Today’s Top 10 is a guest post by Liz Kendall and Miles Workman of the ANZ Economics Team.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

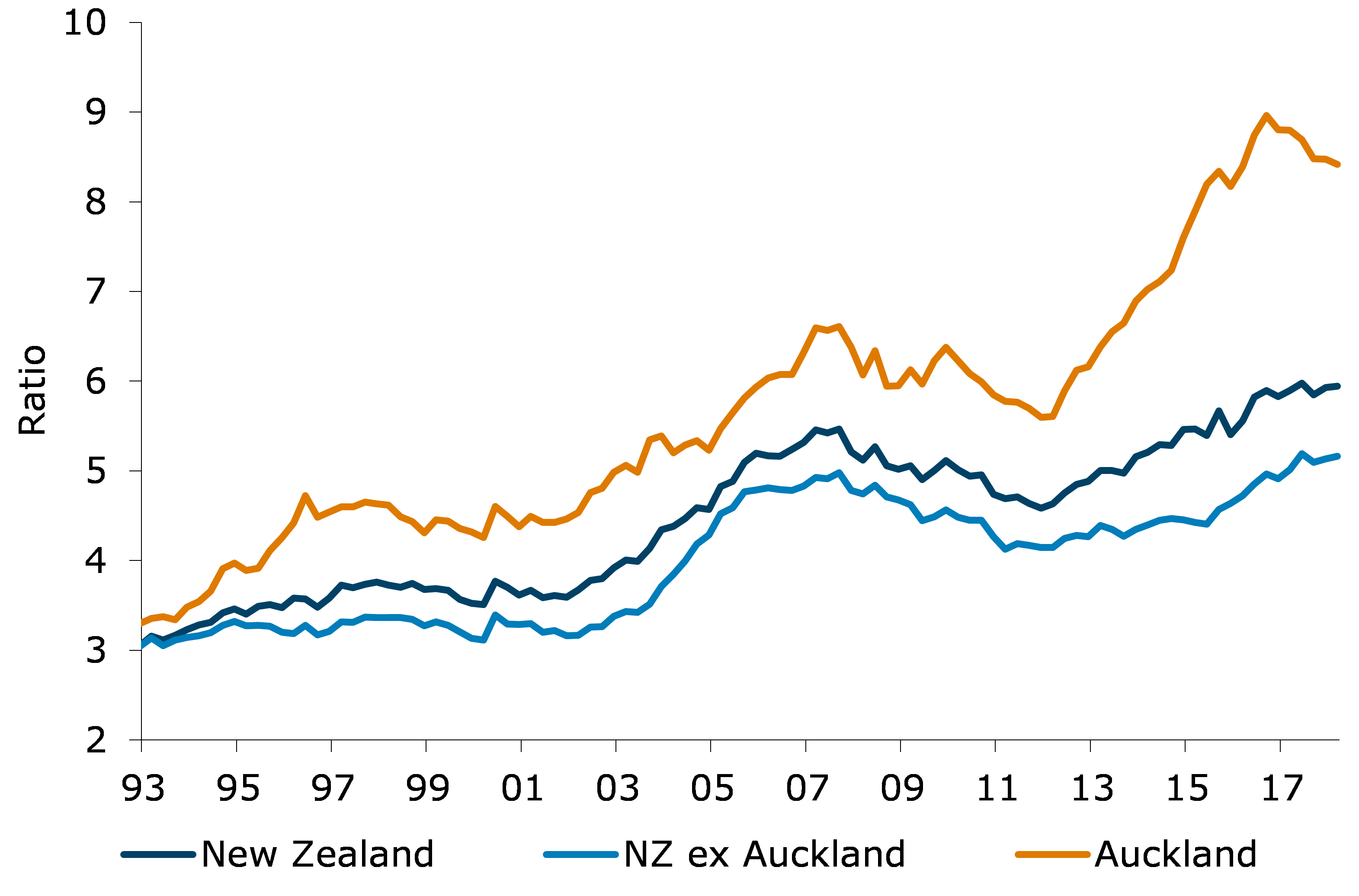

1. Housing is expensive.

It is widely known that house prices in New Zealand are high and unaffordable for many. House prices have more than tripled in real terms since the early 1990s, and are high relative to incomes and on an international basis. But not only that, rents have increased more than incomes over this time as well, meaning renting has become more expensive too, particularly for those in the lower part of the income distribution.

Figure 1. House prices relative to disposable income in New Zealand

Source: Statistics NZ, REINZ, ANZ Research

High house prices have important implications for wealth equality, generational equality and financial stability. They create an obstacle to entering the market, increasing the divide between those who own and those who do not. And when it comes to access to housing, younger generations are now worse off than their parents were. Households have to take on close to record levels of debt to enter the market. As a result, the exposure of both households and the banking system to the housing market is high, and financial distress could result if house prices were to fall sharply.

2. And high house prices have pervasive effects.

High house prices impact our productive potential too. They make it difficult for people to get ahead and it has been shown that poor housing outcomes are associated with poor health and educational outcomes, which in turn then impacts on productivity.

