Financial markets are "becoming attuned" to the risk that the Reserve Bank (RBNZ) may push the Official Cash Rate up by 75 basis points in its November review, ASB economists say.

In ASB's Economic Weekly, senior economist Mark Smith says the markets are now pricing in a 5% OCR by mid-2023 and therefore "there is likely more upside to NZ yields".

"The RBNZ looks like it means business and we are confident NZ inflation will eventually be brought under control.

"However, there will be casualties. Odds of an economic soft landing are also shrinking.

"We have also lowered our house price outlook, with inflation-adjusted cumulative falls sitting at a hefty 24%," Smith says.

Since beginning the latest 'tightening' interest rate cycle the RBNZ has hiked the OCR from the Covid-emergency-low of 0.25% as of October 2021 all the way up to 3.50%, and with more to come in November.

In its last forecast for the 'peak' of the OCR made in August, the RBNZ suggested a high-point of between 4.0% and 4.25% by the middle of next year. Since then, however, fears have grown globally of far more persistent inflation and this has helped to drive up wholesale interest rates - with ours rising accordingly.

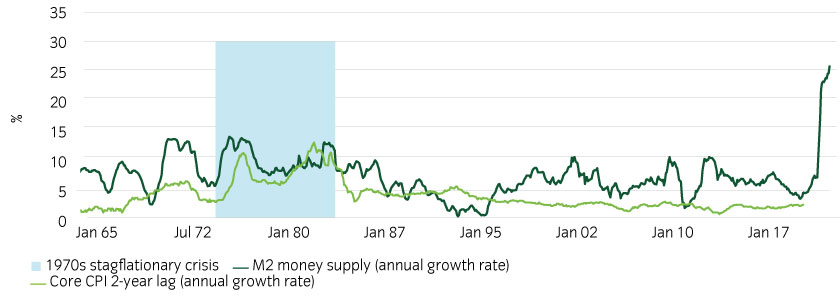

Smith says that annual headline inflation rates in NZ and many OECD countries may "generally" be heading lower but are still around multi-decade highs and "a virulent economic and social problem that needs to be rectified".

"Once up, it will prove difficult to push inflation back down.

"Central banks are now living with the reality that to lower inflation to acceptable levels, it will take tougher talk and more restrictive policy settings than were initially envisaged."

In New Zealand, Smith says we seem to be past the peak in headline inflation, and there are some promising signs that headline inflation should head lower in future.

"Core inflation, however, will likely prove to be more difficult to dislodge from multi-decade highs.

"The RBNZ has the ‘inflation bit’ between its teeth. High core inflation, confirmation of a broadening front of price increases and that of a wage price spiral becoming more entrenched will likely necessitate a quicker and firmer application of the monetary policy brakes."

Smith noted that last week was another volatile one for local and global yields, with double-digit gains for most NZ swap and bond yields.

"Positioning and global influences look to have been the major drivers. Market pricing also firmed, with mid-2023 peak OCR expectations clearing 5% late last week. The 2-year swap yield peaked just shy of 5% (4.97%), its highest level since the GFC, with 10-year swap yields hitting 8-year highs (4.74%) but down at the end of last week. NZ Government bond yields were around 30bps higher with those for the 10-year tenor peaking at roughly 10-year highs (4.61%). Global yields have been volatile, but the trend has been upward..."

However, Smith say despite the "massive" increases of late, ASB economists have retained "our upward bias" for NZ yields.

"The RBNZ looks to remain steadfast in trying to push annual inflation below 3% and in its October Review left the door open to a possible 75bp November hike. Market pricing is adjusting to this possibility (61bps priced in for November), and risks are tilted to a more frontloaded pace of hikes."

ASB economists still expect a 50 basis point lift to the OCR in November (4% OCR), with a follow-up 25bp hike in February 2023 (4.25%).

"We then expect the RBNZ to hold for a period, with cuts from the second half of 2024 as the OCR is returned towards neutral levels (circa 2.5%-3%).

"Risks are heavily to the upside," Smith says.

110 Comments

These ASB "economists" have been privy to the unsealing of the scrolls.

7% Interest Rates This Year, Guaranteed ! Prophecy Confirmed.

30% Crash In Home Prices by December, it's a Certainty. Will Wellington or The North Shore be the Winner ???

Celebrating The Prophet.

