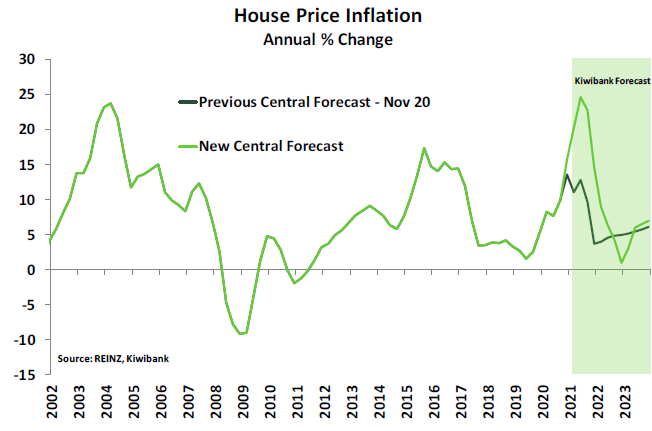

Kiwibank economists say they've "drastically revised up" their projected near term house peak.

In the bank's latest First View publication, Kiwibank chief economist Jarrod Kerr, senior economist Jeremy Couchman and economist Mary Jo Vergara say they had expected house price growth to peak between 12%-15% year-on-year.

"But we now forecast a peak of close to 25% [year-on-year] in the middle of the year before easing to finish 2021 at 14.5% [year-on-year]," they say.

Commenting on the latest Real Estate Institute of New Zealand housing sales figures, the economists said the "unrestrained excesses of the housing market" were again on display in February.

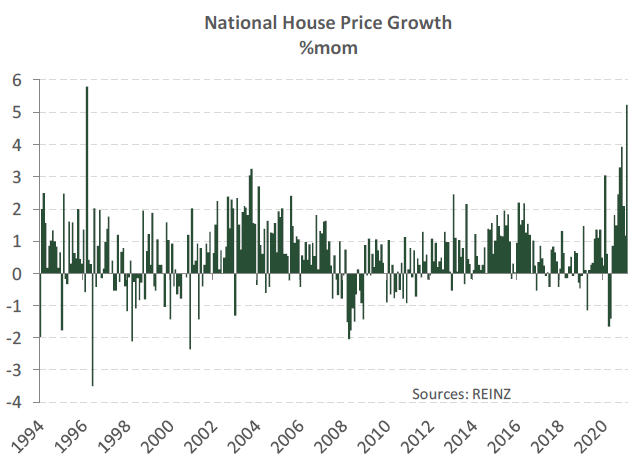

"House prices jumped a blistering 5.2% in February alone. Only one other month on record has posted a higher rate of growth (March 1996 at 5.8%)," they said.

The Reserve Bank has reintroduced the loan to value ratio (LVR) limits as of the start of this month. These include the conditions that housing investors need to have 30% deposits as of the start of March, but as of May 1 this requirement will be raised to 40% deposits.

The RBNZ temporarily removed the LVR limits, which have been around in a variety of forms since 2013, as of May 1 last year in response to the Covid crisis. But the removal of the limits saw high LVR lending to investors go through the roof.

Hence the move by the RBNZ to bring the LVRs back.

The Kiwibank economists say the return of LVRs, with banks effectively applying them from December last year, should take some heat out of the market.

"However, LVRs may not be having as much of an impact on investor activity as previously thought," they say.

"The recent sharp surge in house prices has helped to push up investors' equity on existing portfolios. Equity that can be used as a deposit for additional borrowing."

The economists say "other measures" are needed to tame the housing market.

"...We await to see if the Government gives the RBNZ go ahead to use debt-to-income restrictions on investor related mortgage lending."

The economists do say that "despite the current performance" they do expect house price growth to start slowing over the second half of this year and they are picking house price inflation of 14.5% by the end of the year.

190 Comments

LVRs don't really matter when enough investors refinance their mortgage on increased equity to bid up the price on another property.

In the current scenario, this has created a self-fulfilling cycle whereby investors are using the refinanced cash to pump up the property market, which in turn increases home equity across the board, giving the market more room to refinance and buy yet more properties.

So as long as you're already a property owner happy days. Not a home owner yet or born after the year 2000? UNLUCKY!!! Now shhhh and keep paying me rent and your taxes to fund my non-means tested Super.

"born after the year 2000"

Why would people 21 and younger be looking to buy a house now?

They're not. Point was if you're that young then you have no chance of ever owning a home. Or if you're older than 21 but for what ever reason don't own property yet. For all of you...UNLUGGY UCE!

why not? Kiwis have it rammed down their throats from an early age that houses = wealth

Many 21 or younger don’t even care, it’s irreverent to them, maybe talk to them about royal family or “likes” on their social media.

Ok. So lets just say born after 1990.

it is happy days only if you own 2 or more houses. If you own one house - in best case scenario it is flat for you , you will start feeling the issue once you want to upgrade or your kids need their own place. But you will be supposed to feel wealthy :)

You'll still feel and will be increasingly wealthy compared to those that don't have a house. Wealth is relative and it appears to me that our society is being split further and faster apart than ever before. Young people should leave.

Yeah stop 'whinging' it was hard in my day too /s (total crap. My parents bought in their 20s a 3bdrom on dad's factory worker income)

But he bought a house that wouldn’t get consent these days. It also likely fit the definition of unhealthy by today’s standards and was probably an hour/day commute from a city with a population (back in the 1920s) roughly the size of Palmerston North (today).

