All mortgage rates will be above 6% over the coming year, Kiwibank economists believe.

This will make rates well over double what they were a year ago.

At the moment the mortgage rates range from around 4.4% to 6.9%, the economists say in their weekly First View publication.

"Mortgage rates are rising, and will rise further with expected RBNZ [Reserve Bank] tightening," Kiwibank chief economist Jarrod Kerr, senior economist Jeremy Couchman and economist Mary Jo Vergara say.

There's a strong consensus in the marketplace that the RBNZ will raise the Official Cash Rate on Wednesday by another 'double jump', that is by 50 basis points to 2.0%, following a 50 bps rise in April as it grapples for a handhold on the galloping (6.9% annual rate) inflation. The RBNZ is effectively 'bringing forward' its earlier forecast rate rises in an attempt to get ahead of inflation - though it was at pains to say in its last OCR review in April that it didn't see the endpoint of rate rises being any higher than previously forecast.

"All mortgage rates on offer are likely to lift from the current levels of between 4.4% to 6.9%, to 6% to 7.5% over the coming year," the Kiwibank economists say.

"More than 60% of outstanding mortgages are either floating, or rolling off fixed rates this year.

"The impact of the RBNZ’s tightening is being felt now and will continue to weigh on household budgets in the year ahead."

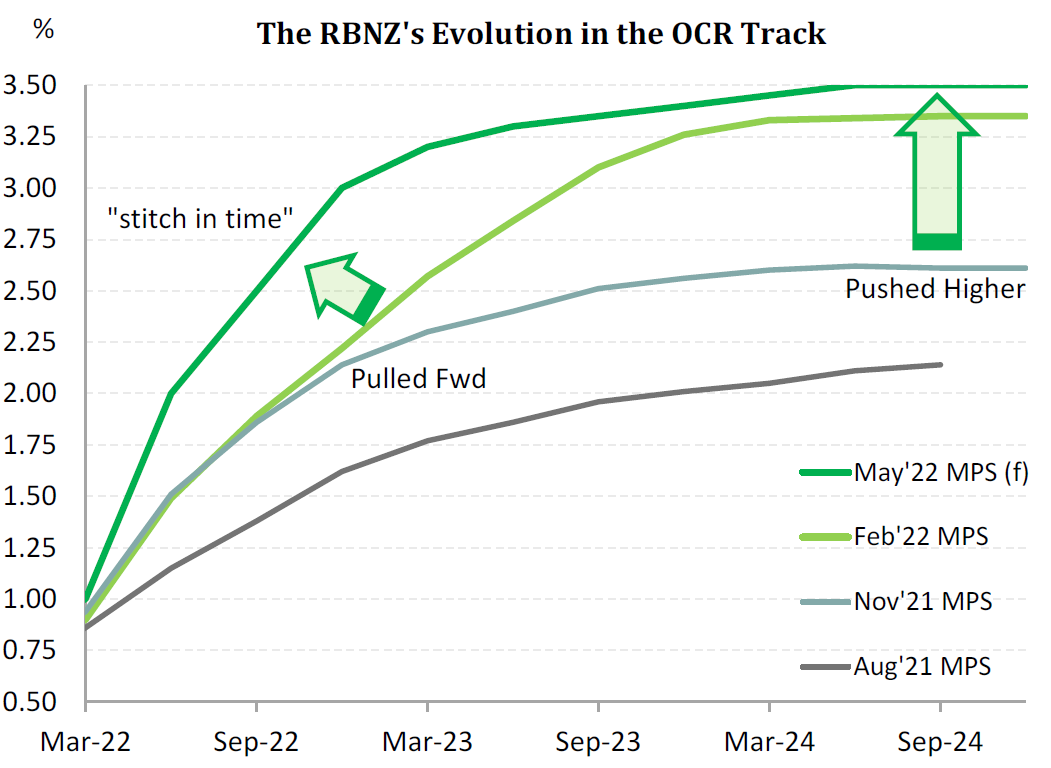

The Kiwibank economists will be closely scrutinising on Wednesday [and they most certainly won't be alone] the RBNZ's latest 'OCR track' that will appear in the Monetary Policy Statement. This 'track' gives the RBNZ's forward estimates of where the OCR will be over the course of the next three years.

"The OCR track will have been pulled forward, to take account of the two 50bp moves, and pushed higher - although we don’t expect the end point to be materially higher, given the 'stitch in time' approach," the economists say.

"We expect to see the end point lift from 3.35% to 3.5%."

"We suspect the RBNZ will [actually] stop around 3%.

"Why? Because the impact of every move to date, and from here, is causing a material impact on the housing market and household consumption. Cooling the housing market and taming consumption is the desired impact of rate hikes.

"And we’re forecasting house prices to fall by around 10% by year end. Consumption growth will wane as households face the negative wealth effect of falling house prices and a continued cost-of-living crisis.