Interest Rates are going 7 and Up.

https://www.youtube.com/watch?v=0gIiNRDdaVI

30% by December, where? So you are saying Wellington will fall another 10% within 2-3 months, or the North Shore will fall 12% in the same period?

Almost no chance

North Shore has already fallen -28%.

Let that anger out HouseMouse.

"Within Auckland, six of the seven territorial authorities had annual price decreases, with the North Shore’s the largest at 28.6% (to $949,000)."

https://www.stuff.co.nz/life-style/homed/real-estate/130137138/house-pr…

Really? On the HPI?

I am not angry at all, I couldn’t care less, other than knowing the facts.

You are wrong HouseMouse thats why you are unhappy. You must be unhappy a lot.

Rates have gone to 7% and you are still in denial of that also. The Prophet is awaiting his congratulations from you HouseMouse, but your jealousy is eating you alive. Do the right thing HouseMouse, you know what that is.

You are weird.

Fixed rates are still much lower than 7%.

And the HPI is down 10.4% YOY in the North Shore.

Now I have seen it all, housemouse fighting property bears. Is that a first

The cat must be away, so the mouse is running a fowl...

Just over a year ago the OCR was 0.25% and no one saw it at 3.5%. No one, that is, who was supposed to anticipate it.

Why we take any notice of those same blind forecasters today is beyond me.

(NB: And it doesn't matter whether any of us 'saw' it or not. We aren't paid a ~quarter of a million bucks a year to get it right. They are. Yet, accountability for their efforts? Zero.)

Absolutely.

But the same applies for all experts right? They get to be catastrophically wrong, and keep their high paying jobs.

While if every day Joe Builder or Chef or Driver gets something catastrophically wrong, they lose their jobs.

And we don't even have to listen to them talk utter offal all the time.

Exactly. The experts have been wrong on this, big time. One Michael Baker proudly told us there would be a massive second wave of Covid about a month ago. Well, he was completely wrong again. I see he is on the news again telling us of some gloom and doom about Covid again to try to stay in the news. Previously this guy was an expert on fresh chicken and tried to get the public banned from being able to access it (lest someone get sick from not cooking it right), no one listened to him then, and yet we believed that he knew something when Covid came along. Clearly, he knew bugger all, just like these economists, with their soft landing, small interest rate hikes and 1-2% house price drops. These guys are wrong about everything. Best guess is usually the opposite of what the experts say. We are going back to 2019 house prices and 2019 interest rates (actually much higher for a while to fight inflation). I actually saw some finance or economist in some rag a few days back musing that 'maybe all these gains will be unwound and we will be back to 2019'.....well HELLO that is exactly what is happening.

That dude has been missing the limelight.

For sure.

Epedimiology has the same problem economics has. It wants to be a grown up science like physics or chemistry so epidemiologists made up a bunch mathematical modelling crap that is full of dumb assumptions and fails to model any real world circumstances.

It's like efficient markets.....nice idea in theory not really how the world works.

Suddenly the lame kids in epidemiology, that were in the dark parts of university that no one was interested in, have found themselves to be the cool kids. And they defintely don't want to lose that.

Enter "long covid".

Baker and Wiles have done massive amounts of damage to society with their fear mongering and pseudoscience. It would be great if our media had at least had voices to oppose them from team reality but unfortunately "nothing much to worry about" doesn't sell well, which isn't just on media.

In the end we are our own worst enemies

You wonder why they keep on embarrassing themselves. And yes that is a good point on models, they are almost always wrong.

As for economists, even if they are right only slightly more often than the market that can be very prosperous. But I’m not sure that they are.

I totally agree with the sentiment, but what makes you think we stop at 2019?

We've been playing with funny money for more than a decade and inflation isn't going anywhere, anytime soon.

You are right of course. I expect it's been going since time immemorial.

The handling of the GFC certainly opened my eyes to the corruptness of our systems.

What was it mortal hazard, doral blazard....ahhhh who cares? Nothing to see here.

But at least it only bought bankers, economists and politicians into disrepute. They didn't have much repute in the first place.

But with covid they decided to throw the reputaion of science and public health under the bus. And as bad as the other stuff was besmirching the reputation of science and public health is just not going to be good when they want us to respond to something serious.

And at some stage, there will be something serious.

I'm thinking Monkey Ebola Super AIDS.

Essentially, now we have no monetary ammo for "Monkey Ebola Super Aids" lol

It's become so ridiculous, a house plant would do a better job of governance at this point.

True.