Expensive housing also makes it more difficult for younger households to invest in businesses. This matters because it limits young people in achieving their potential, and also because new firms tend to be more innovative. This is also an issue for existing businesses in New Zealand. When young people cannot afford to invest, it can constrain profitable businesses from continuing to operate.

High house prices make it difficult for both workers and businesses to move to locations that will prove more productive, meaning that resources are not allocated in the most efficient way possible. And to the degree that high house prices are a symptom of excess domestic demand, they will be associated with upward pressure on real interest rates. All else equal, these higher interest rates will result in a higher real exchange rate than would otherwise be the case, potentially stifling exporting and import-competing activity.

Which leads us to our “productivity problem”.

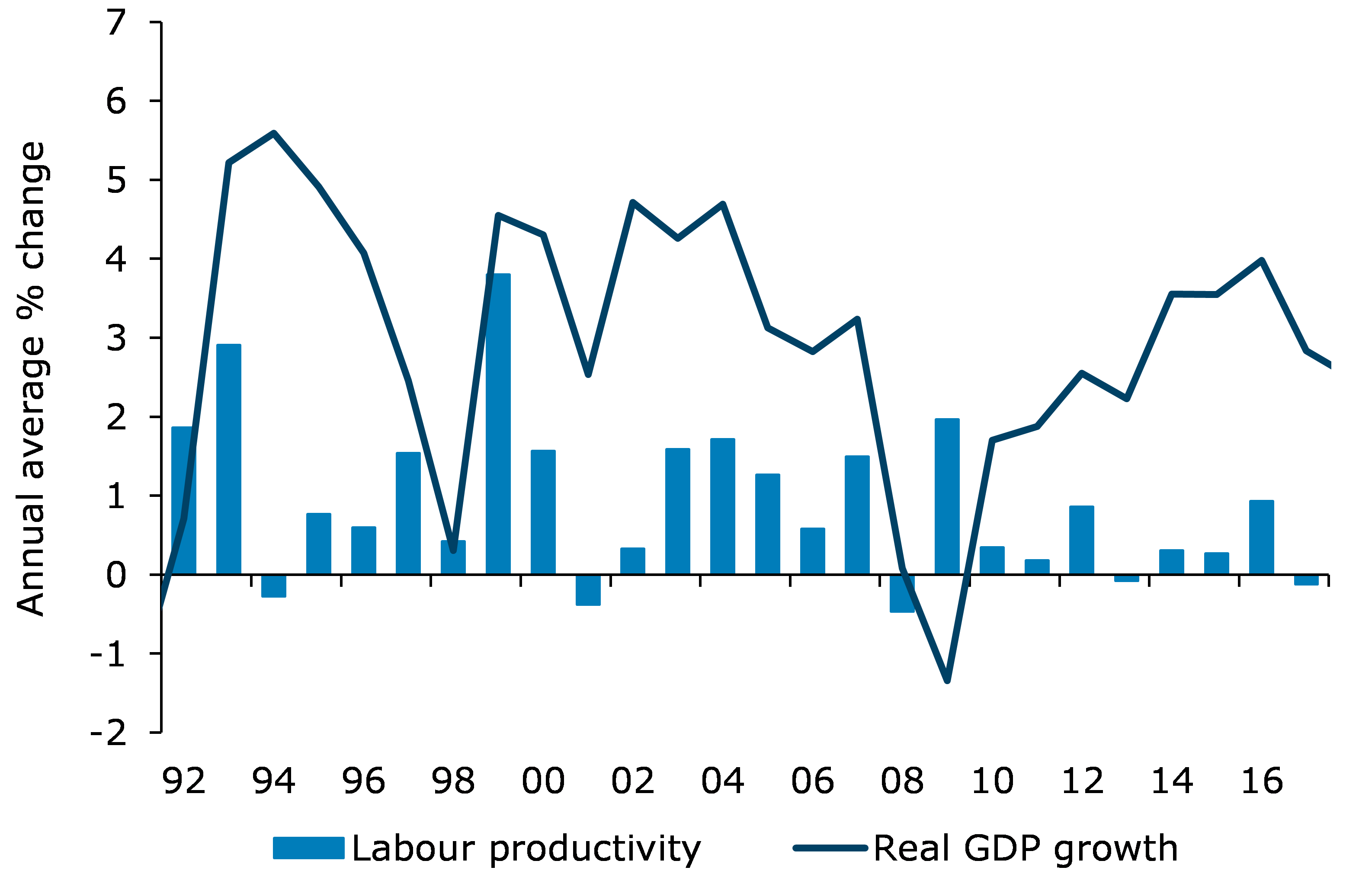

3. Productivity growth is underwhelming.

New Zealand has had lacklustre productivity growth in recent decades – and has consistently been an underperformer relative to its OECD peers. This is important. The most significant determinant of differences in per capita incomes between countries is their productivity performance.

