Summary of key points: -

- Active and passive drivers of the NZ dollar’s value

- The Kiwi dollar is breaking out of significant downtrend restraints

- NZ inflation indicators opposite to RBNZ forecasts

Active and passive drivers of the NZ dollar’s value

Macquarie Bank financial market economists in China have identified, in a recent FX report, that there are both active and passive drivers of the Chinese Yuan’s value against the US dollar.

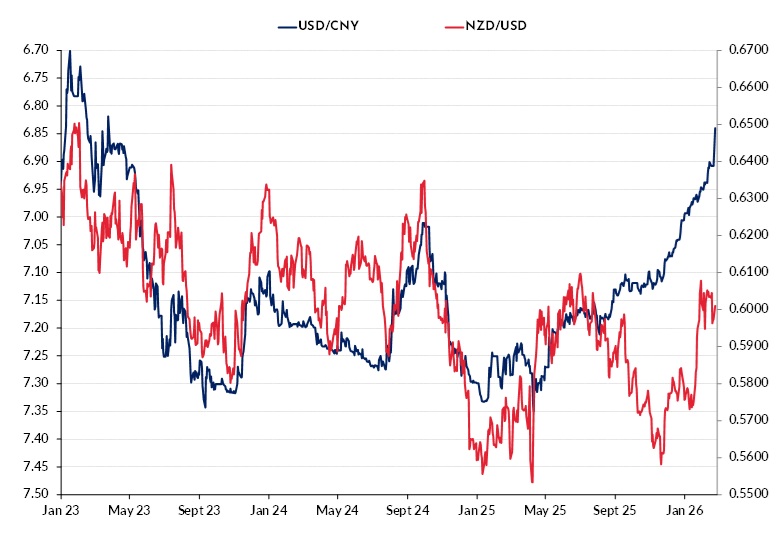

Being a managed and controlled currency, it is not hard to determine the passive drivers of the USD/CNY exchange rate. The general movements of the US dollar against a basket of major global currencies determines the setting of the Yuan’s rate to the USD each and every day by their central bank, the People’s Bank of China (“PBOC”). As a consequence of the USD’s overall 9% depreciation over the last 12 months from 107.50 to 97.50 on the USD Dixy Index, the USD/CNY rate has moved from 7.2750 to 6.8590 (a 6% Yuan appreciation). Arguably, the Yuan has another 3% to appreciate on the USD passive grounds to 6.8000. The active drivers of the Yuan’s direction relate to specific Chinese economic and market reasons. Capital and trade inflows/outflows from the currency will determine ultimate USD/CNY direction over and above the USD passive forces. Right now, the Yuan’s performance is dominated by the passive flows. It will take a change in Chinese economic performance and related stimulus decisions by the authorities to initiate specific (active) buyers or sellers of the currency. Manufactured exports are currently producing most of the GDP growth in the Chinese economy with domestic consumer spending still very subdued, as households save to recover from residential property values going downwards over the last five years. Should the export performance falter, the Government and the PBOC will step in with fiscal and monetary stimulus packages to boost the domestic spending to ensure they hit their overall 5% pa GDP growth target. There does not seem to be much risk of the Yuan depreciating due to inferior economic performance over coming years.

Specific Chinese Yuan appreciation (off its own bat) will come from strong capital inflows into China as foreign investors take a positive bet on China and local companies and sovereign wealth funds return funds home. The impressive spiral higher in Chinese equity markets over the last 12 months informs you that foreign investors, as well as local investors, are adopting a positive view on Chinese corporate and economic performance in the post-Trump tariff global trading environment.

