Summary of key points: -

- Bonds and equities hit hard by the ongoing war, currencies not so much

- US Federal Reserve confident the US economy will traverse this shock as well

- Softer than forecast NZ GDP growth fails to depreciate the Kiwi dollar

Bonds and equities hit hard by the ongoing war, currencies not so much

Global bond and equities markets were hit hard last week as investors started to price-in more of a “worst case scenario” for the outcome of the Iranian war. US bond yields have increased sharply as investors sell out, worried about US inflation staying higher for longer form the oil shock and also worried about the US Government fiscal deficit and related debt issuance blowing out from the cost of the war and potential tariff refunds. The US 10-year bond yield jumping up from the 4.25% area earlier last week to close on Friday at 4.38%. Likewise, US equity markets are reflecting the negative from higher bond yields and a Fed moving away from cuts to short-term interest rates this year.

Interestingly, currency markets have not seen the same panic selling and volatility in response to the ongoing war in the Middle east. The plausible explanation for the lack of response from foreign exchange markets is that all economies are equally impacted by oil prices shooting up and that in turn increasing headline inflation in the short-term. The Reserve Bank of Australia (“RBA”) was the only central bank to change interest rates last week, the US Federal Reserve, Bank of Canada, Bank of Japan and the Bank of England all sitting pat as their wait to see what impact, and for how long, the war and oil price increases will have on their respective inflation rates and economic growth.

