There now seems an all-too-real possibility that the great all-night House Party of 2020-21 will give way to the Mother of All Mortgage Hangovers in 2022.

I fully expected mortgage interest rates to start increasing this year. But I've been blown away by how quickly they've risen.

To be clear from the outset, I don't see much chance that rising mortgage rates will get to the point that people will be forced from homes.

But I think there's an increasing chance that come probably the second quarter of next year there could be a fairly precipitous fall off in spending.

And that's going to have to be watched.

Yes, we know the economy has been stronger than any one expected. And the labour market has been as hot as a hot thing.

However, these things can swing around pretty quickly.

I remember commenting in May that the Reserve Bank had provided the 'Go' signal for financial markets to start pushing up interest rates. The RBNZ did that by something as simple as reinstating forward forecasts of the Official Cash Rate - and showing the OCR rising very meaningfully in the next three years.

The reaction was strong enough that by July I was fretting about the possibility of 'Stagflation'.

All this has happened with the RBNZ itself not having to physically do much. Remember, it had at time of writing done just one increase to the OCR, up to 0.5% from 0.25% (but with more presumably to come as of the Wednesday, November 24).

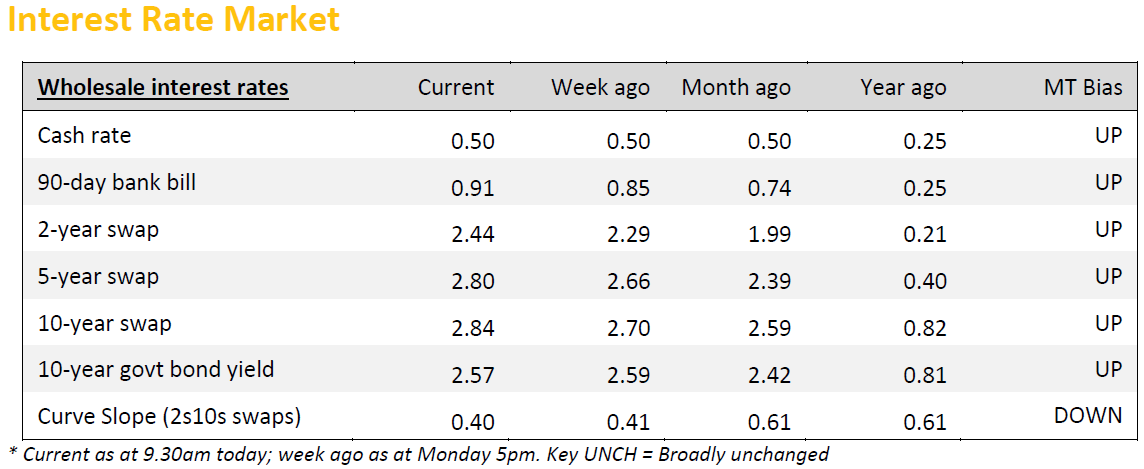

The markets though have just kept on running. With thanks to the ASB economists, here's their table on what the wholesale rates have been doing (as of Monday of this week):

My word for the above is: "Wow."

The above figures in a nutshell are why we've seen mortgage rates screaming ahead. For example the popular two-year fixed 'special' rate has risen on average from around 2.5% in the middle of the year to 4.35%.

Apart from a couple of brief (quickly reversed) blips in 2010 and 2014 we haven't had a rising interest rate environment since the mid 2000s.

The interesting thing to note about that experience was the struggle the Reserve Bank had getting traction against homeowners with fixed mortgage rates.

During 2007 the RBNZ squeezed the OCR till it was blue in the face, pushing it up to a now-seemingly-unthinkable 8.25%.

But the interesting thing to note, via the RBNZ's now-discontinued 'S8' Mortgage Lending statistics, is that less than half, under 40% in fact, of the outstanding mortgage money at that time (using September 2007 as an example) was due to reset/reprice within a year. So, effectively nothing the RBNZ was doing could 'hurt' those paying the mortgage for at least 12 months. They were impervious.

This time it's very different.

The RBNZ's current 'S33' series showing the time till next repricing shows that as at September, the latest month available, over 70% of outstanding mortgage money (nearly $230 billion worth) was due to be repriced within 12 months. In fact over a quarter of the mortgage money (a bit under $90 billion) was due for resetting within THREE months - IE before the end of the year.