Figure 2. Labour productivity and real GDP growth

Source: Statistics NZ, ANZ Research

New Zealand’s productivity issue is complex. Being isolated doesn’t help, and means ideas and technologies are not taken up here as quickly. Our high real exchange rate is an impediment too, related to our high interest rates relative to other developed nations. Related to high interest rates, business investment is weak. Improved rates of saving would help reduce these costs.

Another issue is that resources are not well allocated. Productive firms do not necessarily have greater market share in New Zealand. Increased competition would help in this regard. And well-targeted migration and upskilling of workers would also be beneficial.

But it’s not all doom and gloom. Sure, our productivity performance hasn’t been great. But ultimately, productivity is about doing more with what we have. It’s about us taking our ideas and initiative and putting that to work – and all of us can play our part in that.

4. The next revolution is coming.

The next industrial revolution is already upon us. Artificial intelligence, robotics and big data look set to revolutionise a range of industries.

These advancements are exciting. Technological change has widespread benefits. It boosts our productivity and prosperity over the longer run, improves our leisure, and can improve health and educational outcomes too. But history tells us that the transition is not always smooth, even if the eventual gains are great.

Often benefits of advancements accrue to firms at the frontier of advancement, while other firms are slow to reap the benefits. And as adjustment happens, workers are affected, with loss of work in vocations that are no longer in demand. Initially at least, the share of income going to workers tends to fall.

In previous industrial revolutions, the social backdrop has been important for smoothing the transition. Universities have allowed ideas to diffuse, provision of education has meant people can gain necessary skills, and state support has helped those whose jobs are displaced.

Perhaps counterintuitively, increased use of artificial intelligence may mean that human skills become even more important. For example, people still want to receive a diagnosis from a doctor who can communicate with empathy, even if technology is used in diagnosis.

In time, history tells us that everyone eventually benefits from disruption through higher incomes in aggregate. But that takes time and adjustment, and ignoring the fact that there are winners and losers would be unwise.

