The independent global economics researcher that was among the first to pick house price falls in New Zealand this year is now tipping prices falls for "several' other "vulnerable" countries as well.

Capital Economics senior economic adviser Vicky Redwood who outlined in a report earlier this year the housing markets (including New Zealand's) that looked most vulnerable to rising interest rates, says housing markets are now showing signs of starting to weaken.

"While the consensus is that house price inflation will merely slow, we expect outright prices to fall in several of the most vulnerable markets," she said.

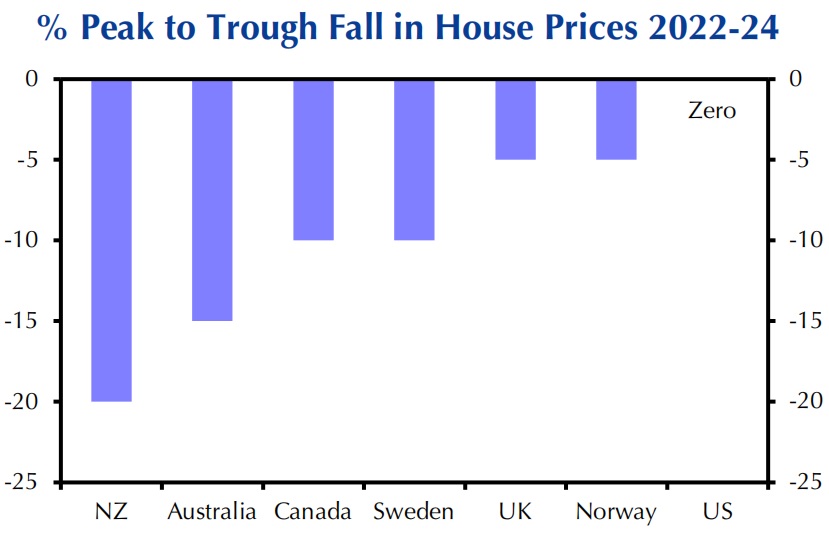

Last month Capital forecast peak to trough falls in NZ house prices of 20% by the middle of next year. This month the economists have forecast a 15% peak to trough drop for Australia.

Redwood said the economists had identified the housing markets that looked most vulnerable to rising interest rates, "based on how overvalued they are and the characteristics of their mortgage markets".

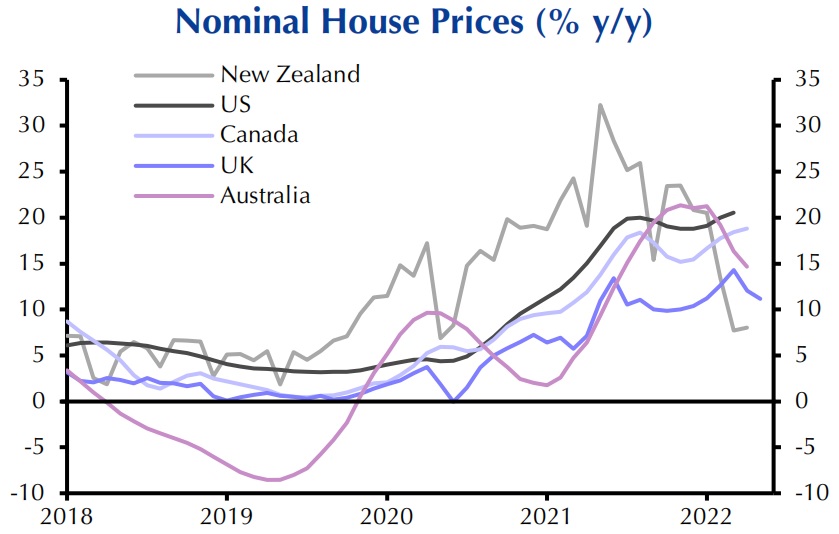

"House price inflation in these countries is already easing. Australia, New Zealand and Canada have seen outright monthly falls in prices. There are also signs of a slowdown in housing demand and sales.

"We have now pencilled in house price falls over the next year or two, ranging between 5% and 20%, in New Zealand, Australia, Canada, Sweden, the UK and Norway.

"And the risks are skewed towards even bigger falls.

"After all, even these drops will reverse only part of the rise seen over the past couple of years. And interest rates may rise further than we expect – in which case, price falls would spread to other countries including the US. (We currently expect house price inflation there to slow to zero.)"

Redwood said the house price falls will drag on economic activity, although it might take until next year for the effects to be fully felt.