This means that any changes in mortgage rates made now get considerable 'bang' for their bucks very quickly. Change of rate today, pain tomorrow - or not that many days after anyway.

It's worth looking at a couple of examples to get some feel for what we are facing.

Let's use our old favourites, the first home buyers.

Two theoretical examples, one of the resetting of a two-year fixed mortgage (30-year term) taken out in November 2019 and the other of one-year fixed mortgage (again 30-year term) taken out in November 2020.

The RBNZ's lending by borrower type figures tell us that as of November 2019 the average-sized loan for the FHBs that month was $440,500. Based on the average of new special mortgage rates then, a two year fixed rate might have been 3.44%. Using the trusty interest.co.nz mortgage calculator gives monthly payments of $1963.

Fast forward two years and facing the new emerging two-year average rate of 4.35%, and let's take the somewhat charitable view that maybe $20,000 of principal has been paid off, leaving $420,500 outstanding, and the monthly payments will go up $130 (per month) to $2093.

The situation's a bit worse for the FHB from November 2020. The average-sized mortgage by this time was $498,000. The one-year fixed rate (average) was 2.53%. Now it's about 3.65%. Using the same calculations (and taking off $10,000 for principal repayment) gives our FHB monthly payments of $1975 as of November 2020, rising to $2232 as of this month - a $257 per month increase.

Now neither of those examples are going to break the bank, or more to the point, the FHB - but the increases are of a magnitude that will certainly be felt.

As anybody knows, you pay the bill for the roof over your head before you pay anything else. And if that roof is costing more to keep over your head then other things, discretionary things, miss out.

So, the obvious areas of spending that might start to go by the wayside are things like eating out, and 'impulse' buys. And it's this sort of drop off in spending that could really start to bite in the economy.

As I said at the start of this, the situation has got to be watched very closely.

Personally, I do not have a good feeling about this at all.

72 Comments

"As anybody knows, you pay the bill for the roof over your head before you pay anything else. And if that roof is costing more to keep over your head then other things, discretionary things, miss out."

Add in $3 a litre petrol, food price increases and the cost of insurances and all you've managed to do is get yourself to and from work, eat and pay a mortgage. How much is left for anything else? Are we heading back to the days of NZ being a dreary little place that shuts down on weekends because no one has any money to spend, like in the early 90s?

Personally I miss the days when NZ was "shut for the weekend". Consumption as a national pastime is not just dreary, its dumb.

You must be fun to be around...

What's wrong with people going out and enjoying themselves in the weekends?

Do you need to buy goods to enjoy your weekend?

Shopping in NZ is so limited anyway. Every mall pretty much has the same dreary chain stores that mainly differentiate by label and little else.

I buy beer, but will now buy a home brew kit, and have garage drinks, happy days.

I know decades of brainwashing have trained people to believe shopping is a leisure pursuit (the only leisure pursuit in many cases), but there was actually life before the consumer zombie. I'm old enough to remember. :-)

"Yes, we know the economy has been stronger than any one expected".

A fair bit to do with the billions being pumped in as covid subsidies would you not agree?

These will no doubt end when we 'open'. This is when the swimming when naked scene is revealed.

Not sure where the "Stronger than expected" narrative is coming from, cannot see it myself. How can it be stronger when loads of people are not working and retail and hospo are going bust ? The current economy is totally fake but no worries, rising interest rates will get the blame for the "Crash". Christmas will arrive just in time before discretionary spending gets slashed. Still think it will be 2023 before the pain really kicks in as practically everyone's mortgage will have rolled over by then.

"Stronger than expected"

Is an indirect way of saying that some expected the NZ economy to be at the bottom of the toilet by now.

Wait.. Soon the tax man will be coming and asking for the way to pay back the billions we just got for free.. 40% tax not too far too.

Modern problems require modern solutions.

Eating out costs can't be impacted by RBNZ if you're not allowed to eat out.

Good thinking. You in cabinet?

Vaccine passports should just be pitched as a new retirement savings plan. Banned from events, shops, restaurants - the ability to save a fortune will put those people in great stead. But then Jacinda will probably seek to implement an "Un-Vax Tax" to take it off them.

