By Gareth Vaughan

Officially New Zealand only has one state owned bank, Kiwibank. But, with COVID-19 smashing the economy, the entire banking sector has now effectively become an extension of a socialist state.

It was just a few short months ago, with the Reserve Bank proposing to increase their regulatory capital requirements, that New Zealand banks were telling us how strong they were. The Reserve Bank’s risk appetite was too conservative, their lobby group the New Zealand Bankers' Association said.

Boy how things have changed and how quickly too. Over recent days banks have received so many different forms of government and central bank assistance, in order to keep their credit/debt conveyor belt flowing, that it's hard to keep track of them all. Of course this corporate welfare comes as authorities try to cushion the impact of a recession stemming from a pandemic whose human and economic costs are unknown but will be significant, and potentially enormous.

The latest government assistance is Finance Minister Grant Robertson's announcement of a $6.25 billion Business Finance Guarantee Scheme for small and medium-sized businesses (SMEs), alongside a six month principal and interest payment holiday for stressed mortgage holders and SME customers whose incomes are hit by the economic fallout from COVID-19.

The specific details of the mortgage holiday are being finalised, with banks to make these public over coming days, Robertson says, adding; "The Reserve Bank has agreed to help banks put this in place with appropriate capital rules."

The Business Finance Guarantee Scheme has a limit of $500,000 per loan and will apply to firms with a turnover of between $250,000 and $80 million per annum, with loans for up to three years to be provided "at competitive, transparent rates." The Government/taxpayer takes on 80% of the credit risk, and banks 20%. Other government moves to counter the downturn include a wage subsidy scheme that's expected to cost $9.3 billion and be available for 12 weeks, while rent increases are being banned.

Last week the Reserve Bank launched a term auction facility designed to alleviate pressures in bank funding markets. It gives banks the ability to access term funding, with collateralised loans, for terms up to 12 months. To help keep the lights on in the financial markets the Reserve Bank has also unveiled a $30 billion quantitative easing programme, and cut the Official Cash Rate by 75 basis points to just 0.25%.

It has also deferred those bank capital increases, which were to be phased in over seven years from July, for a year. And topping it off, buried in the Robertson/Reserve Bank's Tuesday press release was news banks' core funding ratios are being reduced to 50% from 75% - for an unspecified time - to help banks "make credit available."

The core funding ratio was introduced on April 1, 2010 to reduce New Zealand banks' reliance on short-term offshore "hot money" funding after credit markets froze during the Global Financial Crisis. It requires banks to meet a minimum share of their funding from retail deposits, long-term wholesale funding and/or capital. Initially set at 65% the minimum was increased to 70% in July 2011 and 75% from the start of 2013.

Some banks had to work to get above the initial 65% level. The core funding ratio also won the Reserve Bank international praise, with a similar net stable funding ratio subsequently included in global Basel banking standards. Winding this back so far won't have been a decision the Reserve Bank took lightly.

The banks' core funding ratios certainly started this crisis from a strong position. As of December 31 the big five banks' ranged from Westpac's 83.1% to Kiwibank 90.1% with smaller banks even higher.

With many countries now in a fight to minimise the human cost of COVID-19, the economic and financial side effects are going to be massive. New Zealanders head into isolation in their own homes for a minimum of four weeks from tonight with much of the economy also shutting down. Against this backdrop the authorities are doing everything and anything to try and keep the wheels of the economy greased. Hence they're desperate to assist our debt peddlers to keep peddling debt during these traumatic times.

There will be a spike in banks' bad debts as recession bites and unemployment rises, potentially higher than the 10.7% modern era peak from 1992. By helping borrowers the government and Reserve Bank efforts to cushion the downturn will reduce the negative impact on the banks. In this environment close scrutiny will be on bank dividends and profits with all key players in the NZ Inc waka needing to paddle in the same direction.

Interestingly there has been no specific intervention on behalf of savers so far. The Government last year committed to establishing a deposit insurance scheme that will insure deposits up to a limit of $50,000 per individual, per institution. This is taking place via the ongoing review of the Reserve Bank Act. Robertson last week said there are no plans to hurry this along.

Announcing the move to lock-down on Monday Prime Minister Jacinda Ardern spoke in brutal terms.