"Of course, it’s easy to say that the risk of a recession rises with every rate hike. Recession risk is why we expect the RBNZ to pause at 3% - and not follow through with its forecast tightening in entirety," the economists say.

"If we’re right, wholesale markets have too much in the way of hikes priced.

"The terminal rate implied in interest rate markets is closer to 4%. We expect to see a slight rally in rates, lower yields, as the market realises fewer hikes are likely."

They are forecasting the RBNZ to move back to 25bp moves beyond this Wednesday, and with the 3% cash rate by November.

"Come November, the housing market is likely to have experienced a 10% decline in prices. The negative wealth effect will have dampened consumption, and the cost-of-living crisis is likely to be lingering. We suspect a move to 3% will be enough to turn the Kiwi economy and tame the inflation beast.

"We simply think the economy will struggle with aggressive tightening to 3.5% and beyond," Kerr, Couchman and Vergara say.

128 Comments

This is not good at all for businesses, and jobs! People are already starting to reduce spending and it will get worse. This means some businesses won't survive, their employees will lose their jobs… 2023 is looking bleak indeed, recession time in my opinion.

At least, a recession will take care of our high inflation. TBH a recession is well overdue, it will weed out the weak and, once we recover, make the whole economy stronger

Unless of course Jacinda and Labour decided to "save" everyone and give more money to the unproductive, paid for by the productive people. Aroha, care, love and bullshit!

(and yes, I do realise, I'm having a conversation with myself LOL)

No,thats what Luxon has promised to do by reversing the removal of mortgage interest deductions...

And you seriously think landlords will pass on a rent reduction as a result?

Its a Tennant Tax the interest deductability.

They spinned it as a FHB booster/helper.

Why should long term, permanent tennants trying to raise 4 kids in an already expensive rental - half paid by tax payers money in some form of benefit - have to deal with huge rent increases to cover this Tenent tax is beyond me.

Labour have never hurt their own supposed voted base as severely as they have this single term in gov.

Why should the taxpayer be subsidizing people to take out massive residential mortgages often on interest only terms (because that's the deductible portion) becoming tax neutral at best and displacing aspiring First Home Buyers from a fair shot at home ownership?

I understand "business expenses blah blah" but there's a huge difference between a business that pays company tax, collects GST, collects PAYE and keeps people employed vs someone leveraging equity into a down payment and undercutting FHB with the increase borrowing power (20%+) with IO lending?

Further to my comment. I have a perfect solution to the Interest Deductibility issue for landlords:

STOP BORROWING SO MUCH

For some reason that only applies to investors because they are "good at business"

Personally haven't borrowed a cent for ages but still have significant mortgage debt and pay a great deal of money for the use of the banks money (that's what "interest" is for those who failed 3rd form economics) - I still have to pay the bank for the use of their funds - but somehow it magically disappears from the profit-loss statement my accountant generates like as he does for all my other businesses that do allow financing costs as expenses.

Risk weight higher mortgages for Landlords to stop the silly speculators going to the LVR limit every time they can in the hope of cap gains. The 40% LVR for landlords essentially has done this already.

See no reason for this extra TENANT TAX to add to already struggling tenants. All my under market value rents have moved up over the past year, still some under market, but these will move up too. Where will the tenants go? Let them eat cake and give them all spots at the Hilton hotel?

Ridiculous mistake which even IRD and Treasury said NO, DON'T DO IT.

Well said. Sounds like the removal of interest deductibility is throwing the baby out with the bath water.

They could have banned mechanisms such as interest only mortgages and equity leveraging to help even the playing field with first home buyers. Although even the equity leverage is a difficult one, if the equity is derived from paying down a loan or making improvements, then that equity does effectively belong to the investor.

JJS,I was being sarcastic in response to Yvil, as in Luxon's reversal would "give more money to the unproductive, paid for by the productive people."

Landlords being unproductive & tenants being the productive.

In my opinion,this change has been the most effective in cooling the 'investor/speculator' frenzy.

It would be criminal to unwind it.

The main threat to the nz economy and the RBNZ’s being able to achieve what it needs to, is candy bring handed out before the election.

The unfortunate reality is that to tame inflation we all need to have far less wage increases than our cost of living.

sucks, but is the reality.

Then let in bloody workers, even those earning 50k - thats skilled enough to pick fruit, be a care giver in a rest home.

But no - barely a nurses wage gets them in - and we need more of them too!

Yep the few people on here that said rates rises were impossible are about to be spanked hard.

Getting a little kinky, Carlo...

Who said rate rises were impossible?

I think what he is referring to is the rhetoric going around last year from various sectors that interest rates were going to stay low “for some time”. Obviously any comments made by the likes of banks, RE agents and economists needs to be taken with a pinch of salt.

And any comments made by Adrian Orr need to be taken with a pinch of salt, unfortunately.