I think you are joking - but that new tax is not that unrealistic - witness the proposal to levy " a work from home tax " - you are saving money by not commuting - should not really go untaxed .

In that case, I want people biking and walking to work taxed too! A home veggie garden tax and a drying clothes on the line tax could raise a bit of revenue also.

Just between you and me - Covid is losing genetic information (mutating) - naturally trying to return to its unadulterated state. It's likely to die out during the process or become harmless to humans.

I'd recommend opening borders to countries where/as this happens, as to expedite the process in NZ. Just a thought..

My Point: The savings plan might not last as long as people think.

Have you let Dr Bloomfield know your theory....?

It's not really a theory, it's just how nature was designed.

Covid-19 has probably been altered to an extent where it can't revert to its unadulterated, genomic state; as it tries to error correct it will eventually die out OR at least become harmless to humans - as Corona Viruses usually are.

This is the rout of many mutated viruses that become highly infectious. As Covid seems highly contagious yet has a low mortality rate - a highly infectious period [globally and/or nationally] followed by the dying out of Covid is a reasonable conclusion.

No I haven't spoken to Dr Bloomfield lol. It will be interesting to see if Covid dies out in vaccinated or unvaccinated countries first.

Well SARS and MERS? came and left....

I hope you a right!

It’s fading already in Japan.

Japan puzzling over sudden virus success

https://www.nzherald.co.nz/world/covid-19-coronavirus-vaccines-masks-ja…

Hey, have you heard of a thing called science? Because it doesn't look like it.

My word for the above is: "Wow."

Indeed. It's like people all of a sudden woke up and realised there is risk in the world again.

It's like people are realizing the financial stability regulator was not only asleep at the wheel, but had wedged the accelerator down with a brick - and are just opening their eyes as we go over a cliff

I spoke with a lot of investors and owners who could make it work because of 3% or under rates and only fixed for 12 months. SMH.

And if that roof is costing more to keep over your head then other things, discretionary things, miss out.

I've been saying this for years. But it's not just discretionary. It's non-discret as well. The whole developed world (NA, EU, UK, Japan) have been moving to EDLP / discounter retail models because that's what shoppers want and need. Japan has been well ahead of the pack and some of their companies / brands are out of this world in the value equation (Uniqlo, Dasio, TopValu). In the UK, a Siberian retailer has moved in promising to undercut Aldi / Lidl by up to 30%. DollarTree in the U.S. is booming. And Costco is simply one of the best retailers on the planet.

And what about the retail environment in NZ / Aus? It's looking nightmarish (Aldi's market share continues to grow). The reality is that the market scale and manuf capabilities (efficiencies) to produce EDLP goods doesn't exist. The sheeple look rooned.

Do not worry a guys.. Keep buying. What's a few hundred dollars here and there every month.

Soon you will be grin 30% appreciation in house prices and everyone on NZ will be a millionaire.

Let's buy more houses. Go mad and don't stop.

There’s another issue here that reminds me of the Sub Prime mortgage crisis in the USA. There they had Adjustable Rate Mortgages offered to all comers with no/low doc lending. As rates came off teaser levels after a year or two the cost was suffocating and the market collapsed in the 2008 GFC.

Fast forward to 2021 in New Zealand and we have teaser rate construction loans at around 2% seeing a flood of buyers into construction loans and turn key deals.. they are set a margin below the floating rate with ANZ currently at a 2.76% discount. I’m now seeing a two tier market emerge where houses in a new subdivision sell for much more than the equivalent three year old house in a neighbouring subdivision (and arguably in a better location).

What happens when the teaser rate expires and you go from 2% to 4.4% or more? Sell it for a lower price in the secondary market? To who? Everyone wants the brand new product you had to get the same sweet deal!

This literally looks like a house of cards. Speculative demand for cheap money is building houses we perhaps don’t really need given Aucklands negative net migration year to date… Have I missed something?

Ohh common why are talking sense to fellow kiwis. They do not want to listen.

My dear fellow Kiwis why would you listen to any sensible thing. just go out large and buy all the houses available. Keep buying from each other and soon we all will be millionaires. We got to help each other boom this economy and increase house prices by 30% every year.

Just do it people. Don't worry about interest rates, it's not a big deal. She will be alright..

Just pay a few millions for that neighborhood house. Let's go out and do it.