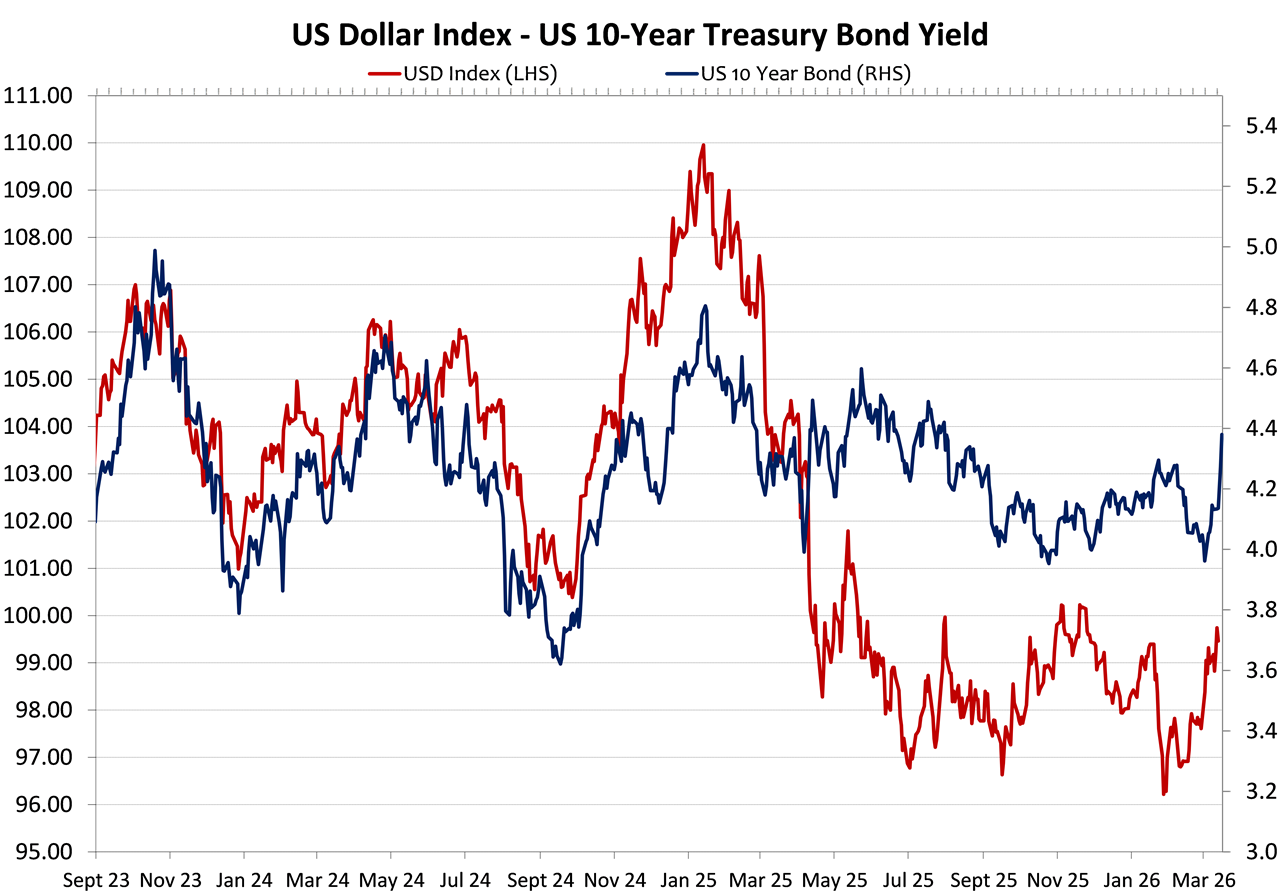

The US dollar Dixy Index has remained within a relativity narrow band over the last seven days, between 98.95 and 100.05. The currency stability reflecting the fact that all economies are being impacted in a very similar fashion. The USD did not follow the bond yields higher last week.

The New Zealand dollar has been sold down to a low of 0.5775 against the USD on two occasions since the war commenced three weeks ago on Saturday 28th February, on the general “risk-off” sentiment in the financial and investment markets. It has to be said that the NZD/USD exchange rate has held its value at around 0.5800 and 0.5900 much better than what most expected when the war started. We are still more likely to be raising interest rates sometime this year, contrary to what the Americans are likely to do, and that factor is dissuading any aggressive NZ dollar selling at this time. The NZ dollar also has the potential to attract some “safe haven” capital flows inwards from global investors exiting the Middle East and exiting the US dollar, looking for somewhere safe a long way away from the turmoil. There is no evidence of these flows occurring yet, however if the war drags on, the NZ Government’s golden visa scheme to attract wealthy investors to our shores is likely to see growing interest.

As the Iranian war enters its fourth week, the markets are still seeking the signal that President Trump has found his “off-ramp” to end the conflict. He is now stating that the US is looking to “wind down” the war and that other nations must guard the Strait of Hormuz to ship the oil supplies out. The US is not reliant on oil coming through the Strait of Hormuz. It seems the Chinese have negotiated safe passage with the Iranians for their oil and ships; other affected Asian countries will be seeking the same arrangement. At some point, the oil markets will start to reflect (through falling oil prices) that the supply disruption caused by the closure of the Strait of Hormuz is nowhere near as bad as first thought. Like the Russians, the Iranians will be keen to sell as much oil as they can whilst the price is elevated.

As we have stated before, the runway of time is running out for Trump with a prolonged military involvement in Iran losing him political support back at home. The Israeli’s will still be keen to finish the job and put their military’s “boots on the ground” to potentially force an Iranian government regime change. Destroying Iran’s nuclear capability is a big part of the US and Israeli objective. They cannot be too far away from achieving that goal. Iran, clearly does not want conflict with their neighbours of Oman, Turkey, UAE, Qatar and Saudi Arabia. However, they have invited such conflict with their drone and missile attacks. Nothing ever quite adds up with simple logic in the Middle East!

Politically, Trump needs to declare a “victory” very soon and when he makes that announcement and the missile strikes both ways cease; the oil, bond and currency prices will reverse the movements they have made since the start of March. The initial estimate that the war will go on for four to six weeks looks increasingly likely to be the scenario that turns out to be true. The wait and worry period on inflation for all the central banks will potentially end rather abruptly.

It should always be remembered that the forces that have driven oil prices higher over the last three weeks are largely speculative selling on derivatives markets by hedge funds and trading desks of global investment banks. These punters will rapidly reverse their bets the other way when the geo-political risk is much reduced with a ceasefire.

US Federal Reserve confident the US economy will traverse this shock as well

The official Fed statement last week on the economy and monetary policy settings was effectively a repeat and rinse of their previous statement in January. Off course, the Iranian war has started in the meantime, however the Fed along with other central banks, is saying that it is still too early to assess the impact of the higher oil prices on inflation, economic growth and therefore the direction of interest rates. The markets do not hold that same uncertainty or caution, with US two-year Treasury Bond yields soaring up 0.50% from 3.40% three weeks ago to 3.90% today. The market pricing has rapidly shifted from pricing-in Fed cuts to interest rates, to now be pricing the prospect of an interest rate hike.

From Chair Jerome Powell’s media conference, the Fed seem supremely confident that the US economy will easily traverse this external shock, just as they have sailed through other shocks in recent years (Covid, tariffs, Ukraine war) with GDP growth intact. Strangely, there was no mention from Powell or the media hacks of the dip in the US annual GDP growth rate to just 0.70% in the December quarter. The US economy seemed the be slowing more abruptly than most expected before the war even started. Chair Powell pontificated that increased productivity was the reason why the economy was able to ride out these external disruptions without GDP growth being damaged.