Orr has been pumping the debt bubble for years now. He was the one that said rates would be "lower for longer". He is the one that made a big deal out of negative rates... and got the population all excited about how negative rates were just around the corner. He is the one who told retirees and savers that they needed to go "further out on the risk curve". He is the one who pushed the "wealth effect" like a dealer pushing crack to school kids.

What RE agents say has zero credibility - always.

Businesses will be fine, they will just increase prices, there is already more jobs and not enough workers.

rbnz need to keep lifting up to ocr level to cool down inflation is this is what they want to do but i have my doubts

hum, I don't think businesses will be able to "just increase prices", not when a lot of people's income is being eaten up by 1) inflation and 2) higher interest rates. $10 coffee? $20 beer? I don't think so

You may have two options Yvil....

1. Increase prices/revenues to avoid negative cash flows.

2. Chew into retained earnings/increase debt while your costs increase (including debt servicing costs).

Or pray to god that disinflation comes back asap.

Disinflation. Now there's a sugar coated, pink coloured, gooey piece of verbiage. A lot like negative growth really. Changing labels can really make these events a positive experience.

A few decades back, there simply wasn't the incredible prevalence of cafes and restaurants. With the prices relative to wages, people simply couldn't afford to eat out all the time. And without mass migration, there wasn't the availability of cheap, readily exploitable labour with which to run hospitality businesses, which would mean you'd have to pay a local and they'd need to be paid enough to live.

Perhaps without the artificial stimulus of "wealth effect" (pulling spending from the future) and mass migration we'd be in a more similar reality now.

I attended a Simplicity webinar today covering current global market conditions. Sam Stubbs quoted the inflation adjusted value of a cup of coffee daily since birth invested in shares at an average historical return would result in $81861 at age 25 & $655130 at age 65.

Tony Alexander may have had a point a few years ago when he got a lot of stick for commenting on Millennials and their addiction to lattes.

All true of course, but how many newborns can afford to invest that amount from birth, and the real value of $655,130 65 years from now is?

Plus if the parents of that newborn had decided not to have that child, and had put that money into that same investment, then look at how much a better investment that would have been over having a child.

Could be a case of knowing the cost but not the value.

It's like the whole Home Ownership vs Renting & Investing the difference scenario. Let's say you're 30 and ready to buy a house:

- Median House Price $850k / $680k mortgage @ 6% on 30 year payment terms.

- Annual rates at 0.5% of property value, then increasing 5% p.a. Insurance also 0.5% of property value, increasing 5% p.a.

- First year ownership = $57k

- Median Rent $26k ($500 per week) increasing at 3% p.a.

- Invest $170k deposit and difference between home ownership costs and renting into NZX50 returning 8.84%

It will take 11 years for the investment to grow enough to buy that house (when subtracting rent costs), assuming house prices stagnate. I'd love to retire on a $10 million nest egg after 35 years of investing, but I'd much rather guarantee my child goes to one school per age bracket among other things.

From November insulation standards are doubling for new builds. Also double glazing Al framing needs thermal breaks (sensible but to make it law simple piles on the costs to every single new build) - And you think in 10 years there is any chance in hell that building a new house will be cheaper?

Min wage already over 40k. Labour have killed the tenants and those who ran sensible legitimate rental businesses providing needed roofs over heads just to please the 1 in 5 home buyers who are looking to buy their first home who complain prices are too high? They actually aren't as there are tons of cheap apartments, or outer suburb small dwellings - but Z gen value status more than anything and think they deserve a quarter acre freshly reno'd home in a great suburb (most owned by people who have been upgrading houses for 20 years+).

And the best thing about it is now that prices are falling they all run scared and still won't buy anything as don't want to lose their deposit as prices fall 200k.

The sympathy and tax dollars given to the 1 in 5 first home buyers by this govt at the expense of the 4 in 5 who they are so called "competing with" is crazy. But it guess it all balances out when these same people looking to buy their first home are smashed by this tenant tax with rents off to the moon.

I dunno Simon, rental listings increasing, rental prices decreasing, rental costs increasing, rental yield decreasing. Working age population is decreasing, suppressing rental demand, making investment less viable (those who can/want to pick up sticks, are). The tenant tax, well we'll see if it's possible to pass that on to the tenant in a year or so.

Wouldn't say that when the median house price is ~10 times the median household income that house prices are not too high. Sure there are apartments and outer suburbs that are cheaper, but the prices there have been driven up also due to gentrification. In fact it's the lower quartile homes which have had the most significant increase in prices, which in many cases are small apartments and outer suburb homes.

1 in 5 FHB? Not sure again.

Houses are worth what people can/are willing to pay for them so if Gen Z are turning their backs at the idea of becoming a slave to debt, then that is entirely up to them.

I would love to know the assumptions behind their model? Does it take into account tax and finance fees? Also, over what time period? I’m suspicious of these claims as the presenters have a vested interest….they collect the fees.