Especially now investors have been driven out of the established house market, they are flooding into the new home market to take advantaqe of the interest deductibility provisions, which is the other reason why new homes are selling for more than the 3 year old ones round the corner - there are more buyers competing for the new homes than the old. If you cant afford to sustain the negative cashflow of those new properties, then you are going to cop a complete loss of capital as well if forced to sell.

Thats true to a point, and is a good analogy. Except they had significantly looser credit, with no credit checks etc and the jump in rates was basically from 0 to 8% + and sometimes included balloon payments if they had been on interest free.

If the banks take the RBNZs lead and rates average out at 7-8% there is going to be carnage in the next 24 months as most of the markets comes of much lower fixed rates. Far to many have dunk the property seminar cool aid and borrowed way way to much. They never considered that we have just passed through a period were central banks moved heaven and earth to protect debt ponzi at all costs. This has been clearly an artificial period. Borrowers have contributed, believed the "there not making any more" and "it only goes up" seminar bs. Throw in dreams of rinsing income tax, now phasing out, and that many chose interest only to build their fabled portfolio faster most just don't realise how exposed they are about to be. As they say... one is born every minute.

Successive Governments have allowed this to build to the mess we have today. They should all be ashamed.

One very smart politician said that, house price increases is a good thing and they I won't like to see them fall.

What do you think such a statement will do in a sheeple economy where donkey follow donkey.

But yeah people just don't stop now. Let's make it another 30% increase in house prices again next year. Then i can make my millions by selling and move up greener pastures

Is that you Brock ? I hope so because I'm not sure I can take another one like him on here. LOL

Hi Carlos69,

No that's not me. But I enjoy living in your head rent free.

Yeah but you keep missing the bowl, not a great tenant.

by Averageman | 23rd Nov 21, 3:28pm

If the banks take the RBNZs lead and rates average out at 7-8%

What lead by the RBNZ ?

Only really people who have bought in the last 2 years. Most people will be sweet as in the event of a crash

"you pay the bill for the roof over your head before you pay anything else"

Spot on.

And the cheaper that roof is, the more you have to spend into the wider economy.

Given that pretty much ALL disposable income was already going into paying off said roof, spending is going to deteriorate - both in quantity and quality.

"Cleanskin" cab-sav anyone....

(NB: We should have stopped this disaster in its track in 2012, when we had it on the ropes. We didn't. But NOW is as good a time as any. If we let this cat out of the bag again - shame on everyone concerned)

I just bought a clean skin Pinot Noir (wine of Australia) from Mr 4 Square for $8 - damn fine drop it is too

You get what you paid for with Australian wine. It’s probably loaded with glyphosate.

And the cheaper that roof is, the more you have to spend into the wider economy.

Yes, the less spent on housing costs, the greater the ability to spend into the consumer economy.

But think of the banks. You don't think they can cream the same profit by selling smaller mortgages, the consequences would be horrendous.

Stop!! I'm welling up. :-(

Great article David, thanks.

There's nothing more frustrating than seeing from boomers "back in my day we paid x%, this is nothing guys"...

The banks and governments all over the world have been lowering rates now everyone is hooked on cheap debt they start to raise rates first people think they’ve got our backs. Turn out they are going to shaft you they have your kiwi pension 20% deposit they are just starting to bleed you dry people start think why would I spend 1.2 million on a 3 bedroom with stamp size lot. if you bought in last year or two you will be lucky to have anything left if you do the banks will take that through bankruptcy, you have been part of the biggest con in history driven by FOMO and greed. The banks will own huge parts of realestate and probably rent them out to previous owners at a huge cost

The issue will be more pronounced in Auckland where average mortgages are much higher than that national average.

Also remember that many FHBs are paying low equity penalties on their interest rates.

As David says, unlikely to lead to many forced sales, but it will certainly impact on discretionary spending. It will also have a big impact for demand on new builds, and if there is carnage in the construction sector and heavy job losses that could result in some forced sales.

I'm not sure he's right but I'm a confirmed DGM. One things for sure, the number of tear jerk stories of self induced hardship in the msm will rise exponentially.

Yeah.

I think there will be quite a few forced sales that come from the job loss collateral, see below.

1.5 years ago you could buy a semi decent 3 bed new townhouse in an 'OK' area of Auckland for 750K (that's what I did).