5. We need to be ready.

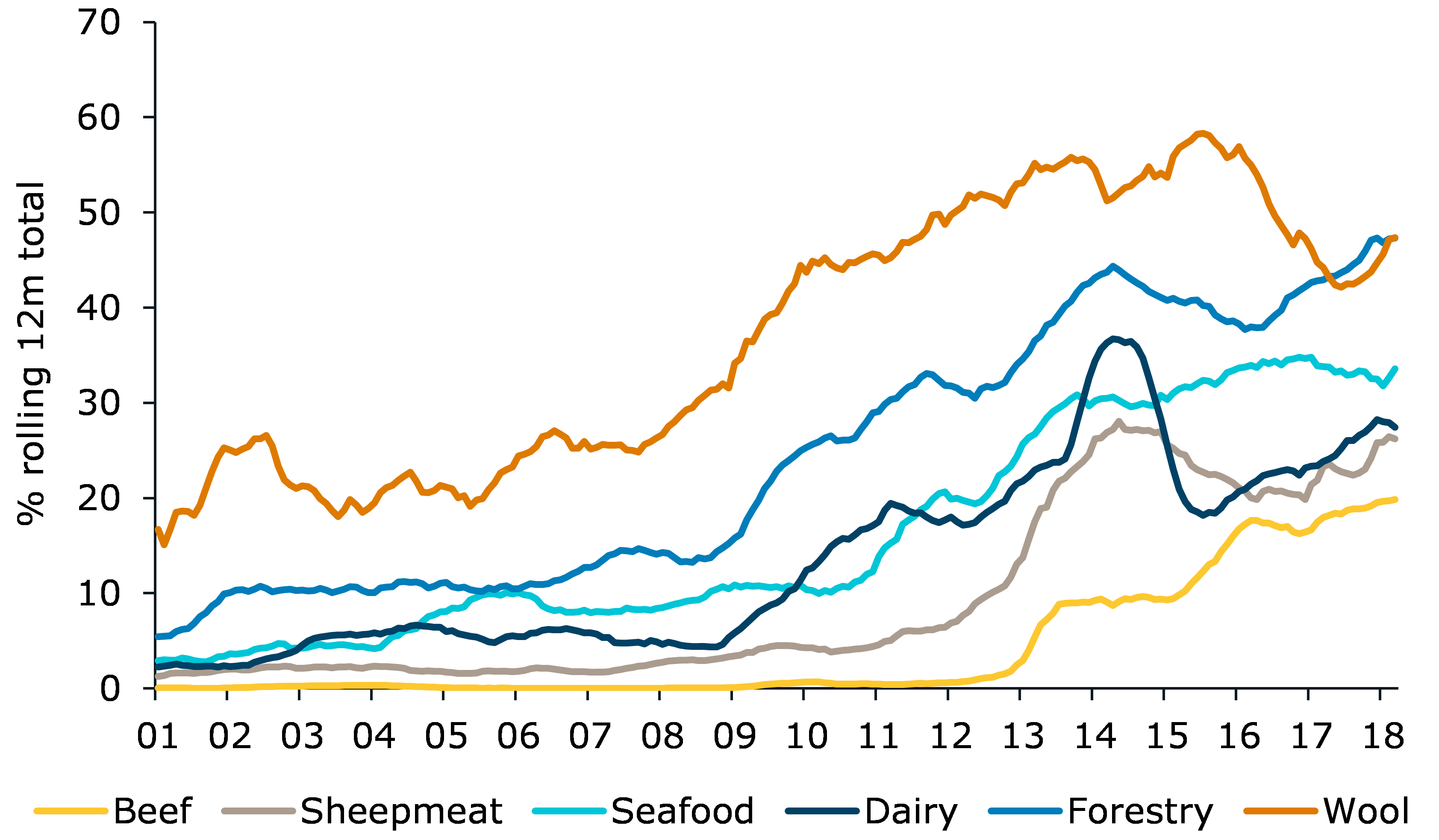

Technology has the tendency to move in leaps and bounds. And as some of the world’s leading scientists turn their attention to feeding the masses in an environmentally-friendly, cheap, and animal-friendly way, New Zealand’s economic model could be in the firing line.

Synthetic proteins could be a real game changer from the perspective of world hunger. The commercialisation of synthetic milk, meat, and other biological products could eventually mean that agricultural production as we know it is no longer one of the primary means of feeding the world.

New Zealand received $22.5 billion in export revenue from meat and dairy over the year to March 2018, comprising almost 8% of nominal GDP. And that’s without taking into account the flow-on benefits to the economy from investment, tax receipts and consumption.

Whether it’s 5, 10, 15 or 50 years away, New Zealand needs to be ready for agricultural disruption. While a market will likely always exist for the real thing, particularly if it’s of high quality, productive resources will likely need to shift away from the production of bulk homogeneous product, such as whole milk powder, at some point.