China’s economic and currency performances are critical and important determinants of the performance of the NZ economy and therefore the NZ dollar’s value as well. Chinese demand for our primary industry exports (dairy, beef, lamb, horticulture and logs) is currently strong, as represented by the high prices in everything except logs. In normal economic circumstances the NZ dollar would be appreciating under its own steam, following record high export commodity prices. However, unfortunately we have not been in “normal” economic conditions in recent years. Aggressive monetary policy decisions by the Reserve Bank of New Zealand (“RBNZ”) over the last five years has produced overly loose monetary policies in 2021/2022, causing high inflation in 2023/2024, which in turn required an overly aggressive tightening in policy to bring inflation down (i.e. causing a recession). We are now witnessing another perhaps overly aggressive loosening in policy which has kept NZ interest rates well below those of the US and Australia. The NZ dollar is horribly underperforming the Australian dollar gains against the USD as the RBNZ is completely out of synch with monetary policy settings compared to the Reserve Bank of Australia (“RBA”).

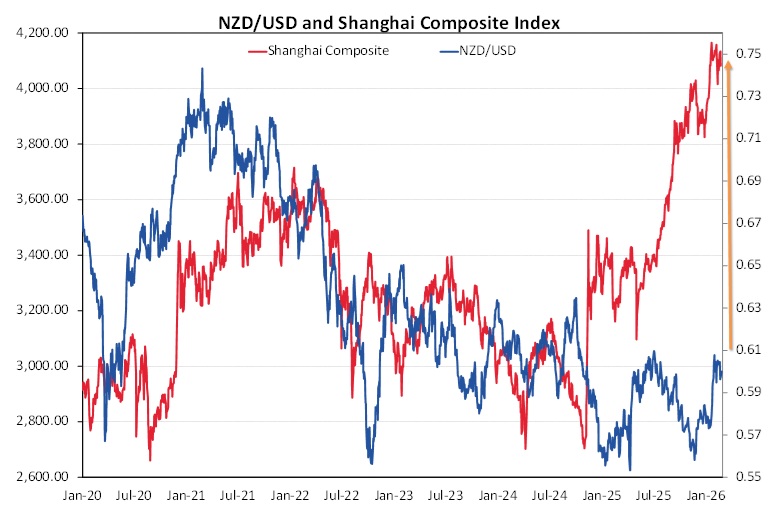

The two charts below suggest the NZ dollar has some catching up to do on the Chinese drivers of its value. Historical correlations are not everything, however divergences catch the eye of currency traders, hedge funds are market arbitrageurs.

Extending the Macquarie active and passive exchange rate concept to the NZ dollar environment results in the following conclusions: -

Passive NZD exchange rate determinants:

- We still see further USD depreciation this year on the back of Fed interest rate cuts and foreign investors into the US equity markets progressively pushing their FX hedge ratios higher (i.e. selling the USD).

- Direction of the Australian dollar. The Kiwi follows the Aussie dollar 80% of the time, except when monetary policy settings in Australia and New Zealand are polar opposites (as we have now, resulting in the NZD/AUD cross-rate tumbling 10% from 0.9300 to 0.8400 over the last eight months).

- Direction of the Chinese Yuan. The NZ economy is highly dependent on China; therefore, it is no surprise that the NZD/USD exchange rate correlates to USD/CNY movements (refer to the chart above).

- Direction of the Japanese Yen. The Yen is the largest freely traded currency in Asia, and the Kiwi dollar is an Asian currency. Expected Yen appreciation this year due to the closing up of the yield difference between Japanese and US bonds is currently being stymied by Japanese PM Takaichi holding back the Bank of Japan back from raising their interest rates. Forecast Yen appreciation against the USD from the current 156 level to 130 and lower, would see the correlated and following NZD/USD rate closer to 0.6500.

Active NZD exchange rate determinants: (NZ specific factors)

- Export commodity prices and foreign tourism inflows. It was not so long ago that the NZD/USD exchange rate was closely correlated with whole milk powder commodity prices (and export commodity prices in general). The connection has been decimated over the last few years as NZ interest rates tracking well below those of the US has dominated the currency scene. In the second half of 2026 we will see the US:NZ interest rate gap reduced to zero as NZ interest rates increase and US interest rates decrease. The FX markets will typically build in that change well in advance. Tourism is booming in New Zealand again, which tells you that we are cheap and the NZ dollar is undervalued.

