- Crunch time not far away for the Fed, US interest rates and the US dollar

- FX market “reef fish” punish the Aussie dollar

Crunch time not far away for the Fed, US interest rates and the US dollar

A number of New Zealand and Australian banks are forecasting a stronger US dollar from current levels (102.50 on the USD Index) over the next six to twelve months, therefore they translate that into a lower NZD/USD exchange rate forecast below 0.6000.

Their currency outlook reports on the NZD/USD exchange rate are generally 90% a discussion on the merits of the NZ economy and 10% on what the US dollar is likely to do on global FX reports. They cite New Zealand’s current/impending economic recession, the Current A/c deficit blow-out and falling export commodity prices as good reasons for a lower NZ dollar value. If they do briefly mention the US dollar side of the currency pair in their reports, it goes along the lines of the paradigm that “the USD always appreciates when the global economy falls into recession” and that is where they believe we are headed.

Regular readers of this report will readily acknowledge that our insights and interpretation on the outlook for the NZD/USD exchange rate are dominated by the direction of the US dollar in global currency markets. The second most important influence is the direction of the AUD/USD rate, thirdly Chinese economic developments and lastly New Zealand factors. Although, to be fair, the NZD/USD rate was pushed down two cents on its own in May (independent of the first three forces) when the RBNZ surprised the markets with an unnecessary unequivocal stance that our interest rates will be increased no further.