"New medical modelling considered by the Cabinet today suggests that without the measures I have just announced up to tens of thousands of New Zealanders could die from COVID-19...The worst case scenario is simply intolerable. It would represent the greatest loss of New Zealanders’ lives in our country’s history. I will not take that chance," Ardern said.

With the stakes this high we are entering territory few New Zealanders alive today have experienced before. We are effectively on a war footing.

What the banking industry will look like once COVID-19 is on the run, whenever that may be, is anyone's guess. My guess is what has been regarded as normal in recent years probably won't be normal by then. Perhaps the taxpayer will even be a shareholder in the major banks.

Personal, business and government debt levels are set to rise. In some cases sharply from already high bases. We can expect more action from authorities, perhaps including a loosening of bankruptcy rules. And maybe down the line we could be seriously considering some form of debt jubilee, or debt cancellation. But that's a subject for another article.

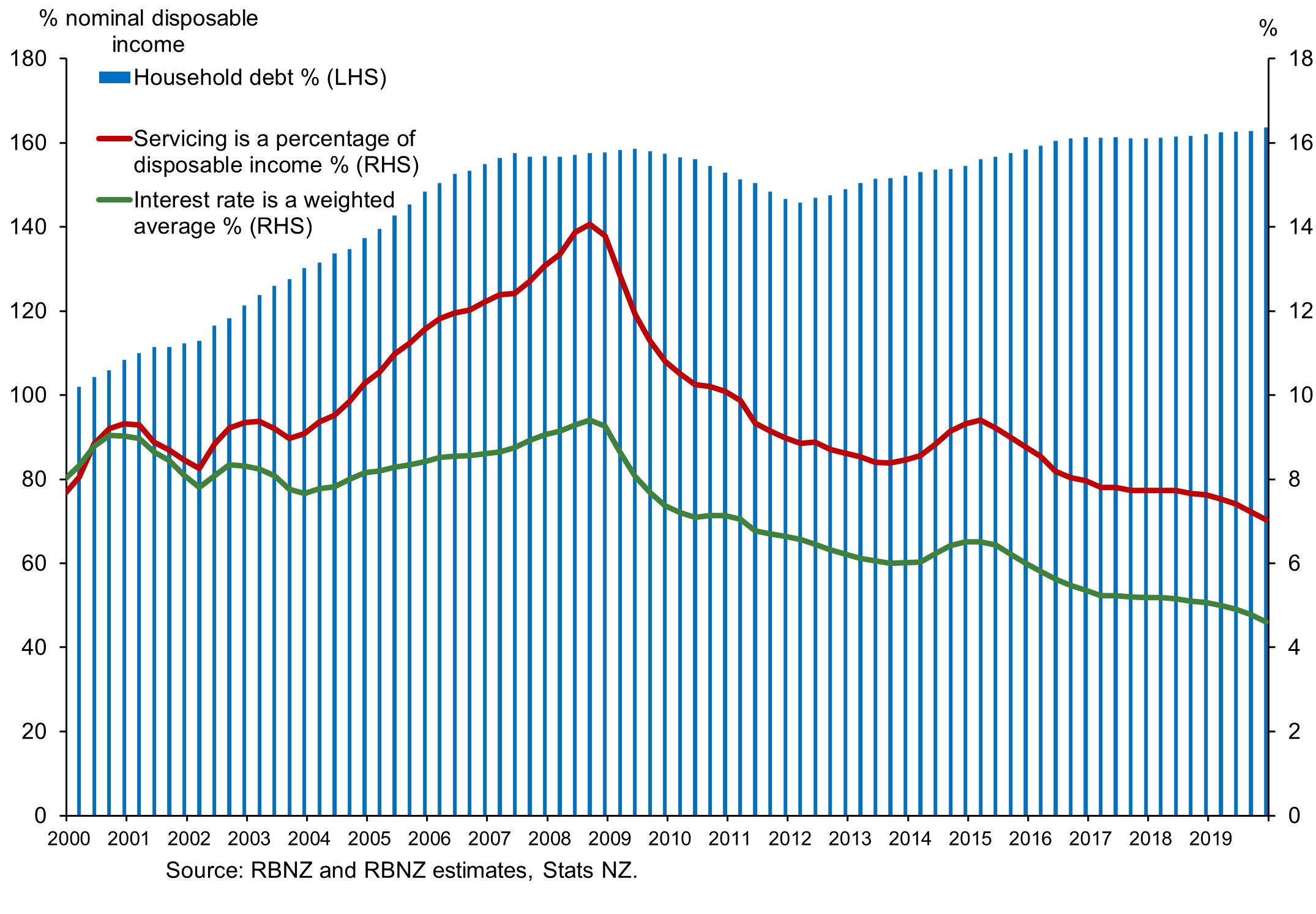

Household debt

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

119 Comments

This is truly shocking behaviour by the government. Basically encouraging you to take on more debt by virtul signaling that it doesn't matter if you don't pay it back "We have got this" in other words we will come to the rescue if you bite off more than you can chew. Sorry but from experience here business rip the profits while times are good but suddenly cannot last a matter of days before they scream help in a downturn. The time for the big reset is here, don't try and stop it.

The old classic, "privatise the profits, socialise the losses".

Politicians ignorance and incompetence sees them pampering to these crocked oversea banksters.

Encouraging the masses to take on more debt is not the solution? They are swimming in debt and the high costs of living it has brought with it.

Rather than government bonds, that will largely be picked uby overseas interests (increasing the future dividends they collect with it, for god sake print some money and hand it out to the masses as a universal basic income. This is the most efficient and equitable means of delivering social welfare.

These tax havens need to be shut down, and expose those who are the main benefactors of lending money. Before this happens, alot of politicians will go missing or change their name or appearance.

How is it hanging guys?

COVID-19 will be gone but the world will be a different place.

COVID 19 will go down as the tianemen square of our generation

Xingmo, are you under any kind of lock-down there in Beijing?

CCP FTW?

Welcome back mo, we were beginning to worry you might have been recalled to party headquarters for re-education?