But is it the fault of the politician...or the system.

I think they mean well, but the reality of power is something different to the dream of public service.

Alan Watts:

"And what seems a good thing (Text sourced from https://www.organism.earth/library/document/mind-over-mind) today—or yesterday, like DDT—turns out tomorrow to have been a disaster. What seemed in the moral and spiritual sphere, too—like great virtues in times past—are easily seen today as hideous evils."

Reality is complex, trying to control it ends almost always in disasters.

As the saying goes: Power corrupts and absolute power corrupts absolutely - hence the govt now wanting to extend their covid powers for a couple more years (smell that desperation as the power trickles from their weedy fingers).

For folk who actually engage with scientists and people, the pandemic hasn't damaged the reputation of these areas. Most damage seems to have been done primarily among those who source much of their "analysis" on Facebook, rather than more robust sources. Anti-intellectualism seems to have experienced quite the rise, as in previous times in history. The folk doing the screeching seem to have been watching "Plandemic" more than reading deeply from science and medicine journals.

Politicians may have played their part in this, but social media algorithms designed to sell advertising by monopolising attention - and there's no better way than outrage - have played a huge part.

Reading into some of the issues, it's intriguing to note that perceptions of bias in media are inversely correlated to depth of engagement with content. And - looking at the example of climate change in USA audiences, for a similarly provoking issue - acceptance of climate change as a real issue correlates strongly with curiosity, regardless of where folk sit on the political spectrum. That is, the more curious folk - representing depth of engagement with issues and serious content - are far more likely to view climate change as a real and pressing issue than those who engage with content much more shallowly.

FHB are lambasted for making poor financial decisions, "they should have known interest rates wouldn't be low forever", despite interest rates only going lower for the last 30 years. Yet the billion dollar profit a year organizations such as the banks who signed off on these loans couldn't forecast interest rates going up? In any other business, the client's risk is generally managed by the business themselves, which is a large reason why they derive a healthy income.

So ASB only think nominal values will fall a further 3%?

I wonder if TA still thinks fixed mortgage rates will peak in the mid 5’s?

What TA thinks, and what he says are two very different things. Do you think he truely believes half of what he writes? He knows what’s coming.. but he’s got bills to pay like anyone

It’s a good question.

I used to think he genuinely believed what he says but I have started to really question that this year. He’s made some shocking calls.

Either way he has lost it.

...but, but it's not TA's fault, it's what his tea leaves (I mean "surveys") said.

TA and the AC only talk what's good for their own book......

They are self interested and are single handedly trying to soft land the sky high housing ponzi.......they may soon need scraping off the tarmac, as wafer thin schreaded sheets of formerly known spriukers!

TA's basically living in Australia now, that might show what he really thinks...and/or he's trying to hide from pissed off kiwis that took his advice.

I didn’t know he’s over there, developing his tan on the Gold Coast?

Seeking a new hair colourist ?

Yea he is literally living on the Gold Coast.

Or all the people like me who were seriously pissed off by his ‘smashed avocado’ BS from a few years ago at the BNZ.

TA made that comment in March 2017. Back then the average 1 year fixed mortgage rate was under 4.5%.

Now all the 1 year fixed rates start with a 5 or a 6 and are rising fast. With a combination of rising rates and upcoming liquidity crunch, all logic points towards house prices falling well below those 2017 levels.

Sucks to be you, Tony, you were wrong, wrong, wrong! I enjoyed my debt-free avo on toast this morning. Sorry for all the young people that debt-peddlars like Tony have sucked onto the debt treadmill. But there is still time for them to sell, and deleverage, if they are quick!

by Yvil | 13th Oct 22, 12:38pm

LAG, it's all about lag and few seem to understand this point.

The lag between the RB raising the OCR and mortgages coming to their term, people re-fixing and then, after a few months realising how much less money is left for lattes. Yes people know the squeeze is coming, but many only adjust their spending when they are really forced to. As I have stated before the squeeze on spending from the increasing OCR is only going to start being felt in 2023

Delay between the OCR rising and the CPI stopping rising. Remember the CPI is being measured year-on-year, meaning that any inflation from the last 9 months and there's plenty, is also included in the latest CPI figure. In conclusion it will take even longer for the CPI to stop rising and it will only do so meaningful when the 2022 first quarter CPI rise drops out, in other words when the 2023 first quarter CPI will be released, which will be in… May 2023 !!! So it's pointless expecting a meaningful drop in CPI before May 2023.