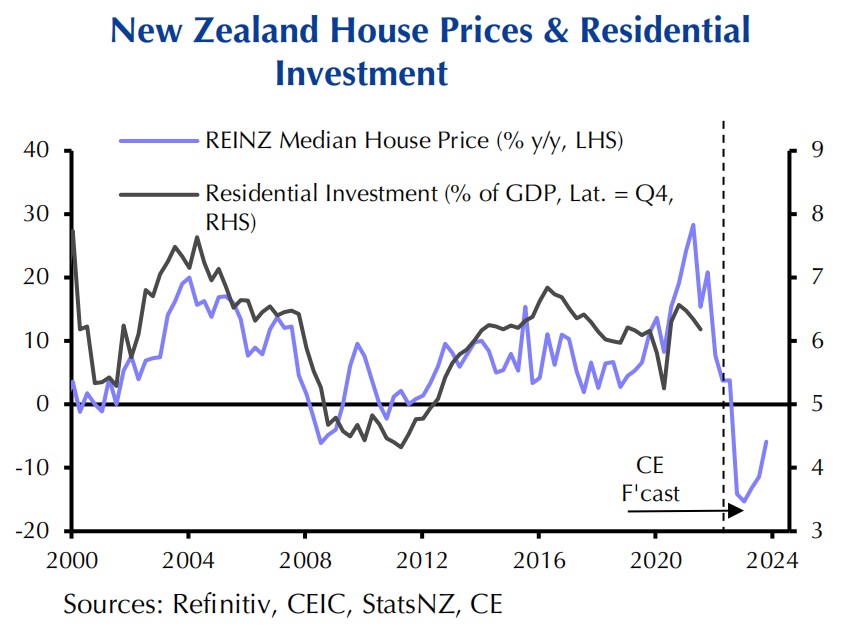

"Residential investment will fall as it becomes less profitable to build new houses; we expect drops of 10% to 20%, knocking 0.5% to 1% off GDP. Canada looks especially vulnerable. House price falls will also dent consumer spending by knocking confidence and reducing collateral."

Redwood said she doubted that any of this will stop central banks in those countries from continuing to raise interest rates.

"After all, weaker housing is one of the key transmissions through which higher interest rates are expected to cool demand and bring down inflation. Even if central banks are worried about causing a total collapse in housing markets, such concerns are likely to take a back seat now that inflation has got so high.

"However, countries that experience large house price falls are more likely to see interest rates peak at a lower level; indeed, this is a reason why we expect the peak in interest rates to be lower in Canada than the US. And once inflation has dropped back, falling house prices could make central banks quicker to cut interest rates; for example, we expect rates in Australia and New Zealand to fall by end-2023."

In a separate report, Ben Udy, Capital Economics Australia & New Zealand Economist, Sophie Oudea, Research Assistant, and Marcel Thieliant, Senior Australia & New Zealand Economist said the Hawkish shifts by both the Reserve Bank of Australia (RBA) and the Reserve Bank of New Zealand (RBNZ) in recent weeks have prompted them to forecast "an even more aggressive hiking cycle by both central banks in the months ahead".

"Both central banks hiked rates by 50bp [basis points] at their latest meeting and we have now pencilled in further 50bp rate hikes in the months ahead. At the same time, house prices have started falling in both countries. House prices are down more than 5% from their November peak in New Zealand. And while prices only just fell in Australia in May, all signs point to the downturn persisting," they say.

"While we had already expected prices in both countries to decline, the steeper rate hikes we now anticipate will feed through to higher mortgage rates and higher debt repayments. That will weigh heavily on the housing market before long. We have therefore raised our forecast of the peak to trough decline in house prices to 15% in Australia and 20% in New Zealand. And those downturns should cause similar-sized falls in dwellings investment in each country in the years ahead.

The economists say that output & activity indicators show growth in Australia should outpace New Zealand in the years ahead.

"...We think that the tailwind from the reopening of Australia’s economy should overwhelm the drag from stagnating real incomes and rising interest rates for now. Indeed, the renewed rebound in NAB business conditions points to GDP growth remaining very strong by past standards. By contrast, we think that a slump in dwellings investment in response to plunging house prices will result in sluggish GDP growth in New Zealand.

"...New Zealand’s labour market has continued to tighten with data showing job advertisements continuing to rise. That said, the steeper tightening cycle from the hawkish RBNZ should cool labour demand. And with the border set to reopen, the labour force should also get a boost so we expect the unemployment rate to rise to 4.0% by early 2023." [NZ's unemployment rate was 3.2% as at the end of March.]

