By Gareth Vaughan

The Reserve Bank ought to move faster to offload the government bonds bought during its 2020-21 quantitative easing programme to unwind the distorting effect this has on the financial system, says John McDermott.

McDermott, Executive Director of economic and policy research institute Motu is also a former Reserve Bank Assistant Governor. He was speaking in a new episode of interest.co.nz's Of Interest podcast.

He says quantitative easing (QE) via the Reserve Bank's large scale asset purchase programme has proven problematic.

"I think we'll reassess history and decide QE turns out to be a really bad idea, apart from [during] the really emergency settings."

"Under normal times central banks should not be doing this and they should be repairing the balance sheet. Because QE just seems to find itself in asset markets. It moves equity markets up, it moves house prices [up], it creates other distortions in the economy that we really don't need to have. It creates all kinds of financial stability problems. QE has proved very dangerous. Maybe we should have it for just in case, but understand the cost of using it is much, much higher than we ever anticipated," McDermott says.

QE is a monetary policy tool through which a central bank buys securities on the open market with the aim of reducing interest rates, increasing the money supply and bolstering economic activity. During 2020 and 2021 the Reserve Bank bought $53 billion worth of government and local government bonds from banks. It's now selling $5 billion worth annually to New Zealand Debt Management, the Treasury unit that manages government debt.

QE, McDermott says, gets into the financial system where it has to work through asset prices.

"So it has over inflated asset prices. It creates a distortion in terms of wealth distribution, it distorts business decisions, and it creates financial fragility in the system so everybody is over leveraged, there's too much debt in the system," says McDermott.

The exit strategy for central banks is tricky, McDermott adds, saying he hasn't seen any country do this well.

"The business model relies on keeping QE going. So I think we need to say that has not to be New Zealand's future, we don't want a distorted financial system. So it's important to reduce it before we get hooked on that really bad habit."

In the podcast he also talks about whether inflation has peaked, good and bad forward guidance from central banks, the sport of Federal Reserve watching, the need for New Zealand to have monthly Consumers Price Index inflation data, the state of the global economy, including China, the United States and Australia, and the three things he'd be watching over summer if he still worked at the Reserve Bank.

102 Comments

And the 2022 " Where were you when we needed you ? " award goes to John McDermott ... the NZ economy would be so much better balanced now , and house prices so much lower if you'd been governor of the Reserve Bank instead of Adrian Orr ...

I often wonder whether we would be better off over time having a permanent OCR of about 3.25%. We live in a time of extremes now, stock markets move around all the time by 10% on short term moves. I remember before 1984 when most stocks moved by less than 5% each year, sometimes trading for weeks at the same price. I definitely think the 'emergency' covid OCR only needed to go down to 1.5%, as we had the business and wage subsidies.

Interest rates should always be above inflation to promote production (growth), not speculation. Interest rates should have gone up in your 'emergency' (fictional, nobody died), when government created so much money that future generations will pay. Business should never operate on wage subsidies (debt), hence our inflation, that will only be tamed when interest rates rise above the true inflation rate. (12%?)

Let's vote Ardern for another term, to complete the collapse.

John McDermott would indeed be a very good Governor of the RBNZ.

I admired his contributions when he was with the RBNZ.

Some readers may recall that I wrote a number of articles starting in June 2020 where I wrote about the inflationary and distorting effects of QE that NZ (and other Western countries) were setting in place at that time place. The first of those articles can be found here. Although all were published at interest.co.nz they are most easily found as a set of nine articles here at my own website https://keithwoodford.wordpress.com/category/macroeconomics/

It frustrated me at the time that I seemed to be a lonely voice saying that we were playing the QE game far to excess. The obvious alternative was to hold the additional Treasury bonds necessary to finance the COVID-related support as bonds in the open market. But the RBNZ was obsessed with lowering interest rates.

Unfortunately there are now no policy alternatives devoid of pain to the situation that has been created. A lot of people are going to be hurt.

KeithW

Keith : you weren't a lone voice , there was a chorus of people criticizing the RB for flooding the economy with cheap cash ...

... clearly Adrian Orr cannot tell the difference between a demand side shock , which does need QE to stimulate the economy , and a supply side shock , which doesn't ...

Orr and his team are not fit for purpose , they need to go ...

GBH,

I am open to correction. But I don't recall anyone else criticising the LSAP flood until it was far too late.