In conclusion, because of the delay explained above, the OCR is going to get raised far too high (most likely 5%), NZ will be in recession in Q1 2023 but this will only be reported in the GDP in June 2023 (we're so slow in NZ) by then CPI will be lower but not yet in the target range of 1-3%, the RB will think "we're heading in the right direction", the next set of data will be Q2 GDP deeply negative reported in September 2023 and Q2 inflation confirming its continued drop towards 1-3% reported in August 2023 and then, the RB will panic and drop the OCR back down aggressively.

So expect a much lower OCR by end of 2023 after a likely peak of 5% earlier in the year.

Yep the banks have got it all wrong. The FED is still way behind the curve, actually its not a curve its a near vertical straight line but I digress. Still 1 in 5 odds the RBNZ will have to go 1% in November unless they want their Christmas holidays interrupted with an emergency meeting.

Agree with much of what you say.

But a lag in data showing recession is not unique to New Zealand.

Possibly the US is already in recession (perhaps we are as well) and it will come out in the inevitable revisions later down the track.

Do you discount stagflation entirely? We might get a recession and inflation might still stay high. It doesn't seem like OPEC are bothered much about our inflation. We have morons in politics (whatever your flavour there is a dearth of anything novel or interesting being said by our politcal class). And we all know all this debt can't be paid back.......

Ultimately I think all central banks will risk hyper inflation over stagflation or deep recession. With the debt load in the west what choice do they have, it will be the last method for kicking that ugly beat up can....just a little bit further down the road.

Well and I agree back with much of what you said.

1) of course the lag is not unique to NZ

2) I think stagflation is a real possibllity

3) I also agree that when the recession officially comes, RB's will agree to let inflation run higher rather than make the recession worse

Well we are agreed than!

I should also throw in the possibility of a banking crisis.

No one learned anything from the GFC and I doubt the banks have even remotely good liquidity (regardless of the "tests" they have "passed").

The strength of USD must be flogging any carry trades and if you are reliant on international wholesale markets (and it's hard to see much funding being provided by deposits here) that is going to hurt as well.

The biggest worry is always the thing no one is talking about.

No one learned anything from the GFC and I doubt the banks have even remotely good liquidity

Or maybe the problem is they learned too well from the banking crisis, that they'd be bailed out and allowed to walk away if their risks went south.

Excellent point.

And depressingly true I fear.

The strength of USD must be flogging any carry trades and if you are reliant on international wholesale markets (and it's hard to see much funding being provided by deposits here) that is going to hurt as well.

Love your work Denny. Definitely cutthing through all the fluff with this insight.

If the average kiwi knew about macroeconomics and the corruption in the system, there would be civil unrest. Perhaps ignorance is bliss for most so long as the mortgage gets paid

The average Kiwi knew about RBNZ corruption.

That's how we got the big peak in house prices during covid.

These are the kinds of comments that people were making to show that they knew about the corruption, were leaning into the corruption, and thought that the corruption would work in their favor and make them personally wealthy:

- "The RBNZ/Govt have got our backs. They will never let property prices fall."

- "The RBNZ will never let interest rates rise."

- "If house prices fall, the the RBNZ/Govt will pull some levers to make them rise again."

Average Kiwis LOVED the corruption. They were all in there like pigs with their snouts in the trough, buying houses like there was no tomorrow, loading up on more and more debt.

Look at the debt to income figures in this article. https://www.interest.co.nz/property/110261/new-figures-rbnz-show-71-mon…

These are not the debts of rational investors, taking on rational risk. These are the debts of irrational investors, who truely believe that the system is corrupt, and will continue to be corrupt, and that the corruption will benefit them if they play the game.

I hope that future generations are not so greedy, or naive.

As you know Yvil I had been thinking the same way but I don’t think it will be nearly as bad now.

I still think the economy will weaken significantly in 2023, and I also think that *some* people who remortgage will have to tighten their belts significantly.

But I am less DGM about it now, heck I think unemployment even has a chance of staying less than 4.5%, because the labour market is so tight.

Strange world we live in when Yvil who found DGM's offensive, has in time become the biggest DGM on the site.

Haha.

I think, fortunately, most will be OK. Some highly leveraged property investors might be in trouble. I have little sympathy for them.

Some people will lose their jobs and their homes, but I think luckily that will be fairly rare.

