A trifecta of economic stimulus in New Zealand

Three forms of stimulus are set to impact the New Zealand economy concurrently and very positively over coming months:

Fiscal stimulus:

The Government’s budget last week included a massive incentive for new business investment with an additional 20% tax-deducible depreciation allowed in the first year on purchased fixed assets. The accelerated depreciation policy was a surprise and much larger than anyone anticipated. It does demonstrate how serious the Coalition Government is about promoting higher growth rates in the economy, as part of the solution to reduce their budget deficit and debt levels. It was really good to see the Government taking some fiscal risk with such a bold policy initiative. Business firms will have a lower tax bill, however still the same cash flow in their businesses. The policy has to be commended for its simplicity, breadth, few restrictions and increased motivation to invest in productive assets.

The change is a shot in the arm for entrepreneurial risk takers, exactly what the domestic economy needs to shift it out of its recent doldrums. One of New Zealand’s largest economic challenges and impediments (outside of the agriculture industry) has been low productivity largely due to poor investment in modern capital equipment. The accelerated depreciation policy will hopefully lift investment in capital expenditure items and therefore increase productivity. If our GDP growth rate is increased by the increase in business investment activity stemming from this policy initiative, this type of fiscal stimulus would have done its job. At some point global investors and currency traders will recognise New Zealand’s superior growth rate and that is more positive for the Kiwi dollar in its own right.

Monetary stimulus:

The Reserve Bank of New Zealand (“RBNZ”) will be cutting the OCR interest rate from 3.50% to 3.25% this Wednesday 28th May, as they continue to loosen monetary policy as the inflation rate has come into the 1.00% to 3.00% target band. The overall tone of their statement and their prognosis on inflation and the economy will determine whether the local interest rate market will forward price the terminal OCR at 2.50% or 3.00%.

In our view, the RBNZ has reached a point in the economic cycle where they run the risk of over-doing the monetary easing. A signal that they are prepared to reduce interest rates further to 2.50% would potentially have monetary policy too loose for an economy that is now expanding. The recovering economy does not need assistance with additional monetary stimulus. However, the RBNZ could get this wrong and deliver that extra stimulus. If the RBNZ miss-read some of the signals on growth and inflation and overdo the monetary stimulation by reducing interest rates to 2.50%, it will potentially fuel another boom/bust housing cycle. That is the last thing the NZ economy needs as it sucks resources away from the productive sector. The RBNZ did earlier forecast a temporary increase in inflation over the first half of this year, however the risk (as the Fed found out to their cost a few years back) is that temporary or transitory inflation has a high chance of morphing into broader based and higher permanent inflation. There are already several indicators of our inflation not staying below 3.00% from the following recent developments: -

- The natural gas market has reducing supply (thanks to Jacinda!) and therefore prices are rising sharply. Electricity prices continue to increase as well.

- Food prices are increasing again as the higher export market prices determine the local prices.

- Public sector prices such local body rates and the cost to renew your passport continue to increase each year, keeping non-tradable inflation above 3.00%.

The latest RBNZ survey of future inflation expectations resulted in increases, something that the RBNZ should take serious note of to dissuade them from cutting interest rates too far.

Export price stimulus:

The sharply higher export prices are delivering additional billions of dollars into regional New Zealand. The extra money is invested and spent, adding to the economic multiplier effect. New Zealand producers of dairy, lamb, beef and horticulture are all enjoying higher prices that lifts confidence, innovation and investment. In April, our higher exports produced an overseas trade surplus of $1.40 billion, an amazing turnaround from a $3.00 billion trade deficit in the month of April 2024. We are now in an export boom, and finally other economic forecasters are starting to recognise the positive impulse that this brings to the rest of the economy.

The concurrent stimulus and resultant economic expansion is positive for the NZ dollar in its own right, however independent Kiwi dollar gains will continue to be restricted by the interest rate gap to higher US interest rates.

Bond markets react to compounding fiscal risks

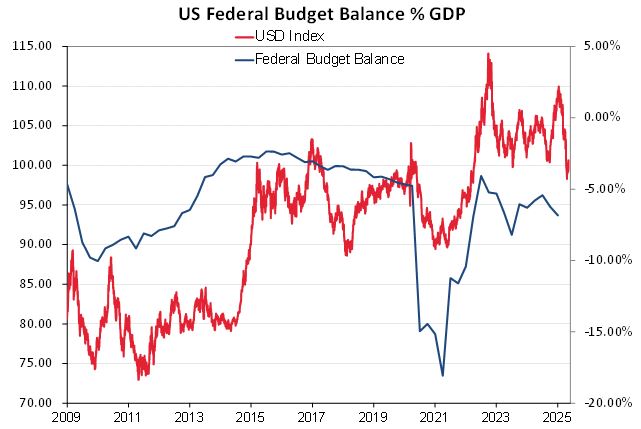

Moody’s recent downgrade of the US Government’s sovereign credit rating to AA1 has triggered a re-assessment of the equation that is US Government revenue, their interest bill and their US$37 trillion debt pile. The passing of the “Big and Beautiful” tax bill through Congress that cuts tax rates for higher income earners and reduces Government revenue adds to the conclusion that the US Government deficit is more than likely to increase to higher levels than the current 7.00% of GDP. Discounting the disruption of the Covid years in 2020/2021, the last time the US budget deficit was closer to 10% of GDP was in 2009 and the US Dollar Index was then around 80.00 (currently 99.00). Refer to the chart below.