I do agree that others were calling for turining off the LSAP tap much sooner than actually occurred.

Within the RBNZ it seemed to be a case of 'group think'.

Where were the independent thinkers within the RNZ team?

And there have been many of us calling for the FLP tap to be turned off much earlier.

It seems that 'Ship RBNZ' takes a long time to turn.

KeithW

Mike Hosking was daily on his NewStalk ZB show criticizing the RB for flooding the economy with cheap credit ... Prof . Robert MacCulloch was , too ... any number of commentators here at interest.co.nz knew that Orr was throwing petrol on the raging fire that was house prices in NZ ...

... Orr & Robbo overcooked the economy , plain and simple . .

GBH

The seeds were sown and the seeds then sprouted back in the middle of 2020, well before the house price inflation took off.

I would be particularly interested in any article written in 2020 on this topic by Prof MacCullough, but so far I have not found one.

As for Hosking, I never saw any reason to listen to his rabbiting on, but I suspect it was well into 2021 before he took up that particular topic to rabbit on about.

KeithW

We all know that if it had happened under Key, mr hosking would have been in awe of the strategy.

GBH you just lost all credibility touting Mike Hosking on 'National' Radio.

Central Bank Heads at the next conference.

'We printed money to avoid recession. That has caused Inflation. That may lead to reduction in demand and recession. So we will have to print money again'.

Repeat ad infinitum. Monetary policy sorted.

FYI, we ran a couple of articles from Raf Manji in March 2020.

In the first one he urged NZ not to get sucked into overseas style QE; https://www.interest.co.nz/opinion/104075/raf-manji-says-nz-shouldnt-get-sucked-overseas-style-qe-or-asset-purchasing-and

And in the second one, once the QE programme was announced, he urged the RBNZ not to make the mistake of focusing entirely on supporting the financial markets - https://www.interest.co.nz/opinion/104209/raf-manji-urges-rbnz-not-make-mistake-previous-overseas-qe-programmes-focusing

I do not recall much criticism of the LSAP at inception. As a small open trading economy we largely import monetary policy from the much larger economies we trade with. Not to do so risks terms of trade volatility, so no QE would have seen Kiwi higher. It didn't need to be that large however and the duration could have been much shorter, those are valid criticisms IMO and Orr is accountable. FLP was completely unnecessary and should have been terminated sooner.

Thanks Gareth

I have gone back and read Raf's articles.

When the RBNZ announced there first 30 billion of LSAP he said "so far so good".

And a week prior to that he had suggested there was plenty of 'headroom' for QE.

His argument was that QE needed to be directed so that it supported infrastructure and not just to support the financial markets. And indeed he suggested the RBNZ support QE by providing money to the Govt for this purpose at zero percent interest.

He seemed to be suggesting that direct funding of the Government rather than via the secondary market would some how make a fundamental difference. It would have stopped the financial institutions from clipping the ticket, but it would not have prevented the fundamental economics of inflationary effects.

KeithW

Thereafter he seemed to go quiet with no further contributions at interest.co.nz until 2022.

I definitely did not see Raf and me as standing shoulder to shoulder on these matters

KeithW

FYI, there've been several other interest.co.nz articles questioning the QE path. Some examples here;

https://www.interest.co.nz/news/108684/qe-ii

https://www.interest.co.nz/opinion/106873/as-qe-gathers-pace

Gareth

I don't see any of those articles having taken on a forecasting position in relation to the major issue with NZ's QE, which has been its effects on the money supply with this flowing through to demand-driven inflation. And that was the policy and associated commentariat void that has been a key contributor to the current situation. Issues such as the relative effects on different demographic groups were of great importance - that is the nature of distortionary policies - but those issues lie out to the side of the fundamental issue of the inevitable demand-driven inflation. Similarly, the need for the RBNZ to provide a liquidity backstop in March 2020 is not as far as I know denied by anyone, but that did not require a massive and ongoing LSAP.

KeithW

Infrastructure is the key word. Infrastructure definition- a governments handout to their pet projects.

Plenty of commenters here were critiquing the RBNZ, Keith. But we are a bunch of anonymous nerds on a non- MSM forum. You are right in so far as there was a lack of published pieces doing so, and you were certainly in the minority, sadly.

Exactly HM, in hindsight many who had the most wisdom were on interest.co and its posters, I can clearly remember the warnings when house prices started rising sharply in 2021, in response to the stimulus that was clearly going into asset speculation.