I worked in an agency environment towards the end of last decade. Many 20-40 year olds (my age bracket) talking about the avocado on toast theory and how silly it was to think not eating avocado on toast would amount to significant savings. I'd then observe these same people buy lunch every day of the week, brunch in the weekends after the regular expensive night out. Take out coffee at least once a day and various other snacks. The discretionary spending blew my simpleton mind. Heard a story of a barista in Auckland earning over $100k making coffee, on which planet do we live again?

Very specific reference but you can really see the metaphor of the avocado here... there will be some forced lifestyle changes and some may not like it. Better to buckle in now.

I suspect at some point, you're either consigning yourself to a live of abject misery and still not being able to save as fast as prices rise, or you might as well just have something in life to look forward to. For every story you have about people buying lunch or getting OTP, I have three of couples who I just stopped saying because they never came out or could afford to anywhere after saving, frequently only to end up further and further behind the market. That's the problem with anecdotes. They're just anecdotes, not meaningful data - like the documented statistical decline in housing affordability relative to incomes, for instance.

People just need to cut back on wasteful spending and saved 150% of their pay every month like the boomers did.

Absolutely agree. I can’t imagine trying to save a deposit through 2019-2021, the necessary savings cost just to keep the same % deposit would have been insane. Still surprising there are FHB over stretching now… though the trends for DTI and BGI are changing. The required income and deposit needed now is exclusive and unsustainable.

I was referencing more the lifestyle changes that may be enforced due to recession and the impact that may have on local eateries, cafes, “clubs” even.

Although Im a bit older, after going through a marriage bust up in my 30's and deciding to start a business instead of buying a house, the housing market became a real source of misery for me. I still dont own a house, have a successful business, I decided to live a life less ordinary, bought a yacht, and will be sailing away next year. I made a call 3 or 4 years back to not get involved in owning property. A one man protest.

As long as you now know that not purchasing a house 3 or 4 years ago turned out to be a mistake and can just accept that and move on no problem. Its those that could have bought a house and didn't that are still trying to justify their position that are now pissed off that I have a problem with. Sure nobody really knew house prices would go crazy but historically they only go one way if you zoom out on the graph.

Something something “starting a business that became successful instead of buying a house” “was a mistake”.

I believe there in lies the instability of the NZ economy.

Carlos - by historically you mean since the 80s. House prices have actually had many booms and busts in NZ. They fell significantly during the 1930s depression. They also fell by 40% in real terms in the 70s but that was masked by high inflation. They also fell by about 10% (nominal) after the GFC. However that average concealed the sad reality that many sales were forced sales, due to the recession and some buyers drove really hard bargains.

Tony Alexander thinks there is a 50% chance of a recession in NZ but reckons there won’t be big price drops or many distressed sales, due to factors like the high level of job security.

Im seeing a lot of rentals and development properties on the market in my area of Auckland. I reckon some ‘specuvestors’ will be feeling the pinch.

The funny thing is I believe owning a house is a mistake, the penultimate ball and chain to living if you will.

You only get one shot at this life, being a debt slave wasnt on my bucket list when I was 10.

Yeah, exactly. It's all very well cutting out every luxury when there is a reasonably short time frame involved. But when you are cutting out every single luxury - and curtailing time spent with friends in the process - and the result is that if you spend 10 years doing this you might be able to buy a pretty crap house somewhere and then spend the next 30 years cutting out every luxury in order to afford said crap house, then things are a bit different. Particularly if cutting out a small luxury (like fish and chips once a week) is only really the difference between achieving ownership of a shitbox in 10 years rather than 11. If your timeframe for saving is as long as ten years, then the live you live in the meantime has to be tolerable. Not buying any new clothes or having takeaways and never meeting friends for coffee or having people over for drinks for a year or two might be doable - do it for ten years and you'll have no friends and likely no undies in a wearable state.

Kind of ironic that the recession/depression that the government wanted to avoid resulting from covid, all they managed to do was to delay it.

This is what happens when incompetent clowns sit at the helm of the RBNZ and the Government, in their delusional thinking that free money, ultra-loose monetary conditions and a ballooning housing Ponzi would have no side effects to the real economy.

but changing to National would just install a new batch of incompetent clowns, if Luxons hair brain schemes are anything to judge it on... they all (including Jacinda) put politics before long term successful cross-party decisions so are doomed to repeat stupid mistakes or in the case of National enrich the already rich at the expense of people who work hard but dont profiteer and extort.... like property investors do...Chloe Swarbricks my vote and as a boomer thats saying something...

yeah I reckon Chloe and the IMF will be running the country in five years time if we aren't careful

If you were paying attention, we were about to slide into a massive recession before covid. Covid just gave the governments a perfect cover to kick the can down the road

Every major economy in the world literally froze at the same time for months. There was always big negative aftereffects coming, even if it wasnt due anyway before covid. All any govt can hope for is that they can move through it slowly with minimal damage. The idea that these times can be perfectly navigated with no negative economic effects from a 100 year pandemic is ludicrous even in a boomer forum like this

Kiwibank effectively acknowledging what many people seem to have a hard time understanding. It doesn't matter much what happens to the OCR, mortgage rates are heading up regardless.

