Summary of key points: -

- New Zealand’s economic performance grossly misrepresented

- Expectations of interest rate cuts in Australia dramatically change to rate hikes

- US economic data weaker, as expected

New Zealand’s economic performance grossly misrepresented

The Kiwi dollar posted its largest weekly gain since early September last week, appreciating from 0.5600 to 0.5740. The NZD buying prompted by a RBNZ monetary policy statement last Wednesday that was not as dovish on the economic and interest rate outlook as the markets had been expecting. Without stating it explicitly, the RBNZ inferred that the monetary easing cycle had come to an end with a cut in the OCR interest rate to 2.25%. The local economic forecasters were confident beforehand that the door would be left open for even further interest rate decreases.* The FX markets were sitting on “short-sold” Kiwi dollar positions in anticipation of that outcome; however, they were rudely surprised and forced to buy the Kiwi dollar back.

However, the RBNZ statement was not the most influential factor for the future direction of the NZ dollar last week. The following day, Thursday 27th November, the release of the September quarter’s retail sales figures would have sent shockwaves through every forecaster of the New Zealand economy. Retail sales increased 1.90% over July, August and September, a period that the media consistently reported that the New Zealand economy was in a recessionary hole and needed to be rescued by aggressive interest rate cuts to 2.00% by the RBNZ! The strong pick-up in retail sales was not identified in earlier released monthly electronic retail sales data, as large purchasers such as motor vehicles are not paid by a card. It appears that the Government’s accelerated tax depreciation policy on new fixed asset purchases has had a positive impact on vehicle and machinery sales. The 1.90% increase was three times above the prior consensus forecast of a 0.60% increase. The annual increase in retail sales lifting to 4.50%, well above forecasts of a 1.80% increase. On top of the retail sales positive surprise, business and consumer confidence also shot up in November. The ANZ business confidence index increased to 67.1 from 58.1 last month. The ANZ Roy Morgan consumer confidence index lifted to 98.4 from 92.4 last month. Both confidence surveys were well above prior forecasts.

Looking back, the question now has to be asked as to whether the RBNZ would have cut the OCR by 0.50% to 2.50% on 8th October if they has known then that the consumer demand side of the economy had rebounded so strongly in the September quarter.

It will be recalled that bank economists and other economic forecasters were cajoling the RBNZ to cut the OCR through the September/October period as they determined that the economy needed a “kick start” out of the funk and downturn in demand that we were supposedly in. The economic forecasters calling for such action were wildly incorrect on three counts: -

- The RBNZ’s sole job is to maintain inflation between 1.00% and 3.00%. Their mandate does not extend to “kick starting” the economy to get it back on a growth path and increase jobs.

- The negative impact on the NZ economy from Trump’s tariffs was way over-exaggerated.

- As the retail sales data has confirmed, the domestic economy was already recovering very strongly through this period. The regions were experiencing a significant lift in economic activity on the back of higher export prices and volumes. The export-led recovery was happening, unfortunately very few recognised it.

The New Zealand public, the Government, the RBNZ and the media have all been duped by the so-called economic gurus into believing that the economy was not recovering in 2025 and that additional monetary policy stimulus was required to save it. As we have highlighted previously in this column, one has to be careful about reading too much into bank economists demanding large interest rate reductions. The banks’ largest lending margins and the most profitable part of their business is home mortgage lending. They make more money when house prices are rising and homeowners borrow more. Off course they want lower interest rates. The vested interest and conflict of interest is plain to see, unfortunately it is very rarely called out.

The poor quality of New Zealand’s economic data, in terms of the large subsequent historical revisions to GDP growth numbers and the extraordinary time lag for the release of important information such as retail sales (September quarter figures released on 27 November, eight weeks after the end of the quarter) is damaging to our reputation as an advanced trading economy.

For whatever reason, here in New Zealand, we just manage to find ways to make it unnecessarily hard for ourselves!

