver a speech on March 24 touching on the current economic outlook, drawing on insights from the February Monetary Policy Statement, and outlining how the RBNZ is working to modernise New Zealand’s payments system, Breman adroitly pivoted to instead talk about the impacts of the Middle East conflict and emerging fuel crisis.

It is this speech that is likely to form the backbone of the RBNZ OCR review in the coming week.

No bells, but definitely some whistles

The April 8 OCR review is one of those that's styled as a 'Monetary Policy Review' (MPR). These ones alternate with reviews that are known as the 'Monetary Policy Statement (MPS) and OCR' reviews. This year there will be seven reviews in total - four MPS ones and three MPRs. From next year there will be a total of eight reviews each year.

The MPRs have in the past tended to be straight forward, perhaps even boring, affairs. Before the Monetary Policy Committee was formed they were but a single page. This meant the RBNZ tended to prefer to wait to the following review - the one that had the bells and whistles 60 page Monetary Policy Statement with charts and projections and a media conference with the Governor - before signalling any change in direction.

This situation changed a little after the MPC was formed because then the MPRs would, as well as the single page media release, also have the more detailed record of the MPC meeting. Still, however, these were usually fairly routine occurrences.

But on April 8, and from now on, the MPR is also going to be accompanied by a media conference, albeit an online one rather than in-person. So, now we get some whistles with the MPR, if not bells too.

The immediate question is whether the expanded MPR means there will be some attempts by the RBNZ Governor at pre-signalling to some extent some of the forecasts and forward-looking sentiment that might be contained in the next MPS (which will be released on May 27).

The major bank economists' commentaries I have been reading this week are mostly suggesting this WON'T be the case and that the Governor will essentially use her March 24 speech as the template and stick close to that, given the inherent uncertainties and the fact this is a constantly developing and evolving situation.

Remember the March 24 speech essentially said the RBNZ would 'look through' the initial impacts of the crisis. However, if there are subsequent effects on medium-term inflation or inflation expectations, the appropriate policy response could be to increase interest rates to prevent these second round effects.

Financial markets race ahead of themselves

So, in other words, the speech was attempting the difficult balancing act of soothing the financial markets that the RBNZ won't be jumping in with interest rate rises - while at the same time making clear that 'second round' inflationary impacts will be trodden on.

This all did calm down the financial markets a bit. But not a lot, immediately. However, in the past week or so, pricing has started to ease back.

At the time of writing the financial markets are still pricing in a nearly 4% chance of an OCR hike in the coming week (when, really there is NO chance), while pricing for the May OCR decision has a 1-in-4 hike chance built in. The financial market pricing was earlier seeing it as nearly a given that there WILL be a rise in July, but at the time of writing this had eased back to a 60% chance. At one point markets were just about pricing FOUR hikes during the rest of 2026, then it was three and at the time of writing a little bit over two (55 basis points of hiking are priced in by December).

To go back then to the question of whether any attempt will be made to give a bigger hint into what might come ahead in May and beyond that, I actually wonder if there will be at least some efforts to give broad-brush indications of some of the potential inflation impacts.

Now, that would undoubtedly be difficult, to say the least, given how dynamic the situation is. In some respects it might be useful though to at least attempt to do this, so, that people are not surprised. If indications of the type of near-future inflation we could see are provided, they could be accompanied by some reassurance that upon 'normalisation' of the situation, the inflation will abate. The point of that would be to stop inflation expectations galloping away and people increasing their prices right, left and centre. Because that would probably lead us right into stagflation.

Look, there's never going to be a good time for a fuel crisis. But the timing for us of this episode is particularly harsh.

First up, we have gone into this with our annual inflation at 3.1% as of the December quarter - so, we have absolutely zero wiggle room when it comes to pricing shocks.

On top of that our battle to get inflation down into the RBNZ's 1% to 3% target range from the heights of 7.3% in mid-2022 saw the economy battered and bruised. And confidence disappeared.

The patient was recovering, but has now taken to their bed again...

However, in the back half of 2025 we had two consecutive quarters of GDP growth, and by all accounts the March quarter will show good growth.

Confidence WAS slowly, gingerly, starting to return, but it feels like it has been snatched away again and we are back down in the dumps. Certainly the ANZ Business Outlook for March suggested confidence collapsed during the course of that month as the realisation dawned the Middle East situation would not quickly be resolved.

If we choose to focus on potential 'positives' it is that this very lack of confidence is likely to crimp spending again - meaning that it could be a hard sell for businesses to increase prices and therefore 'second-round' inflation could be limited. Of course, I say that's a 'positive' - well, it ain't a positive for the business that might be faced with higher costs but can't recover them.

Unemployment was 5.4% as of the December quarter and economists, who previously expected it to fall, now see it hitting 5.6% by mid-year.

The upshot is that the long delayed economic recovery just got put on hold again and, in all likelihood, we are set for our third consecutive diabolical June quarter GDP result.

All of which is why the RBNZ will tread carefully. And, yes, we do hear the talk about why is the RBNZ going to try to protect the economy when its single monetary policy goal is targeting inflation between 1% and 3%? Well, the simple answer is that if the RBNZ jacks up interest rates in an economy that's tanking there is the prospect down the line of actually undershooting the 1% to 3% target.