President Trump’s master plan was that all the revenue from his import tariffs would pay for the tax cuts and reduce the budget deficit. So far, the revenue from tariffs is coming in at about 30% of the Trump claim of US$3.00 billion per day. The bond market in the US is now delivering its verdict on the Trump regime’s management of fiscal policy. The 10-year Treasury Bond yield has increased to 4.50% and the 30-year bond yield to above the critical 5.00% level. The bond auction last week was not well supported by investors, with foreign investors no longer having any interest in the US market. Foreign bond investors have abandoned the US and do not see that Trump has the capability of addressing the deficit/debt problem. Bond investors are displaying a loss of confidence in the US government, the US economy and with that a loss of confidence in the US dollar currency value as they continue to exit their funds.

The European Central Bank (“ECB”) Vice President Luis de Guindos stated last week that a “fundamental regime shift” could be underway in financial and investment markets as investors appear to be reassessing how risky US assets really are in the wake of trade tariffs. Foreign exchange markets no longer regard the US dollar as the safe haven place to go to when there is turmoil in the economic world. The US Government’s fiscal policy is seemingly adding to that downside risk on the US dollar. The Bond market and the currency market are essentially voting with their feet as they express concern about the US’s budget deficit, inflation and growth. US residential property sales in April were at the lowest level since 2009. Home mortgage interest rates for new builds are now over 7.00% and that stops activity levels as Americans cannot afford 7.00% mortgage rates.

President Trump re-ignited trade war uncertainties last week with a threat of an additional 50% tariff on European imports. The new tariff threat was either a negotiating tactic on the Europeans or a diversion strategy to pull the media focus away from the carnage in the bond market. Earlier Trump and his Treasury Secretary Scott Bessent had championed falling bond yields as evidence that the markets were supporting their economic policies. The bond vigilantes have destroyed that claim!

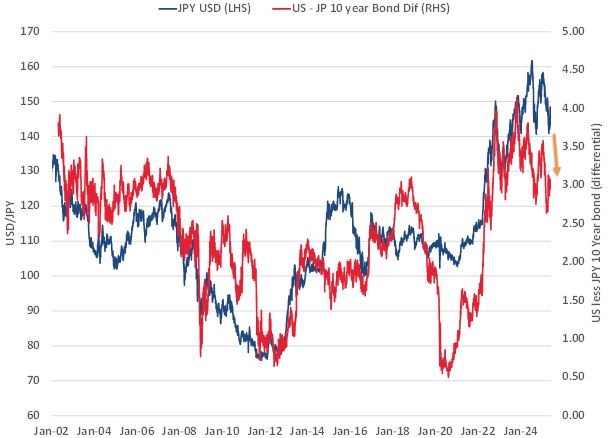

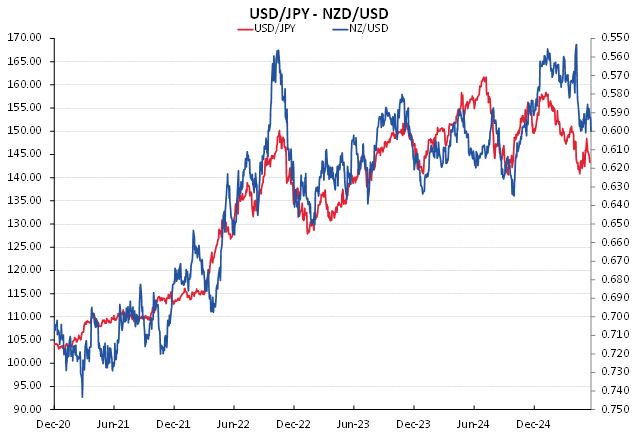

The sell-off in bonds was not confined to the US market, Japanese 10-year bond yields soared higher from 1.30% to 1.50% following their higher 3.50% inflation result. The current 3.00% gap (4.50% c.f. 1.50%) between Japanese and US bond yields still points to a much stronger Japanese Yen against the USD. The Kiwi dollar continues to closely track the Yen (second chart below).

The RBA start to yoyo exactly as the RBNZ have flip-flopped in the past

The Reserve Bank of Austral (“RBA”) somewhat surprisingly delivered a more dovish than expected monetary policy statement last week. As well as cutting their OCR to 3.85%, the RBA reduced their inflation and growth forecasts for 2025 and 2026 based on a weaker global economy. The softer outlook did not reconcile to the more hawkish tone and warnings from the RBA just six weeks ago when they expressed concern about rising wages and low productivity adding to upside risks for inflation. Perhaps the new independent Monetary Policy Committee, in their second meeting, are viewing the Australian economy as in need of support with lower interest rates. It could be argued that global risks to Aussie economy have reduced with the recent China/US postponement of high tariffs.

The rapid shift in the RBA’s economic outlook and monetary policy signals is a reminder of the RBNZ’s see-sawing in monetary policy management over recent years. Financial markets want to see consistency from central banks, not regular flip-flops in their economic forecasts and monetary policy stance.

As it transpired, the more dovish RBA did not send the Australian dollar lower for very long last week. A brief AUD sell off to 0.6390 against the USD was quickly overtaken by a weaker USD on global FX markets. The AUD/USD rate ended the week at a much stronger 0.6500.

The US dollar was again under downward selling pressure again following Trump’s 50% tariff threat on the Europeans, the USD Dixy Index dropping away on Friday 23rd April from 100.00 to close at 99.00. As a consequence of the USD depreciation, the NZD/USD is once again poised to move above 0.6000.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

1 Comments

"some point global investors and currency traders will recognise New Zealand’s superior growth rate and that is more positive for the Kiwi dollar in its own right"

What superior growth rate? Evidence please. I understand that officials look at the accelerated depreciation offered by 5 countries; the US, UK, Canada, Australia and Germany, but then followed none of them. All the others have caps and limits to the type of assets that qualify-NZ will have no limits. The revenue minister Simon Watts says there can be no cost blow-out, because there is no limit. If the tax deductions run to $10 billion or even $10 billion, that's ok. That's despite official advice that much of the money will flow to offshore companies.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.