70 Comments

20%? Ha. I see that 20% and raise you 50%!

... yes ... house prices in NZ are 100 % above fair value ... a 50 % drop will bring them back to affordability for regular folk : families & friends !

How long will it take for our political leaders to realise that rampant house price increases is a very bad thing for our society ...

How long is a piece of rope?

Oops, shouldn't be putting ideas into people's heads.

Sorry Dale that's a dumb comment not something you should mock or joke about.

I'm just really upset that NZ isn't very special anymore.

What we need is a graph of economists' predictions for peak to trough falls over time. They started off talking about a "moderation" in house price growth, then minor falls, then 10%, now 20%. What next?

Economists should put their money where their mouth is. I'd happily offer to sell my house to Vicky Redwood under contract at the end of 2024 for 20% less than peak price.

Look at that graph, we are leading the world...................sadly for overpriced housing

Countries like Australia, Canada and New Zealand that avoided the worst during the GFC may be the countries that take the biggest hit this time around...

Nah Adam, logic is that house prices only fell 10% during the GFC in NZ and that was the worst case ever...so therefore house prices can NEVER fall more than 10% here. (sarc).

... " house prices double every 10 years in NZ " ...

ROFLMAO !

Can you please clarify why this is so funny?

"House prices double every 10 years in NZ"

This is demonstrably true, unless you think they also mean "House prices go up in a straight line"

https://www.interest.co.nz/property/87961/adjusting-inflation-gains-hou…

House prices doubling every ten years is a 7.5% return. Is this only crazy because it's the housing market?

"Share prices double every ten years" - Is that statement just as mind blowing to you?

House prices doubling every ten years is a 7.5% return. Is this only crazy because it's the housing market?

It's the religious undertone that doesn't work for me. NZers put more belief in this kind of stuff than the laws of physics.

Right, if it's a "rule of thumb" then its fine?

The numbers themselves don't matter?

It's a case of "past performance is no guarantee of future results". Extrapolating this trend ad infinitum is what people are poking fun at (aka Ashley Church and other simpletons).

Yes, past performance is no guarantee of results. But trends exist.

As do real estate market crashes that take decades to recover.

Ireland's property market doubled in the last 10 years. So it's true.

Just make sure don't "zoom out" otherwise you'll see the 70% drop and that it's still 10% down on the peak 15 years ago.

Relative to income/earnings yes it is.

Say if NZ wages increase at CPI in the longrun of 2-3%...how do we expect house prices to increase at 10%p.a. in order to double every 7 years (or 7% for 10 years).

I did some calculations a few years back: in 100 years Auckland average house price would be $1 billion at double every 10 years, and I think the average wage would be $1 million at 3% pa, so house prices 1000x average wage. So no it can't continue forever.

It's not a doubling compound. It's like Ireland, doubled in the last 10 years. Still 10% below it's 2007 peak which was followed by a 70% fall, buuuut it still doubles every 10 years...

More like 4.5% over the last 20 years.

Why is a fact regarding past performance funny?

I'm not laughing. Just pointing out that a big number (house prices) can't compound at a higher rate in the long run, than a smaller number at a lower rate (incomes) when the bigger number is valued by the cash flows from the smaller number.

There is a disconnect and that has been covered over by falling interest rates for the last 40 years. Now that nominal rates have more or less hit zero and appear to be regulating back to longer term, historical norms.

So at some point, the smaller number must catch up with the bigger number either by:

a) static prices while interest rates and wages regulate

b) market deleveraging/debt defaults/financial crisis/crash - price reset.

The bigger number cannot, without the benefit of falling interest rates, continue to out compound the smaller number it is dependent upon.

Same with share prices and company earnings....hence why P/E ratios have been very accurate over the years for determining future returns on stocks (see the cyclically adjusted P/E ratio (CAPE) that Robert Shiller has put together). If prices ever get too detached from earnings, in the long run, the subsequent return is poor until CAPE returns back towards a longer term norm.

"House prices double every 10 years in NZ"

It's bias and funny... Of course, it can double when you look at the timeline back and time the right 10 years. But not every 10 year, if house prices double every 10 years in NZ, then no one should lose money through investing into property, right? then how are you explaining this to the people who bought houses last year November and had to sell theirs now at cheaper prices?