Those red blood Italians, started to see the influx of Chinese tourist, student, business, people migration etc. in the name of 'wealth, prosperity' - shall see it now from different perspectives, Then watch out their reactions.. started 2021.. then the rest of the world to follow suit. They shall just simply have to follow an old advise.. don't put all your eggs in one basket. China current economic strength it's from massive cheap labour, to supply the products to the world, even to put their engines to work? the oil have to be imported from Saudi (how big is China natural resources again?) - This event, just simply a reminder to the world of diversification, different countries, location,.. wealth distribution in the end.

So there needs to be a debt jubilee to save those who were irresponsible, while those who were prudent and saved are punished?

Consumerism based economies can run because these 'irresponsibles' spend.

The cost of living is so high, many Kiwi's are simply unable to put aside enough to have a cushion to get them through this sort of shock, living paycheck to paycheck.

How cold-hearted do you have to be not to get that? Many of these are not home-owners either, where most of the resentment here seems to come from. I'm not a huge Ardern/Labour fan, but I think she's done a great job, consistent with the support in the UK (10% of GDP), Germany (30% of GDP)

I think I've been missing your point Te Kooti the last few posts. Those who are struggling to get by have been and will be receiving government support.

The crux of the issue is that we've allowed too many to gamble on the future and now we might end up in the situation were prudence comes to the rescue to the unwise.

Feeding carrots to fools instead of applying the appropriate stick simply creates more fools.

I think what the OP is alluding to is that property investors mortgages will be paid by rent subsidies. So basically that the state will now prop up the very speculators that have caused our ridiculous high living costs

Supported by overseas banksters, who care not for social consequences of high leveraged prices but profit maximisation.

Then when the going gets tuff for these banksters, they get a government guarantee to help themselves to more profit.

Lending should be restricted local ownership, so they bear the consequences of their actions, rather than the current faceless overseas banksters.

If unemployment gets beyond 250,000; which I'm thinking it will, I wouldnt want to be a local bank manager.

The cost of living is so high, many Kiwi's are simply unable to put aside enough to have a cushion to get them through this sort of shock, living paycheck to paycheck.

I think you will find "most" NZ h'holds are living paycheck to paycheck, whether they're beneficiaries or high-income earning h'holds. But that hasn't stopped the banks leveraging the nation to the hilt on a goddam housing bubble. For a NZ h'hold (with the means to do so), the idea of a rainy day fund is quite foreign I would suspect. There is no definitive data that I'm aware of, but in Australia the ME Bank Financial Comfort Survey (going for approx 10 years) suggests that approx 70% of h'holds have <$50,000 of cash savings while approx 50% have <$10,000.