Agreed some people here don't get it, the 4 major banks are no longer New Zealand banks and their rates are going to do whatever they need them to do. You have to laugh at the economists, a year ago they said rates wouldn't even begin to rise until 2024, yeah right.

This is how we dampen inflation. We take more of our money and we send it to Australia. Thus, we have less of our money here to spend buying from each other.

More fool me for listening to them, despite being a regular reader of this site.

Is raising interest rates really going to help if the inflation is coming from inelastic spend on fuel, food etc.

There is discretionary spend in this sure but not too much in terms of traveling to work and buying groceries

Yes higher interest rates are going to stifle inflation! I understand the argument "inflation is caused by a scarcity of goods", but still, when you have no more money left to spend… well, then you stop spending

We do need to be careful, our tradeable inflation will continue and indeed our producer prices are heavily influenced by price of fuel, machinery and sub-products.

Just because we cannot afford the products does not necessarily make them cheaper. In an ideal world it means we choose like-products or do without where we can.

If you think the logic of raising rates to reduce inflation is mad, then you should think what we've done the last 20-30 years in the reverse is equally as mad. i.e. dropped mortgage rates to zero so that people had 'spare money' to compete with one another in the economy and create aggregate demand for that level of supply of goods and services. Oh and creating a massive debt/asset bubble.

I do think that the previous 20-30 years is equally mad yes.

But the situation we are in now seems to be that we lurch from one extreme to the other, is it not reasonable to plot a middle ground between the two? Make a change, wait a couple of months and see if it is better or worse and then either reverse it if it is worse than before or keep it if has had the desired outcome...

Reasonable middle ground went out the window back in 2020 when we had emergency interest rate cuts and removal of LVR's when we had a 'sniff of deflation' (not even measured deflation!). And now here we are pumping the economy with -5% real rates, stimulating the economy with inflation at 7-8% as asset prices start falling.

Its pretty crazy stuff if you have an interest in the history of inflation and interest rate settings.

Debt to income ratio should have been in place 10 years ago as the OCR was being reduced if you want to think that we should be using a middle ground approach.

We pumped the market up so much now that the middle ground option may not be an alternative until the bad debt gets ejected from the system and we have a more balanced economy where incomes a related to debt levels at a more rational level.

I do think that debt to income ratio should have been in place for at least 10 years, probably more like 20 or 30?

Going forward it looks to me like either major party seems to want to further tax the productive areas of the economy to subsidize the less productive areas. Whether it is allowing the property investors to write off their interest for free capital gains or if it is not adjusting income tax brackets to continue to up benefits and WFF etc it doesn't really matter...

sooner or later the piper must be paid

A reasonable middle ground would have to be an OCR level between 4% and 5% right now, considering the current monetary and inflation environment. People do not want to understand that even an OCR at 3% would still be very loose and excessively stimulatory under the current conditions, Sorry but it is time to pay the piper, the fools' paradise of excessively loose monetary conditions has finally gone, and it is high time that monetary conditions finally start normalizing once and for all.

We could go full Turkey and cut rates instead, like our great mate Erdogan.

what a full on balls up that is. 70% inflation last time I checked.

Perfect example as to why religion needs to stay out of politics / economics.

I have a friend who lives in Turkey, everyone is in employment (in his sector at least) and their wages are going up regularly but they are never sure how much things will cost. There is therefore a real handbrake on planning as it cannot be risk-managed.

Turkey is going through a lot of pain to rebalance an overly dollarised economy that was being milked mercilessly by overseas investors taking quick gains at their expense. I don't think the process is being handled well at all (they should have implemented capital controls like Russia) - but it's too early to call it a failure. Revisit the story after the summer tourist season.

I think the average Turk would see Erdogans measures as a failure that make our clowns look almost credible.

I think the average Turk would see Erdogans measures as a failure that make our clowns look almost credible.

I think 80-90% of the world's population would swap their government for ours in a heartbeat.

We moan about our politics like a nerd turns down a supermodel for having pointy elbows.

Yea can’t stand pointy elbows.

Quite an aside,but being a figurative artist of 40 years practice, pointy elbows and other similar surface expressions of underlying skeletal forms ,always are more obvious in lean figures which make up the highest prevalence of models.

So it is a feature ,not a bug!

I think the 'dampened consumption' is already occurring, so it will be interesting to see whether or not

a. OCR remains under 3% in 2022,

b. OCR achieves and remains at 3% or

c. the OCR goes above 3% in 2022/2023.