So it wouldn't be funny if it was said more accurately?

"On average over the last 60 years house prices have increase by 7.5% per year which equates to doubling every 10 years"

Let it go Kjeldorian, you're wasting your time. House prices are going down now, therefore people cannot possibly see that house prices can double in 10 years. It's just short sightedness.

Well exactly. Ireland's a good example. They had a dreaded housing market crash, and yet house prices doubled from 2012 to 2022 showing how resilient housing truly is.

I mean, you just have to ignore the 70% decline and the fact that anyone who bought in 2006 - 2007 will only be at 90% of their purchase price.....

same story...

https://www.ceicdata.com/en/indicator/ireland/long-term-interest-rate

in 2012 interest rates in IR were were circa 7%

in 2022 they were 1%

the amount of money that could be put in houses more than doubled.

That doesn't demonstrate at all that the housing market is resilient.

The cost of an house is always the same, aka is equal to the max amount of money the bank is willing to concede you.

if anything it demonstrate how stupid the system is

like you said... just pretend you didn't see the way down :D

Yes, they are silly sayings for justifications they don't warrant.

Who cares if they double every ten years if income keeps relative pace. But it's not.

There have been periods where they have doubled in 10 years. Over the same timeframe, incomes havent increased anywhere near as much.

The increases are unsustainable and don't seem likely to continue in my view.

From the data series you linked, I make the average annual increase ~9% in nominal terms and just 1.9% after accounting for inflation. I'd very roughly categorize this as a tale of two halves - high inflation caused the early doublings and falling interest rates caused more recent doublings and are likely responsible for most of that 1.9% real annual return.

Inflation is clearly still a real threat, but the downward trend in interest rates doesn't have much further to go unless we head negative.

I couldn't easily find one for NZ, but USA is a good example too

https://themortgagereports.com/61853/30-year-mortgage-rates-chart

so... I think that is more like:

"the amount of money you could afford to be given to buy an house doubled circa every 10 years in the last 30 years"

Ergo, the correct question is: is it possible to have OCR in negative territory (nominal, not real) in the next 10 years?

I hope and I think that that won't happen. Then house prices will not double again, (probably never again in real terms, given also the fact that the demography is going down too).

Shares prices are susceptible to interest rates too, btw... and no, that is a false statement too

House prices could drop 50% in 1 year, and then double again in 10 years. You'll be back to where you started from in dollar terms after 10 years, prices will have doubled in 10 years. Rinse and repeat. House prices double every 10 years.

:D

Kj - very interesting link. But it only shows 50 years of house prices, so any statement made about house prices should really be qualified by that. NZ has a long history of boom and bust, not just in house prices, starting with when the English started to settle here imho. Also house prices stagnated and dropped around 40% in real terms in the 1970s after a boom. This was masked my the very high inflation of that period. House prices started to climb again in the 1980s after the Rogernomics deregulation when credit became much more readily available and reserve banks “ tamed” inflation. We have probably entered the endgame of that massive boom, or series of booms. I think we are in for a long term decline in house prices, It may play out like the 1970s. Inflation is the debtors friend.

They very well could double in 10 years, from the bottom of the coming trough. 2020-2030 through 2022-2032, not so much.

Only if RBNZ could come to rescue by dropping LVR and OCR but Alas... !

ho ho ho but there was a problem last time round with 2% mortgages wasnt there.............

Plenty of houses went way lower than 10% in GFC

So... welfarism for property investment to taper for a while before attempts to reinflate can recommence.

Labour WANT House Prices to Increase.

Both tinges of Natbour are unfortunately beholden to this entitlement mentality.

The Force is strong Luke.....

Want to guess how many of the approx 50,000 consented homes are actually going to get built?

20% looks likes fair call to me. This will not be an even distribution however as places like Auckland will get hit harder.

"places like Auckland will get hit harder" - big call. To me it is the provinces that seem the most overvalued. Why is an average house in Palmerston North worth $750,000? There is plenty of land so it is very hard to justify.

600-700 in Turangi ?

Yes the places out the back, in the scrub like Palmy and the other country towns will drop bigly as the City homeowners faked wealth evaporates.........as is happening now.

Auck outer suburbs house and sections (1970's/80s) are now listing for sale in the 750 -900k bands, and soon to be sinking further, without trace.......the slide down is greased and slick.

Looking a prices for houses in a large Tauranga suburb today (on TM) and there is barely an 'auction' left. Just a bunch of houses still at last years price .. and those that really need to sell seem have ever decreasing prices with 'price reduced' .