Some people will lose their jobs and their homes, but I think luckily that will be fairly rare.

For the majority, she'll be right ya reckon

Yep!

what do ya reckon?

Are you much more of a DGM? 6-7% unemployment?

Not a 'reckon' kind of guy. As for the unemployment measure, it's of no interest to me as I believe that unemployment measaures are broken. I recommend your read the Roy Morgan Real Unemployment methodology.

https://www.roymorgan.com/findings/australians-say-the-roy-morgan-unemp…

Oh I know that. But even so, the extent to which that flawed measure rises or not is still a useful economic gauge.

Oh I know that. But even so, the extent to which that flawed measure rises or not is still a useful economic gauge.

Not it's not. It's useless, even directionally. It sends false signals.

Ask an employer whether the record low unemployment rate is true! I’m pretty sure most would agree it is very difficult to find an employee right now.

You obviously overthink

Well it's simply because, until 2022, I didn't see large scale trouble ahead, now I think things are going to get ugly.

Do you still rate TA, Yvil?

Yvil has always been a DGM, but refuses to accept it.. symptom called Dual personality ..

Or maybe it’s just called being correct! Time will tell I guess.

Many are not feeling the actual pain yet as are seeing diminishing saving by growing inflation but still able to pay the bills so is wait and watch

Many people have had pretty decent pay rises this year that will have covered much of the increased costs of living.

In the case of our household we are significantly better off as I type than at the start of the year. But once our mortgage rolls over in early December those gains will be pretty much cancelled out. But we certainly won’t be worse off than at the start of the year. In fact we will still be better off as I am finishing a car loan late this year.

I am sure many are like us. I am sure too that some are genuinely hurting.

And there in lies the rub HM.

The cafe's, bars and restaurants round me are buzzing. My 16 year old is getting paid adult minimum wage to wash dishes in the school break as there is such a shortage of applicants for hospo jobs. All anecdote but persuasive and I'm sure not isolated. Then we have a very weak NZD that arguably will weaken further due to the Fed. As a result I don't see any massive changes coming soon for tradable or non tradable inflation.

My pick is that the OCR may well peak at 5% but I think it will stay up there for much longer that anticipated and that will be the story of 2023. The pain it inflicts when a person re-fixes is sufficient, it just needs to happen to a lot more people to have the desired effect hence my prediction.

As a result I think we will see 1.2 - 1.8% HPI drops month on month with a peak to trough of around 35%. The elections in September may give some earlier respite but National are doing such an outstandingly average job that they risk snatching defeat from the jaws of victory.

Yep a very weird mix right now- slumping house prices, rising interest rates, very low unemployment, relative economic resilience.

And I think all of these things will be sustained, more or less, for the next six months.

I think it’s hard to make any predictions, look how much has changed in the last 12 months. But yeah the safest prediction is always “more of the same”

Bring back the youth wage I reckon' too many teens getting too much money for simple work when there's people out there doing hard yakka for the same wage. Devalues the hard work of many who do magnitudes more work for only a slight bit more pay

Markets are now pricing in a 5% OCR by mid-2023. I actually think that, if Orr does not raise by at least 100bps (to 4.5%) next month, he will be forced to raise the OCR to a peak of 5.5% or 6% by mid 2023, and keep it at around that level for quite some time. The longer Orr waits before taking any serious action, the higher the OCR peak will have to be, and the longer it will have to stay at that level.

Surely the longer they keep inflation high and the kiwi dollar dropping the better (for them).. as our house prices appear (to the average punter) to have dropped very little and govt and household debt seems much less. Also by prolonging the slowdown we are less aware of the contrast of the peak and troughs.

However If they rush and kill inflation too quickly it all looks very obvious. Even though in real terms the economic outcome would be much better.

I agree Fortunr. I think people have reallt underestimated the degree to which rates will need to rise to get inflation under control. The danger is that action comes but only after a damaging delay.

"We have also lowered our house price outlook, with inflation-adjusted cumulative falls sitting at a hefty 24%," Smith says.

So if that is their inflation adjusted pick, nominal falls >30%?

Keeps going up...

No their maths is nominal fall of 15% + 9% inflation = real fall of 24%

So as I say higher up, prices nationally have already fallen 12% from peak in nominal terms, they only see a further 3% fall? Lol

No their maths is nominal fall of 15% + 9% inflation = real fall of 24%

Yawn. Real price movements are such a cop out. Nominal is all that matters as 'real income' growth is more or less negative (and has been long before the Covid period).