Financial markets and central banks require timely and accurate economic data releases so that the price of interest rates and exchange rates can be determined efficiently and accurately. We are not getting that in New Zealand today. The financial markets and the RBNZ were made to believe that the economy was struggling to expand in 2025. It clearly was not struggling, with the export-led growth well and truly driving increased economy-wide demand in the second half of the year.

In their statement last week, the RBNZ confirmed that the reported June quarter GDP contraction of 0.90% would likely be revised to something nearer -0.30% as the seasonal and one-off factors are subsequently adjusted. The RBNZ’s own GDP-Nowcast predictor for the September quarter’s GDP growth has jumped up to +0.80% following the booming retail sales numbers. The December quarter is likely to be above a 0.50% expansion, so the 2025 year in total should see an annual GDP growth rate of around +2.00%.

Our 12th October column, entitled “Trusting New Zealand’s economic numbers – yeah/nah!” highlighted the incorrect conclusions that can be made when the economic data is dodgy and untrustworthy. It is confusing for everyone, especially overseas investors into our economy. The unhelpful revisions to our GDP growth numbers and delayed information such as the retail sales data, means that the markets are working on a false premise.

The NZD/USD exchange rate was sold down four cents from 0.6000 to 0.5600 from mid-September to mid-November on its own account on independent/specific local factors: -

- The 0.90% GDP contraction for the June quarter released 18th September.

- RBNZ 0.50% cut to the OCR to 2.50% 8th October.

The GDP number is wrong and the RBNZ cut was now arguably unnecessary. We are already seeing the Kiwi dollar value reverse rapidly upwards, and there is a lot more to come as the rest of the world works out just how much we have misrepresented our own economic situation over recent months.