I've been commenting on the moral hazard of QE since 2008, to which the response was generally, you can't go wrong with houses. Where's my accolade? Oh that's right, no one cares about my ego.

QE stimulates the economy in the short run. Kinda like taking a pain pill. Feels good aye, but the ache just got worse.

QE is like bleeding a diesel engine with a can of engine start....theres a reason it knocks, as it fires before TDC, but if you are stuck in a boat in a shipping lane and you need to start that engine NOW its amazing what a can of the stuff can do.... I imagine that all the CBs expected covid was the end of the world. Now we have to pay the bill.

Starting fluid is about as dangerous(for the engine) as QE,(for the economy) you can start a diesel safely by squirting a little oil into the cylinder via an inlet valve, if you can find access; it increases compression safely

GBH,

I am looking at a copy of an email I sent to the RB in early Nov. In it I made a number of points including this; "Under his command, I think the RB has performed dismally. It is quite clear from the amount still sitting in the commercial banks' settlement accounts that QE was greatly overdone."

I made several other points and ended by suggesting that as he engineers a recession, he should join the ranks of the unemployed and the sooner the better. I have yet to receive a reply.

Good on you for writing in regardless, maybe spam it weekly as we all know nothing happens until it irks someone enought to drive them to do so

The problem is not so much "Softie Orr" but the new mandates given him by Stalinda and Robbingson. .

Maori and Green mandates compromised his ability to go hard..

And Orr didn't tell then No!!! I say No!!!!

The "money creation machine" of the housing bubble has popped due to the return of mortgage rates to historic norms (6.5% to 7.5%). The 40-year long Bull market was based on costs continually dropping due to technology, financialization (declining interest rates and ever-expanding credit and money supply), globalization, and expanding workforces, production and consumption. These trends have reversed. Costs are rising, technology is no longer leading growth, globalization is ebbing, workforces are shrinking and consumption is constrained by scarcities, depletion and higher costs. (CH Smith)

There is no exit strategy for QE. The options are keep printing or default.

Incorrect, there will be neither. The LSAP portfolio duration is 5y and WA yield around 1.0%, or near there. Back of the envelope then it will cost the tax payer 3.5% (OCR less WA assumption) to fund this which equals approx $2bn per annum for 5 years. It's a very very large number, but quite manageable.

Accountability though, that has been "cancelled". The opportunity cost is enormous - roads, hospitals, schools.....

Eventually the bonds will mature and the negative carry will end.

Incorrect, there will be neither.

That may be so. But remember, global debt to GDP is approx 4x. Assume a long-term interest rate of 3%. Therefore, GDP wlll need to grow at 12% to keep an even keel.

Makes you wonder where the liquidity and money are coming from.

QE as a stimulatory tool is mind bogglingly stupid. But there is nothing wrong with Yield Curve Control to set market rates where you want them, or direct financing of state infrastructure - both of which also involve some Crown purchase / ownership of bonds.

In ten years time, we will wonder why we ever placed any store in medieval monetarism. It is holding us back and is completely ill-suited to the challenges we face

Letting a handful of suits determine "market" rates is mind boggingly stupid. A return to a system where no central party controls money is just what is needed. Separate money and state.

Makes you wonder why they ever moved away from that scenario.

Actually if you did some reading you'd know.

I recommend The Creature from Jekyll Island

It's been a while.

There were some pretty fundamental issues with decentralised banking.

JRSNZ,

You're joking right? Griffin was a conspiracy theorist par excellence. He was unhinged.

'Did some reading' 🤣

People seem to only learn about the creation of the central banks onwards, and not much about the conditions leading up to that.

I'd recommend 'Debt: the first 5000' years by David Graeber with a side helping of Keynes work on financing the war (which contains the recipe for financing climate change adaptation etc)

Batshot crazy idea!

QE as a stimulatory tool is mind bogglingly stupid. But there is nothing wrong with Yield Curve Control to set market rates where you want them, or direct financing of state infrastructure - both of which also involve some Crown purchase / ownership of bonds.

Hmmmm. Japan has been able to directly finance infrastructure but they're essentially a creditor nation with a massive industrial capacity. Not sure that NZ is capable of doing similar. How would this work in the case of NZ? No financial and / or monetary stability risks?

As opposed to 1940s NZ when we directly financed building thousands of houses, or later when we built hydro?!?