Homes within an hour of Palmerston North still aren’t that expensive.

The point is that you could buy a house anywhere at 3x median household income, which back in the day was only one income earner. Now Auckland is at 10x, the rest of NZ at 6x, and the household income now, more often than not, is two income earners.

Rubbish. Its a beautiful sturdy home 25 mins drive from Wgtn city and now worth 700k

.. No now worth 750k

It's been roughly an hour since you've checked homes.co.nz, quick go back on...it's likely now $775k. Ask your parents what it's like to "feel" wealthy.

Lol.. I'm sure if dad were still around he would be more likely to complain about what the price is doing to his rates bill than feeling wealthy

Assuming your parents bought 40 years ago. The population of Wellington back then was about 100k (https://ecoprofile.infometrics.co.nz/Wellington%2BCity/Population/Growth), a city of comparable population today would be Dunedin. How many times the median NZ household income does a house 25 minutes from Dunedin cost? Adjust for increased cost due to regulation and taxes (GST to build new) and how much has it really inflated?

He means they were in their 20's age wise. Not 1920's.

Yes that's what I meant

Please don't push the tired false narrative that the younger generation want brand new, dry and warm mansions in the central city. Willing to guarantee that 99% of first home buyers would love an uninsulated 40 year old draughty starter home that requires a tonne of work at 2 - 3 times their income. Unfortunately investors love these properties too for value add potential, and thanks to equity many don't need to save a single cent to purchase one.

It's a very boring, irritating and untrue narrative. The kind of crap that Tony Alexander peddles.

"But they must want them, because when I drive around all the new subdivisions I see McMansions with Ford Rangers and boats, why in my day we paid for a house without floor coverings and a driveway. The garage came later.".

dago...back in the 80s and 90s almost anybody who had a job and was not a solo parent or had more than 2 kids could buy a house in any city in NZ if they really wanted to. With extortionate rents and low income wages being forced down by the availability of foreign labour, very few can now buy a house in a NZ city without the help of Mum and Dad.

Housing market hyperinflation...to infinity and beyond!

Adding up last year's increase, so it's 40% increase in two years. Better start preparing a hard correction now.

There will be no correction, Govt. have already guaranteed it.

lol, do you really believe in a labour led government? That's really funny.

This is the qualifications of our Minister of Finance!

– studied political studies at the University of Otago, graduating with a Bachelor of Arts with honours in 1995.

– His honours dissertation studied the restructuring of the New Zealand University Students’ Association in the 1980s.

– joined the Ministry of Foreign Affairs and Trade in 1997 after leaving university. His overseas postings included the United Nations in New York. Robertson also managed the NZ Overseas Aid Programme to Samoa

– worked as a Ministerial advisor to Minister for the Environment Marian Hobbs and later Prime Minister Helen Clark.

– left the Prime Minister’s office to work as the Senior Research Marketing Manager for the University of Otago based at the Wellington School of Medicine.

Jacinda’s only job outside of Govt was as a teenager in a fish and chip shop. These are the people running this country.

They probably don't have a clue what is happening right now! Jacinda even said that she like to see a small increase of housing price every year since most of people's wealth are in properties. Did she really know what she was talking about? I don't think so.

Better she would have supplemented her experience in Fish & Chips only, not how to rule/ruin a nation.

It's not what you know, it's who you know.

"They probably don't have a clue what is happening right now!"

They do.

But they and, the rest of their bureaucratic class, haven't got a clue what to do about it.

Or rather, the courage to try a different tack.

They all went to the same finishing schools and learned the same failed economic doctrine (You know. The one that got us right here, right now).

All they can try to buy, is time. The most precious commodity any of us don't have the capacity to waste.

The bureaucracy is hardly known for courage and creativity!!!

Gold mate !

Also, did you know Clark Gayford owns property in Gisborne where Cindy is originally from ? And also HB. Nice little tax free earners I bet with both regions leading the price gain charts of late.

What's the bet that's really Cindy's IP having grown up and known the Gisborne region.

GAYFORD, ANTHONY CLARKE Newcastle Street Mahia Hawkes Bay Owner

GAYFORD, ANTONY CLARKE Salisbury Road Awapuni Gisborne Owner

Is that so? Clarke sure has his fingers in alot of pies

That is a complete breach of privacy and I hope the moderators do something about this.

I don’t care that it is on a public list or whatever source you got it from it is very poor to post that on here addresses and all

I think the public deserves to know....and yes that is why public registers are important

Disagree. As the electing body, the people of this country (and all democratic nations) should be entitled to know everything about what is going on in government as well as everything about the people who are in government (within reason). Conversely, they shouldn't need to know anything about us (again, within reason). If you don't like it, then you don't need to be a public figure - nobody is forcing you. How can we the people hold the political class to account when we don't know what is going on?

The unfortunate dilemma we find ourselves in is that the government and politicians seem happy to hide as much as the can from the public, whilst at the same time, trying to gather as much information about us as possible.

I should note that I'm fairly sure I heard the above (I'm paraphrasing obviously) from an interview with Edward Snowden (who we should all consider a hero) and I happen to agree with him completely.

If he wanted to keep his name private he would have bought using a Trust. Disseminating publicly available information in a public forum is what media is for?

Why would he have made the information public (by adding it to the publicly accessible land register) if he wanted the information to be kept private?