However, what is becoming very evident in the US economic data is that the “K-shaped” nature of economic growth (the wealthier spend more, but the poor are forced to spend less by affordability problems) will deteriorate further from higher gasoline prices. With equity markets now going south due to the war and the prospect of lower economic growth, even the upper income earners may have to curtail their spending as their share portfolios are trimmed in value. The net effect is likely to be the US economy being more adversely impacted by this external shock than previous shocks.

Judging by last week’s statement, the Fed also appear overconfident as to the strength of the labour market. They are seemingly not worried by the fact that the number of jobs being added to the US economy (as measured by the Non-Farm Payrolls data) has plunged to zero over the last eight months. The Fed state that the supply and demand for labour is in balance at a lower level, and that is why the unemployment rate is not rising. The supply of labour is down as there are fewer workers seeking jobs in the US economy due to Trump’s immigration policies and resultant deportations. Plunging equity markets and much higher market interest rates as a result of the war, suggest that US business firms will be hunkering down, postponing new initiatives and reducing hiring over coming months. The household survey of jobs which produces the unemployment rate is heading the wrong way, pointing to the US unemployment rate rising over the next period.

When the war ends and oil prices correct down, we would expect to see a reversal in their two-year interest rates, which will reflect the need for the Fed to still cut interest rates this year on the employment side of their dual mandate. If this scenario eventuates, the US dollar will return to its previous depreciating trend.

Softer than forecast NZ GDP growth fails to depreciate the Kiwi dollar

The weaker than forecast GDP growth figures for the December 2025 quarter, which were released last week, only had a very temporary negative impact on the Kiwi dollar’s value. The NZD/USD exchange rate dipping from 0.5870 to a low of 0.5785 before quickly rebounding back to 0.5870. The fast-moving events in the Middle East having a greater impact on the currency’s value than historical economic data from three to six months ago. New Zealand’s GDP expanded by just 0.20%, well below prior forecast of +0.50%. A 1.40% contraction in the construction sector pulled the numbers back. Agriculture, exports, retail, tourism, telecommunications/media and services sectors all recorded strong growth. Anecdotal evidence from sawmills is that local New Zealand demand for sawn timber for construction has certainly picked up over recent months, suggesting that the lag from the building sector will not be too long lasting.

Depending on how long the Iranian war goes on for will determine whether the stronger growth now coming through in the domestic economy will be adversely impacted by higher petrol prices at the pump and mortgage interest rates going up. Sharply higher petrol pump prices do act as a regressive tax and reduces other discretionary spending in the retail sector of the economy. Our exporters have so far been able to divert ships carrying apples, meat and dairy products bound for the Middle East to other markets. Higher sea freight costs will be a negative for exporters, again depending on how long the war goes for and oil prices remain up. A prolonged war would not be good news for our foreign tourism industry which has finally pulled itself back to full noise following Covid.