Imagine how healthy the financial sector would be if loans had to be 100% backed by deposits?

Be like moving back towards the Gold Standard which by the sound of it didn't work for the US during the 1930's depression.

The creation of financial instruments prone to abuse don't seem be helping us in the "modern" system, however.

You mean mortgages? Using fractional reserve banking?

It's okay when interest rates are regulated and asset prices are kept under control. When banks lend too much assuming asset prices will continue to rise, then you find yourself up a brown creek with not much of a paddle (even lower interest rates...)

I'm not very savvy with the workings of financial institutions but what I would say is irresponsible lending and credit creation for the purpose of asset speculation has really undermined our society. The natural osmosis of investors chasing the highest returns was always bound to expose the fundamental flaws in this behaviour. Unfortunately, we all have to pay the price.

Depends on what the debt is for TK. A blanket debt jubilee may actually encourage bad behaviour. Some degree of selectivity would be useful.

I agree, but it's not practical to discriminate.

It's not practical to give anyone a debt jubilee.

You know you're just going to have to get over it right?

Nope.

Unless you want to deal with a revolution.

Because that's how this ends with a debt jubilee.

I'd prefer people endure some tough medicine.

That's what's needed, not just another can being kicked down the road.

I'm sure this is an educational experience for you.

Have you looked up moral hazard and incel from yesterday's lesson yet?

I'm thinking a few hundred angry pakeha with term depo's isn't going to frighten too many people.

What has this got to do with race?

FYI, I am Ngāti Toa.

Nice of you to turn it into a race issue though.

And I don't have one single cent in term deposits. Not one.

So, also, nice of you to be dismissive of those who do though. Mostly the elderly living on, increasingly, limited means.

I'm not elderly too before you hit me with some generalisation there - I'm 37.

Ain't no party unless it's a victimhood & identity party though right.

You're really pushing for this debt jubilee.

Must be feeling the heat for some reason - worried about asset values perhaps?.

You're far more worked up about this than I am. I do have term deposits (terrible investment) and I'm not accessing any of the schemes announced.

None of my comments are from my own personal situation. The pakeha comment is humor, not identity politics. Does that clear it up for you?

I don't tend to make "jokes" that include race.

It's not that "humorous" when the shoe is on the other foot, so why would I do it to them.

Just me maybe.

Why aren't there any angry Maori with term depo's?

Agree - cmat. If there are debt jubilees I think our society will break down. There would be zero equity and would result in some form of revolution.

At that stage you may as well nationlise the housing stock and start dividing it up again to ensure everyone is housed. Because personal responsibility and financial management will have lost all meaning. And investors will have proven themselves incapable of managing their own affairs.

Perhaps things are going to normalise sooner rather than later? Certainly the recent upbeat Interest.co comments have reverted back to their usual resentment and bitterness.

Oh boo hoo personal responsibility is such a bitter pill.

It was so mean of that Bank to force all those people to sign up to mortgages;

So mean of the Bank to give them as much debt as possible after borrowers shopped the market for as much as they could get;

So mean of the Bank to provide the funds that allowed people to win auctions and pop champagne; and

Now it's so bitter and resentful for other people who didn't get 'forced' into that debt and pop champagne to feel bitter and resentful about bailing out these people.

I really feel sorry for those people, being forced into such an oppressive situation against their will.

Some bizarre cognitive dissonance going on here, indeed.

Do you have quite a bit of debt Te Kooti? Just trying to put myself into your shoes and understand the heuristics/biases.

Mostly freehold as it happens.

Well done!

My heuristic is I'm a big believer in home ownership. Positive benefit to society and it indexes families to rising house prices. It fosters a sense of community.

Did anyone pay any attention to the graph in the article? Housing affordability has improved dramatically over the last decade, where is the case that people are locked out?

It's not affordability of servicing the mortgage, it's getting the deposit in the first place.

The economic finance system my friend has been encouraging us all to get indebted and be irresponsible for 45 years

Falling interest rates since the mid 1980's has fooled many people into thinking they are smart property investors...will see what happens when interest rates regulate. Valuations like bonds - prices fall when rates rise.