It's not a breach of privacy if it's publicly available information.

Even if it’s legal it doesn’t seem right that kind of information is made public he should have the right to keep that private

He could put them in a trust if wanted them to be private right? He obviously doesn't care.

ld..there may be a case for the address of your private residence where you live to be made public but......

It is like revealing the prime minister's salary. It is public information so hardly a breach of privacy

Please be careful about adding one and one and coming up with eleven. Clarke Gayford grew up in the Gisborne area and has family there. Jacinda Ardern did not; she grew up in the Waikato region.

It is always revealing when anecdotes are jumped on, to support a political conclusion before basing them on facts.

David...so do you know, is it Jacinda's partner who owns these places or not?

Exactly. Never had a job on the tools.

True 'company of heroes', but to be fair he may have also gathered a few tips from his father which might prove useful in his finance role because in Grant Robertson's wikipedia page the following is noted: "In 1991, his father was imprisoned after stealing around $120,000 from the law firm he worked for." Look it up for yourself if you doubt this little gem.

Fortunately(?) the government doesn't have a brilliant record of keeping their promises.

If there is no serious talk on immigration in the next few months and it is looking like a return to the mass immigration of pre covid I think I am going to look for a rental. And if I do buy one I will be telling my tenants that I will never increase the rent and not coincidentally I will probably always be paid on time, only be asked to fix stuff when absolutely necessary and be unlikely to see my investment carelessly damaged.

I think they will start talking seriously about immigration soon. When it comes to fixing the housing crisis It is always good to pull a bit more time talking about thing which won't help

andreas... I am not so sure but we will see. I think Jacinda probably has very open borders/global village attitudes, there are some strong and politically powerful vested interests ie landlords and business owners not to mention her desire to build her international image for her own personal gain in the future. It all depends whether she is prepared to throw our poor people under the bus and I think she might be.

You and every other investor will be looking for more rentals. And of course those 70,000 people coming into the country might be looking for a home too...

The last rent change I made for my tenants was in 2015 when I put the rent down.

lh.. good on you for not putting rent up. You are one of the few who don't gauge every last cent they can. What is the story with the A Zeneca vaccine? Is it safe? I have read conflicting stuff recently.

Good, you’ve finally seen sense

Scary times when to see sense you must join the insanity.

Why exactly would you need to do this? You mentioned elsewhere that you bought a house with cash previously. You'd still almost certainly be taking a ridiculous portion of your tenants income to benefit yourself for many years regardless of whether you increase it over that period. Notice that you list as one of the upsides of this, that your tenant would likely only ever ask you to fix things if they absolutely need to be addressed. Don't you see the issue with that? They might be too afraid to come to you for fixing things as general maitenance that should be your responsibility and not theirs, for fear of you resenting this and therefore increasing the rent on them.

As soon as you step into that role, your interests are quite opposed to the interests of your tenants. Despite stating that you wouldn't increase their rent, you still expect something in return for this - that they don't bother you with anything that needs fixing unless it is absolutely necessary. They could insist on their rights under the act, but you could always increase their rent. It's still exploitative with the balance of power in your hands.

The RBNZ has created the perfect conditions for housing speculation.

In Jacinda's own words her Government should 'go hard and early', any minute they don't is a treason to their own people and significant amount of voters who supported her.

This is what adds to FOMO.

Unless Jacinda Arden and Mr Robertson takes a firm stand and take meaningful action, this housing Pyramid will keep continuing as Mr Orr has made it clear that it is not his concern.

So now Mr Robertson, your announcement this week has gain more importance and will depend upon, if you put a full stop on Interest Only loan or not. CAN VOUCH THAT INTEREST ONLY LOAN ARE STOPPED LOT OF SPECULATIVE ACTIVUTY WILL STOP AND IT IS FOR THIS VERY REASON NO ACTION WILL BE TAKEN ON INTEREST ONLY LOAN.

Wait and Watch.

Second step that can be taken after stopping interest only loan is DTI and can very easily have two parameters just like LVR, one for FHB and another for so called investor (should not be a problem in implementing as mentioned by some with vested interest)

Wait and Watch

Sorry.. but word on the street is the announcement will be next week, and we know..and speculators are seeing, 'next week' never comes (until it does!)

IO loans are a small tax break investors use to ensure debt against IPs remains as high as possible while paying down the non-tax deductable debt on their OO place. It won't change much.

Banks don't test income on IO basis, actually it often gets investors in trouble if they stay with the same bank as IO is always a short term set up then when principle needs to be paid they do the math on the remaining term (eg 25 year orignal, first 5 years IO, PI will start being paid on a 20 year term - unless they switch banks and reset the clock to another 25-30 year term, with the first 5 years being IO of course).

There is nothing to stop the government basically placing a freeze on new Interest Only loans for investors and introducing a DTI. This would have a massive impact on peoples ability to leverage up to speculate on housing.

Do this at the same time publicly stating the goal of the government is to at the very least stop house price appreciation completely, you would tilt the balance back towards FHB, and reduce the wild FOMO.

It won't fix the housing crisis - that will actually require more houses (or fewer people to live in them). But it would at least put the brakes on the wild speculative behavior that has taken hold.

little, you say wait and watch… this hasn't paid off has it?

Kiwibank still trying to talk up OCR? The squeeze must be painful.

