Summary of key points: -

- Time is running out for Trump as markets start to capitulate

- The tale of two halves that is the New Zealand economy

As the Iranian war moves into its 12th week, the oil price and the financial markets are telling us that the US Government is no closer to reaching a solution, conclusion or end point. The great dealmaker, President Donald Trump, appears to be once again failing to secure a deal, just as he failed to secure a deal to end the Russian/Ukraine war. Geo-political nuances and forces are proving to be greater obstacles than what Trump contemplated or imagined. There were hopes that his high-powered meeting with Chinese Premier Xi Jinping this last week would have delivered some progress on leveraging the Iranians to come to the peace talks table. The outcome of the talks was a lot of ceremony and fluffy words, however little progress on ending the conflict and reopening the Strait of Hormuz.

The lack of progress towards ending the war has resulted in oil prices being sold higher again as global supplies see no end to the disruption. WTI crude oil prices moving sharply higher over recent days from US$100.00/barrel at the start of the week to US$105.40/barrel at the Friday market close. The US dollar made similar gains on its Dixy Index from 98.00 to close at 99.20, its highest level since early April. As a consequence of the USD appreciation, the NZ dollar and Aussie dollar are both down one cent to 0.5840 and 0.7150 respectively.

Global bond markets have also sold off over this last week, reflecting increasing investor concerns of the oil shock lasting longer and therefore potentially turning a temporary inflation spike into more permanent inflation increases. The higher yields from the bond market sell-off also represents investors expecting Government bond issuers to be borrowing more/increasing the supply of bonds as GDP growth slows and fiscal deficits increase and tax revenue are reduced. In the case of the US, the Government’s budget deficit is also increasing from having to repay tariff monies and the extra cost of the war. At a 4.60% yield, US 10-year treasury Bonds are at their highest levels since late 2023 when the Federal Reserve were hiking short-term interest rates. It is the same story for the following NZ and Australian 10-year Government Bond yields at 2 ½ year highs of 4.78% and 5.11% respectively. A substantial political risk premium has been added into the negative mix for UK Bonds (Gilts), as their 10-year bond yields soared up to 5.20%, the highest level since 2008.

The bond and FX markets will not turn around the other way until there is clearer evidence that the Trump regime have a workable plan to end the war and reopen the Strait of Hormuz. Trump’s only plan at the moment appears to be exerting economic pain on Iran by blockading their ships at the oil export ports. Iran now only has two weeks of oil storage capacity left before they have to stop pumping it out of the ground. It will be hurting them financially; however, the Iranians have proved to be a lot more resilient to date than what the Americans ever imagined.

Whilst the oil, bond and FX markets now seem to be placing renewed bets that the war will go on for longer and inflation will stay higher for longer, the investment guru Warren Buffet is seemingly betting the opposite way, with Berkshire Hathaway selling US$8 billion of Chevron Corp shares in recent days. Buffet “taking some cream off the top” as they reduce their holding in Chevron from 6.60% to 4.20%. The run up in equity markets may also be becoming to an end as higher bond yields hurt valuations.

Trump is rapidly running out of runway on a number of fronts: -

- His claims that the US economy is doing well because the equity markets keep going up was always misplaced, however a serious downward correction in equities from here will have him scrambling to find anything positive before the November mid-term elections.

- US gasoline prices at the pump are now over US$4.50/gallon and household affordability is a major issue, as confirmed by the plummeting consumer confidence surveys.

- US interest rate markets are now pricing-in increases in the Fed Funds interest rate later this year, making it extremely tricky for incoming Fed Chair Kevin Warsh to deliver to Trump’s expectations of lower interest rates.

- The US housing market has serious problems as new-builds come to a grinding halt with 30-year fixed mortgage interest rates now at 6.70% and that is unaffordable for most.

- His tariff policy is in disarray with the 10% global tariffs also ruled illegal under the 1974 trade law by the US trade court. The US Government is currently refunding US$35 billion of illegal tariffs following the Supreme Court ruling, and the Government expects to eventually refund up to US$166 billion to more than 330,000 US importers.

- He has riled all America’s allies on both security and economic matters to the point that no-one trusts the Americans anymore. The Americans have pushed away all their friends and are now seemingly not capable of solving the Iranian situation alone.

For the Trump-led Republican Party to have any chance of retaining the House of Representatives and the Senate at November’s mid-term elections, the current volatility and uncertainty in oil markets, equity markets and interest rate markets needs to come to an end very soon. For all these reasons, Trump is under increasing pressure to find a diplomatic solution to end the war. He has always stated that higher gasoline prices for a short period “is the price that has to be paid” by US households to rid the world of the nuclear terrorist threat that is Iran. Time is running out for Trump as US households do not see the benefits of that outweighing the financial pain.