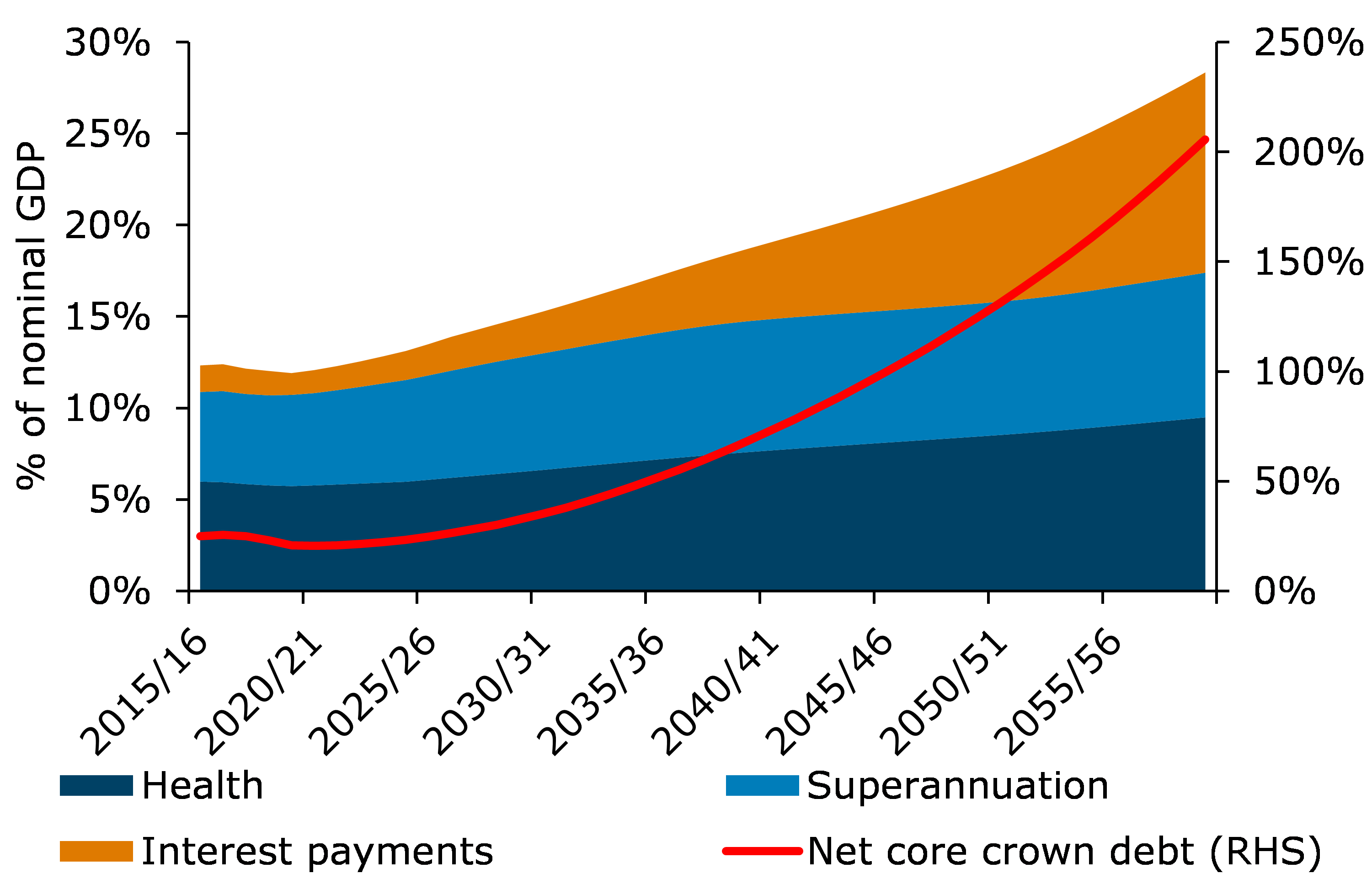

6. Long-term challenges are looming.

Some cans shouldn’t be kicked down the road. The cost of an ageing population is one of them. At current retirement age settings the number of superannuitants is expected to increase dramatically over the next few decades. Add that to the fiscal cost of the public health bill that accompanies the elderly. Something’s got to give.

Increasing taxes or the retirement age are both options, but there is little political appetite to do either. The longer it’s put off the bigger the eventual adjustment.

Figure 3. Long-term fiscal projections

Source: The Treasury, ANZ Research

And all cans should be recycled. Climate change is real and the window we have to address it is shrinking. The likely impacts of climate change include rising sea levels (ports are important economic links, hence our largest cities are often positioned by the sea), and more frequent extreme weather patterns, such as drought (even synthetic milk requires agricultural inputs). Either way, it looks like it’s going to be costly.

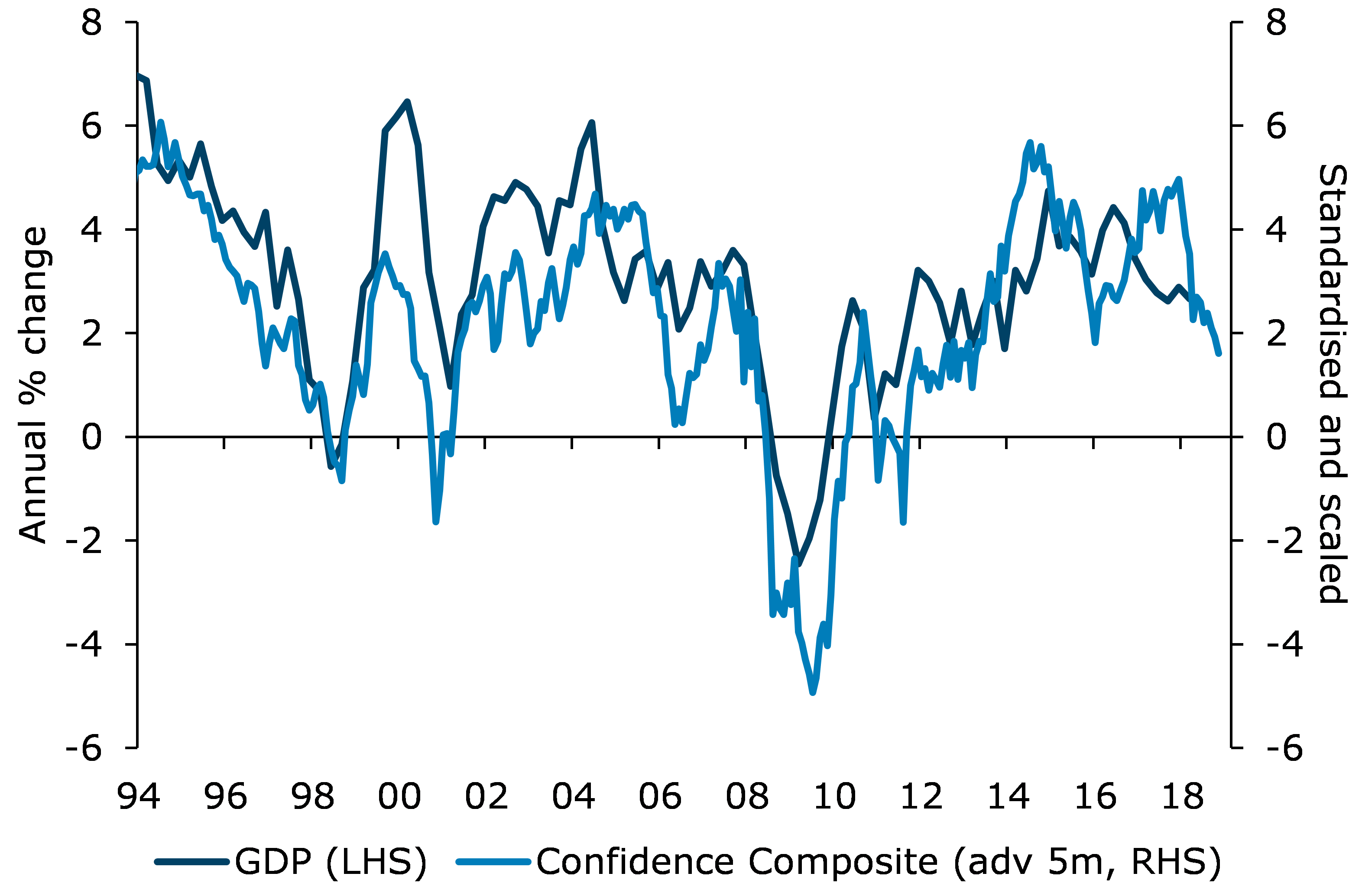

7. Businesses are anxious.

Business confidence has fallen significantly over recent months. In our June ANZ Business Outlook Survey, a net 39% of firms were negative towards the business environment, which – aside from immediately after the election – is the lowest since 2009.