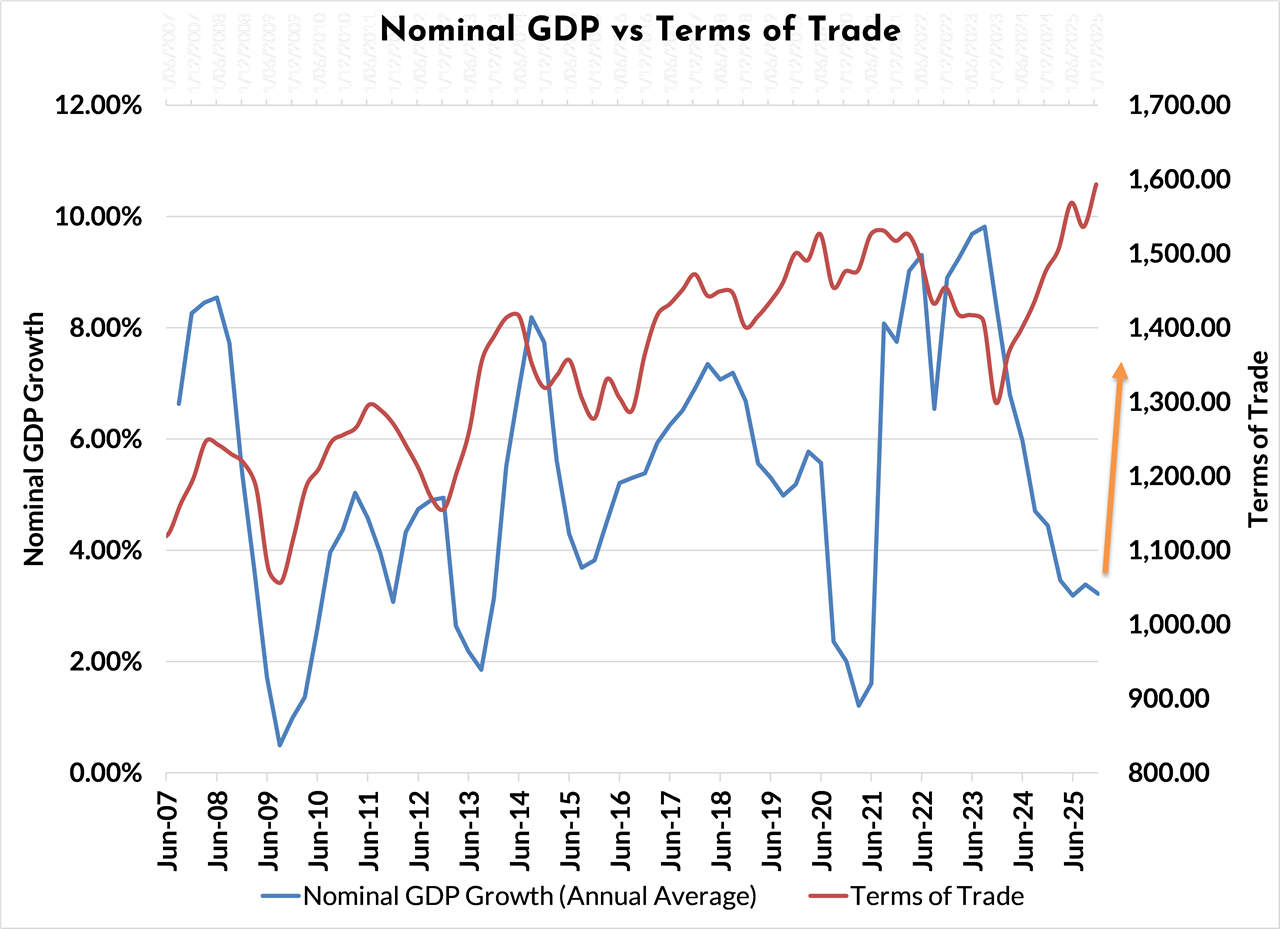

As the chart below confirms, it is the level of our export commodity prices (as measured by the Terms of Trade Index) that ultimately drives GDP growth in our economy. Whilst rising house prices and immigration are often seen as the impetus behind growth in the economy, the real wealth creation comes from primary produce being sold into export markets. On the proviso that the Iranian war is not long lasting, the New Zealand economy looks in a better position with high commodity prices to be outperforming Australia and others in the GDP growth stakes over coming years.

Credit rating agency, Fitch has adjusted New Zealand’s AA+ sovereign rating to a “negative” outlook, citing debt reduction concerns. They correctly point out that fiscal consolidation has been delayed in recent years. However, we are not at risk to a credit rating downgrade as higher export commodity prices improves our ability to service any debt. The Fitch report was very light on mentioning the export boom offsetting many of the negatives for the NZ economy.

The Covid shock in 2020/2021 was the exception that forced nominal GDO growth downwards, contrary to rising/stable export prices at the time. Outside of that period, GDP growth for the NZ economy is highly dependent upon our Terms of Trade performance (export prices over import prices).

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

2 Comments

These punters will rapidly reverse their bets the other way when the geo-political risk is much reduced with a ceasefire.

The "when" is the big unknown at this point.

Trump needs to declare a “victory” very soon and when he makes that announcement and the missile strikes both ways cease; the oil, bond and currency prices will reverse the movements they have made since the start of March. The initial estimate that the war will go on for four to six weeks looks increasingly likely to be the scenario that turns out to be true. The wait and worry period on inflation for all the central banks will potentially end rather abruptly

I don't understand this way of thinking, which seems very US-centric

If I am to summarise the war in a sentence, it's: "Trump gave Iran permission to use its most lethal weapon: control over the Strait of Hormuz, and they really like their newfound toy"

To assume that anyone but the IRGC has control over the flow of the slow moving toppled blocks of apartments that the crude oil carriers are, is beyond me. This war has suddenly become more asymmetric than it looked on paper before it started: IRGC have cheap ways to make transit unaffordable and unfeasible. Trump has midterms to cater to in a few months. I see no incentive for the IRGC to leave such leverage on the table. And I see no acknowledgement of the asymmetry from Trump or anyone else around him

We have a long way to go until the interests will converge into a deal. First, both actors need to be on the same page. And I'm afraid currently the IRGC are the ones which have a better grip on reality

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.