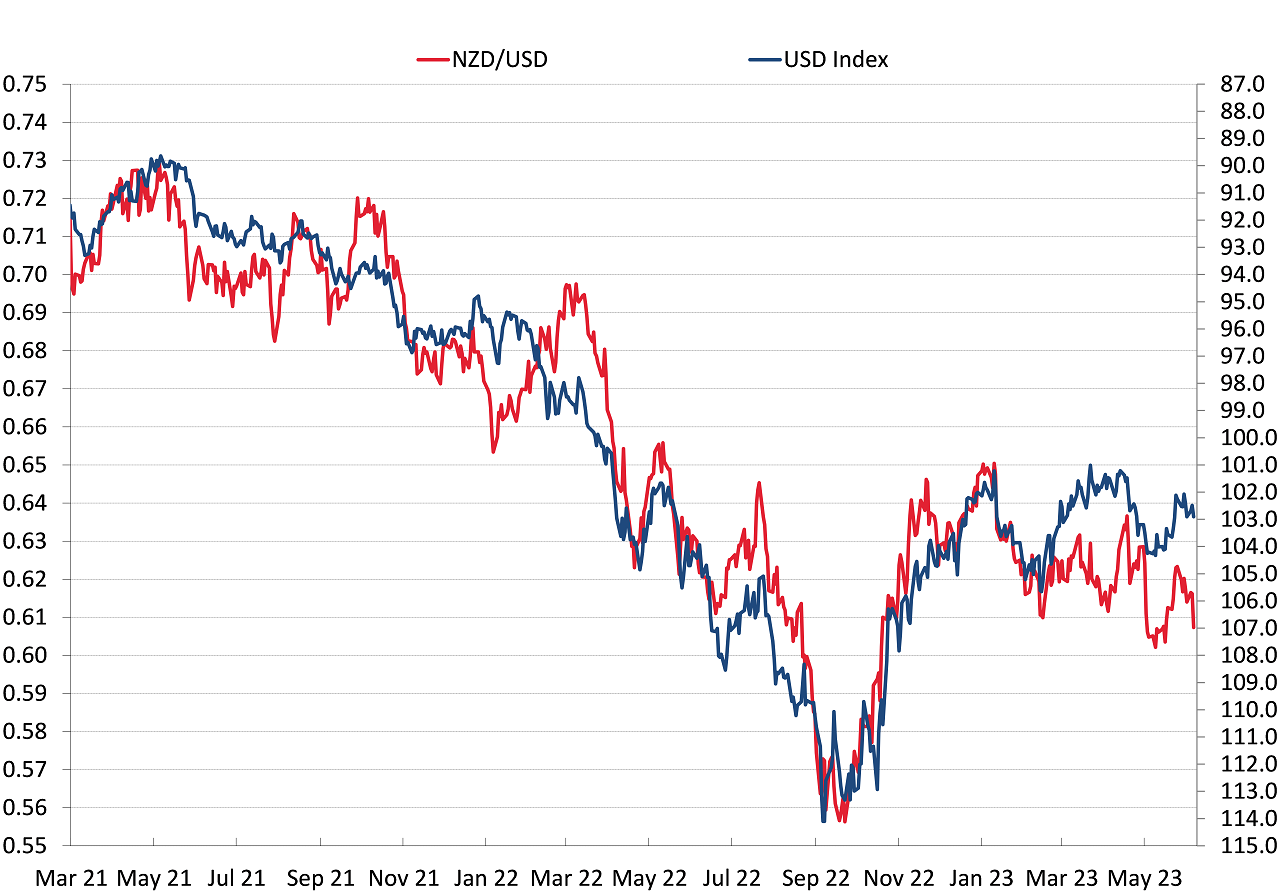

As the chart below confirms, the NZD/USD rate has been fundamentally driven by the USD Index over the last two years. However, the recent divergence of the Kiwi dollar under-performing the USD Index has ben caused by a loss of confidence in the Australian dollar (which the NZD follows) due to an inconsistent monetary policy stance by the Reserve Bank of Australia.

The USD appreciated from 90 in mid-2021 to 114 by October 2022 on the US Fed hiking their interest rates. Late last year, the FX markets started to price-in a weakening US dollar as they anticipated that the Fed would end the interest rate increases by mid-2023. The USD Index plunged in value from 114 to the 101 area by late January 2023. Over the five months since January, the FX markets seem undecided as to whether the US dollar will continue to depreciate or not. We have seen the USD Index oscillate between 101 and 105 with two pushes higher when stronger labour markets data convinces the markets that the Fed has more to do with further interest rate hikes. Our view is that the US labour market will now start to soften, and US inflation will continue to decline at its rapid rate, and the USD depreciation will recommence. The Fed may well do one more 0.25% increase later this month (26th), however that change is already priced-in by the FX markets. The PCE inflation measure for the month of May released on Friday 30th June was below prior forecasts and inflation will continue to reduce over coming months as the rents/shelter component finally decreases on their 12-month lag. US CPI inflation data on Wednesday 12th July for June will see the annual headline inflation rate drop from 4.00% to 3.60%.

The forex markets will recommence selling the US dollar as they price ahead the last Fed tightening action and factor-in that the next move in US interest rates after that will be downwards in 2024. In addition, the probability or risk of a bad global recession is diminishing every day, so the expected USD strength due to a recession, from some quarters, will fail to materialise.

Next Friday night’s US Non-Farm Payroll jobs numbers for the month of June stand as a pivotal decision/crunch point for the markets and the Fed. An increase in employment well below the 250,000-consensus forecast and a continuation of the lower hourly earnings (wages) will send the USD lower and reduce the market bets on further Fed rate hikes.

In conclusion, we continue to hold the view that the dominant USD influence over the NZD/USD exchange rate will push it to the high 0.6000’s over coming months, with the USD Index depreciating to the 95 area from its current 102.50 level.

FX market “reef fish” punish the Aussie dollar

A former New Zealand Prime Minister, the late David Lange, once famously described the FX markets as “reef fish”, as they all blindly follow each other one way and then they all abruptly reverse to the other direction for no apparent reason.

The reaction of the FX markets to Australia’s monthly CPI inflation figure for May released last Wednesday followed that “reef fish” pattern of behaviour. The headline result was a surprisingly large decrease in the annual inflation rate from 6.80% to 5.60% (prior consensus forecasts were for a drop to 6.20%). The Aussie dollar was immediately sold down once cent from 0.6700 to 0.6600 against the USD. However, looking behind the headlines, the detail revealed that the annual core inflation rate (excluding volatile food and energy prices) was largely unchanged and remains elevated at 6.40% (down a tad from 6.50% in April). As we have seen in New Zealand, a sharp drop in fuel prices can surprise the forecasters and deliver a lower-than-expected inflation outcome. However, the underlying inflationary pressure from wage increases in Australia suggests that the Reserve Bank of Australia (“RBA”) still have more to do with interest rate increases.

The local Aussie interest rate markets are now 50/50 on whether the RBA will increase rates by another 0.25% to 4.35% at the next meeting this Tuesday 4th July. The Aussie dollar lost two cents the previous week from 0.6900 down to 0.6700 when the minutes of the RBA 6th June meeting revealed that the decision to increase interest rates to 4.10% had been a much closer margin than originally reported in the RBA statement.