Headline business confidence measures are by nature subjective and can be affected by the political cycle in addition to purely “economic” factors. But whatever the drivers of responses, they are accurate barometers of how businesses are feeling (see our ANZ Market Focus for more on this).

Perceptions matter, particularly to the extent that they flow through into firms’ decision making. And the recent fall in business confidence appears to be flowing through into decisions around investing and hiring. Moreover, history tells us that weaker expectations of profits tend to be grounded in reality.

Overall, the economy has lost some momentum recently and business surveys suggest that may continue. But does that mean something sinister is on the cards? We think no. While business expectations have pared back, they are still consistent with robust (albeit below trend) GDP growth. A number of factors are supporting continued expansion, including fiscal stimulus, income gains (from the high terms of trade and real income growth), and accommodative financial conditions.

All of this suggests the cycle has further to go yet.

Figure 4. GDP growth and confidence composite

Source: Statistics NZ, ANZ Research

8. Trade wars are bad and everybody loses.

We now have to accept that the global economy is in a trade war. The US has imposed tariffs on China, Europe and others, and they have retaliated. Reduced trade will directly dampen global growth, and could have spill-over effects to financial markets, and consumer and business confidence.

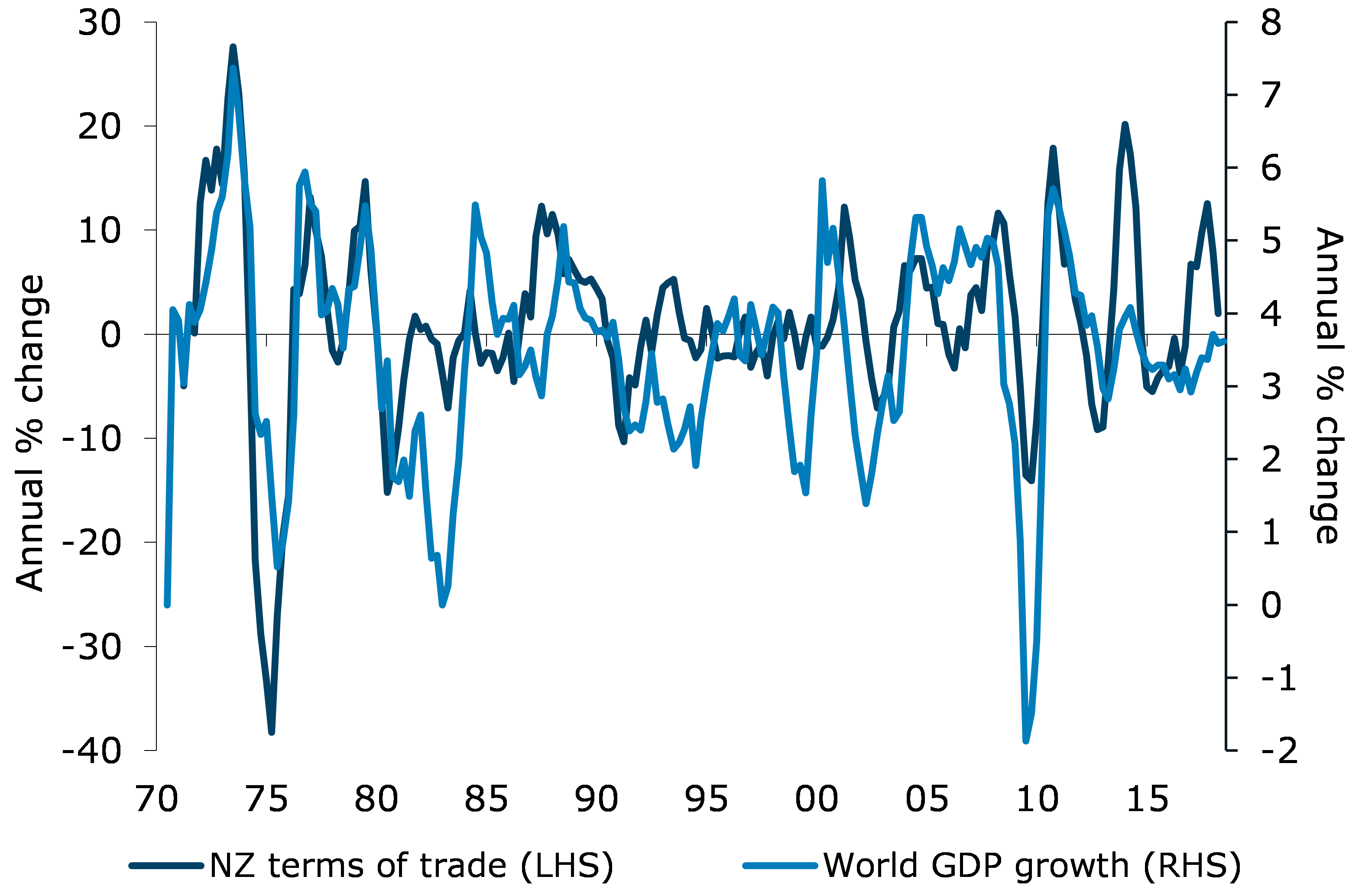

As a small, open economy, New Zealand is affected by the global environment, with prices for our key commodities determined in world markets and directly affected by global demand. New Zealand is well placed to benefit from global growth and trade. But that also means our economy can be buffeted by less favourable global developments. In fact, New Zealand’s terms of trade cycles broadly follow that of the global economic cycle.

Figure 5. New Zealand’s terms of trade and global growth

Source: Statistics NZ, IMF, ANZ Research

Impacts of the trade war on New Zealand will depend on how far things escalate and New Zealand’s own response. In the short run, New Zealand is well positioned to meet Chinese demand for some agricultural commodities in place of the US. However, the more trade tensions escalate, the greater the risk of collateral damage and New Zealand getting caught up in the crossfire.

Fortunately, the global backdrop remains positive for New Zealand. The global economy is expected to grow above trend and demand for our exports is strong. Nonetheless, the possibility that the trade war might escalate and have negative effects means this is something we are watching.

9. Debt, debt everywhere.

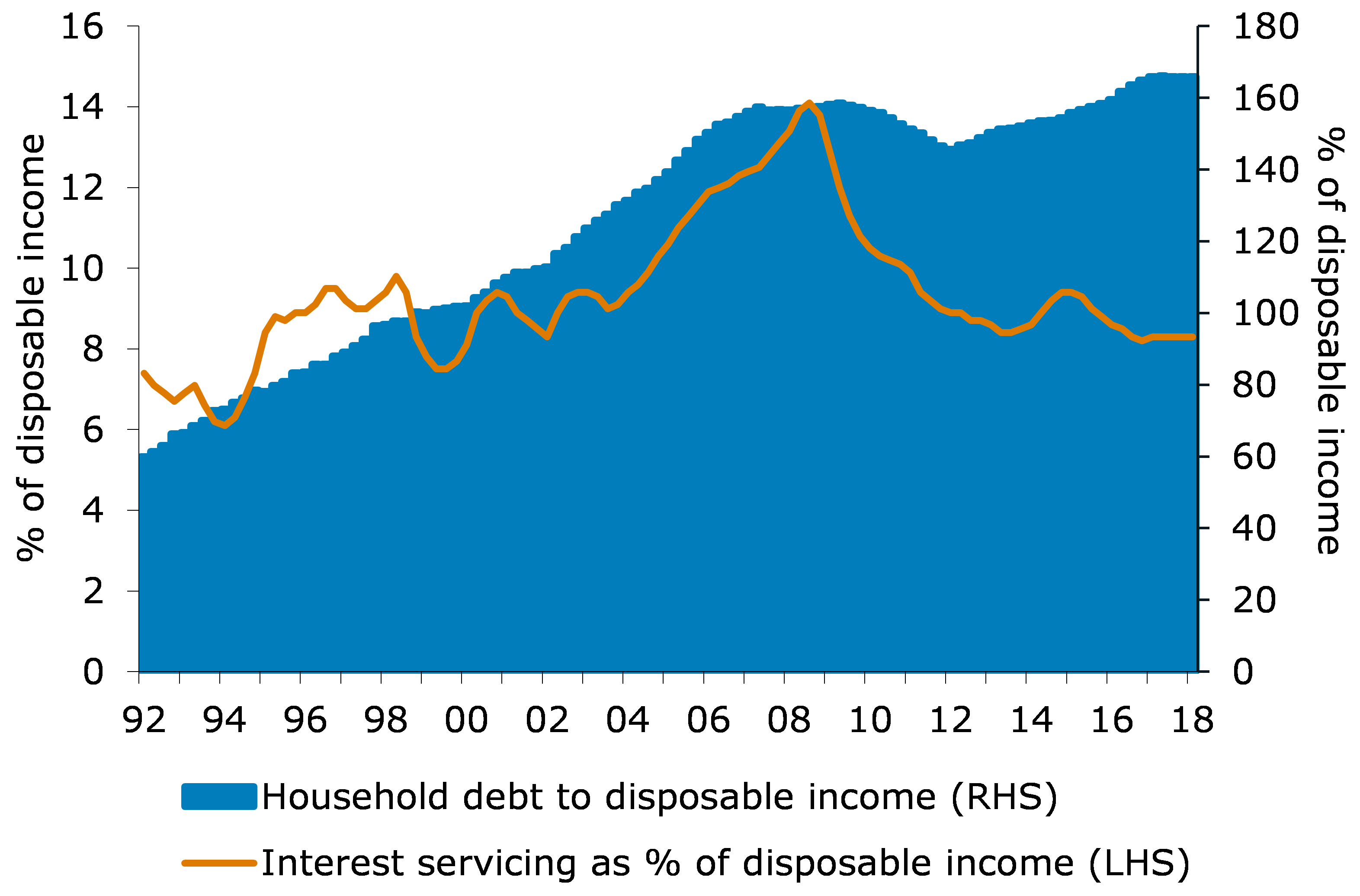

Debt levels are high. New Zealand household debt is near record highs; government debt is low by international standards, but still above fiscal targets.