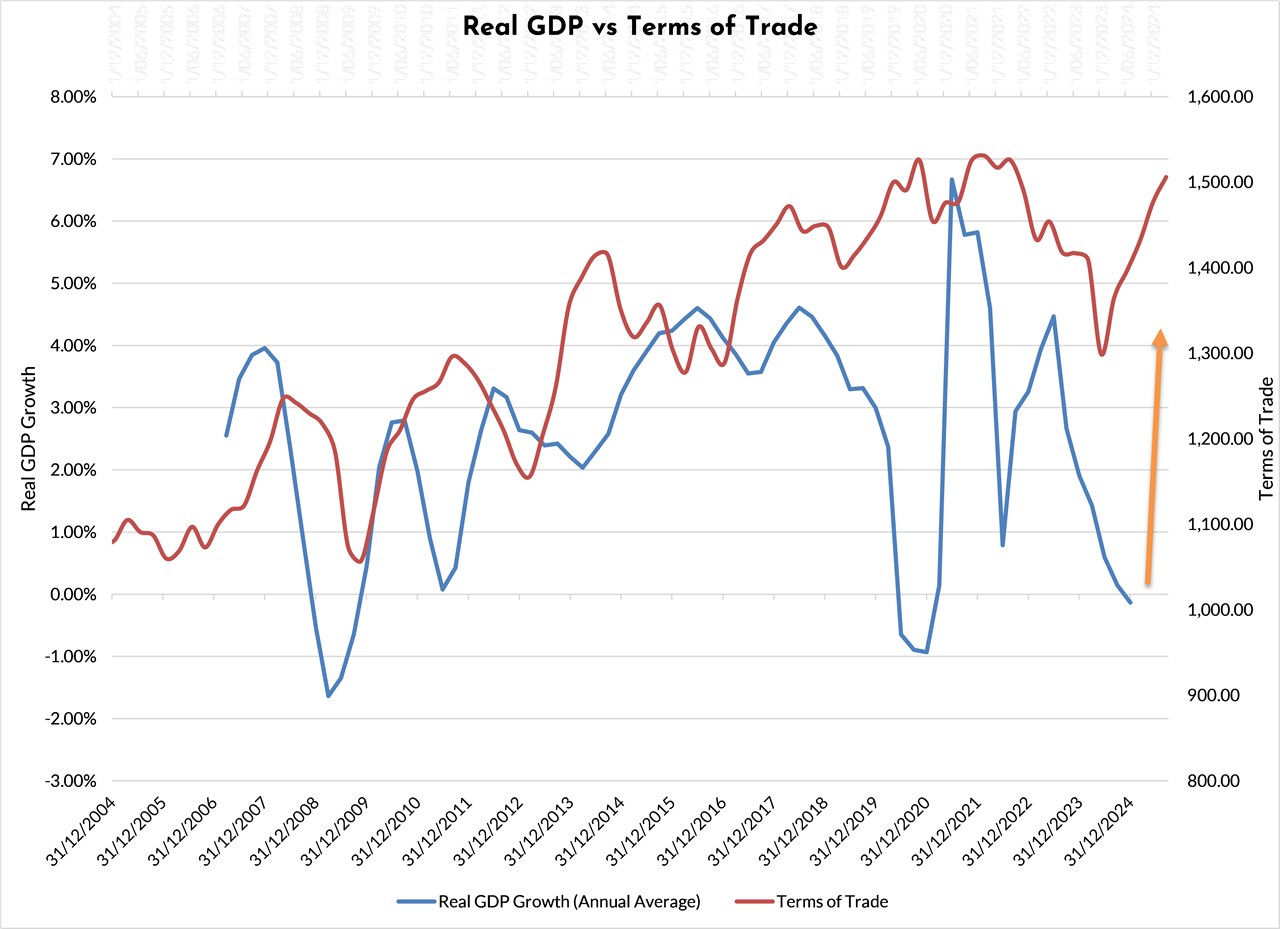

A central theme of this column over the last 12 months has been that our higher export prices would lead to an export-led economic recovery. The only question being on how long it would take for the pick-up in economic activity in the regions to spread into the big cities. The Auckland economy is heavily reliant on the residential property market and high household indebtedness, and low immigration has dampened things down. However, as the chart below confirms, export prices (Terms of Trade Index) does drive overall GDP performance of the NZ economy (Covid years excepted).

The New Zealand economic performance in 2025 has blown away the naysayers and scaremongers, it looks set to exceed most GDP forecasts in 2026 as well.

The Kiwi dollar was sold down on a false premise; it looks set to recapture that four-cent depreciation over coming weeks as the more accurate New Zealand economic picture is understood and reacted to.

Expectations of interest rate cuts in Australia dramatically change to rate hikes

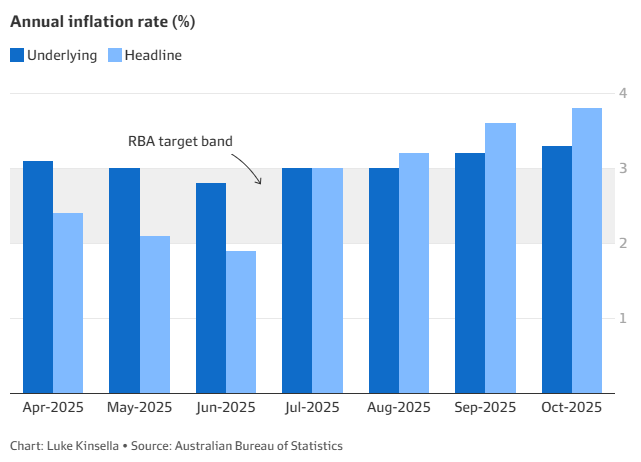

Interest rate and exchange rate direction in Australia is also being rapidly re-rated as fresh data comes to hand on their inflation trends. Back a few weeks ago, the RBA and market’s view was that the increase in inflation in Australia to back above 3.00% was merely temporary. That proposition has been destroyed by the higher-than-expected inflation increase in October; the headline annual inflation increase is now a high 3.80%. Electricity and gas prices jumping up 37% compared with a year earlier as the energy system rebuild becomes hugely expensive for taxpayers and consumers. House building costs are now also on the rise.

The Australian interest rate markets are no longer pricing-in interest rate cuts; they are now pricing-in a rate hike in late 2026.

