Summary of key points: -

- The markets surprisingly back Trump’s claim of an Iran agreement

- Pullback in the Aussie dollar is a healthy market flush-out

- Volatile market environment for Kevin Warsh’s first Fed meeting

The roller coaster that is the ever-changing mind of US President Donald Trump remains as the dominant determinant of global currency movements. Last week, the US dollar appreciated to the top of its trading range at 100.30 on the Dixy Index when the US military recommenced hostile attacks on Iran. The plan was to obviously leverage the Iranians back to the diplomatic negotiating table. It may have worked! Since then, the US dollar has rapidly reversed its direction downwards following the latest flip-flop from Trump wherein he has stopped the attacks and claims that a “Memorandum of Understanding” deal has been settled with Iran, and it is just subject to signatures this weekend. The Iranians have called Trump’s claim as “speculative”, and they have not agreed to anything. A subsequent report from the Pakistani Prime Minister, who are the prime brokers in this affair, suggested that the Iranians are accepting the terms.

We have seen all this before from Trump over the last two months, boldly claiming he was close to a “great deal”, only for nothing to actually materialise. The markets could certainly be excused for being very sceptical about the accuracy of an agreement to extend the ceasefire and reopen the Strait of Hormuz. However, for the meantime, the oil and FX markets seems to be backing Trump’s position with WTI crude oil prices plummeting 11.5% from US$95.00/barrel to US$84.00/barrel over the last week. Trump’s comment that oil prices would plummet once the war ended is proving to be correct (so far!). Our view has always been that the US dollar would follow the oil prices sharply lower and that would automatically lift the NZD/USD exchange rate.

We have also been of the opinion that Trump would eventually be forced to compromise on securing a final position on Iran’s enriched uranium/nuclear capability as an integral part any peace deal. As time has marched on, he has become under increasing pressure of the approaching US mid-term elections in November and the US’s rapidly declining stocks/reserves of oil to end the war sooner rather than later. His previous bottom and red lines have been conveniently parked for another day. There is no guarantee that Trump’s latest “agreement” gets signed and implemented. However, the markets are sufficiently convinced to act. The oil price on futures markets is plunging as the speculative traders close down their “long-oil” positions entered three and a half months ago.

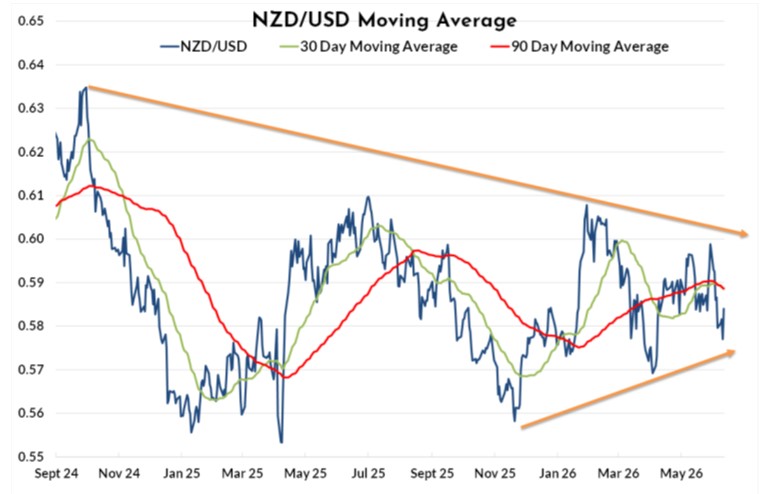

On the expectation that an agreement is signed with the Iranians over the next few days, the oil price does seem to be on a path of quickly returning to somewhere near US$70.00/barrel. The USD Dixy Index has already dropped to 99. 77, allowing the Kiwi dollar to crawl off the bottom of its trading range once again. The NZD/USD rate fell away to a low of 0.5770 when the USD Index peaked at 100.30, however it has since recovered to 0.5835. Unwinding of long USD positions entered on the elevated geo-political risk of the war should send the US dollar sharply lower over coming weeks as the war risk comes to an end. The USD selling from this source is expected to outweigh any positives for the USD from US interest rates remaining higher for longer this year.

The NZD/USD exchange rate has tested both the upper limit at 0.6000 and lower bound at 0.5750 of its converging wedge formation over recent weeks. We have included the same chart below for the third week in a row in this report to demonstrate the closing of the wedge with the upward sloping support line and downward sloping resistance line both containing the daily spot market movements. A continuation of the fall in oil prices should see the resistance at 0.6000 being tested in the very near future.