Hahahaha. "Soft Landing".

The only thing soft around here is the brains of the idiots who thought we could have two years cowering under our beds, higding from little more than a bad flu......and that that would somehow be "better for the economy".

You are fast becoming one of my favourite commenters… lol

.... that's not nessasarily a good thing lol! 😆

I fear you're showing signs of Early Onset Curmudgeonhood. Kids gonna need to get off your lawn.

Even with a 75 basis point hike the RBNZ is going to fall well behind the Fed which is predicted to make two 75 basis point hikes in the same period. The NZ dollar may have further to fall yet

Min 150bps, Orr we are just playing footsies at this point.

Unfortunately the media pearl clutchers can't bear the thought of it....

This is correct and a huge risk of undoing all that work of raising the OCR and having to keep it up higher for longer as RBNZ seeks to unwind their mistakes. Unfortunately, nobody seems to care. Busy gloating at other countries it appears. Sometimes about stones and living in glass houses come to mind...

The chances of house price declines overshooting on the downside has certainly increased. With each passing month, animal instincts for financial survival will become more imbedded in society. No-one wants to me the one left holding the baby. Why buy when it will only be cheaper tomorrow? Interest rates are still rising, sales volumes and pricing power remain severely anaemic, even after already forecasted percentage declines have been matched ahead of time, then easily surpassed.

House price fall. Till now only the froth has been removed but the cup is still full.

Further Fall from here on will result in pain.

The perils of negative gearing.

Nobody will want to hold the baby, if the baby costs 100s of dollars a week to hold.

Every 1% up or down in rates works over time to a 10% climb or 10% decline in housing prices simple formula but it works, the speed of decline in rates was quick and so was the house price climbs now the hikes in rates are coming quickly so will be decline in house price’s. The big unknown is how inflation affects the fluctuations but when mortgage rate hit 7% that would add up to around 40% crash but would have around a six month time lag.

When does a prediction become a persuasive plea?

These bankers know that the CPI read tomorrow will start with a 6. They know that there is increasing and justified pressure across the world to calm the farm with the rate hikes already. They also know that if the momentum reduces on rate hikes, their fat bonuses will be a few thousand lighter in 2023.

I am mortgage free with cash in the bank and I am getting solar installed, $30k.

Got a mortgage from ANZ @ 1% for 3 years as part of the energy efficiency scheme.

How cool is that!

1% for 3 years ???

Yep. 1% mortgage.

Presume that's a 5KW or more system, including battery storage? For ~$30k.

Hope so.

If we are talking about good or bad investments - that sounds like a good one.

Would take our household about 10 years just to break even on the purchase price, and that is assuming it supplied all our power. Hard to see it as a good investment.

Depends on where you live as well, the likes of Hawkes Bay and the top of the south island would pay the system off in no time with the sunshine hours

When you consider 200 ah lithium battery are around 4k each (for decent lithium phosphate ones with internal bms ) I doubt that would include batteries... I spent 30k on my yacht solar with 800ah lithium storage, 1600w solar, 3kw inverter.

I think you'll find you are not mortgage free if you have a $30k mortgage.

Don't forget to keep those panels clean and avoid any partial blocking.

Very cool, just don't expect to achieve ROI. That's only a perk for the installer.

That's right Juzz, we have been off the grid since 2015 and it's good, no power cuts etc. But even if you pay 3 or 4k a year for power it's cheaper than setting up a real power system. Stay on the grid unless you really need to go off.

I really dont get this inflation stuff and frankly dont believe this whole story about rates being required to keep it under control. Look at what is going on internationally with war and climate and then inside NZ and tell me how much of it is due to our current overspending.

From where I am standing I certainly dont see people throwing cash around to the extent it would cause inflation. Certainly not like it was when we were locked down and no one could travel and we were all online shopping and building decks and overbuying toilet paper etc.

Yes I understand if you flood the economy with cheap money it will drive inflation, however we have had cheap money for 10 years and its only in the last few that we have had REALLY cheap money. So whats changed? Covid, climate change, war.

It feels to me that everyone is going through the motions set out in the economic textbooks coupled with keeping up appearances and the frankly draconian tools and system the Govt and RBNZ has to influence the situation, but the line that we need to raise rates to curb inflation just leaves me completely unconvinced.

But then I am just a man on the street.

