Summary of key points: -

- More aggressive tightening of monetary policy from the Fed

- Change of monetary policy stance from the RBA to the rescue of the AUD?

- Kiwi also lower due to a more general loss of confidence

- True sources of NZ inflation not well understood by our politicians

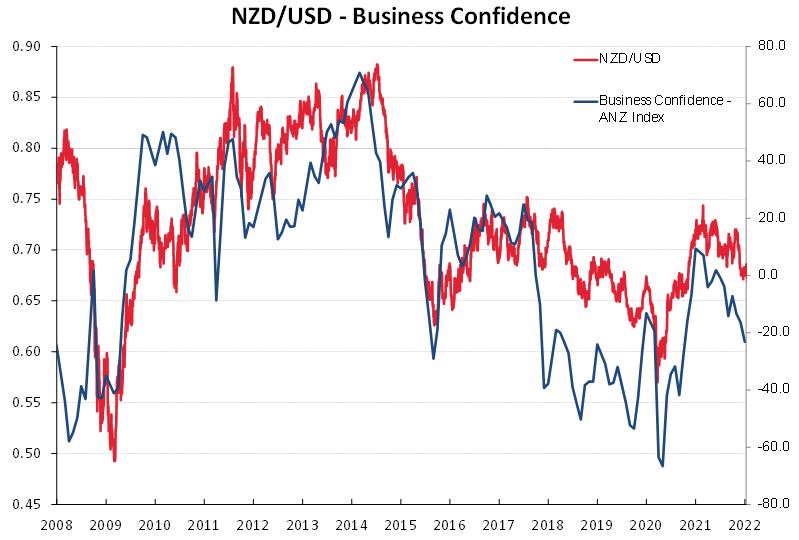

The pandemic boom is starting to go bust as the US Federal Reserve act more aggressively against high inflation and that has resulted in the NZ dollar being whip-lashed down to 15 month lows against the US dollar at 0.6540.

The consumption and investment binge has ended abruptly as the extraordinary fiscal and monetary stimulus measures implemented across all western economies over the last two years is hastily removed from the table.

The Kiwi dollar (along with the Aussie dollar) was smashed down by 3.0% in the FX markets over this last week as the US dollar strengthened sharply against all currencies due the Fed confirming an earlier and more stringent monetary tightening policy stance than generally expected. In addition, the US economy expanding at a more robust pace of 6.90% annualised in the December 2021 quarter. It was a double-whammy negative impact on the Kiwi dollar as selling intensified once the previous support level of 0.6700 was decisively broken.

Just where the next support levels will be for the Kiwi dollar to attract some buying interest is difficult to judge. There is no question that both the NZD and AUD (in having the label and reputation as “risk currencies”), suffer more than most under speculative selling attacks in the FX markets when equity markets tank.

The extreme volatility in equity markets from the Fed’s tougher stance has prompted hedge funds to add to their short-sold NZD and AUD speculative positions.

The long-standing view of this column that the widely expected US interest rate increases in 2022 and 2023 were already fully priced-in to the USD exchange rate value at $1.1300 against the Euro has proven to be wide of the mark as the USD has posted further gains to $1.1150. It was expected that the USD would start to weaken in 2022 when the actual US interest rate hikes started to occur as the US currency had already strengthened in anticipation of the monetary policy change (a buy the rumour, sell the fact situation).

However, the Fed’s endorsement last week of earlier and more rapid interest rate hikes was over and above what the FX markets had already baked in. To be fair, the USD gains of 1.3% over the week to $1.1150 were a lot smaller than the 3.0% depreciation in the NZD/USD rate from 0.6750 to 0.6540. The selloff in equities contributed to the additional NZD and AUD selling.

Change of monetary policy stance from the RBA to the rescue of the AUD?

Similar to the “over-cooked” call that was made in March 2021 when the NZ dollar spiked sharply higher to 0.7400, it does feel that this latest sell-off in the Kiwi dollar is also “too far, too fast” and some form of rebound back up has to be expected. A stabilisation in US equity markets would assist that to happen over coming weeks. Whilst the view and outlook of this column was that the NZD/USD rate would hold above the previous support levels of 0.6700/0.6800 and move higher in 2022 on a weaker US dollar, the old FX market adage that the Kiwi dollar always falls two cents further than what you think when it is on a downward tear has proven to be accurate once again.

Whilst the NZD/USD movements over this past 12 months have been dominated by the US dollar side of the equation, there must come a point when global investors and traders will consider the NZ dollar seriously undervalued at 0.6540 and the AUD seriously undervalued at 0.7000 against the USD on the respective local economic fundamentals. Australia is running massive Balance of Payments Current Account surpluses (4% of their GDP) from higher export commodity prices and a lower AUD/USD exchange rate value. New Zealand’s local NZD positives include record high dairy export commodity prices and sharply higher interest rates.

It will require a significant event to act as a catalyst to change the FX market speculative positioning from being heavily short-sold the AUD to aggressively buying it. The Reserve Bank of Australia’s (“RBA”) statement on monetary policy on Tuesday 1st February is likely to be that event as they are expected to signal (perhaps only a “hint”) at much earlier increases in Australian interest rates than the previous stance of no increases until 2024.

It would be highly unusual for the RBA to adopt a continuing monetary policy stance the is polar opposite of what the US, UK, Canada and New Zealand central banks have currently embarked upon. A re-rating of the AUD value higher is expected from the RBA relenting on their previous stance.