This is typical...one day the news is that housing market has peaked and the next day that will rise and than another will be down than up...keeps continuing.....GIVING POOR FHB A ROLLER COSTER RIDE AND GOVERNMENT TALKS ABOUT MENTAL HEALTH.

Long Live the Queen ....who has got absolute power to solve but instead is promoting and supporting by her action and inaction.

Terrible for the young people. How dare Jacinda even talk about mental health..she has no credibility looking concerned or frowning about anything, such as mental health, suicide, Australia sending people here etc. The worst kind of revolting hypocrisy I've ever seen. Why so many young love their Dear Leader? Maybe they love to live in windowless mouldy flats with the chance to work till they are 75.. Surely not

The future is uncertain, discourse from various parties in the media helps to develop your own position.

If you want homogenized media to save your precious mental health, move to China.

There is no point for new UNI passouts and renters to stay in this country, they will struggle and will get nowhere. There life will be wasted paying rent (biggest expense) and taxes to support long term beneficiaries.

I know lot of professionals (bright minds) started looking to migrate, this country only respects property investors, not the one who work hard to build the nation.

It's better to move across the Ditch before they stop accepting Kiwis, if that happen you are stuck.

Indeed, New Zealands unwanted generation. The kindest think to do would be buy them a one way ticket.

I used to think that so I went away and spent more than 10 years in the UK and Australia. But when it comes to starting your own family there is no better place than NZ. They will be back.

But when it comes to starting your own family IN A GARAGE there is no better place than NZ.

If you can't afford private schools you need to get out of UK and Aus and back to NZ pronto. The UK is cooked, Brexit is a disaster and selling a central London house will barely get you into a mid-tier Auckland suburb these days.

You can do that if you want to buy a shelter with insane price and than working crazy for years to pay the Debt.

In return what you will get here other than low standard education, no business opportunity, low pay packages and damp & cold whether.

https://www.nzherald.co.nz/nz/foul-mouthed-aussie-businessman-rants-abo…

Well I don’t agree with him on the weather as we have had a cracker summer with day after day hot and sunny but the lack of pretty women is accurate. That’s why you should always import a wife if you’re a kiwi.

What an entitled misogynist. Referring to women like they are just objects that you should import because the local ones aren't up to your standard. Makes total sense when you clearly view other people as mostly just a means to an end.

Pretty much sums it up - people are a commodity to some

Oppposed to misandry and hypergamy. So what if a guy imports. Quiet desperation obviously forgot his soy milk..

I'm opposed to the objectification and demeaning of people, regardless of their sex. Treating other people like commodities is pathetic. Of course you would assume that I'm a male. I am a millennial though and I never forget my soy milk. Beats consuming bovine growth formular meant for calves as a weaned human adult.

Has it occurred to you it works both ways and some male 'imports' find a good kiwi lass very exotic.. They think they're in heaven and found Rachel Hunter

Yes and no. Education here is fairly good, in general, and compared to Aus and the UK.

But the cost of living is horrendous, which isn't great when you've got several mouths to feed.

If you are well off, then I am sure NZ is amazing.

Every country in the world can be amazing if you have the money, but of course in many countries that will also mean your as corrupt as and in government or part of a drugs cartel.

"There life will be wasted paying rent (biggest expense) and taxes to support long term beneficiaries."

Not all landlords have been doing it long term

Touché!

"...We await to see if the Government gives the RBNZ go ahead to use debt-to-income restrictions on investor related mortgage lending."

Perhaps Grant is finding it hard to grab any free time to get this going – what with never ending meetings with Jacinda to ensure their lack of action spin is in sync, along with every day having to write out a cheque for $1 million to cover emergency housing and then another for around $6 million in accommodation supplements – really, where does the day go?

they won't , or the DTI will be like 15 years of income , otherwise it will seriously correct the market which they don't want to do

Actually, thinking about it – I don’t think they’ve ever really clearly stated what outcome they actually want when it comes to housing – there’s been some ill-considered waffle but nothing succinct or definitive.

How can you have and articulate a plan when there is no clear desired outcome.

Is that their problem.

EXACTLY!! , in order to fix the issue you need to come to the Definition of what the issue is. No one for now expressed the definition of issue as "HIGH HOUSE PRICES", the issue has always been articulated as "UNAFFORDABLE HOUSING" which means if you put the OCR down you make it more AFFORDABLE to enter your own house and service the dept. No one cares of how long and how many generations will be paying off the dept. No one cares what quality of the house you will be living in.

There are international definitions of what affordable housing is eg 3x median income multiple.

But what happens is the politicians, and the MSM like to redefine words so what was 'unaffordable' yesterday is 'affordable today', what was a 'crisis' yesterday is a 'challenge' today etc. etc.

Definition of words matter as does the context in which they are used.

DTI will not have as much affect as regulating, if not stopping Interest Only Loan.

How will stopping IO loans impact prices ?

Do you know why accountants set these up in the first place ?

Banks have already crunched the numbers on PI over a fixed term eg 25-30 years, and at test interest rates of 6-7% far higher than they are now. It won't effect the amount someone could borrow by much at all, it will actually lead to slightly higher net profits and slightly more tax being paid as interest they can deduct reduces as principle is paid off.

Currently you own a property on P&I, buy a second one and shove all the debt on the first one interest only and rent it out. End up with lower or same payments but 2 assets and more leverage. House price rises and you use your equity to buy another one. Never have to pay down principal on the investment properties. Rinse and repeat.

The RBNZ sure knows how to deliver stable prices.