Now, an equivalent townhouse for sale today off the plans will typically be 1 mill or even higher (seeing some in places like the rougher areas of Mt Roskill at 1.1 mill).

1.5 years ago - A 600K, 30 year mortgage at 2.5% is about $550 pw. Add in $100 pw for insurances, rates etc. and circa $650 pw. Quite do-able for a 'middle-middle' income household (120-160K).

Turn to November 2021. A 850K, 30 year mortgage at 4% is about $940 pw, add in those other costs and well north of $1000 pw. That's out of reach of most 'middle-middle' income households. And that 4% will probably be 5% within 6-9 months. Plus day to day essentials like fuel, food having also been rising.

You don't need to be a rocket scientist to see that construction of townhouses will fall off a cliff as demand evaporates, especially given FHBs have been such a big part of that market.

I don't have to hand what proportion of the economy and jobs are directly or indirectly related to residential construction, must be north of 7-8%? So the jobs of 2-3% of the workforce could be in jeopardy with a house construction crash.

Architects, engineers, surveyors, planners, valuers, builders, contractors, building suppliers, tradies, landscapers, RE agents etc etc.

all valid observations ; which is why I think a way to justify not increasing the OCR by all that much will be found.

Yes I agree. Mind you, even if they only go to 1 5-1.75, as I have been predicting for some time against the majority here, that still.means retail rates of at least 4.5-5%.

But RBNZs hand might be forced anyway, if US Fed raises rates.

It seems like a lifetime ago. That's about the time I was booking flights home to New Zealand. If only I knew then what I know now.

Time to load up on them Bank shares.

House prices and sales are still ticking along quite well despite all the doom & gloom merchants and rising mortgage rates.

I don't think anyone is suggesting the boom is turning to bust... yet....

Can't speak for others, but it seems most think this will be a 2022 / 2023 'thing'

Also, FOMO is probably at play, before interest rates go any higher...

The market has plenty of inertia for sure. We’ll see a slowdown in sales volumes, an extension of days on the market, and an increase in listing numbers - all for at least 6 months before prices start to change direction. Of course the froth can go off the top at any time. Cue popcorn me thinks

The market here in Auckland has definitely changed. Where I’m looking, there are heaps more houses coming onto the market, agents are chasing sales, and are saying things like “the vendors expectations are a bit high” (ie by $100k), and also auction clearance rates are falling.

The worm has turned ... oh and there's a new version of Dune about to be released

Yeah stuff those doom and gloom merchants…. yeah who’d want house prices to come down to realistic levels…. bloody DGMs trying to ruin the party with their crazy rational empathetic logic.

/sarc

DGM headline... wont be happening in my lifetime

Yeah stuff those doom and gloomers….Just leave us speculators (sorry investors) alone to sniff our cash like feral Hannibal Lester’s in peace while society falls apart

/sarc

Hannibal Lester ... relative of wellington mayor Justin Lester per chance ??

I’d be calling it: ‘The mother of all corrections is about to happen’. And it needs to. NZ house prices are off the chart, totally insane and unsustainable for our economy. There will be pain, there will be screams, there will be tears….but there will be green shoots once we have a much needed rebalancing of our housing market.

NZ house prices were stagnant from 2008 to 2019. The last 18 months has been catch up.

Some levelling off soon perhaps.

Did you forget the boom from 2013-2017?

I think that was largely Auckland.

Green shoots for those who cashed out and could afford to sit on the sidelines.

Bad news for anyone who was born at a certain time and was simply trying to buy a family home. But that tends to be how NZ works these days.

I'll worry about it when there is a meaningful uptick in defaults on home loans. For many years we had a very easy ride, mortgages are tested to much higher rates so I don't anticipate stress until mortgage rates roughly double.

If rising rates are causing financial stress we have a serious issue with the way loans are being approved.

Great article, I'm used to property going up and interest rates dropping so will have to re-check those assumptions.

Although only another crisis in the world away from interest rates dropping back again

"But I think there's an increasing chance that come probably the second quarter of next year there could be a fairly precipitous fall off in spending"

If that proves to be accurate, then how will that affect inflation? Surely this strengthens the case for the current spike being temporary. My view throughout has been that the global disinflationary forces will prevail, though it might take a couple of years.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.