- As monetary policy in New Zealand normalises this year with a return of the OCR to “neutral” territory above 3.00%, the carry-trade of borrowing the low interest currency (USD) to invest in the high interest yield currency (NZD) may make a comeback – just as it has in Australia recently with AUD interest rates now 0.75% above US interest rates.

- Speculative FX market positioning. The US futures markets are now net long the AUD against the USD. NZ dollar speculative positioning is still net short NZD (35,000 futures contracts). With the NZD trading to above 0.6000 and likely to go higher, those short NZD position holders will be close to closing out i.e. buying the NZD to do so.

- Investor risk-on and risk-off sentiment. The NZ dollar is regarded, along with the AUD, as a growth/commodity currency. When equity investors are selling out under a market risk-off sentiment, the Kiwi dollar will struggle to make gains (and vice-versa).

- Cross-border capital flows – Mergers and acquisitions activity (Aussie private equity firms taking advantage of the weak NZD against the AUD currently to buy in to NZ), along with immigration flows and direct foreign investment all have an impact on the NZ dollar value. The cross-border flows are more likely to be increasing over coming years after several years of lower activity.

- Economic health of key trading partners. Australia and China are the most important for us.

- Relative economic performance. The NZ dollar has been out of favour over recent years due to its lower interest rates and bouts of economic recession. Business confidence surveys are an accurate lead indicator for GDP growth. Both are looking super positive this year. GDP growth in New Zealand in 2026 (above +3.00%) is likely to be superior to growth in both Australia and the US.

- Sovereign credit rating and confidence in Government finances. Despite inaccurate predictions from some quarters that New Zealand would suffer a credit rating downgrade after several years of poor economic performance, the high export prices have prevented that from happening (as we expected). Stronger growth in the economy this year (producing higher tax revenues) will assist the Government’s deficit reduction efforts more than anything else.

Both the passive and active forces determining the NZ dollar value appear much more positive than negative as we move further into 2026.