So Kiwibank appears to be leaning towards 'b'. "All mortgage rates will be above 6% over the coming year, Kiwibank economists believe...We suspect the RBNZ will [actually] stop around 3%". About 1/2 of their rates on offer are already over 6%, however it will be interesting to see whether the OCR does get to and stay at 3% or above in 2022.

I think there is much more uncertainty and instability to occur in the world and NZ during 2022 which makes 'a'. more likely - time will tell.

It is also always 'interesting' when banks, even NZ ones, make statements and predictions on OCR and that all rates will be 6% and above in 2022 and have their featured 2-year rate at 5.19% as an advert in the mortgage rate sections. Are they sincere, trying to gain market share or both?

the big question is what will happen with the price of Oil and the value of our dollar.

Oil hits $150 per barrel (a real possibility if Russian Oil gets taken right off the table) and our dollar hits 50 to the USD, we are in for a world of hurt, OCR will have to keep being raised just to stop the rot.

98% of the economy relies on Oil, just think about that for a moment.

And of course we do not refine the product here anymore.

Funny how we now view 6% as “high”. This is just a return to the lower end of normal.

People now assume shaping an economy around a debt bubble is 'normal'....and things returning to 'normal' as being 'abnormal'.

Yes 6% is not high, but how quickly we have gone from 3% to 6% has been significant.

Flip side...Part of the problem was how quickly rates went down when it was not needed, and the crazy low rates post GFC for to long. We avoided taking our speculative medicine, and put bank profit ahead of the interests of the voting public.

And here we are today with no options and inflation destroying the tax paying part of the economy. Property speculation has been a net tax avoider...not generator.

What to do....

Yes, and the OCR should be at the very least 5% right now, which after all would still be the lower end of normal in the same way that 6% inflation is the lower end of normal.

The rate increases so far - coupled with higher priced goods and services - are already biting hard into disposable incomes. As people roll onto new mortgage rates, this is going to accelerate the transfer of money from spenders to savers, demand is going to collapse, and we are going to throw tens of thousands of people on the dole... and for what? To reduce house prices? Talk about a hammer to crack a nut. If we want cheaper houses - just constrain the availability of credit harder. It's not as if higher rates will make a jot of difference to the 'cost of living crisis', which is driven, in the main, by offshore factors and higher costs of credit.

I look with some envy at Switzerland - where inflation is running at around 2.5% whilst their neighbours wrestle with near double digit price increases. Switzerland has focused on food and energy security, strong scrutiny of prices and profits, and an export market focused on high value products. Imagine having a plan to achieve something like that?

"demand is going to collapse, and we are going to throw tens of thousands of people on the dole... and for what? To reduce house prices?"

What is the alternative? Not raise rates in synch with the Fed?

Remember Orr saying the only way to avoid a depression was to 'lend, lend, lend' back in 2020.....so to avoid a depression we've pumped house prices another 30-50% higher....increasing the debt load/drag on the economy and increased financial risk.

Lending money to a residential property market that was already overcooked to avoid a depression was the economic solution of a mad man (in my opinion). Absolute last gasp desperation.....

Now you know that I agree that, given our policy and tax settings, pumping cheap credit into housing was monumentally stupid. But, using monetary policy alone (hiking rates) to: tackle price increases driven from offshore, hold our currency value; reduce consumer demand for goods in short supply; and, deflate our house price bubble... all whilst maintaining 'sustainable employment' (the feted soft landing) is even more stupid. It's like trying to land a helicopter in a strong wind by only using the throttle.

Even if all of the inflation is imported, keeping the ocr low will make it worse via the tanking of the nzd.

realterms - the market has already given it s decision on NZ$ and by association the Govts policies - NZ$ down 16% - milk prices consistently down so the future looks at best tricky and we have a juggler (Grunter) juggling for the first time with hand grenades minus the pin!

If we want cheaper houses - just constrain the availability of credit harder.

Constraining credit reduces its supply. When the supply of something goes down, its price goes up. Interest rates are the price of credit.

There's no escaping the fact that interest rates are heading up, regardless of what we do. It's not a decision we get to make.

Yes and in theory as the risk of default rises on mortgages, the lending rate should go up, not down. Yet we've done the opposite, when the default rate was rising, we reduce rates. Which is back to front. Same with the debt markets....we have zombie companies out there, but the cost of debt has been falling because central banks have been buying the bad debt to support a broken economy. Crazy stuff.

IMO, this is what's behind Grant Robertson's rush to implement a taxpayer insurance scheme for mortgage payments. It will be taxpayers paying the cost to hold house prices up and keep banks in gravy. A two-tier welfare system where the beneficiaries are property and banks.

Agree....bonkers...

That's a very narrow view. Market rates (and therefore mortgage rates) are a function of what market players think the central bank is going to do, coupled with the market's risk assessment. The central bank is not a passive follower of the market by any stretch - particularly if it is willing to intervene forcibly. Attaching a price / supply graph to something so complex is classic 'reckonomics'.

