Summary of key points: -

- The Kiwi dollar reverses upwards – with more to come

- Some positive New Zealand economic developments you never hear about

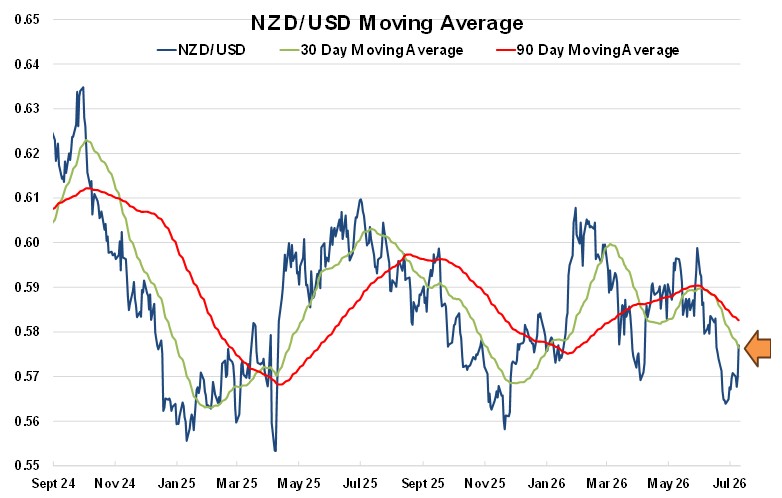

For most of the last 12 months the Kiwi dollar has been under the pump from bouts of concerted selling, aided by the currency punters who receive the added benefit of the positive forward points when holding “short sold NZD’ positions (NZ interest rates below those of the US, therefore they effectively borrow the lower NZD interest rate and invest in the higher US interest rate). Whenever there has been a reason or catalyst to sell the NZ dollar (RBNZ monetary loosening or USD appreciation from tariffs, the Fed or the war), the additional forward points benefit has made it a relatively attractive trade. As a result, we have seen the regular spikes downwards in the NZD/USD exchange rate to the 0.5600 area (refer to the chart below).

Recent events have now fundamentally shifted that “one-way bet” environment for the Kiwi dollar. Over the last two weeks NZ dollar has again rapidly reversed out of the latest spike lower (as we projected it would), appreciating from 0.5630 to 0.5770. The sea change in sentiment and expectation for the Kiwi dollar has come about through a combination of: -

- A hawkish pivot on monetary policy from the RBNZ which has seen them increases the OCR to 2.50% and signal further hikes to come.

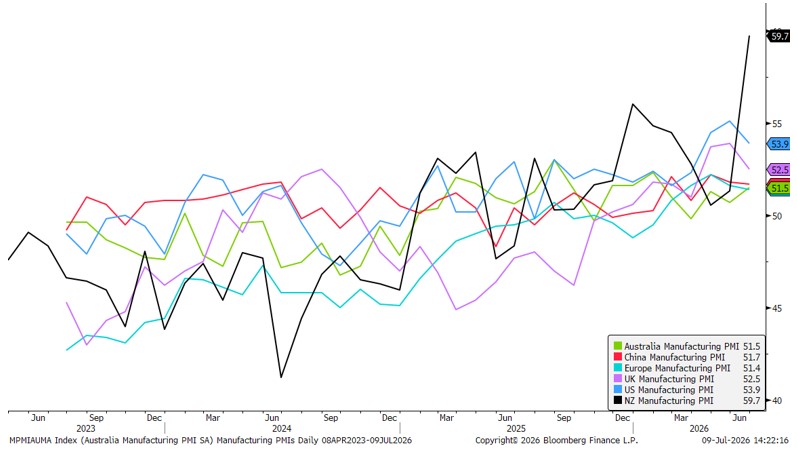

- A spectacular increase in the Business NZ Performance of Manufacturing Index in June to 59.7 from 51.3 in May – a very positive economic response to oil prices plummeting (refer to the second chart below).

New Zealand is suddenly standing out economically and the previous prohibitive interest rate differential for the Kiwi dollar are starting to move the other way.

Global Performance of Manufacturing Indices

The RBNZ’s Monetary Policy Review report last week highlighted and confirmed two important aspects on the New Zealand economy and monetary policy settings that we have commented on several times over the last 12 months in this column: -

Underestimated economic growth: Over the period July to December last year the RBNZ slashed the OCR interest rate from 3.00% to 2.25% as they determined that the economy was faltering and inflation would decrease in that environment. We stated at the time that the economy was already in a strong export-led recovery, and we were not headed for another mini-recession. As it has transpired, GDP growth in the September and December quarters last year were a robust +0.90% and +0.50% expansion respectively. The RBNZ have now belatedly recognised and admitted that the economy was travelling in the opposite direction to which they were forecasting.