Regulation will be in the form of lower wages and lower prices; the result of high unemployment, rather than increasing interest rates. Banks cant afford to lift interest rates in a hurry, as they risk loosing their share they have remaining.

Dont expect property appreciation any time soon. Investment prices should be based on positive cashflow returns, and with events like this, the yield paid in the future is likely to reflect the risk involved; which the majority of investors have little understanding of until now.

Now NZ has its very own REPO market launched by the RBNZ

"Last week the Reserve Bank launched a term auction facility"

It always had one, it just wasn't used as it was too expensive.

The government are mugs, clearly the lobbyists ran rings around Robertson and co. Banks should have been sharing the risk 50/50 with the taxpayer.

Look at the more hard-nosed Aussie government and what they mandated.

is it kind of start of English-speaking USSR state I wonder. Err, and if you don't like what government does , you can't actually run away , they say you "Stay at home!!"

Just remind me how much the executives/management of our banks are getting paid? There should be nobody working in any bank earning more than an MP right now given that they can't stand on their own two feet.

Gareth - can we confirm please if any bank staff have lost jobs/are losing jobs at this time and whether any reduction in wages across the board has been announced? If not, please ask why this isn't the first action before tax payer assistance is even considered.

Independent Observer what are you going on about - banks can and are standing on their own two feet, this isn't a banking crisis - if fact so much so the Govt & RBNZ are asking for their help in supporting the economy, not the other way around. The GFC was a banking crisis globally, and although the NZ banks the better of them. they still required support at that time to get through because their funding markets closed down on them for a few weeks, but this is totally different and banks are much longer term funded.

If only all businesses had followed Bill Gates and always had enough resources to operate for one year without income. He did this early on after having a nasty period where no income came in and swore to not have that stress again. Apparently Microsoft can still do this.

I have always followed this principle as well. I have always arranged things so that I can meet all expenses with absolutely no income for one year or more. This should be like an essential for everyone. Yet you have people who would rather have tattoos than an emergency fund.

So pleased to hear this.

Now hand it over so the rest of us can continue with the Ponzi party.

Haha exactly - those who have saved enough to be self sufficient for a year (or more) may take a haircut for those who have decided to gamble it all on outrageously expensive housing (which by any measure was likely to a very risky move).

Give the fools sticks and the wise carrots.

The incentives being used are 180deg out from any type of moral compass that will make the future better than the past.

I have always followed this principle as well. I have always arranged things so that I can meet all expenses with absolutely no income for one year or more.

Well if you do, good for you. But I'm not sure I believe you based on your track record of what appears to be trollish tendencies on interest dot co.

I can see why you may think that but I have consistently said that I am very frugal. I've also had my wagons circled for a couple of years now after becoming subtly influenced by the DGMers.

Some thanks we've got from your comments over the past 12 months... :/

All these [reformed] spruikers now dancing on the heads of pins.

My name tends to get left out of the list of spruikers and usual suspects these days. I was pretty open about doing all you could to get positively geared with the changes in tax laws and landlord rules and had stated I had circled the wagons but was getting pretty bored. However I feel I have the whole Apache nation whooping and hollering all around me now! So thanks guys!

Good for you.

Genuinely.

Don't worry, ZS. The Hollering Hordes are only firing virtual arrows, whereas your situation is real, physical, and (it seems) comfortable. Maybe them Hordes are just plain Jealous?

Meh.

I'm in 100% cash and liquid securities - I'm up 10% in the past month.

Who am I supposed to be jealous of?

I'm sure Waymad wasn't referring to you as part of the horde. Not quite sure what he meant actually. It sounds like you're in a castle on the hill while I am down on the plain. Relatively safe for now but we are not entirely safe and may have a long fight on our hands.

Being in one asset class is not prudent, even if it’s doing well right now. I have an unencumbered house, no debt or contingent liabilities, with the rest in TDs and cash (even KS is in cash), and feel exposed. I’m moving into equities through Simplicity funds to balance my asset exposure. My wife is also proposing converting the garage to a separate 80m2 unit for our children to use. I have no interest in outside tenants.

I'm not in one asset class.

Cash

Bonds

Commodities

Other hedged derivative products

Got out of equities in January.