Over recent years, the Australian Labour Government made appointments to the Reserve Bank of Australia Board who favoured lower interest rates. The interest rate decisions are no longer made by the Board, but now by a separate Monetary Policy Committee with external members outweighing RBA staff. Strong immigration and resources sector exports continues to drive the growth in the Australian economy. The lower Australian dollar value has been a major boost to their export sector, with the mining states of Western Australia and Queensland booming again.

Against all measure the AUD is significantly undervalued, with the change in Australian interest rates being 0.75% below those in the US three months ago, to now being above the US interest rate levels as the most significant development. As the Australian dollar is regarded by global hedge funds and currency speculators as a proxy for the performance of the Chinese economy, it now just requires an improvement in Chinese economic data to prompt the Aussie dollar buyers.

US economic data weaker, as expected

As US Federal Government staff return to work following the shutdown, the deluge of economic data for September and October is starting to be released. Last week we received the first batch of September catch-up data: -

- ADP Private Sector Employment Change decreased again, down 13,500 jobs over the week.

- Retail Sales for September increased by 0.20%, well below the prior consensus forecasts of +0.40%.

- Producer Prices Index (PPI) for September was bang on forecast at +0.30% for the month.

- S&P/Case Shiller Home Price Index for September was 0.00%, against the previous +0.40% in August.

- Conference Board Consumer Confidence for November recorded another significant fall, down to 88.70 from 95.5 last month, and well below forecasts of 93.4.

- The Federal Reserve’s Beige Book economic report (a compendium of regional surveys) reported weaker employment trends in 50% of the Fed’s 12 districts and consumer spending also declined. Overall, the report indicated economic activity going sideways.

Over the last week, the forward pricing of the probability of a Fed 0.25% cuts at the 10th December meeting jumped from a 35% chance to now near certain 85% probability. The markets clearly believe that the October data on the US economy will be very much on the softer side.

Ahead of the Fed interest rate decision on 10th December, important economic data releases include ISM Manufacturing PMI (1st December), Industrial Production (3rd December), ISM Services PMI (3rd December), PCE Inflation (5th December) and JOLTS job vacancies (8th December).

The interest rate cut should trigger further US dollar selling in the FX markets, particularly if the Fed indicate that the weaker employment trends suggest further interest rate reductions in the new year.