'Kiwibank economists see 25% house price inflation'

Hi David,

Can you please advise if it is after officaly 19% rise plus 10% ($100000) rise in february that is appox 29% rise.

So we are looking at 29% plus 25% = 54% rise by middle of this year or OR is this just to create news /FOMO.

As I see this is not news as house prices are already up between 30% to 50% in a year and this also confirms that Kiwibank economist knows that government is not going to act on speculators to controll the shooting house price and Mr Robertson is just playing with time and has no intent of controlling the pyramid - Real Shame

You are absolute correct.

This does imply that Kiwibank is privy to information that no one else is and is that government has assured them that will not take any action to control the ponzi and niw by inaction will support and promote the pinzi - earlier supported by taking action and niw by their inaction.

They say 25% by the middle of the year. That 25% is over 12 months, so most of it is baked in already. Effectively they are saying some small rises through to the middle of the year then static in the second half of the year.

So by the end of this calendar year prices would have risen 30-35% over 2 years if Kiwibank are right

If prices trot along at the tame 14.5%, they'll be 104 times average household income by 2040.

THIS IS FINE.

Stop being cynical, if young adults in 2040 forgo lattes & smashed avo for 1,425 years they will be able to afford a house.

Quite right. Less smashed iPhone on toast and new avo every year.. sky subscriptions.. foreign holidays.. etc. etc.

Some boomers would happily eat their own children if it meant one more investment property added to their portfolio. The mainstream media has a huge role in promoting this insane, absurd and extremely dangerous idea that everyone has to become a landlord "to get ahead".

To many kiwis if you have a portfolio of rentals say 4-5 then you're 'successful'. Even if they're all bought with debt backed by paper wealth equity that can as easily erode as it was created. But hey John and Jane seem to really be doing well...Have you seen the new Ford Ranger they bought (with more borrowings) wow.

I see KiwiBuild houses in Papakura advertised at 575k currently. Would they not be good to buy if you were eligible?

For an average couple earning $43,500 each with a 10% deposit, let's do the math:

Earnings, each, after student loan and kiwisaver (3%): $2,721.68

Mortgage: $2,152

Manageable, assuming they're both working and 2.89% interest. It won't be fun.

If they decide to have children and (god forbid!) some time off to care for the new born, poverty.

If one of them loses their job, poverty.

If interest rates go to 7% ($3,443 mortgage), it's poverty.

So the answer is - it depends. Historically, no it's f$#%ing madness. In today's climate, you're in the precariat anyway so why not?

But if they're juniors on $43,500 with a student loan then they can also expect their salary to increase fairly rapidly over their first 5-10 years of working. Also the student loan will eventually be paid off.

ok - drop the student loan and assume they're not university educated. Which would be "more" average I think.

Either way, it's not pretty and leaves them living on the edge for a long time. Especially with kids.

Wouldn't we be a healthier society if the mortgage was half that amount? Totally achievable with sufficient housing supply.

I think you really need to base the calculation on what you can afford now and dismiss the worst case scenarios. Cross those bridges when you come to them.

Having kids is a worst case scenario?

ok boomer..

Well, you shouldn't be having kids if you are on 43k. However when the time comes you will be earning more and there may be WFF assistance as well. Things will have changed by the time you get to the bridge. For me I went on call and was offered a lot of OT. I didn't plan for it, it just worked out.

‘You shouldn’t be having kids if you’re on 43k.’

Do you really not hear your arrogance?

Aroha

How is this arrogant? This is the most sensible comment on here. I earn $80k, work long hours and am 32yrs old. I am waiting to have kids till mortgage is down abit. Id love to have 10 kids but why should taxpayer pick up the bill?

I'm not a fertility expert, but don't wait too long.

https://www.babycenter.com.au/ims/2020/09/infertilitygraph-ER.png.pages…

{kind=link}

Not an arrogant strategy, just an arrogant comment. It avoids the question of how we've got here, whether its right and how we fix it as a society and instead simply removes the right for young couples to procreate unless they earn over a certain threshold. All from the place of not having had to face the same dilemma.

It is difficult or nearly impossible to increase interest rates up.

NZD against USD is over 72c, over 15% increase after the pandemic.

Let's assume RBNZ declares OCR 3.0% then the commercial mortgage rate hit 7%.

That will add at least add another 15~25% increase on NZD, pulling it close to 90c against USD.

Don't think we can allow that and kill the export market completely.

Jay Lim..first of all nobody in NZ has total control over the OCR. Secondly our dollar was 88c vs the USD quite recently and the world of exports did not fall apart.

Yes there are some good Kiwibuild buys. Many of them have ballots though, so it's a lottery.

It’s literally winning the lottery. The market value is way above what they will sell them to you for.

"The recent sharp surge in house prices has helped to push up investors' equity on existing portfolios. Equity that can be used as a deposit for additional borrowing."

YES, these theory/book based economists can only see hse prices ever going up. But, no worries, as they know/guaranteed if prices head south, BAILOUT would be there.

A 1% increase in house prices on a portfolio of 40 or more properties gives an investor enough additional equity to purchase another property.

40 properties in Taumaranui is worth one property in Auckland so yes sell them and come to the Golden Triangle. Or vice-versa sell one ten million dollar home and become a mega landlord in the sticks..... lots of hard choices

https://zensecondlife.blogspot.com/2021/03/fake-recovery-max-pain-trade…

Of all of the massively overbought and overbelieved fantasies in this era, none will be more painful than the falsehood of recovery now being spun by global central banks...