Underestimated the level of inflation: In loosening monetary policy so aggressively last November, the RBNZ must have expected that there was a real risk of inflation decreasing to below the 1.00% bottom limit of their target range. There was no other justification for such monetary stimulus under their single inflation mandate. Back then, they were forecasting that the considerable excessive capacity in the economy would lead to domestic (non-tradeable) inflation reducing from well above 3.00% to 2.00%. Disregarding the US/Iran war and higher oil prices, non-tradeable inflation has, to the contrary, remained elevated over the last nine months as the excess capacity had no impact on price setting behaviour in the administered (public sector) and non-competitive parts of the economy. We have listed these non-competitive culprits many times e.g. banking, supermarkets, insurance, electricity, domestic air travel and some building supplies. In addition, the cuts to interest rates last year depreciated the Kiwi dollar and that contributed to higher tradeable inflation (imported product prices higher) than the RBNZ were forecasting. Last week’s statement from the RBNZ confirmed that the excess capacity did not reduce inflation as they expected and the administered, non-competitive and imports (currency related) sectors have all increased prices.

These admissions from the RBNZ all add up to a major monetary policy blunder last year when they cut the OCR to 2.25%. At the time, this column was very much in a minority view when stating that the RBNZ were “overcooking” the monetary easing. Time has proven that position to be the more accurate one.

The following extract from our 25 January 2026 FX Market Commentary report also pointed out the likelihood of a monetary policy error: -

“Further evidence of a likely monetary policy mistake is comparing the length of time interest rates stay stable following a monetary policy easing cycle. If the RBNZ is forced to increase the OCR interest rate as early as June this year, the time from the last cut in November 2025 will only be seven months. History tells us that the average time period of stable OCR interest rates following an easing cycle is 12 to 15 months. The very short time period on this occasion tells you that the RBNZ got it wrong in easing policy too far”.

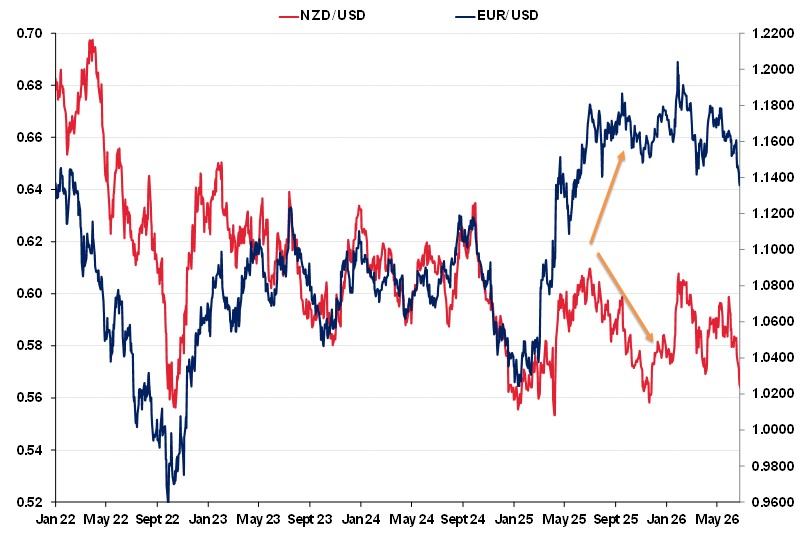

The wayward decisions by the RBNZ over the second half of 2025 had a major impact on the NZ dollar currency value. The decreases in NZ interest rates caused the NZD to depreciate against the USD from 0.6100 in July 2025 to a low of 0.5580 by mid-November 2025. As the chart below confirms, the Kiwi was forced lower by the RBNZ at a time when the USD was softer against major currencies, such as the Euro. The previous close correlation of the NZD/USD exchange rate to the EUR/USD rate was completely demolished and a major divergence transpired. The weaker NZ dollar on its own account sunk the NZD/EUR, NZD/GBP and NZD/AUD cross-rates. Up until now, the NZD/USD rate has been unable to close up the gap to the EUR/USD rate.