As time runs out for Trump, his next TACO moment is likely to be suddenly forgetting his previous ultimatum that agreement on the uranium must be an integral part of a peace deal and the re-opening of the Strait. It does appear that the Americans are weakening on this point and therefore a separation of the uranium resolution from a peace deal and Strait re-opening seems the likely next step. China, India and Japan, along with the UK, need to take the lead in a multi-lateral agreement to re-open and control the Strait so the oil tankers can get going again. Trump will now be squeezed to agree to any method to get the oil price down again.

Drawing the likely war scenarios together does result in a conclusion that this latest bout of higher oil prices and higher US dollar will be as short-lived as the previous spikes higher. The pullback in the NZD/USD exchange rate to 0.5840 should therefore be used as another opportunity by local USD exporters to ensure they are hedged to maximums against the risk of sharply lower oil prices and USD value when the war ends. Should equity markets continue to fall ahead of any Iranian resolution, the NZD and AUD, as risk currencies, will be susceptible to further depreciation in the very short-term. However, perhaps over-riding that negative force on the Kiwi dollar, we would expect that long-USD position holders in speculative currency markets to be taking their profits at the current Dixy Index level above 99.00 i.e. selling the USD here, not buying more USD’s.

The tale of two halves that is the New Zealand economy

Whichever way you look around the world currently, it is a landscape of strained and sometimes hostile division. Global superpowers are exerting their muscle as Trump rewrites the rules of diplomacy and stability. Politically, the US is divided internally as ever. Australia and the UK are politically unstable as their respective Labour Government’s lose public support.

Here in New Zealand, the general election on Saturday 7th November looms as a tighter contest between left and right than otherwise might have been the case had the economy continued to grow robustly in 2026 if the Iranian war/oil shock had not happened. Our observation over the years is that “political risk” as a factor on the NZ dollar value is more of a risk in the minds of local business folk than it is with offshore currency players who are active in the NZ dollar market. To them, Labour’s and National’s economic policies are not that far apart, merely some minor differences on distribution policies. The fear locally is of course that a Labour Party, reliant on the Greens and Te Pāti Māori to form a government, will be forced into more “far left” economic policies. The oil shock is a good reason currently to postpone major business expansion or investment decisions. However, the risk that we could have a close-run election result in six months’ time should not be flashing red flags in any business’s risk register at this time. Interest rate differentials and relative economic growth performance are likely to swamp political risk as drivers of the NZ dollar value later in the year.

In the US they call it “Main Street versus Wall Street” to describe the chasm in financial and economic wellbeing between the haves and the have nots. Outside of the skyrocketing AI, semiconductor, software and technology stocks on Wall Street and the wealth created by the folk who have invested in those stocks, business and personal financial wellbeing is not in good shape in the main streets of US towns and cities. Here in New Zealand the chasm is between the two big cities and the rural countryside. As we witnessed in the latest employment statistics for the March quarter, the unemployment rate is significantly higher in Wellington (Government restructuring) and Auckland (flat property/construction market) than what it is in Otago where tourism and agriculture are booming.

Unfortunately, the majority of the media’s journalists who report on the NZ economy live in the two cities of Auckland and Wellington. The local economic commentators, and the media that regurgitates their analysis/views, are all seemingly blindly extrapolating the current downturn in the economy, due to the oil shock, as if it will be a permanent situation for all of 2026 and 2027.

We take a different view.

On the scenario that the oil prices revert to US$70/barrel on the Strait reopening sometime in the next few weeks, business and consumer confidence in New Zealand will bounce back up just as rapidly, to the previous levels before the war. The overall negative impact on the economy will be much less than what most people expect as the duration of the disruption was not actually that long. In any event, New Zealand has not run low on energy as many feared it would, it is just that the price has shot up. Like all free markets, if the higher price is due to less supply, demand will automatically reduce in response and that evens out the supply/demand imbalance. In the case of New Zealand, the discretionary demand for petrol and diesel has reduced as you would expect it to do. The use of petrol and diesel for sport, recreation and “fun things to do in cars” will be curtailed, however it is not the end of the world as we know it. Discretionary retail spending is also down as higher petrol costs squeeze household budgets. The same happens when interest rates go up. It is not unusual or terminal.

The cities have not had the boost to incomes that regional New Zealand has experienced over the last 18 months due to higher dairy, meat and horticulture prices. Tourism numbers and tourism spending levels have returned to pre-Covid levels, and the Aussies are swarming in as the Kiwi dollar is very cheap for them against their Aussie dollar. Economic activity, optimism and investment is strong in the regions, which highlights the substantial chasm/divide between town and country that is poorly understood and hardly reported on.

House construction activity has taken longer to pick up in Auckland as it takes longer for the benefit of lower mortgage interest rates to flow through as everyone fixes their rates. Job security is also a major factor in retail spending and the property market. Some of the alarmist media reporting on the negative impact of the oil shock on the NZ economy is causing some of that job insecurity. It will change dramatically when the oil prices inevitably reverse.