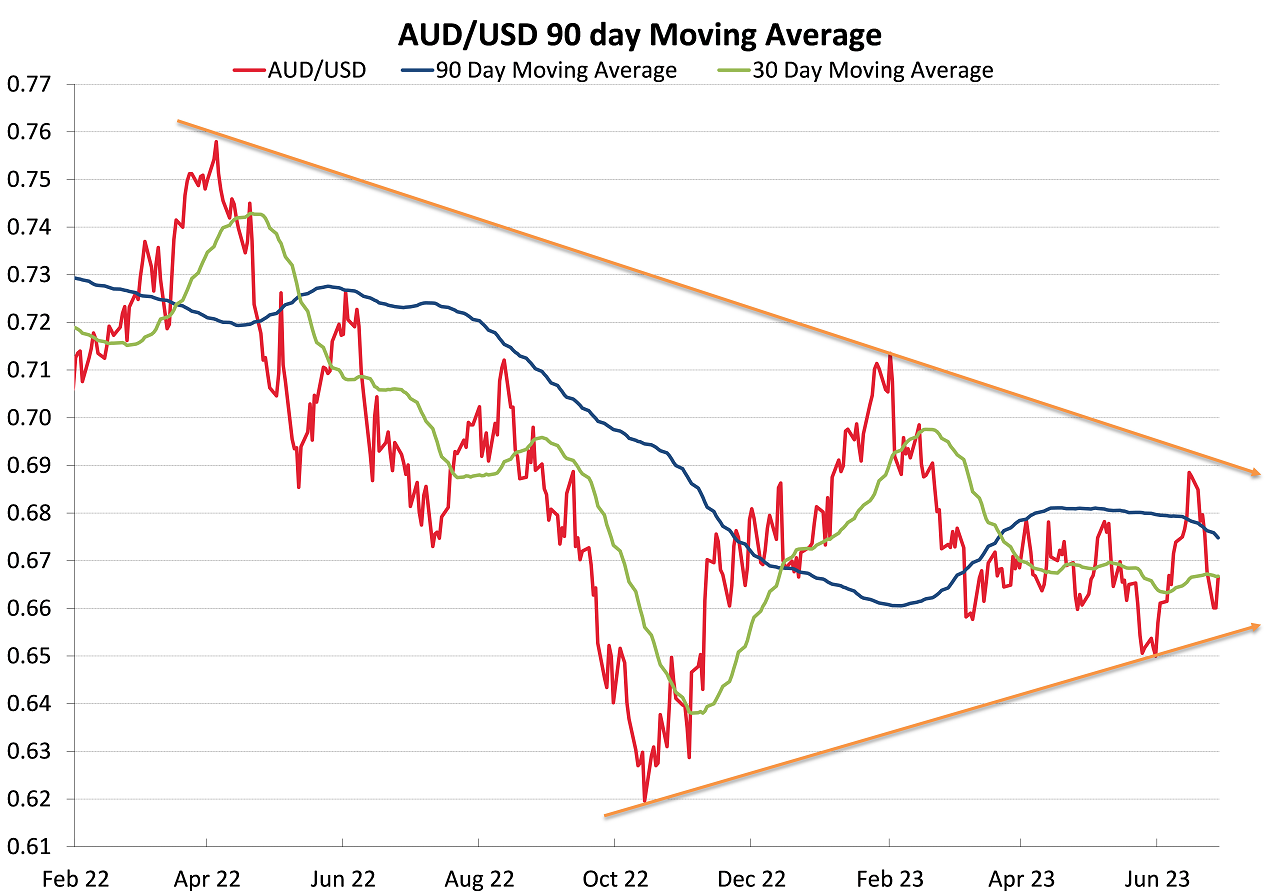

A weaker USD following the lower US inflation result for May last Friday has allowed the AUD/USD exchange rate to recover back up to 0.6665 from the 0.6600 lows. As the chart below indicates, the AUD has remained below the downtrend line over the last 15 months. A move higher above 0.6900 would break-out of the downtrend and lead to further AUD gains well above 0.7000. The support/uptrend line since the low of 0.6200 in October 2022 suggests that the AUD/USD rate needs to hold above 0.6550, otherwise lower levels are likely. A weaker USD and another hike from the RBA this week (which we expect) should push the AUD higher to the 0.6700 area – to the middle of the converging wedge chart formation. Blockbuster employment and retail sales numbers in Australia recently do not suggest that the RBA should be taking their foot off the monetary brake. However, the RBA has proven to be unpredictable and inconsistent in their management of monetary policy over the last two years and we should no longer be surprised at their surprises!

The AUD recovery to 0.6665 has allowed the NZD/USD exchange rate to, once again, pull itself of the bottom of 0.6070 to trade marginally higher to 0.6130. Further Kiwi dollar near-term gains will be determined by the USD general direction and whether the AUD breaks higher or lower.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

1 Comments

Many thanks to Roger Kerr for the excellent analysis. However, surely the re-election of a Labour-Green coalition with the Maori Party thrown in, and the Greens having more influence than this term, will put severe downward pressure on the NZ dollar over time. The economic policies of such a Left-wing government will continue to be disastrous for New Zealand.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.