Figure 6. New Zealand’s household debt and serviceability

Source: Reserve Bank, ANZ Research

And it’s not just New Zealand. Global debt is also at record highs. According to the International Institute of Finance, the global debt-to-GDP ratio is sitting at almost 320%. Following the global financial crisis, credit became cheap (very cheap), encouraging the private and public sector to take on debt, which has helped stimulate the economy.

But now balance sheets are humongous, notably within the world’s two largest economies. In the US, this is being exacerbated by expansionary fiscal policy at a time when they should be consolidating for the next rainy day. China’s situation is also one to watch. Ten years of debt-fuelled growth has seen debt increase by around 100%pts of GDP.

Chinese policymakers have sent a strong signal that the economy is on a path of deleveraging. So far so good, but there’s a long way to go and defaults are rising. Deleveraging comes at the cost of short-term growth, and that may make the effort difficult to sustain, particularly if growth slows more than anticipated. The reality is: there is only one way out that doesn’t hurt – the slow grind of growing your way out.

10. The only thing constant is change.

One thing is always true: the only thing constant is the changing nature of things. In some ways New Zealand has become less vulnerable over the past decade. The current account deficit has narrowed, our external debt has fallen, and the resilience of our financial system has improved. But in other ways we have become more vulnerable as the economy has shifted and changed.

One key area where we have become more vulnerable over time is our exposure to China. We, along with much of the world, have benefited significantly from China’s increased prosperity through solid demand for our exports and cheaper imports. Demand for some of our products has been insatiable.

But the other side of the coin is that increased exposure to China heightens our vulnerability should conditions deteriorate there, particularly as other large trading partners are also heavily exposed. China’s market is opaque and centrally controlled, meaning it is hard to keep tabs on how things there are tracking. And the economy is undergoing transition to wean the country from debt-fuelled growth.

The long-term outlook for demand from China is undoubtedly strong and supportive of our exports, especially as they move their demand towards consumption. But transitions aren’t guaranteed to be smooth and there could well be bumps in the road ahead.

Figure 7. Share of exports to China

6 Comments

Of course the debt story is one to watch , this madness will end , but I suspect it will end badly

We've borrowed from the past - fossilised sunlight as energy. A one-off draw-down.

We've borrowed from the future in ummitigated pollution, resource draw-down and debt-repayment expectations.

And even then we peak borrowers are in trouble. One has to feel sorry for future - if indeed they happen - generations.

The writers obviously haven't read my piece about relative work, and seem to parroting the econ101 line about labour - for the record, human labour is less than 1% of work done globally, and human labour is so much underwritten by fossil fuels (10-27 calories of fossil oil to deliver 1 calorie of supermarket-shelf food) that it hardly counts.

And if they're not energy-aware, they probably don't realise that productivity gains are really energy efficiencies - which follow a path of diminishing real returns - somewhat at odds with the demand for continued doublings, which is why the Productivity Commission got established (by the elite but funded socially, of course). And why it won't solve the problem.

An aging population, of course, relieves so much resource-demand on the planet and leaves so much under-utilised infrastructure (for instance no housing crisis with a population of 2 million, despite the msm refusal to

point this out) that the benefits far outweigh the downsides. It's just that economists don't count the right things, and appear to have been taught some incorrect ones. .

....and the reasons behind the top ten are nicely explained here -

https://surplusenergyeconomics.wordpress.com/2017/07/09/100-defining-ti…

Bingo!

1) and 9) So ANZ economists worry about high house prices and high debt levels.

Didn't seem to when they were lending as much money as possible to anyone who could fog a mirror during the house price boom.

In fact some would say they greatly added to the problem.

It is hard to understand why banks are potrayed as the ONLY bad guy in a debt crisis. Why do the people who take out the loans that go sour get a free pass? Seems to me they are the reckless ones, and to some extent the banks are the victims of this recklessness.

There was a time when getting a mortgage was really hard. You had to sweat and jump through hoops and it was such a relief to get your loan approved. Do we really want to go back to those days?

Seems to me everyone was a villain in the GFC. Heedless borrowers, incautious banks, but most especially an absolutely toxic government created mortgage securitisation system, that put the risk on taxpayers, so politicians could take the credit for putting more people in houses.

So why not lay off banks a bit, and spread the blame around a bit more widely.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.