Looking at getting back in to particular select stocks on case-by-case basis.

I completely agree. Well said.

Microsoft have the biggest rainy day fund of any company in the world, I believe. At something like 135b USD.

Dude, which planet you're coming from? tell me if Bill or you have or ever.. or never expected to have a stadium 4 cancer? - mate, you won't believe how many property moguls bigger than you.. were in our terminal care.. you just & won't believe it. It's harrowing & sad.. your Wealth seems something you would like to confidently flaunted .. even to the level that will make you worry free about your Health status. When you get this Covid-19 or say stadium 4 cancer? - I suggest to please.. never talk of such non-sense when you're in ICU ward or Cancer ward to those junior registrars.. which .. despite they're in 6 digits salary, some of them still paying the student loan.. and? yip, still renting. Dude..

A well-written article, hinting at what's to come in a dispassionate way. I am sure all of us, and those in our wider circles, can comfortably understand it. I'll be referring those who have any concerns to it for a first-up read.

"Interestingly there has been no specific intervention on behalf of savers so far." They don't need to say anything at this juncture. NZ does not need to to be overrun with offshore funds looking for a sovereign safe-have above what is required. That savers are protected by the implicit Government guarantee at times like this is a given. They may say something at a later stage if necessary, but that will be into a 'new' environment of New Zealand banking. (ie: the entire banking sector has now effectively become an extension of a socialist state.)

With housing wealth at 4.5 times GDP , surely New Zealand has the underlying wealth to weather any financial storm , or is that the problem

Just watched Dr Fauci spend the best part of the latest briefing, scratch all of his head, place his hands on the podium, followed by orange Daffy.

We'll be drawing down on that wealth, don't you worry!

The obvious way is to redirect any future debt into 'other things' and not property.

Property values fall = Other industry value rise ( very simple equation, but you get the idea!)

Quite the opposite.

When things settle down, people will buy property to secure their futures, shares will be a gamble.

Hopefully the sharemarket bounces back or retirees are going to have to stay in work longer.

For that, we need to work to make housing more affordable for more folk so that they are secure in their future. Enough of it being a speculative investment vehicle for a few who then expect to be rescued in bad times.

If sanity prevails, when things settle down people are going to be afforded a hell of a lot less debt.

New lending will have very strong DTI restrictions.

And many will be stuck in equity traps for a long, long time.

We obviously need to learn that lesson though. Having lived in the US through the GFC and witnessed first hand the outcome, the culture we have/is in NZ towards debt/property is/was very foolish.

A generation of property owners being scarred with an extended equity trap is a harsh lesson.

Watching John Key and Bill English saying we should be celebrating having some of the worlds most expensive houses nearly pushed me over the edge a few years ago - knowing the damage that could be done by having this much leverage against the property market. But when politics becomes so selfish that its is just about you, now, and not all Nz'ers, for the future, then it shows the character of parties/people.

Absolute muppets, indeed.

Was it you Rick that recently posted the quote along the lines of:

A society grows great when old men plant trees whose shade they know they shall never sit in.

I think my grandparents did that (grew up through the depression and fought in WW2) for my parents generation. Watching Key and English make those statements, while JK then sells his house out to a foreigner, is a complete sell out.

It actually makes me physically sick. And dont mention the mans knighthood.... yuk!

It will appear clear to everybody, once the housing bubble burst, that no asset class is risk-free, regardless of the King Canute efforts of the RBNZ to stop the incoming tide. And it is going to be a very expensive lesson, notwithstanding the delusional wishful thinking of many commentators. The fundamentals of the economy will reassert themselves, and once the price discovery mechanisms in the housing market start to function properly, an almighty slump in real estate prices is going to prove unavoidable. QE, OCR and similarly desperate moves are not going to change its progression, but only to postpone it by a little.

We can but hope, re 'affordable' housing. If the Gubmint is gonna give itself the power to alter any law, any time, with zero prior consultation let alone sound advice, let 'em hack away the TLA's monopolies on inspection, wipe zoneration by declaring all District Plans null and void by lunchtime, declare housing factories and their supply chains Essential Businesses, and watch those houses roll out the door onto sections costed at rural land raw prices plus regulated amounts for three waters etc. Move the displaced brown cardies into them Factories. Instant productivity improvement.