I am not seeing it's happening yet. Just go to the mall and see how many people there, how busy the road is during the weekend. I don't see any slow down for our economy yet. Yes the current mortgage holders has been hit hard but mostly the FHB for the last two years. For mortgage holders had been holding mortgage well, they are still in ok position as their equity is still good, mortgage had been paid down for quite a bit. People who sold their properties at the peak last year, they had extra capital gains and spare money to spend.

All a fair challenge - and the amount of people that paid off their mortgage in full at the back end of 2021 was very very high - around $12 billion in final settlements per month from memory (nice to have the money to beat the rate rises eh?)

It is easy to see the trend you expect in the data - but I think the point of inflexion was a couple of months ago. Look at under-utilisation rates, actual earnings, card payments, mortgage drawdowns vs repayments, heavy goods traffic, jobseekers allowance, etc. They all have the same profile as the NZ Activity Index - a stall in mid-2020, followed by a boom resurgence a year later, and now a depressing looking slump to below pre-COVID levels.

Jfoe - an excellent comment - there may be an opening at RBNZ later this year just enough time to be considered for an opening in Nov 2023 to an even more influential position, pity more people don't see the woods for the trees.

Look at the trends with an objective eye

If your plan includes existing close to the middle of a large prosperous market, then sure, copy Switzerland. We have to forge our own path because there's not many developed economies situated geographically like we are.

My point - and reference to Switzerland - is that there are benefits in having an actual plan for what we want and need from our economy. It is particularly important for a small country like ours to get as close to food and energy security as possible so that we are better insulated from the global chaos of today and tomorrow. We also need an even trade balance (at least) so that we are not reliant on flogging financial assets to maintain the strength of our currency.

Oh I agree. And parties should take the plan to the election. An actual plan though, not soundbites. Hard to do in an MMP environment though.

Switzerland enjoys the benefits of a fantastic trifecta:

1) high levels of education

2) a hard working mentality

1) & 2) create high productivity

3) a low corruption government which reinvests its high productivity in its country in high quality infrastructure

Don't forget

4) historical tolerance of Swiss banking practices which siphon in all sorts of dodgy money.

Incredible banking sector revenues, essentially that is the oil of their economy. They are as singular in their economy as we are in ours.

There are also many top pharmaceutical companies such as Roche, Novartis, ever heard of Swiss watches? Swiss chocolate, cheese, tourism, the best ski fields in the world

Multinational corporations choose countries such as Switzerland (8%) for low corporate tax rates to facilitate profit shifting transfer price tax avoidance

Sure, those things are good, but I think we can all agree that Swiss banks are top of the list.

They’re really good a money laundering :)

Weird that you forgot to mention that it is a tax haven. How come you left if it’s such an amazing place?

Be nice to see NZ governments more focused on investing in education and infrastructure than blowing housing bubbles.

'If we want cheaper houses - just constrain the availability of credit harder.'

So what you are saying is make it so difficult for people to purchase housing they can't afford it, so people will then have to drop their prices to meet the market?

Doesn't work.

South Korea has very low LVR's yet still has very high house prices to median income multiple.

You can't fix a supply restriction by putting in a demand restriction. All that will happen is less supply in real numbers and still high prices.

If you want affordable housing, you need to remove supply restrictions.

House prices rise and fall in perfect unison with the availability of cheap credit - they have done in NZ since 2010. There is an underlying trend, sure, but cheap credit fuels the booms. Constraining credit on non-owner occupied homes, coupled with an expansive public / social housing programme, investment in infrastructure, a well-resourced ministry of works, a rental WOF and landlord register, etc would bring house prices down.

These rates are low compared to other times when inflation is high. The problem is a lot of naive people thought rates would stay low for years and were able to borrow way too much and will now be in a tuff place for years as rates raise pushing payments in some cases out of reach.

This is just a massive shock to a generation that never ever witnessed a rate hike and were told repeatedly there wouldn't be a hike until the foreseeable future

This is just a massive shock to a generation that never ever witnessed a rate hike and were told repeatedly there wouldn't be a hike until the foreseeable future

No generation in human history has seen rate hikes into a debt bubble of this magnitude

That's just like no-one is history has seen a falling rock stop fall and rise against gravity. The 2 existing at once can't happen.

"Rate-Hikes" are going to be many times watered down from the last decent rising cycle 2004-2008.

OCR peak 2.75% (but the banks would love to freak ya out to get you locked into those 6%+ long term rates on their way very soon; shorter term I'm still liking)

Stay short - girls might not like ya but at least you can move with what I'm seeing as the most volatile and unpredictable economic periods in history. Recession on the cards far sooner than people realise.

Fed not meant to but the excitable US stock market crash that is slowly happening will even have them pull back as they realise a 2% rate rise in todays debt filled society hits just as hard as a 10% rise would have if there wasn't so much debt floating around.