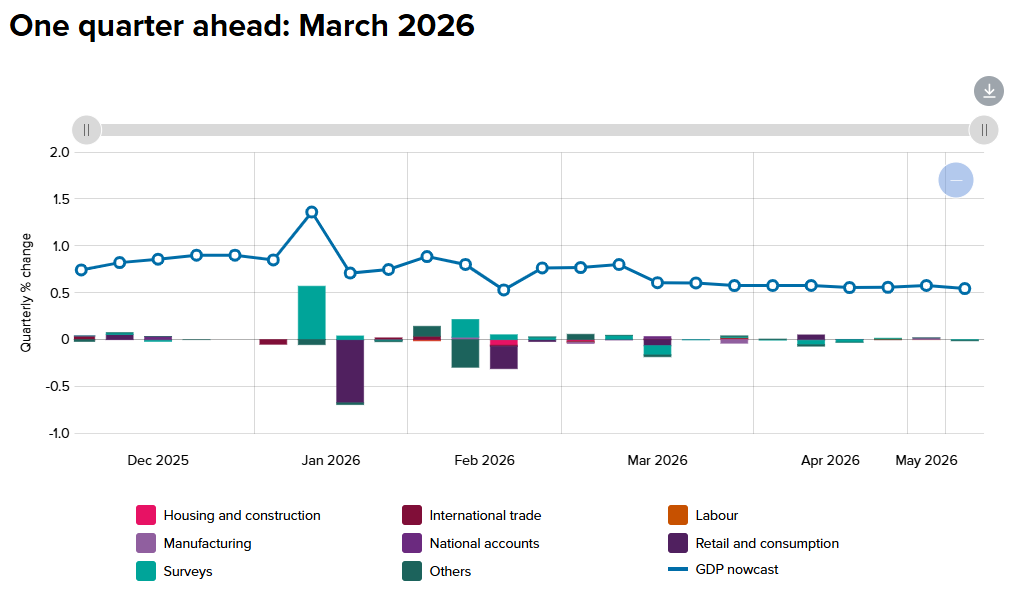

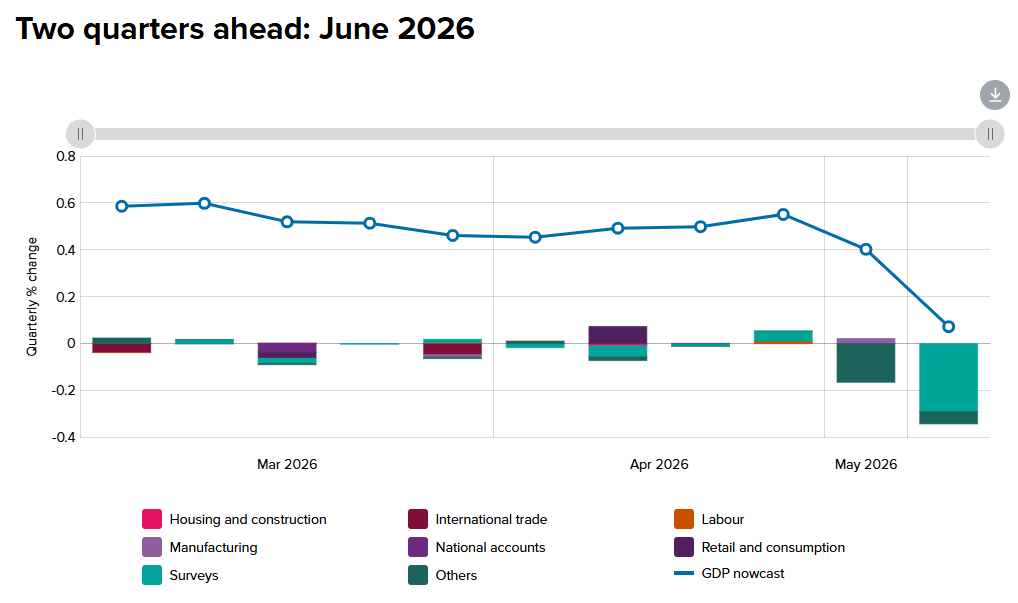

The RBNZ’s Nowcast predicter of GDP growth in the March 2026 quarter has not changed too much from the +0.50% expansion expected, despite the oil shock hitting in the month of March. However, the Nowcast predicter for the current June 2026 quarter GDP growth has plunged from +0.60% to below +0.10% over the last month. Note that the cause of the decrease to +0.10% is “survey’s” i.e. the sharp fall we have seen in business and consumer confidence. Strong export and tourism industry results should hold the June quarter’s GDP growth above zero, potentially higher if the war ends soon.

chart:daily exchange rates]

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.