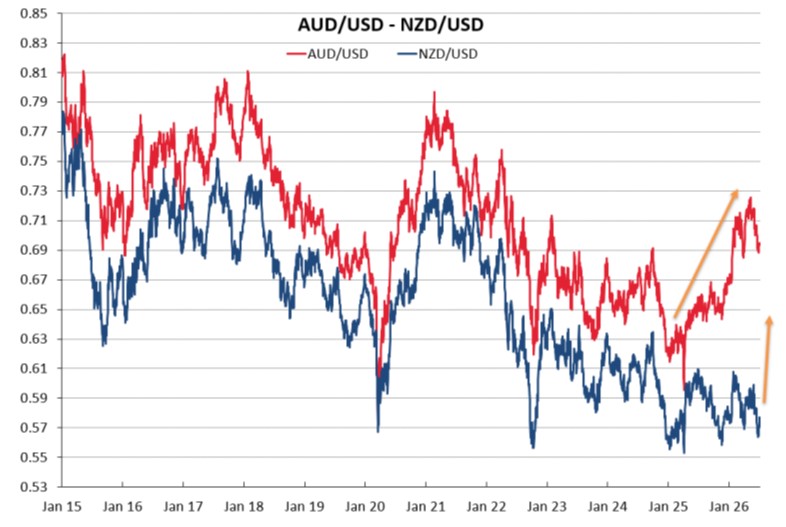

We now have the real prospect of the next six to 12 months being a period in the currency markets where New Zealand will be increasing its interest rates, in stark contrast to the potential for Australia and the US to be cutting their interest rates. We have always stated that the RBNZ have been six months behind the Reserve Bank of Australia in monetary policy adjustments. Therefore, it will be of no surprise that the Kiwi dollar copies the AUD playbook of six months ago, when the AUD/USD rate appreciated eight cents on its own from 0.6400 in November 2025 to 0.7200 by May 2026. Changes to interest rate differentials stimulated the dramatic AUD appreciation, the same could be in store for the Kiwi dollar.

In summary, the RBNZ scored a classic “own goal” with monetary policy management last year as there was no need to loosen policy so much in the first place. The rapid pivot in monetary policy since proves that point. The good news is that prolonged period of NZ dollar weakness has been a major boost to our export sector with substantially higher export commodity prices. We will now see NZD appreciation in its own right, returning all the currency cross-rates higher. The hedge funds will be very busy unwinding their “short sold NZD” positions as the NZ economic landscape has changed.

Some positive New Zealand economic developments you never hear about

The following two significant developments for the New Zealand economy have largely gone unnoticed and scantily reported in the mainstream media here.

You will not know about these very positive economic/business initiatives from watching TVNZ One News or reading the Royal NZ Herald online!

“How New Zealand became a global laboratory for climate friendly cows”

(the newswire headline on Bloomberg 8th July 2026 - written by their NZ reporter Tracy Withers)

It is often said that the New Zealand economy is based on our ability to commercialise “agriculture science”. It seems we are putting another step forward in this space to find solutions for methane emissions.

Bloomberg report “New Zealand is on the cusp of giving farmers new tools to curb the amount of greenhouse gas (methane) livestock emit, with Ruminant BioTech awaiting registration for a bolus that can reduce emissions per anima; as much as 70%”. The capsule placed in an animal’s stomach slowly releases a compound to suppress the production of methane. The company is one of a growing number of startups and researchers testing everything from methane-inhibiting compounds extracted from daffodils to vaccines and selective breeding for lower-emitting livestock. Reducing emissions is important for our food exporters seeking to convince global customers like Nestle and McDonalds that New Zealand dairy and meat deserve premium prices.

AgriZeroNZ is a co-investor alongside government research agencies and Beef + Lamb in the CoolSheep program, which is breeding low-methane rams. It is developing a similar program for beef cattle.

Scientific solutions to our livestock methane emissions issue is not just something that is being talked about, it is actually happening in practice.

“Game development studios now exporting $800 million per year”

The video gaming industry in New Zealand is going from strength to strength. Latest data shows that combined studio sales revenues (95% exported) increased to $829 million in 2025/2026, up 17% from $710 million the previous year. The industry here is almost two years ahead of its target to reach $1 billion is annual sales revenue. There are now 43 game development studios in New Zealand with the number of games in development up from 170 to 194. New Zealand made games are reaching global audiences, translating into significant growth in export income. The industry is a digital export success story and seems to be one that will continue to grow at a rapid pace.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.