Kiwi also lower due to a more general loss of confidence

Perhaps something has been missed over recent months in respect to how the rest of the world now view New Zealand in respect to our handing of the Covid pandemic and the related impacts on the economy. The depreciation in the NZ dollar against the AUD from 0.9700 to 0.9350 since October tells us that the NZD has under-performed the AUD against the USD.

Global FX investors and traders have clearly lost more confidence in the NZ economy.

We see this reflected in the poor performance of the NZ sharemarket over recent months as international investors have sold out of the market. We also see it in our plummeting business confidence surveys. Why would an international investor continue to invest funds in the New Zealand market/economy when they observe that the local business community have much less confidence in themselves and are full of uncertainty?

The hesitancy and uncertainty stems from the Government’s lack of forward risk management and being poorly prepared for the Delta Covid variant last year and also for the Omicron Covid variant currently spreading across New Zealand. The political leaders and Government bureaucrats have only just now returned from their summer holidays and are making up more regulations/restrictions on the hoof! Add on the universal condemnation of the New Zealand Government’s refusal to allow its own citizens to return home easily, it is plain to see why we are not on anyone’s investment radar anymore.

Offshore Kiwis can return home; however they have to buy the equivalent of a winning ticket in a pub chook raffle to get in. A prioritised points system for expanded MIQ facilities with expat Kiwi’s and immigrant ICU nurses at the top of the list would have been the solution.

True sources of NZ inflation not well understood by our politicians

The depreciation of the NZD/USD exchange rate to 0.6540 has significantly loosened monetary conditions in the economy, precisely at a time when the RBNZ has commenced its monetary tightening action. The lower currency value adds to the already high tradable inflation rate, so a more stringent tightening tone should be expected in the next RBNZ statement on 23 February. The underlying sources and cause of New Zealand’s high 5.90% inflation rate has been previously well canvassed in this column. Core and permanent domestic (non-tradable) inflation from local government rates increasing on average 4.5% every year for 10 years and house building costs also increasing on average by the same amount every year for 10 years (refer to the 12 December 2021 column) are the real cause.

Until recently, low tradable inflation from offshore (oil, reducing prices of Chinese manufactured consumer goods and commodity prices) disguised and covered over this inflation problem for many years. Consistently falling communications costs acted in the same way.

Therefore, it was galling and a bit rich to hear from both our Prime Minister and Minister of Finance last week that the reason for the higher inflation was all due to offshore factors and out of our control. It is all just a load of codswallop!

Successive NZ governments have failed most Kiwi households by squeezing their finances with constant cost increases from poor policy settings and regulations, resulting in non-tradable inflation well above 3.00% every year for the last decade (i.e. restrictions on the supply of land for house building). What is even more disturbing is that the RBNZ never identify and address these true sources of inflation that every household and business is bearing the brunt of. The inflation will not be fixed by adjusting interest rates, it requires reducing the cost of regulation.

Local USD exporters who have already hedged forward to maximums of policy limits at higher exchange rate levels above the current market spot rate (resulting in some regret factor and opportunity cost) are advised to continue to replace maturing hedges with new hedges at the lower spot entry levels. In this manner, the weighted-average hedged rate in the hedgebook is lowered.

Exporters who find themselves with reduced bank FX dealing limit availability (due to existing hedge contracts being in marked-to-market loss positions and thus reducing bank credit), but they wish to protect future company profitability, should consider buying low premium cost NZD call options with strike rates up at 0.6700 and 0.6800.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

11 Comments

Excellent article Roger! Bang on the money, I’d say.

Therefore, it was galling and a bit rich to hear from both our Prime Minister and Minister of Finance last week that the reason for the higher inflation was all due to offshore factors and out of our control. It is all just a load of codswallop!

When things are going badly it is always beyond our control. When things are going well it's NZ's astute financial management. You've got to laugh at our politicians.

Wow that's making things even worse for inflation on petrol and imported goods. Orr makes his announcement between the RBA announcement tomorrow and the FED one in March, talk about being trapped between a rock and a hard place. Even I'm going to get the popcorn out.

Simply, this will force the OCR in NZ to go even higher than what already expected.

Expect an OCR peak at least at 4% if no higher, and mortgage rates at almost 7%. The music has not stopped yet, but it is slowing down - and significantly so. The impact on the NZ housing Ponzi is going to be brutal.

The RBNZ will be forced to keep rising the OCR until something breaks, and what is going to break this time is definitely the NZ housing market.

I would have thought given the risks outlined in the second half of your article that global investors and traders would see substantial downsides in the value of the nz dollar, and subsequently have not devalued it beyond reason. In fact it should have a further devaluation against both the us dollar and Australian dollar .

Everyone talking about doom and gloom. But here is the NZ hosting market selling at 1mn+ per house.

Wages in the range of 60+ k / year.

Where is all the money coming from? Are we just positively optimistic that someone else will pay our big mortgages or we seriously have a lot money hidden somewhere which we will be using to pay these off?

Some will be paying cash. More wont be. Those borrowing will have planned on interest only at the lowest rates in history continuing for ever.

Good luck with that plan.

60k per couple more like it. 🙄

Let's see if the NZD will reach a unrevivable record low.

They're not so much leaders, more like bleeders.

The fact that we had some healthy government debt levels before the pandemic meant we could afford to spend a bit. The market is brutally honest in that it reminds us that there is no free lunch. Lockdowns are expensive as are picking some of the most stringent off the shelf measures. You can say no to mining, no to foreigners buying, no to supporting farmers, no to immigrants and in the end the NZD starts to look dusty. As always most NZers pick up the tab but don't always connect the dots. At first we can blame the, supermarkets, building suppliers, petrol suppliers, energy companies and then someone can start talking about price controls. Which usually only leads to less suppliers.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.