But, I agree that monetary sovereignty is easier to maintain without a current account deficit. But, getting to balanced trade and energy security would require an actual strategy.

Stimulating the economy by funding big projects or even just paying people to dig holes seems a better approach than reducing interest rates so that money can be fast tracked into asset prices.

Maybe a better recipe for the next pandemic would be to let all the cafes and restaurants go under, make sure there is basic food available for everyone while they are locked down, and ensure banks don't kick people out of their houses by legislating a interest free payment holiday. Then in the past year plenty of workers would have been available to pick fruit, build tracks, roads etc. It would have been painful but at least we wouldn't have the hangover we currently face

What pandemic? Perhaps a pandemic of the Pfizer gene therapy experiment. We just don't know; the clinical trial is still looming...

Oh FFS, get real.

Sadly we could only build said houses as we had ample native forests to rip out and use for local resources, now we are not in any position to do so again with the same quality. Try finding enough of the old hardwood to build a modern sized home. Currently we have to focus on core matters to NZ being energy security, infrastructure, education, healthcare.

QE is a great stimulatory tool if you have the world's reserve currency and want to export your inflation. I don't think NZ fits that description.

Yes, having the world's reserve currency changes all of the rules.

It makes many things possible

KeithW

The West and the World is paying the price for the Monetary Policy dictated by the US.

It is a tool designed to keep the Rich richer.

Totally agree we cannot carry on in NZ with a distorted financial system

Looks like the answer is cold turkey and a 12 step program.

John is one of our great economic scholars and is a true gentleman - another great Interview Gareth!

Robbo is on record as saying that the jury is out on whether or not QE is a driver of inequality.

Nobody raised an eyebrow.

... no one bats an eyelid anymore when Robbo bloviates about finances ... only the lamingtons look shocked when he walks into the room ...

Lamington #1: We're on the guest list!

Lamington #2: That's the menu.....

There should be no doubt that QE and inflation help those who have a combination of property plus loans.

There are two problems:

1) It is a zero sum game from the outset where there have to be losers to an equivalent extent

2) It is distorting in terms of resource allocation and hence long term economic efficiency.

KeithW

Not sure why John McDermott has to get in the snide comment re gold and the ol' rat poison. If people started to actually think about sound money principles, we might be better off in the long run.

I guess if we are talking monetary policy, you want money more liquid not less.

Depends. As I mentioned earlier, global debt to GDP is already 4x. You start to challenge economic fundamentals. Or more importantly, your fiat money starts to become worthless.

So how does making wealth less liquid help that then?

It's fairly clear the powers that be want money used, not stored.

It's fairly clear the powers that be want money used, not stored.

The ruling elite has no problem with banks creating credit (money) and you spending it as long as it fits within their agenda.

This is also why CBDCs are useful for them as well. They can incentivize people to spend.

Doesn't stop the value of fiat deteriorating. It's all about trade offs.

You didn't explain why making money less liquid is superior. They moved away from the gold standard for a reason, using a finite amount of crypto would be even worse.

Did the banks actually need this money or have they asked for 'cheap' money ?

ANZ senior economist Miles Workman says banks’ “treasury” teams work constantly to source the money each bank needs in order to make loans.

The sources of bank money include households putting money in savings and other deposits at banks, but also banks borrowing from large investors, like pension funds, on international “wholesale” money markets.

The bank funding backing floating rate loans is short-term funding which is very sensitive to rises in the OCR, says Workman

https://www.stuff.co.nz/business/money/130570693/why-dont-fixed-term-in…

So looks like the govt/reserve bank wanted some kind of marketing headline .. so came up with LSAP ...

Banks don't take deposits and they never lend money. They are in the business of purchasing securities. When one gets a bank loan, the loan contract is a promissory note. The bank purchases that contract from the borrower. Now the bank owes the borrower money and it creates a record of the money it owes, which we call deposits - source.

But thats only according to Werner and co ; but it makes sense to me ..

But here bankers are saying we have enough deposits to fund . I think if money creation for security-purchase is right , what our bankers tell here is that mortgage create deposits and they stay within the banking system. Hence they can say that they have enough deposits to fund mortgages ..

Chicken egg problem ?

According to Werner indeed. The same economist who understands why credit creation for productive purposes trumps credit creation for asset speculation and living beyond your means.

Great podcast, thanks for sharing Gareth

Great interview. Should be the Gov in 2023. Path of least regrets.