Governments and Central Banks have been very reckless the last few years - why? Because they have become terrified of recession, deflation and the possibility of debt default.

So, they completely overcooked the COVID response.

Have a look at the significance of the increase in money supply in 2020 - it is quite extraordinary:

https://www.insightinvestment.com/globalassets/images/redesign-images/p…

{kind=link}

There is no doubt that when you pump the system with this quantity of money with little to no increase in the quantity of goods and services supplied within that same system, you are going to have inflation issues.

Yeh that graph is crazy. I am still unconvinced by the RBNZs actions however.

Maybe our base level of consumption has changed and we all need to move it down. Which would be great for the planet but its hard to see the average human doing that.

Id love to see what the average person consumed in 1970 compared to now.

the big issue is the inflation started in housing over 10 years ago but because cpi does not include housing it was mis labeled healthy growth.

the cause was excessive low interest rates which led to there being more money bidding up a finite resource. the lucky punter who got on the treadmill back then has had a risk free gain on the central banks dime.

covid popped up and the govt. threw more fuel on the fire and we had a blow off top in the market.

just as this was unraveling our mate putin decided to invade Ukraine and take 1/4 of oil, gas, grain and fertilizer off the market . not surprisingly this let the inflation genie out of the bottle and the reserve bank had to act.

the theory that low rates stimulate and high rates constrain is their mantra.. however, what has been missed is this inflation is not caused by excessive liquidity, but supply constriction and scarcity.

so we have a wall of debt, constrained supplies, and a bank raising rates at a time when the global economy is under pressure from covid which leads us to this sh#t show we find ourselves in.

given that we have only just erased the gains of the blowoff top, which in investing you look at as being not real pricing, we could be looking at 20-25 % down from the 2020 prices before the end unless the central bank/ govt policy panic and drop rates...

the big issue is the inflation started in housing over 10 years ago but because cpi does not include housing it was mis labeled healthy growth.

Not quite correct. The CPI includes housing costs.

Construction costs and rents yes.

But critically not land values.

nor the secondary market. where properties jumped 15-20% during covid.

Construction costs and rents yes.

But critically not land values.

The CPI doesn't include any growth in asset values. That is why the CPI is a generally incomplete inflation measure. Inflation is measured by 1. Growth in CPI (which in itself is limited) + 2. Growth in broad money supply + 3. Growth in asset values.

Up until the late 1990's land was factored into inflation. It was Don Brash the then RBNZ governor who "temporarily" removed land from the CPI calculation as he would have lost his job if he hadn't. He had stated if he couldn't keep inflation between 1-3% band he would resign.

The Asian financial crisis arrived late 90's and land values fell (which would/could have dragged down the CPI to under Brash's goal).

He said it was distorting and misrepresentative to include the land portion in the CPI calculation because it didnt really reflect the cost of living movement. We were told it was "removed as a temporary measure" and would be added back at a later date when it was not so distorting of the actual inflation rate of day to day living costs...

It has never been added back.

Went to Bunnings yesterday, first time ever that I couldn’t find a park, place was packed. Briscoes next door was packed too as were the cafes. Maybe it’s a mixed bag in different places.

So they are predicting a 4% OCR rise and just 24% house price falls (inflation adjusted).

Who do they think they are kidding?

Markets are becoming attuned to the risk of a 75 basis-point OCR hike'

If Markets are attuned to 75 basis-point OCR hike, to get the desired result should go with 100 basis-point = Shock treatment as will help in future to go slow, hopefully.

Knowing Mr Orr even 75 basis- point will be only if knows that should be 100 basis-point or will be 50 basis-point.

I wish the CBers knew what was going on, but sadly, history tells us they don't.

Bash the economy around the head and then sell voters an aspirin (for your vote...)

This government are orchestrating a hard landing so they can then try to look like a knight in white shining armour by dishing out hollow initiatives to 'save everyone' from the crisis they have created through their mismanagement of the economy.

This will happen to coincide just in time to get a few measly results of improvement before next years election.

Wrong. Things won't have recovered by the next election - if anything they will still be heading south. Labour is toast and the only issue is what amalgamation of crackpots take their place.

Sounds very plausible to me. We need to remember this simple fact. No country, anywhere in the world, has successfully reduced inflation with policy rates materially below the starting rate of inflation. We can look forward to further OCR rises during 2023 and perhaps into 2024. This is gonna be a hard nut to crack.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.