Is this designed to help people or to scare people into locking long term with them?

Interesting question! I would be very careful about locking in 5 year rates

I fixed in the 3s through till 2026-2027. It’s looking like a good decision right now. I should be paid off by the time the term is up.

That was a good call, I meant I would be very wary of fixing now and in the coming year for 5.9% and higher

How come? If one can afford it I don't really see the problem.

Sure, if you like certainty, lock in 5 years. I would be wary of locking in for 5 years at 6% today and higher in the coming year, because I'm of the view that interest rates are going to start falling again by the 2nd half of 2023. IMO the one year rate might peak at 6% then drop again. If I'm right, locking in for 5 years at 6% or higher will be a significant waste of money

I locked in 5 years in December (4.95%) for the certainty of payments. Also a case of opting for the lesser of two evils in uncertain times.

I'd much rather "waste money" if rates do drop but be comfortable with my payments for 20% of the loan duration, than come out of a shorter fixed term into considerably higher rates.

If the bank sees the rate dropping then definitely love to see as many people lock in for higher and longer terms.

I guess they will need to stress test at 9% then...be interesting if new builds take a hit as most are on existing expensive land and they still need to sell for 850-1 million given what the builder has got in the property (labour,materials etc).

seeing heaps of completed new builds on the market in west central Auckland at the moment. This is a huge shift as the were tending to be all sold off the plans or during construction up until a couple of months back.

These need to be sold to finance the next project.

Tough times coming and IMO they're accelerating towards us.

"They need to be sold to finance the next project", hmmm. Im past personal experience, and amongst developer friends of GFC time, they need to be sold ,so that the developer doesn't lose their own home break their marriage and end up" back on the tools," personally.

And the quickest sold and out the door with shirt and pants still on, are the ones that can take a breather and be capable of starting any new project at all.

Buying land( with or without buildings on it,or some other developers fire-saled consented land) again, at the bottom land value of the next cycle.

"Be quick!! "-Is to get out quickly.

When have economists ever predicted mortgage rates correctly ? They have failed to predict house price inflation and even have had conflicting forevasts about OCR . In short , all Economists pretend to know the future whereas the fact is no body has any crystal ball .

You always have to question why they are saying what they are saying... Is it just a coincidence that there's always statements like this just before an RBNZ announcement...

I don't know why but in the eighties it took more than a couple of tiny rate rises and a few months to get inflation in line . Maybe the huge interest rates weren't neccessary, if only we had a genius like Orr back then it would have saved a lot of pain . I remember the constant strikes by various groups and the ever increasing wage demands all contributed to higher inflation and interest rates being raised to counter the corresponding inflationary pressures. All that and we could've just kept rates at 3 or 4 % .

I think the lessons learned during the 80’s is the reason we will get things under control now. The rbnz ( and other central banks ) are behind the 8 ball, but the will hike aggressively now to catch up.

The other major factor is the much larger pile of debt. They won’t need to hike as far.

Wait... So kiwi bank expect all terms to be 6% or more - but agree with me that 3% is where the OCR will max out not 3.5 like most other banks?

That's a pretty sweet margin they have got going their on their shorter term funded money.

60-odd% own homes and vote (as they're generally older and concerned about the country, money etc not car, girls and trying to be cool Z-gens).

10% drop sounds really light as many have seen higher drops than that already.

Data is too slow - official reports of 10% drops will come around same time as 60% resetting mortgages this year and we already have the worse consumer confidence ratings since the GFC.

I feel prices are falling too fast, the internet speeds up the slow learners who were still buying last year - all Bulls now Bears - 80% of the RBNZ work already done.

Wouldn't rule out a 2.75% top out of OCR (overseas and unpredictables at play could easily cause this)

Auckland’s HPI is already officially down 10% from peak, but possibly 12% by now. If the OCR keeps getting hiked it’s highly likely by end of 2022 the fall from peak will be circa 20% for Auckland.

For an investor who has been buying houses for the last 20yrs and still owns several, a price drop will not hurt, as you have to look at the average price at purchase and rent will likely cover costs. Anyone who has purchased a house recently for their family to live in will just knuckle down and pay the mortgage, time will take care of any loss in value. That just leaves those who started buying additional property as investment recently in possible trouble as rents are unlikely to cover all costs.

In the end if the market drops most will sit tight.

I want to know how we make someone accountable for the epic negligence that has been on display since 2003 when house prices started to escalate. Its beyond belief, that having jacked up house prices to one of the most expensive in the world (with mortgages to match) the government is just sitting around while the RBNZ puts interest rates up on heavily indebted kiwis who had no options if wanting to buy a house over that timeframe. The whole system is moronic. Why weren’t escalating house prices considered “inflation”, and therefore worthy of interest rate hikes, earlier?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.