As a property investor I welcome these "moderate" price increases Prime Minister Jacinda Ardern is delivering. The governments fair and balanced approach to housing is delivering outstanding returns to investors, far higher than any other government historically. It's sad to see so many who begrudge our new national 'industry'.

Stunning and brave

What's the point in pretending? The young people idolise our Prime Minister. Michael Gove summarised a change I missed when he said "People in this country have had enough of experts" and he was right, we live in an era of political personalities where we are post-truth. It doesn't appear to matter how much quality of living is improving or declining, taxes rising or falling, houses being built or decaying. Sewage can flow down Wellingtons streets and into the bay, people are acquiescent and accept it as a new normal. It costs far less to hire a PR expert to manage the messaging than a team of civil engineers, surveyors, digger operators, pipe layers etc. to fix the problems.

Our thinking about governments being effective and Prime Ministers leading is old fashioned and dated. We need to move on and understand the world the way it is, not as we'd like it to be. :-)

Who is Michael Gove??

The only Michael Gove I know of is a UK politician.

UK cabinet minister and one of the key Brexit cheerleaders in the lead-up to the UK referendum.

Also known as "Cockweasel".

He is a four eyed git who stabbed Boris Johnson in the stomach.

he must be one of the many thinking the same

They idolize Ardern while they are young enough to not understand what these mental house prices mean for their future.

Of course some of them are little Gretas - virtue signallers with rich mummies and daddies who needn't worry.

KIA KAHA ❤❤❤❤

Orr lifted LVR immediately upon covid with just 7 days consultation, despite claiming housing was not in his mandate. Covid was just a perfect excuse for banks and specuvestors to pump and dump real estate like its 2008. Have my popcorn and bubbly on standby

Maybe Grant Robertson will get around to announcing a meeting about having a meeting about doing something by the end of 2022.

Where is the "financial stability" Adrian?

Don't worry. A working committee will be convened. And look over there! It's a climate emergency!!

If the Tooth Fairy and the Fat Controller elect to do nothing, they damn their core voting block to further damnation via endless rent increases at the interests of global banking owners. Speculators are just the banking sectors risk proxy. Perhaps tax payers will just continue to be bleed dry with wff and emergency accommodation.

Will they, can they actually show some leadership in the interests of he average man and woman in NZ, or will they be the biggest left wing sell outs in NZ's history?

Immediate ban on interest only, and and an introduction of DTI for investors at the range of 6-7x or bust. Speculator medicine https://www.mypharmacy.co.uk/product/pepto-bismol-liquid-120ml-240ml-48….

Should be 4-5x not 6-7x for the DTI. The UK has it at 4.5x.

That wouldn't even be "bold" action.

The Tooth Fairy and the Fat Controller have indeed been busy... and that's helped rents to jump higher. One hamilton rental is increasing by 150pw from a low 300 up to 500. Reason given was the landlord has to cover the increased costs... well what a surprise

Is that the soon to be demolished house that the (developer) landlord has to either leave empty or pay to bring up to healthy homes standards whilst awaiting council consent to put 8 town houses on the site? Poor fella tried to increase housing supply and got demonised for it. The stuff article mentioned that even after the rent increase to cover the cost of improvements required (which had to be recovered over just 1 year due to scheduled demolition) that property was still being let for below market rates!

I read the article on that example you are using band the rent had been underpriced for years and years so the $150 increase has to be taken into context

With toxic mould from structural rot known to permanently impair and disable humans with organ damage and severe window leaks and illegal conditions it should be under market rent. In fact the NZ taxpayers are paying the cost to support the childrens illness and the parents ill health. Kids have died from better housing mould conditions than that place. Complete lack of basic maintenance for decades should cost any asset owner as the leaks only get worse with complete disregard for the health of the asset (knowing the landlord does not even care about the health of humans in it they should at least care about the asset but in this market human life is the lowest concern, followed by building structural health).

Well said. From memory there were no extractors in the kitchen or bathroom either. They were intending to demolish the house at some point and did not care at all that they had any obligation to provide a safe environment for their tenant.

Too much global debt. Central banks have decided to inflate it away via printing. How about Mr Orr fronts up and tells the public, clearly pointing out who will win from this and who will loose.

Instead we get BS. I am sick of the dishonesty and lying by our leaders.

Inflating Debt Away only works if income rises to meet the payments due on the Old Debt (which stays contained).

If either Debt is created faster than income rises (Old Debt is just replaced with New Debt) or incomes (wages) don't rise ahead of the Debt Repayments, then all that happens is the Debt Load overwhelms the capacity of the Debt Donkeys (that's you and me) to Inflate it Away.

(NB: in the 70s, when this policy was last tried 'successfully' wage demands of +30% swamped the World, and were granted. That was possible because the Western World still needed productive workers. Today, it doesn't, and Asset speculation by the unwashed masses was virtually unknown, so they didn't go out and borrow as we see it today. )

that is the thing , the "income" is actually rising , but not wages - by "income" I actually mean unrealized equity investors can use as a deposit to by another house. Hypothetically this can go if not forever but for a very long time , because with every surge in price - investors can use more equity. The net result of this will be super asset rich (but cash poor) investors and cash-"rich" wage earners. As we see the core inflation is not going up that fast so the wage earners still will be able to buy a lot of stuff from the supermarket, but will never be able to afford to buy a house. This is the divide. No one is actually starving , but part of the society will never be able to live in their own houses.