Does anyone know if the banks have been asked to suspend their dividends while they are receiving government support

Banks have been making huge profits over the good times but at the the first sign of a downturn they go to the government for help

The shareholders need to share in the pain like all of us are doing.

At least Air New Zealand have suspended dividends

Many business owners have bought their new boats and toys while times are good but some are being very quick to lay off their staff

Everyone needs to do their bit in these uncharted waters

The major banks aren't 'ours' to tell them what to do. They have foreign parents who'll want every cent they can get.

Taxation changes may convince them otherwise. But as long as they are offshore banks, they can and will do what suits them.

Banks aren't welfare agencies at the best of times; especially foreign-owned banks and these are not the best of times.

(What would you do if you were struggling at home, and you had an offshore subsidiary that could provide you with cash flow? I doubt you'd leave it there!)

Our government (and the RBNZ) control the conditions under which they have a license to operate. They can change these conditions.

Given the decline in market cap, dividends will be on the chopping block. Given the housing market has effectively shut down on both sides of the Tasman, the banks are on the chopping block.

The banks will primarily become one giant call centre in the coming weeks, (hopefully not outsourced to India ), providing information on mortgage holidays.

Fletcher Building has scrapped a dividend payout to shareholders which was due to be paid in just two weeks' time.

Fletcher Building pulls dividend and guidance on rocky times ahead

A dividend payout due in two weeks has been ditched, the Rocla sale process halted and profit guidance pulled as the dual-listed group heads for rocky times.

afr.com

What Govt support are they receiving ? You mean the RBNZ changing their core funding ratios etc because they want to banks to lend more to support the economy - hardly support, more like setting them up.

A question: During the Key administration, Parliament debated and passed some kind of regulation that allowed our banks to establish and trade in some kind of debt instrument that was high risk and of the kind that had created havoc in the US. Does anyone recall what exactly those instruments were called? I need to look up the Hansard record on that debate.

(Someone will know)

Found it (the Reserve Bank of New Zealand (Covered Bonds) Amendment Bill)- and interestingly, Steven is the first poster on Gareth's article on it;

https://www.interest.co.nz/bonds/60147/covered-bond-opponent-urges-parl…

What on earth are you talking about? Covered bonds are at the safest end of the spectrum. How on earth are these anything like the CDO rubbish that was thrown about in the GFC?

All they are is an additional guarantee on top of bank debt to say if the bank falls over you have these mortgages on houses as security.

A few weeks ago I asked a question if a swing back to centre would be recognised as such or would the accusation of "Socialism" ring loudly. Gareth's headline seems to prove the latter.

Under the current situation, the broad picture is what I believe the Government needs to be doing. Yes there is some devils in the detail, but as Te Kooti identifies, this Government is doing very well, but are they turning Socialist? I feel they are just apply socialism where it is needed in a time of crisis, but I could suggest there are areas where they are not doing enough, and some where they have gone too far.

It might appear we're going to apply carrots were there should be sticks, and sticks where there should be carrots.

Filled on all 250m. RBNZ said they had offers submitted for 810m First QE

Finally the commentariat mentioning debt jubilee that Steve Keen came up with in 2008

Just out luck it hits in election year (both here and in the US). This 6 month mortgage holiday will last until the election. The consequences of QE and increased debt will not be felt till well after that. The banks can ask for whatever they want for next 6 months and our MSM will be too stupid and dependent on the ad revenue to think of standing up to them.

The next step will be to ban cash for convenience and health and safety. Full digital currency and block chain central banks. You will have 6 months to return notes and coins. All central banks led by the fed will insist on a new global digital currency for the world, including a global UBI for everyone. However you will have to conform to all the rules and regulations set out by our new masters. Like what you watch and wether you have had the new covid antidote etc..

I hope they let us go fishing!

Just go off the beach thats the safest way. I live 5 mins from the beach so I'm planning on some self isolating surfcasting

Not what Clarke Gayford said and he's 2IC. I wouldn't site Stuff as a credible source either

Encouraging people to take on more debt is about all thats left in the toolbox. With Interest rates having been quickly reduced after the GFC they have continued on a downward trajectory since. Many households are maxed out now before we have shutdown for a month. Short term financial aid may work for a few weeks but all hell could breakout afterwards.