I guess that when buying Kiwibonds from the debt management office we are helping dispose of this horrible money printing: in a very very small way.

These purchases could grow by the way when the govt brings in the deposit guarantee because term deposit rates will most probably drop down to that of Kiwibonds. And the advantage with Kiwibonds over deposit guaranteed TDs, is that there is no additional OBR haircut lurking in the background.

"when the govt brings in the deposit guarantee because term deposit rates will most probably drop down to that of Kiwibonds." Would the Kiwibonds not be adjusted down as well to keep a relative differential? It think it may skew funds toward kiwibond and starve the banks or the banks would need a suffcient margin above kiwibond to attract funds. Will have to wait and see.

yes will be interesting, the funds will always look to bonds when they see an opportunity for an increase in face value as well as the coupon rate.

John talks about how rosy things in Aussie are, yet the former Treasury adviser and Chief Economist at ANZ is talking DGM and bailouts:

"And of course, the burden will have to be shared between not just the individuals involved, but also the shareholders of banks – they'll take a hit, and potentially the taxpayer, depending on how severe the problem becomes."

Kind of a stark difference.

https://www.abc.net.au/news/2022-12-17/housing-apra-rba-forced-sales/10…

Very Fragile if Hogan is talking like this publicly

Bank of Japan 'stunned' the markets w/major shakeup to YCC. What it all means.

Let the clown-show roll on. Bank of Japan votes to widen the trading band for yield curve "control" over the JGB 10s. I'll go through what YCC is, where it came from, what's going on with it now, most importantly what it means for all of us unsure about 2022 heading into 2023.

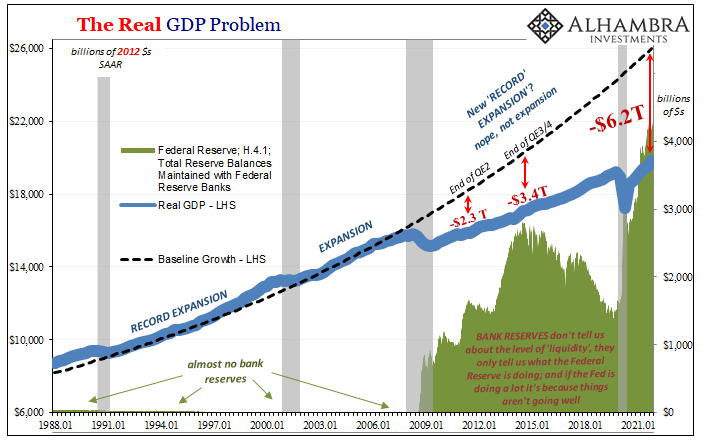

A recent Bloomberg article described central bank easing with the phrase “pumpingd money into the economy.” That’s a misconception. Monetary easing is actually an asset swap. The public was holding savings in one form, and now it holds it in another. The Fed buys Treasury securities from the public, and replaces them with currency and bank reserveds (base money) that someone has to hold, at every point in time, until the Fed sells its bonds and retires the cash. All monetary policy does is change the mix of government obligations held by the public. Only fiscal policy – specifically deficit spending – changes the total amount of those obligations. - courtesy of Hussman

There was prior evidence elsewhere that LSAP (QE) failed to generate sustained economic growth - it should have been noted and acted upon.

"Investors" have persistently over capitalised the rising discounted present value of cash flows associated with assets, financed by bank credit as interest rates fell.

Policy makers sometimes flatter themselves with the idea that holding interest rates at untenably low levels makes it cheaper for borrowers to obtain funds. Unfortunately, it does so only by transferring income from people who are trying to save for the future. Replacing Treasury securities with base money may make savings more “liquid,” but it doesn’t suddenly make people abandon their retirement plans in favor of consuming today. Low rates also don’t magically create productive investment opportunities.