ANZ chief economist Sharon Zollner has summed the situation up nicely, as per this quote:

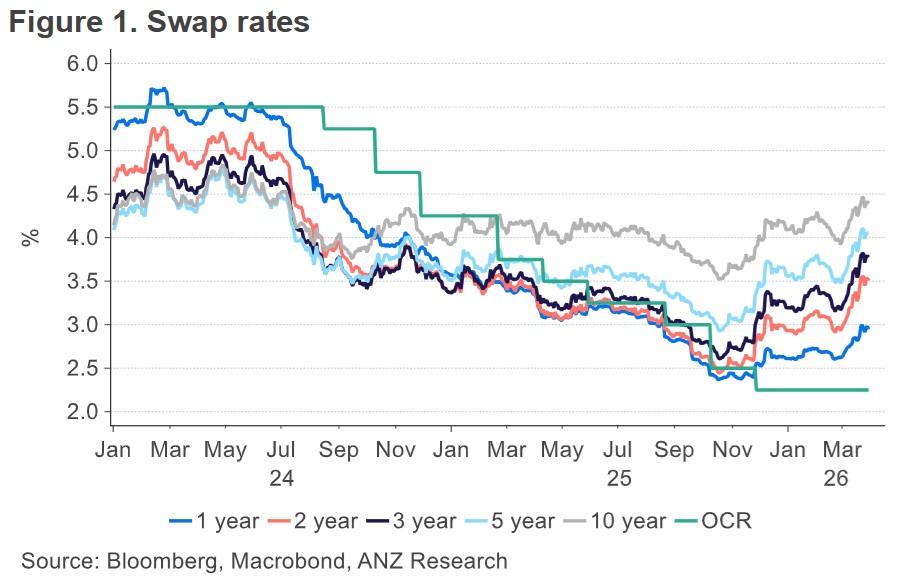

"There certainly seems to be little risk that the [2.25%] sub-neutral OCR is going to set off a wave of risk-taking anytime soon – not least because interest rates have gone up all by themselves [see graph]. Last week we revised down our house price forecast. While the outlook is a lot more uncertain than it was, and a very wide range of scenarios is plausible, we continue to see [monetary] policy normalisation kicking off in December. But we can’t stress enough how fluid the situation is."

What do we expect on this coming Wednesday then? Well, in cricketing parlance it will be very much the RBNZ playing it 'with a straight bat' and aiming to be calming while maintaining a 'but don't start thinking about putting up prices for the sake of it' theme. Beyond that, the interest will be around whether the RBNZ does try to quantify just how high our inflation may go in the short term, and just when it might consider raising the OCR. Or whether it will make very much 'holding' comments and await the May MPS before digging into the nitty gritty. Either way, it is not to be missed.

15 Comments

In the last month or so, the gst component of diesel has gone from about $0.25 to $0.50 per litre. I don't know about petrol, maybe a $0.20 per litre increase? That tax revenue stream will be showing an unanticipated boost.

Okay, for a business, that gst component is offset as an input cost. But gst liability for a registered trader is a proxy indicator of profitability.

If business gst liability in current and near future return periods remains the same as pre 28 February is that an indicator of traders being substantially squeezed? I.e. sales pricing reflects lower margins for those traders?

The OCR hasn't been influencing what is actually being charged to borrowers for some time now. If you look at the 1 & 2 year rates, they're back up to the same level as when the OCR was at around 3.25%, so we've effectively had the equivalent of 100 basis points in tightening since December. That will be taking a lot of wind out of our sails right now, so I do understand why the RBNZ is reluctant to jam on the brakes any time soon - even with the inflation spike we're experiencing right now.

Yeh true, thats the bit that seems like its getting a bit lost

OCR still 2.25 but mortgage rates have already done a fair bit of the tightening.

So we’re kinda already seeing the effects people are worried about, just not coming from the OCR itself.

Wouldn’t surprise me if the OCR just stays where it is for now.

A balancing act?

According to google AI:

Following the 2023 amendment to the Reserve Bank of New Zealand Act, the RBNZ mandate focuses solely on price stability. The primary mandate is maintaining low and stable inflation between 1% and 3% on average, with a focus on the 2% midpoint, removing the previous dual focus on maximum sustainable employment

Sounds pretty straightforward doesn’t it? Inflation above 2%, push lever up. Not sure how they could draw any other conclusion.

Will it work? Probably not, but they should have thought of that before now.

Not quite that solely simplistic, note also Operational objective 2ii: "...the MPC shall...seek to avoid unnecessary instability in output, employment, interest rates and the exchange rate"

https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/monetary-poli…

It's a straightforward dilemna: Worsen the economy by raising interest rates (leading to higher unemployment and more business failures), or let inflation run above target by not raising interest rates. Since raising the OCR in NZ cannot lower imported inflation due to higher oil prices, the RBNZ's path is easy to predict. The projected inflation is due to a supply shock, not excessive demand. No changes to the OCR for the foreseeable future and IMO none for 2026.

I warned about 18months ago that central banks will have no choice but to learn to live with higher inflation rates, and that they will most likely raise their "target" rates. This time is coming soon.

I would have thought raising our interest rates could increase the NZ$ relative to the US$, reducing the cost of imports, including fuel.

In a stable economic environment that usually works. But with the current global clown show to contend with, the currency traders are very much on the defensive.

At the margin, yes Norm, but it is far outweighed by increasing the cost of money on top of the increase in the cost of goods and services.

Above you said cannot, I'm saying could. I'm not discussing "at the margin".

It depends upon the perceived relationship between the two....and that perception need not be correct.

Crucially we have no control over the dominant factor....and the previous accord has been abandoned.

But it could.

I dont think it ever could....they attempt to control the quantity and ratios of the dominant currencies and the tools they have are inadequate and badly lagged.

Are you saying it couldn't?

I'd suggest if it did it would be the result of good luck rather than good management....there are too many variables they have no control of and they are reactive by design and necessity.

In other words, expect this year to be another dud.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.