It honestly is like telling a drunk to drink his way through his addiction, meaning you don't have to face the pain of your problem today.

Utterly shameless, flagrant, opportunistic,orgiastic and gratuitous socialist takeover taking place in this country right now.

This is Jacinda's dream finally realized. Yet she will have saved... maybe a few hundred who might have otherwise died from flu.

Turning NZ into the utopian Norway of the south. Er, only... without the revenue. Never mind... high taxes!

Bet the people who voted her in never thought one day they'd be giving up more personal control all to be paid by the state.

The piper will have to be paid eventually.

The odd thing is that it is socialism coming to the rescue of a broken capitalist system. And the capitalists appear to be happy for the support. If it wasn't COVID19 that acted as the black swan, it was going to be something else. So do we address the core issue, or do we keep putting band aids on a severed artery?

They're right about one thing though - "The piper will have to be paid eventually", and that's right now. The tune that's been played for the last decade or four had ended. And it's payment time....

Brought to you by Alex Jones's newsletters.

According to the RBNZ two thirds of households are mortgage free. Hence two of the variables in the posted graph above are not applicable to the one third of households that actually do have mortgage liabilities (~$465,000 on ave). Try this adjusted RBNZ version

{kind=link}

Those are two very different looking charts.

Any idea how many property investors were/are interest only?

No.

I seem to remember reading 25% somewhere but that may be overall population so i would expect the number to be much higher for speculators.

God help the people, the socialists are in charge.

Do not buy into what you're listening to. It is bull....t of a global order. The world is in the process of shutting down everyone's livelihoods so that it can save a few thousand people from pneumonia. The stupidity on display here is of mind boggling proportions. We have lost our collective freedoms for who knows how long (no pun intended) for the sake of saving a few thousand sick people. Think about it.

PS: In case you hadn't noticed, we have enough human beings already.

Socialist systems always screw the middle class and workers...that’s just a historical fact.

Debt wipeout will occur because of govt debt more than anything else. They have no intention of paying it back and are going to double it to prove that they really don’t care about it. Buy govt bonds if you want to flush your money down the toilet.

A lot of places are not accepting cash because of the virus. This will be the perfect excuse for the Government with support from Adrian Orr to introduce the cashless society. This will be socialist ratchet and socialist creep that can’t be reversed - this will lead the dark horse for fascism to ride in on. It’s all part of the global elites plan for social control of the masses that allows their tiranny.

Not sure who terrifies me the most.. The virus or the government.

My personal bet Gareth? - The current Worldwide banking, will start to adopt the cooperative banking style, and ditched the good old capitalism systems. Profit sharing, but also burden sharing more tight knit loan/borrower business involvement process, rather than 'water tight' contractual systems (fire & forget methodology).. as it's always subject to 'leak' from both sides.

My advised to govt & RBNZ (I'm glad they really followed my suggestion even to details of rates movement).. Execute the OBR by 2022, you've got no options left. Since none, of you dare to bite the bitter pill, which actually will save the economy.. so yes, go ahead.. put out the country like the rest of worldwide will do. Abort the deposit guarantee/reduce it to 10-15K by this April or? abort, reduce OCR to 10-15%, borrow more, loan more, extend mortgage holiday to 12 months, CAR liquidity 75% to 50% soon make it 25%, CAR from 5 to 7years? make it to either 10years? or abandon the idea, Now do re-visit again that CGT, but in toned down version.. named it as the memoriam naming convention to 'honour the person'. Reduce/remove the LVR, reduce/remove the FHB deposit requirement, make the 40-50years mortgage borrowing as the new norm. Enforce QE more, borrow more, loan more, loosening up for age group loan borrowers & criteria. 2021 is the year for licking the wounds worldwide, 2022 is the actioning.. OBR is just a way to fence off the external banking force which shall swallow the entire.. OZ/NZ combined local banking..'robust ness'.. They robustness claim is as good as JK claimed about AML in NZ, and as good as our border screening in the current worldwide Covid-19 event.

Reducing the core funding ratio is the most insidious step in this package. The discipline of relying less on hot money is gone and the indiscipline of using the funds for speculative lending/investment by banks is going to increase the risks. Hope the banks behave responsibly with the leeway given to them now. And hope it is dialled back, once the crisis is over.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.