Nobodys buying here right now...

OSE,

Not quite. I have just sold a small house in the Mount after 22 years. It took just 30 days, though nobody went to the auction. The day after 2 qualified offers came in and a day later, an unqualified offer at a price i was happy to accept. Ignoring the net income, the return on what I paid including lawyer's fees, was just under 8%pa compound.

I think I would have got a bit more last year, but then i would have had much less interesting reinvestment options.

Aeesome stuff. Good for you!

During GFC higher end prices were more like 50 % in some cases in PN

Silver lining the more and faster house prices drop the less the interest rate rise , I suppose that's a cup half full approach to it .

Not a given unfortunately. House price falls do not directly affect the ocr decision making.

It will take time for the ocr/rate rise to affect households spending (only affects someones discretionary spend when they actually remortgage and have higher interest payments) and in the meantime we will need to keep raising the ocr to brake local spending faster, to match international rate moves and thus keep the ex rate low enough we can affors to buy stuff from overseas.

I would guess if a neg wealth effect happens and people stop spending because they feel poorer ( because their house price dropped) it may have some effect on inflation sooner?

But i cant see any way for rbnz to reduce the ocr because house price drop - regardless how low they go.. for if we need to move the ocr to protect our economic fundamentals that has to come first.. else society fractures when noone can afford to buy food and they take to stealing it.

I would love to hear another way.. as house price falls mqy be catastrophic for many.

Is Doom Goblin syndrome the new Covid. Its spreading to international independent think tanks, or are they just taking the piss...?

I remember the 70's which were ugly in a lot of places. It hit my fathers generation much more than ours. The 87-91 downturn was also painful if my memory serves me. It took 5 years before prices regained, to where they were at the start of their fall in 88. But I wont say that because most of you don't wont to read that.

I ways said the covid boom was 5 years of growth at once so that seems about right.

It is happening in other countries as well, which is correct but not to forget that worst hit will be countries which has had the biggest and fastest jump - NEW ZEALAND.

Most countries had a jump of 15% to 25% unlike NEW ZEALAND where it jumped from 40% to 60% plus.

This was always a huge bet on low rates (and therefore low inflation) persisting perpetually. Unfortunately for the people stuck in property times change, the fundamental assumptions that drive house prices have collapsed.

Unfortunately ( if we take into account not just investors and recent FHBs.. but also builders, developers, RE agents, tradies, supply chains etc...) we are talking a LOT of people stuck in property?

bit like being stuck in storks in 1987..... Propellor property adds still on NEWSTALK ZB there will be stunning yield plays at the bottom of this mess

Storks never fail to fly, eventually.

yes...

I mean, it was obvious that letting house prices going so high would have been a very big issue, soon or later.

The possible blast radius of this bomb become bigger and bigger every time somebody "fixed" the market in favour of even higher house prices.

so yeah, now is "later"

What would you suggest?

Let inflation go? Bail out?

Popcorn ?

lol

Well we have let inflation go but wages never kept up, that was kind of the flaw in RBNZs plan. I'm not sure that bailing out housing would be a productive use of taxpayer money.

Popcorn might be a better answer, let the market resolve its own issues. Banks are well capitalised.

-20% looks far too optimistic to me. I think Ireland’s experience 2006 - 2014 is more likely. Rising interest rates create the first phase of the falls. But before that is over secondary effects kick in….less disposable means economy slows and job losses, job losses mean even slower housing market, constantly falling house prices mean even those who want to buy will defer till they see market bottom out, and so it keeps falling lower and lower. It will be painful, but ultimately necessary with long term benefits for many more than will be hurt on the way down

These guys are worth listening to, at least.

Unlike the clowns (often with vested interests) that we have as economists in this country.

It would make interesting reading if economists had to publish a 'forecast vs actual' based on their past predictions.

NZ and Ireland are two VERY different scenarios.

Ireland had a massive boom due to EU and a huge amount of international investment (Apple etc).

Their workers production efficiency increased increased hugely - our is dropping.

We have no EU, nor any inward investment the size that Ireland had.

Key factors for large house price reduction in NZ

- Reduced land costs - possible

- Reduced material costs - impossible

- Reduced paperwork and infrastructure costs - like hell.

- Reduced population - possible

- Much higher interest rates - a given

Correct around their boom. Plenty of Multi-national American corporates with head offices based in Ireland.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.