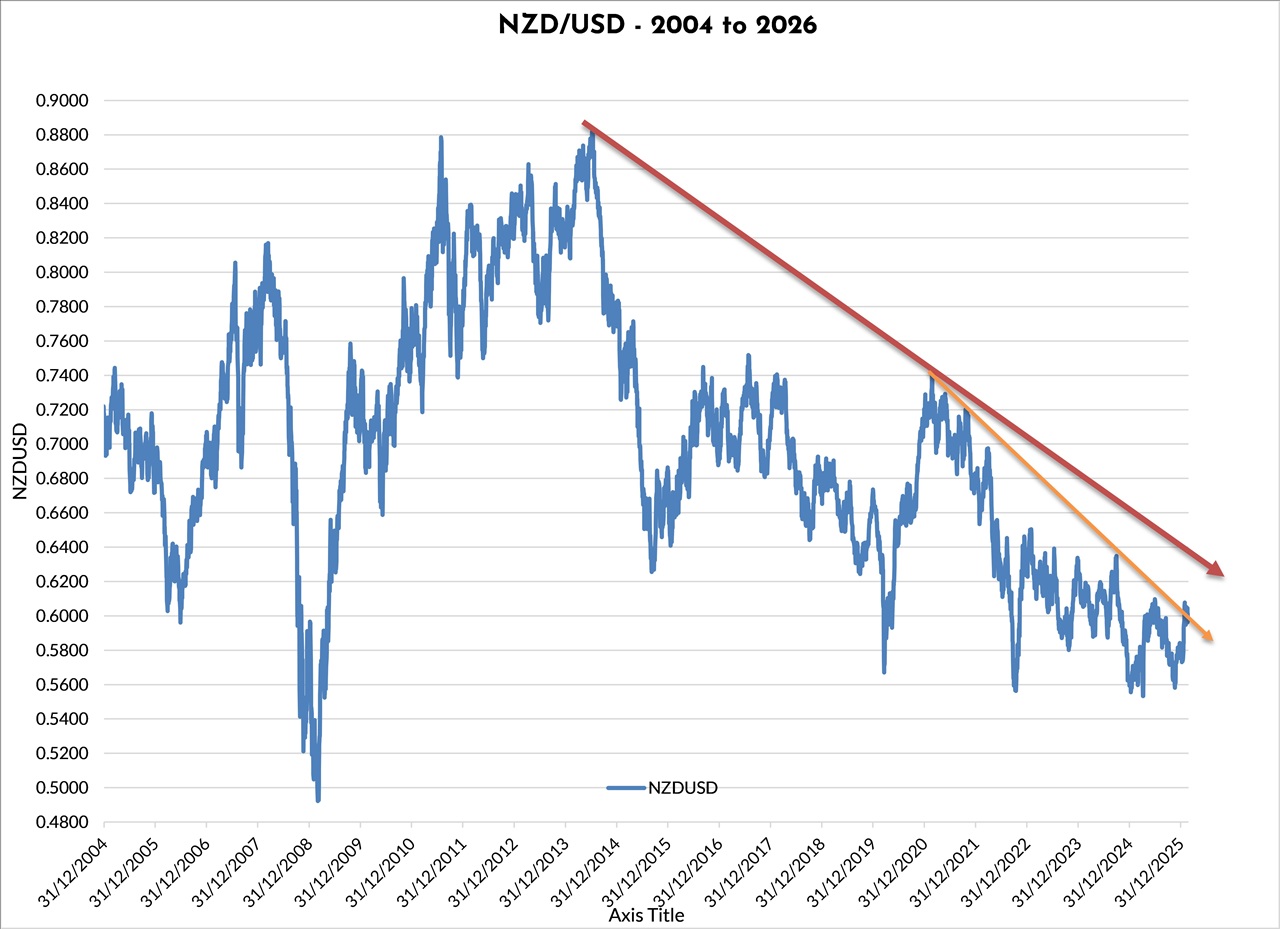

The Kiwi dollar is breaking out of significant downtrend restraints

The recent move to above 0.5950 in the NZD/USD exchange rate has broken out above the five-year downtrend line running since the highs of 0.7400 in early 2021 (Gold downtrend line in the chart below).

Further moves higher to above 0.6300 will break out above the longer-term 12-year downtrend line that the Kiwi dollar has remained below since 0.8800 in 2014 (Red downtrend line in the chart below).

It will not go unnoticed around the world that the Kiwi dollar is again recovering strongly from the two selloffs below 0.6000 in 2025. A move higher towards 0.6300 over coming weeks/months will certainly return a lot more currency trader attention to the Kiwi dollar.

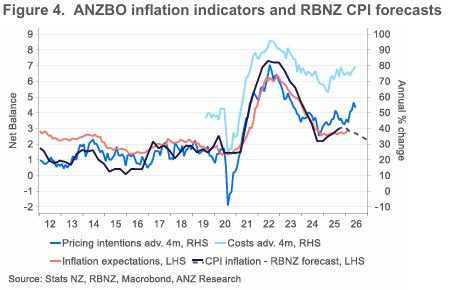

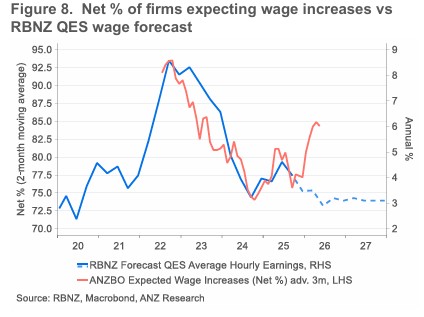

NZ inflation indicators opposite to RBNZ forecasts

Two charts in the latest monthly ANZ Business Opinion survey stood out like beacons in terms of communicating a completely different message to the RBNZ on the trajectory of inflation this year.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.