Pullback in the Aussie dollar is a healthy market flush-out

Over recent weeks the AUD/USD exchange rate has undergone a decent correction downwards from above 0.7200 to below 0.7000 against the USD (now trading higher at 0.7050). The stronger US dollar due to an earlier re-escalation in the Iran war and the strong May Non-Farm Payrolls jobs data being the two factors that triggered the AUD selling. We have also witnessed a fair amount of profit taking by currency speculators who rode the AUD higher when their interest rates increased to above those of the US a few months back. Speculative positioning currency data in the US has seen “long-AUD” positions pared back over the last two weeks. In many respects, it is a healthy sign that the AUD/USD exchange rate has corrected back as it has, as the “long-AUD” positioning has been flushed out and reduced. The speculative market positioning is now in a better place to enter new “long AUD” bets.

There are a number of developments that suggest the Australian dollar still has further upside against the USD after its nine-cent climb from 0.6300 late last year to above 0.7200: -

- The inevitable reopening of the Strait of Hormuz is seen as an AUD positive and USD negative as the energy crisis subsides as a factor in currency markets.

- Lower oil prices are a negative for the USD as the US is now a net exporter of oil, therefore the lower oil price results in lower US exports.

- The ending of the energy crisis is positive economic news for Australia’s trading partners in Asia, who have seen their economies and their currency values reduced during the period of the Iran/US war.

- Emerging market equities have been rising strongly and will receive another positive boost from lower oil prices. The AUD/USD exchange rate has been historically closely correlated with emerging market equities; therefore, it is difficult to see the AUD depreciating if these share markets continue to rise.

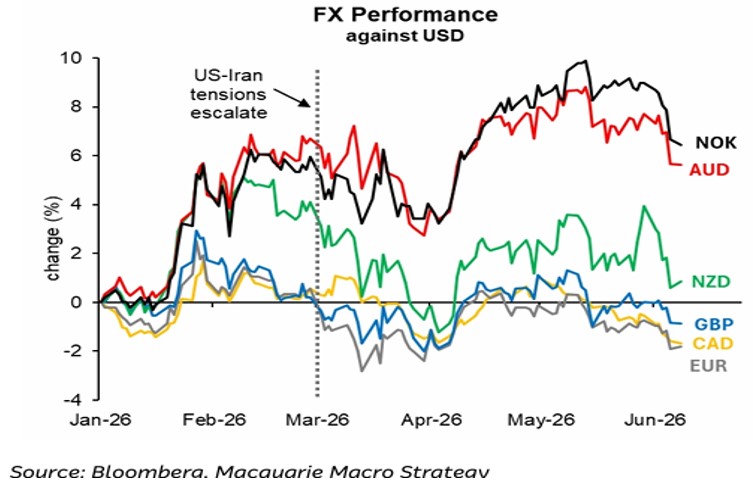

Despite the forward interest rate market pricing in Australia pulling back from a terminal OCR increase to 4.75% to 4.55% today, the Australian dollar has been one of the top performing currencies against the USD since that war started at the end of February. Only the oil-linked Norwegian Kroner has matched the AUD’s performance against the USD. The Aussie dollar gains are yet another reminder of the power of interest rate differentials is determining currency movements (refer chart below).

Volatile market environment for Kevin Warsh’s first Fed meeting

The markets are expecting that the wording in the Federal Reserve monetary statement this Thursday night will remove the bias to the next change being a reduction in the Fed funds interest rate. The change will come as no surprise as the forward market pricing has shifted from interest rate cuts to one interest rate hike this year. It is a very tricky economic and financial market environment for Kevin Warsh’s first meeting as Chair. He has to balance the prospect of rising headline inflation (due to oil price increases) causing second-round price increases and wage increases against the increasing probability that oil prices will plummet further to US$70.00/barrel, rapidly reversing recent increases in the inflation rate. Last week’s CPI inflation figures for the month of May caused some alarmist media reaction as the annual headline inflation rate jumped up to 4.20%. However, what the Fed will be more interested in was the fact the core inflation (excluding energy and food prices) for the month came in at +0.20%, below the +0.30% expected. The potential for rapidly falling oil prices and imported goods prices no longer increasing from tariffs are likely to produce an environment for US inflation measures to reverse sharply lower over coming months. That is not an environment requiring higher interest rates to slow demand to beat inflation down. You cannot often agree with Trump’s views on the US economy; however, he may well be proved correct on the war ending causing immediate and significant reductions in gasoline prices, and therefore US inflation.

There will be much interest in Mr Warsh’s views on the US employment market, however we suspect that his preparedness to share his view in the press conference will be less than what we have become accustomed to with previous Chair Jerome Powell. Expect shorter/sharper answers to questions in a more cautious communication style. On the surface, recent months’ job increases have been very strong, however a spurt in hiring in the hospitality sector will only be temporary and will reverse once the Football World Cup is over. We have not seen any increase in employment in the manufacturing, energy, housing or transport sectors over the last 12 months. Employment growth is very narrow, and it will be interesting to see if Kevin Warsh views the strength in the economy as sustainable going forward, given that it is almost entirely in the healthcare and hospitality sectors.

We expect Kevin Warsh to project a very neutral outlook for the US economy and also for interest rates. The financial and investment markets are in for some disappointment if they expect some fireworks at his very first meeting.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.