Summary of key points:

- Global factors conspire against the Kiwi dollar

- When will “political risk” loom for the Kiwi dollar?

- The Japanese are warming up for interest rate hikes

- Private credit risk ramps a notch higher in the US

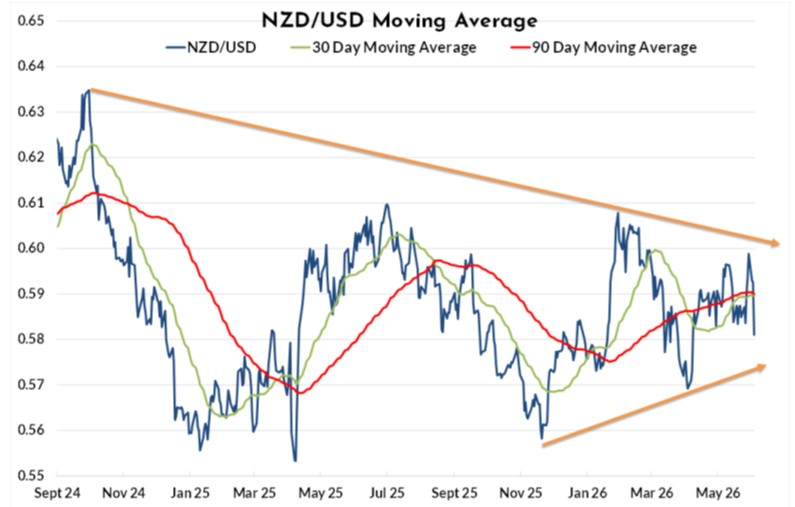

It seems that the Kiwi dollar cannot take a trick currently as global factors cause US dollar buying. After nearly reaching the key 0.6000 level on 29th May, the NZD/USD exchange rate has been forced sharply back down due to two developments that have stimulated US dollar buying across the foreign exchange markets: -

- Oil prices moving higher last week as any progress towards a peace deal between the US and Iran was destroyed by renewed hostilities. West Texas crude prices increasing to US$96/barrel, which in turn sent the USD higher and the NZD lower to 0.5860.

- Another surprisingly strong Non-Fram Payrolls job increase in the US economy in May sent the USD higher still, pushing the Kiwi dollar lower again to close at 0.5810. The US interest rate markets have swung strongly in favour of the next move by the Fed being an interest rate hike, rather than the earlier expected cuts. US inflation is higher due to oil, and the labour market has not weakened over recent months as we expected it to do.

Over the last three months we have become accustomed to the reverberations up and down in the Kiwi dollar as the global FX markets react to news in the Middle East by buying or selling oil. In turn the USD is swinging about in line with the oil price movements. That strong correlation between oil and the USD was under pressure of breaking late last week after the stronger than expected US jobs release prompted USD buying, even though the oil price came back abruptly from US$96/barrel to US$90/barrel. The oil market reversal to lower prices came about last Friday after President Donald Trump expressed a reluctance about restarting the war with Iran. Trump is slowly manoeuvring himself into a “pincer move” whereby he is running out of options and the public mood in the US is clearly heavily against the war causing higher gasoline prices. The US House of Representatives voted against continuing the war, reflecting the public mood, however even if the Senate endorse that rebuke against Trump, he has the power as President to veto. Unsurprisingly, Trump labelled the politicians as “disloyal” to appeal to his own Republican voter base.

The US dollar Dixy Index has returned to the 100.00 level again, a position that it has appreciated up to several times over the last two years, however, it has always rebounded back down again from that barrier. Oil prices will need to continue to decline further into the US$80’s to reverse the USD gains and turn the USD down again. There is a reasonable prospect of that happening as Trump is likely to compromise with the Iranian just to end the conflict and get the oil tankers through the Strait of Hormuz again.

US economic data trends have taken something of a backseat to the Middle East war over recent months as a determinant of the US dollar direction. Three successive strong monthly jobs numbers is certainly a positive for the US economy and the US dollar value. However, other important economic indicators such as consumer confidence and revised lower GDP numbers for the March quarter do not suggest a robust uplift in activity across the US economy. Therefore, the positive Non-Farm Payrolls figures still have to be regarded with a large dose of scepticism, as the economy appears to be moving sideways with a “low hire, low fire” labour market environment. Yet again, the job increases in May were concentrated in the hospitality and healthcare sectors. You just wonder how sustainable the strong increases on those industries actually are.