Jumping on a few months data to project for rest of year.

Every month the banks seem to revise the % growth rate for rest of year.

No % guesstimates will hit the mark

Who's guesses do I trust more... yours or theirs? Mmmm...

It’s the same with all official targets. They are never hit. The only people to hit their targets are the banks, mortgage advisers and others selling debt/loans.

A buy to let mortgage is needed in this market at 2 base points above any offered rate. DTI is common sense but it needs to be net pay, not gross pay. We need to factor in other expenses also (rates, bills, food, dependants, etc) and there should be enough evidence to baseline this. Existing loans should be a red flag regardless.

I'd like to see the 2 base points for investors offset for first home buyers. In this market if would effectively give FHB a 1 year fixed of 0.25 if the total loans were a 50-50 split. Stamp duty on second properties also offset for FHB making the deposits less...

I'm sure we all have other and varying suggestions to help solve the housing issue. But one I really would like introduced is where new property developments are ring fenced for state housing with long term occupancy resulting in an opportunity to buy factoring in a percentage of the previous rent paid. Surely if we allocated even 5% of new builds to state housing in the past year we would have a indication if a long term solution.

How is all this"sustainable" anyway? Salaries don't move at 10 - 20% a year.

I think thats the hardest thing to get your head around. House prices are not linked to your Salary. House prices are linked to what someone is prepared to pay for it. The money is clearly coming from "Somewhere" because prices are still going up faster than wages.

Falling interest rates and people using equity in previous property to buy more properties (ponzi characteristics).

Fine on the way to zero interest rates - then a world of pain if rates rise.

Watched the latest George Gammon video this morning about Michael Burry thinking hyperinflation could be on the way...what a time to be alive. America turning into 1920's Germany with destruction of the USD.

House prices are linked to banks offering cheap credit which enables people to 'think its worth xyz' because every man and his pet bunny are jumping into outbid. People need to realise the only reason house prices are completely detached from wages is the cheap credit..and interest only house loans. As previously stated, once banks have had their fill of increasing their asset ledger..no more lendy-lendy. Time to pay-pay

Simce last two weeks everyday have news on housing ponzi, has Mr Robrrtson or Jacinda Arden or anyone in govetnment has come out and spoken........

Ignoring to support the ponzi or are too ashmed (seem highly unlikely as are shamelessly too thick skin %) @$&) to respond.

Corina virus has been a blessing for such politicans who are running a country such as ours to hide, avoid, deny and lie to manipulate the situation to serve them.

Debt based Ponzi scheme will be sucking in a few more “customers”. Lets look for some great fomo articles in the press over the next few days. Just remind me again what happens when we get inflation, or hyperinflation and wages don’t keep up. People cut back in other areas of expenditure, reduce their mortgage payments (this has already happened), don’t visit the dentist, buy stuff at Briscoes, cut back on travel etc... This effects local businesses, jobs and increases the likelihood of rising unemployment. Interest rates may stay low BUT in an inflationary environment expenses go up and this aspect is not being talked about.

Found one.... It never happened before and so it will never happen in the future Thanks NZ Herald. https://www.oneroof.co.nz/news/39125

Nothing to see here.... move along and "keep taking on debt and we'll reward you by putting up interest rates." said J Powell this week.

I think I finally have to admit that the problem is now to big to solve. Its been simply ignored for decades and house price increases are seen as a success story now. Its a mindset now and its not going to change. The successive governments didn't care when they finally got into a position to actually do something they reneged.

The problem is going to be resolved - in the most financially painful way imaginable.

Those like Lex Greensill are just the very public face of a much wider problem that the New Zealand real estate 'market' is not going to avoid.

A little over a decade ago, the global economy was left teetering on the brink of destruction after the world's brightest minds applied their talents, not to exploring the realms of the universe or ridding the world of disease, but to create ever more elaborate means of gambling. The asset was a shaky boom in American real estate. … complex investments all conspired to obscure the extent to which debt had permeated the system, until the system cracked and then crashed.

If anything has changed since then it is that there is vastly more debt at household, corporate and government levels...vast trillions of dollars in stimulus coursing through the financial system and interest rates at zero..

https://www.abc.net.au/news/2021-03-08/lex-greensill-fall-from-grace-co…

Carlos, it’s because the entire monetary system across the world is a debt based ponzi scheme. If any central banker anywhere in the world fiddles with his magic toolbox too much then the whole thing will come crashing down. Once the first domino falls it will completely destroy the system. Think 2008/9 was bad? With the amount of debt now in the system it will cause a massive reset of the global financial system.

Sure I can relate to that my my question is always the same, WHEN ? The USA is giving away 2 Trillion. Its sounds a lot but it is peanuts, $1400 each and that would probably not pay your rent here for 3 weeks and then your back where you started. All very well making a prediction it will crash, sure its going to crash but when ?

I remember people saying it was all coming down back in the 1980s.

Hi Carlos, It's very difficult to say when it will happen as nobody knows. I believe that we are in the final stages of a CRACK-UP Boom. It started at least 50 years ago when Gold no longer backed the US dollar. This is why Zachary's comment is correct as are the commentators who have been on the receiving end and had massive wealth creation through these policies. It can never end, or can it?