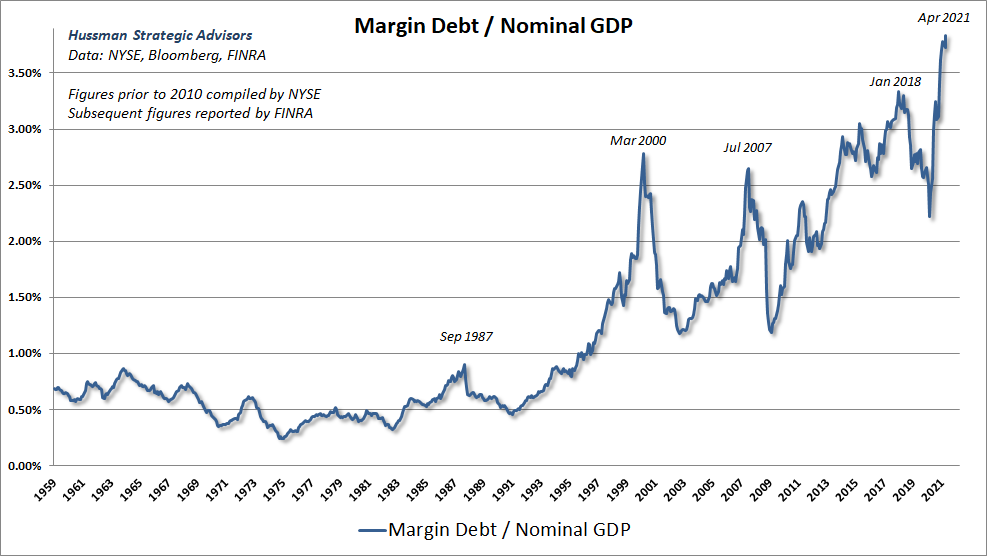

What economic activities suddenly become viable at zero interest rates that were somehow not viable before? Only projects so unproductive that any positive hurdle rate would sink them. The main activities that are encouraged by zero interest rates are activities where interest is the primary cost of doing business: leveraged real estate transactions; “carry trades” that employ enormous amounts of leverage to profit from small yield differences; and speculation on margin. Presently, margin debt as a percentage of GDP is at a historic extreme. https://www.hussmanfunds.com/comment/mc210614/

The idea that “low interest rates justify high stock valuations” is really a statement that “low interest rates justify low expected stock returns as well.” Those high stock valuations are still associated with low prospective future stock market returns.

Worse, the notion that “low interest rates justify high stock valuations” assumes that the growth rate of future cash flows is held constant, at historically normal levels. If, as we presently observe, interest rates are low because growth rates are low, no valuation premium is “justified” by low interest rates at all.

Presently, the combination of record low interest rates and record high stock market valuations does nothing but add insult to injury.

...the iron law of investing is that a security is nothing but a claim on a future stream of cash flows. Valuation is a crucial determinant of long-term returns. The higher the price an investor pays for those cash flows today, the lower the long-term rate of return earned on the investment.. Hussman

The corollary is also true. The lower the long-term rate of return demanded by investors, the higher the price moves today. So clearly, changes in investors' attitudes toward risk will strongly affect short-term returns. If investors become more willing to take market risk, it is equivalent to saying that they are demanding a smaller risk premium on stocks (that is, a lower long-term rate of return). Prices rise as a result. Now, the fact that current stock prices are higher also implies that future long-term returns will be lower, but that's part of the deal. Courtesy of Hussman Funds

{kind=link}

{kind=link}

But Audaxes I was told to save for retirement, and I worked so hard! Hard work doesn't pay.

Completely out of context but with no 4pm update its hard to put this elsewhere. $1 reserve Auction on the shore sells for $480,000. It has an RV of $840,000.

https://www.stuff.co.nz/life-style/homed/real-estate/130828755/how-scar…

They appear to have got 175k more than they paid for it 14 years ago. I can't help feeling they would have got more by negotiation however it seemed to be an urgent sale.

last sale 2014 it was a loss

I didn't see a sale for 2014.

ok homes saying a sale in 2014 for 540k

QV and TradeMe though?

Stink. If they were FHBs that would have really sucked. I imagine when they bought it the damage was not known. Rotten piles? It wasn't leaker age.

Yeah shitty do ups are worth land value in this sort of market.

I know the market isn't great but I doubt we are at that level yet. Either the $1 reserve really backfired, or the house was more of a tear-down than a do-up.

16 registered bidders 5 active, on the day it sold to the person who put there best foot forward!

- hard to get finance for purchase and construction, as an auction has to be a cash/approved buyer

- possibly hard to insure (making it almost impossible to finance)

- expensive to do and if done officially, could take a year or more

- probably worth 30% less once finished than the cost of buying and doing up

The property is a punt and the amount of people willing to take one at the moment is pretty narrow, and occupied by bargain hunters. Actually probably a good time to buy if a Reno is your idea of a good time.