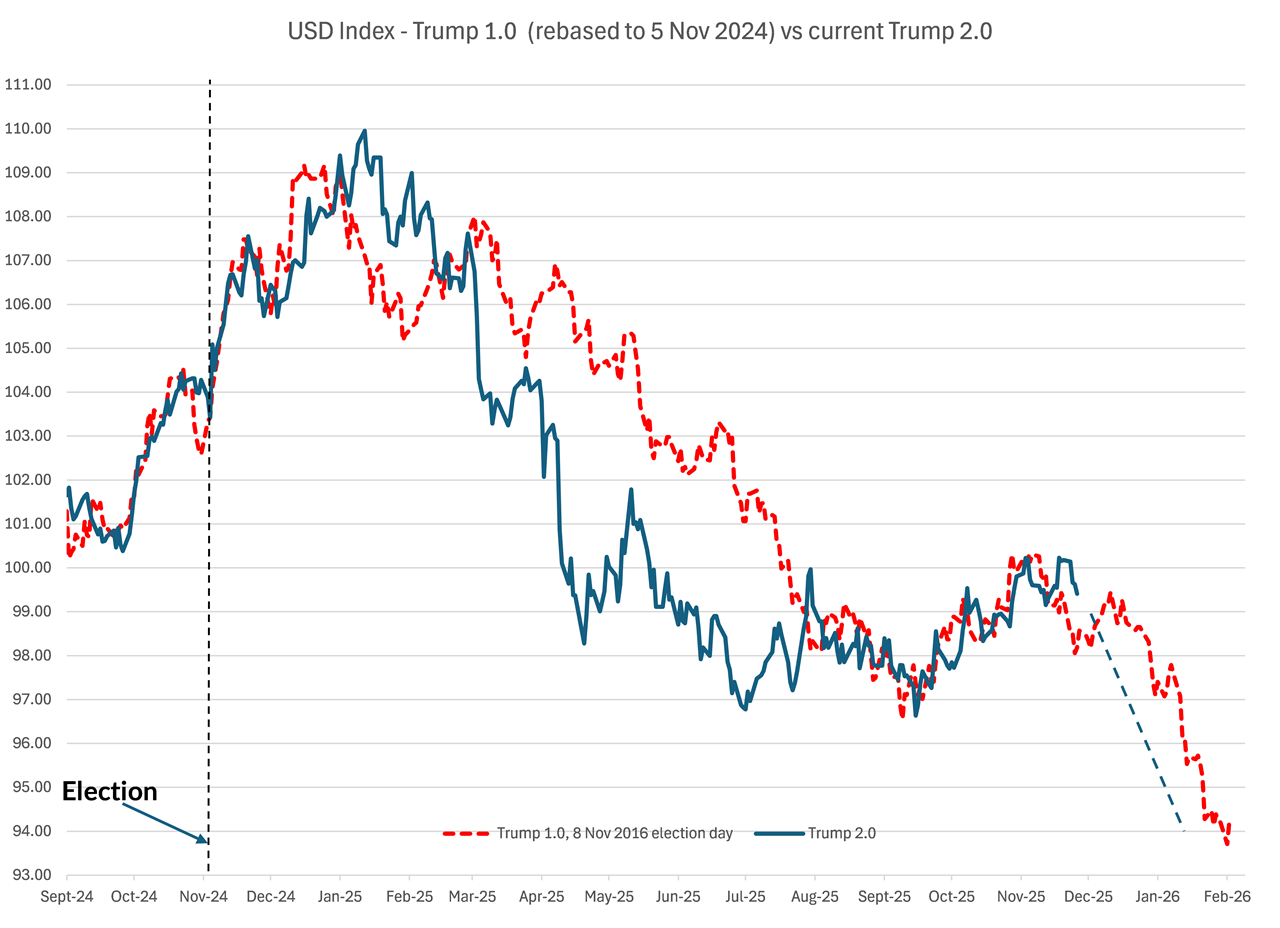

The scary repetition of what the USD Index did eight years ago under Trump’s first term continues. FX market traders are following what happened eight years ago and the upcoming US interest rate decreases points to the USD undergoing another significant sell-off to 95.00 and below on the USD Dixy Index.

We repeat the chart below because it has proven to be so accurate!

*This was corrected from 'increases' in an earlier version of the article.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

9 Comments

The free real time models on the internet are better than the stats releases 3 months after the fact, maybe we just ask AI to build us a new stats department.

Good to see some analysis to show how vested the banking/bank economist narrative has clearly shown to be pushed to best suit the banks profits (wanting lower interest rates however they can influence it in order to increase mortgage lending). Perhaps if everyone realised the banks are not your friend, they are providing you a service and out to profit from you as much as they can.

"The local economic forecasters were confident beforehand that the door would be left open for even further interest rate increases."

This should be interest rate decreases.

Who edits this stuff?

Thank you Roger, excellent article. NZ is becoming more Auckland centric hence the one eyed " economic analysis" such as it is.

We just get on with it here on the Mainland.

However, as the chart below confirms, export prices (Terms of Trade Index) does drive overall GDP performance of the NZ economy (Covid years excepted).

The chart referred to does not correlate all that well. Clutching at straws me thinks.

That is the same for your view the economy rises and falls on housing and immigration - they both follow economic upticks (which makes sense, people are more likely to migrate to an economy doing well, and more likely to overspend on housing when the economy is doing well).

Safe to say the economy is comprised of multiple influencing factors.

I doubt the NZ economy is currently overheating and will need rate increases next year TBH.

An understatement right there, and a good one.

I believe the MS price has been reduced despite a falling dollar

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.