Local US dollar importers and exporters have both had ample opportunity to top-up hedging percentages recently with the NZD/USD exchange rate trading above 0.5950 and below 0.5850 respectively. On the balance of risk against reward, we still recommend that US exporters are hedged at exchange rates below 0.6000 for multiple years, whereas USD importers are now generally hedged six to nine months forward at around 0.6000 (having the benefit of forward points added on).

The next move in the Kiwi dollar still seems highly dependent upon how soon Trump will construct an exit for himself from the war that looks like a victory for his supporters. The oil price remains as the key forward indicator in this respect. Further decreases into the US$80’s this week will see the USD bounce down from 100.00 on the Dixy Index and the NZD/USD bounce up again from 0.5810.

When will “political risk” loom for the Kiwi dollar?

We are often asked about how much the upcoming general election in New Zealand in November will influence the NZ dollar exchange rate value. Our considered answer to date has been “it is still too early and not much”.

In the past, offshore participants in the NZ dollar have regarded political risk as a quite low factor for their view on the NZ dollar value as the two mainstream political parties, Labour and National are not that far apart on economic policy settings. They do differ on distribution of tax revenue and debt management, however, not enough to cause a foreign player to adjust their NZ dollar assets/holdings. The offshore investors and traders do not really understand the vagaries of our proportional representation voting system and the part the minor parties play in forming coalition governments. Some local businesspeople might fret about the risk of Labour forming a coalition government with the Greens and the Maori Party; however, it is not likely that offshore players will be selling the Kiwi dollar because of the existence of this risk. Interest rate yield pick-up is what the global hedge funds and investment banks want to see in a currency, we do not have that helping the Kiwi dollar at the moment, however we may well see that later in the year.

The current Coalition Government in New Zealand were hanging their hat on the economy improving substantially this year to prove to the public that they are better economic managers than the “borrow and hope” policies of the Labour Party. Unfortunately, Trump’s war has stymied the strong growth we have seen in the economy from June 2025 through to March 2026. PM Christopher Luxon needs a quick end to the war politically, just as Donald Trump does.

By September, the political opinion polls will be telling us whether there is any downside risk for the Kiwi dollar if the Labour/Greens/Maori Party group are attracting sufficient votes to form a government. Winnie and Christopher will be hoping that Trump has manipulated a “victory” well before then and the economy is on the up and the oil prices are on the down.

A return of the National/NZ First/ACT coalition government would be seen as a marginal positive for the Kiwi dollar as the economic policies promoting exports and inward foreign investment will continue.

The Japanese are warming up for interest rate hikes

The stronger US dollar late last week on the US jobs data has pushed the USD/JPY exchange rate above the key 160.00 level that the Bank of Japan have been busy defending with US$75 billion of market intervention buying the Yen. We have always been of the belief that the intervention will not turn the tide for the Yen exchange rate, however combined with interest rate increases, it can still be effective at the end of the day.

Last week, the Bank of Japan officials delivered their strongest signal yet that they are about to return to interest rate hikes to control their inflation. Bank of Japan Governor Kazuo Ueda cemented a June rate hike in a narrative pivot toward inflation-fighting, as the Iran war-driven energy shock sharpens price risks and opens the door to more frequent increases in borrowing costs.

“The hawkish tone has strengthened further, including a clear expression of concern about behind-the-curve risk,” wrote Naohiko Baba, head of Japan research and chief Japan economist at Barclays. “We stick to our June rate hike call.”

What we do know about the Yen exchange rate is that when it does move to an appreciating trend against the dollar it will move fast and a long way. It has not happened yet, but it will happen!

Private credit risk ramps a notch higher in the US

We have previously warned of this growing and largely unreported financial risk in US funds management and lending markets. It seems the risk of a bust-up is continuing to grow, judging by these recent reports: -

- Blackstone announced Thursday it was restricting withdrawals from its flagship fund following a spike in investor redemption requests.

- It comes a day after private markets giants sold off after Switzerland’s Partners Group said it was curbing redemption requests in one of its European private equity vehicles.

- Partners Group later warned it was prepared to restrict withdrawals from more funds; warning client withdrawals were spreading from private credit into private equity.

Well respected market commentators are stating that we may be in the first stage of a default cycle for private credit funds. Watch this space! It will not be positive for the US dollar if there is a major market meltdown in private credit funds.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.