Central bank policy has been to facilitate as much lending to as many people as possible, with the occasional injection of inflation to inflate away the debt and increase asset prices to the levels we have today. We have also had healthy business cycles where people and businesses went bankrupt. Yes it's horrible but it happens. As we near the top of the crack up boom no one wants to allow bankruptcy's and they are put off for as long as possible and often especially with businesses they are offered more debt to get them through or restructure the business. This can sometimes work but if it doesn't then the business is left with even bigger debts that it can't pay off. What is a lot of this debt backed by? Yep Your House. So we've moved from a gold backed currency to a housing/debt backed currency. If you want more money you get more debt. If you want more debt you have less money.

This is a definition of a crack up boom:

"The crack up boom develops out of the process of credit expansion and resulting distortion of the economy that occurs during the normal boom phase of the Austrian business cycle theory. In the crack up boom, the central bank attempts to sustain the boom indefinitely without regard to consequences, such as inflation and ASSET PRICE BUBBLES. The problem comes when the government continuously pours more and more money into the economy to give it a short term boost, which eventually triggers a fundamental breakdown in the economy. In their efforts to prevent any downturn in the economy, monetary authorities continue to expand the supply of money and credit at an accelerating pace and avoid turning off the taps of money supply UNTIL IT"S TOO LATE"

The question we all have to ask is at what point is it too late? Or, do you think that the Central Bankers can keep the game going through your lifetime.

Hi veryinterested, sharing what posted in another article...New Million Dollars Beggars Created By Jacinda And Robertson

Credit goes to Jacinda Arden to create a new breed of beggars - FHB with million dollar

https://www.newshub.co.nz/home/money/2021/03/first-home-buyers-resort-t…

Kudos to Jacinda and Robertson for jointly achieving a feat of creating new breed of beggars - FHB who with money are going begging for a house.

Hi taimaiakka0

Thanks for sharing the link. Another great example of extreme Fomo which could indicate we are in a crack up boom.

Carlos67...nobody can tell you that with any certainty at all.

Yeah I agree. At some point we will have a crash, or at least a 'correction', but that will only bring prices down to 'insane' from totally insane. And then the whole nonsense will start again. Can't lose with property mate (50% sarc, 50% not sarc)

Grant still mulling

https://www.newshub.co.nz/home/politics/2021/03/deputy-pm-grant-roberts…

Whenever this gentlemen by the name Mr Robertson wants to delay or avoid responding comes up with :

1 : Waiting for more information

2 : Waiting for advise.

AND this when everything is out in public domain.

Last week was asked about rising house price and his response : Waiting for advise....really...

Interesting how couple of OZ banks started being hawkish.. eg. Westpac, ANZ cautioning about the sky high property values in NZ, with the private debts that goes with it, and recent graphics also in this Interest.co.nz site showing that NZ just second to the top one/Luxembourg. But yea, the local/Kiwibank seems a bit more upbeat, surely as one of those local Bank championed by Lab govt. - So? nothing to see folks, go leverage mortgage to the neck.. good time still ahead for sure.

This extremes by frustrated and desperate FHB may end up badly unless Jacinda Arden comes down from her hibernation on the issue :

https://www.newshub.co.nz/home/money/2021/03/first-home-buyers-resort-t…

Why are they testing patience of average Kiwi and FHB....Is she waiting for violent retailiation....if it continues the way it is, that day is not far away and the responsibility will be on Jacinda Arden

I respectfully disagree with Jarrod Kerr, I am seeing early signs of the housing market losing steam, I believe the rate of price increase is about to go down. (please note I did not say house prices are going down or crash)

So you're saying it won't keep increasing 20+% per year? Truly groundbreaking prediction

How anyone could ever think house prices could continue to increase even at 10%+ a year for any prolonged time while wages increase at 1 or 2% and our income to house price ratio is already at 10 is beyond me.

Yes it is

Yvil... if only I were as smart as Ashley and Tony.

Isn't that essentially what he's saying?

That the big gains of the last 6 months will start to slow for the balance of this year, and especially the second half of the year.

If economists were forecasting a 25% drop the RBNZ and the govt would have both stepped in already. It is completely ridiculous that what would be considered a 'house price crash' would only take prices back to a month ago.

When will they cotton on to the fact such a change in any direction is equally as bad.. we have just had the equivalent to a house price crash to non owners.

The short answer is that they don't care.

Whinging on the internet is going to change nothing.

If you have the ability, leave, there is genuinely much more opportunity overseas.

This country has a very dim future ahead.

Agree as politicans are thick skin #$#@ and as of now one of the most corrupt in thinking and manipulation is current government - power corrupts

You're forgetting how good the wealth effect is ...

Hahahaha pop

So we're still waiting for the proverbial "greater fool" to step up, borrow and buy with capital gains dollar signs in their eyes.

New Zealand's mortgage market ballooned to about 95% of GDP according to the RBNZ in 2020, up from just 51.4% of GDP in 1998.

95% of GDP!!!!!

We're departing controlled flight.

I think it will be good to get out of the country ahead of vaccinations and get the vaccine overseas. For the young and able who are category 4, are last in NZ. By this time there will be a massive line of people heading for the airport, ticket prices will rise, accomodations overseas etc will all rise. For the young kiwis who flood to Aussie the best jobs available will go to the first and best dressed.

Best to be ahead of this looming traffic jam if you have the means.

Pathos... do you realise how few people even consider stuff like this when trying to work out what will happen in the future?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.