Lol, the agents sales pitch:

This sale isn't going to set any records but the numbers will work at some level. If you think your game get in touch with Alex or Ammy to arrange a time to come and do your due diligence.

The central problem I have with the central bank groupthink is the bonkers belief that price control will work if only it is they who do it.

Price control of individual items causes the pricing signalling feedback mechanism to malfunction.

How do they manage the Orwellian double-think that price control of interest rates will not bugger up investment decisions and make the country poorer, more divided and more fragile if they do it?

Is it self delusion in order to be a loyal tribal member? Do they really believe they are so special that that which has repeatedly failed will work when they do it?

They must really practise believing in at least four impossible things before breakfast.

Definitely a kind of weird master-of-the-universe position with a fair bit of imposter syndrome IMO

AFR -

Dec 21, 2022 – 3.52pm

James Hardie Industries is cutting hundreds of jobs globally and making workers redundant before Christmas as the building materials maker struggles with what it claims is “a perfect storm” of falling demand and soaring costs.

JHI moved its headquarters twice in its recent history - from Australia to Netherlands to Ireland. No surprises that this corporation has no loyalty to anyone but its investors and would rather throw workers out on the street lit with Christmas decorations than give a dime less to its shareholders.

Central bank have screwed up and are being paid for it.

What a job !

No accountability.

Isn't the issue where the easing goes - if it was used to fund infrastructure builds (hospitals, schools, rail, public transport) and support people on lower incomes (including via long term low interest mortgages for first homes) wouldn't the result be better than just providing welfare for the FIRE sector?

The whole Covid (Big Pharma enrichment) scam was providing welfare (government debt) for the FIRE sector (non-productive society) and who propped them up. The 'essential workers'. Why in the hell did they call them essential?

AR5886

If infrastraucture projects are worthwhile then they should be capable of being funded through a fiscal allocation linked where necessary to funding in the market. If the project is not viable when funded that way then it should not be funded. QE for infrastructure lets the politicians loose in the candy shop. But the lunch of candy does not come free. Someone somewhere has to pay for it.

KeithW

The problem sometimes with infrastructure is the benefits may not be directly monetisable.

Take public transport, if it's running at an operating loss, but you're saving money not having to build and maintain more roads, and have labour wasting countless hours and money a week sitting in traffic, is that worth funding with magic money? Because the private sector won't be interested.

The money from QE doesn't go anywhere if it only involves buying back government bonds and is then only returning reserves back to the banks which are their own assets. Banks can choose to hold their government currency as central bank reserves or they can buy government bonds with them and not much else.

The government is not financially constrained in its spending as it is the currency issuer and every dollar that it spends is a new dollar and which is then paid into the reserve accounts of the banks and this is how they acquired their reserves initially.

Economist L.Randall Wray explains here, https://youtu.be/E5JTn7GS4oA

It’s pretty clear that central bank monetary policy doesn’t work irrespective of QE.

Its the low interest rates that blow the asset bubbles, QE just provides a blowoff on top.

We need a lower limit on the OCR and to use other tools such as fiscal policy instead.

Comprehensive capital taxes are also required to reduce the profitability of asset bubbles.

A former Assistant Governor of the Reserve Bank who seems not to understand QE. Returning reserves back to the banks which the governments bond sales had reduced will not lead to asset price inflation as banks are unable to lend out these reserves and QE only has a very limited effect on interest rates.

https://www.hks.harvard.edu/sites/default/files/centers/mrcbg/programs/…

It might be time we discussed whether the current monetary system is fit for purpose. When did you last hear any politician talking about monetary reform?

But, but, but, our childish politicians do not have a clue about money. To them it is something that is just there for them to spend. Same for the sheltered teenager bureaucrats, they just go to work and money appears in their bank accounts by magic. No feedback mechanisms whereby they go broke if they make poor choices, but instead bad choices that conform to current groupthink get rewarded.

Central bank studies - the most recent being form the Reserve Bank of Australia - suggest LSAP programs reduced bond yield by about 0.30%. The RBNZ is showing a loss of $9 billion + on its holdings, so that means each 0.01% decline in yields cost NZ taxpayers $300 million. That's a lot of hip operations......

Was it worth it? More to the point, was it needed? Answer: No.

The New Zealand bond market is a minnow in global terms and our yields would have followed other countries down regardless of LSAP (as they always do follow global trends). We could have just ridden on the backs of the Fed, ECB, BOE, RBA etc and saved ourselves $9 billion.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.