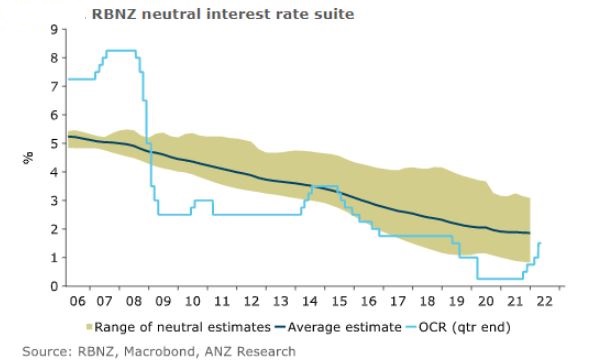

The Reserve Bank (RBNZ) is widely expected to increase the Official Cash Rate (OCR) by 50 basis points at Wednesday's review, taking it to 2% which is the level the central bank currently views as neutral.

The neutral OCR rate is the level where it's deemed to be neither stimulating nor constraining economic activity.

As ANZ's economists led by Chief Economist Sharon Zollner put it, estimating the neutral interest rate is a difficult task at the best of times. And with COVID-19 disruption "still everywhere in the economic data," it’s very difficult to accurately pin it down.

"However, we wouldn’t be too surprised if estimates of the neutral interest rate start to edge upwards, given the sharp rise in inflation expectations here and overseas. And it really matters what the RBNZ thinks neutral is, because they need to lift the OCR one for one with any increase in their estimate of neutral, otherwise interest rates can become more stimulatory, even if the OCR remains unchanged," ANZ's economists say.

Any upward revision in Wednesday's Monetary Policy Statement would increase the odds the RBNZ isn’t finished with 50 basis points hikes after next week, ANZ suggests. The RBNZ increased the OCR by 50 basis points to 1.50% at its last review on April 13.

As ANZ's economists put it, the policy outlook becomes more nuanced once interest rates are back into contractionary territory, or above the deemed neutral rate.

"Core inflation is clearly far too strong, and wages are accelerating. But at the same time, the RBNZ is hiking into a sharply slowing housing market. Our central forecast, which assumes no unforecastable downside risks materialise, predicts that the strong labour market will stop economic momentum from being completely flattened by the housing downturn."

"But falling house prices have the potential to dent consumer spending, through wealth and/or confidence effects, and it’s a pretty unpleasant mix for the construction sector, with construction costs up 18% year-on-year in the first quarter, even as the end product (housing) is losing value," ANZ says.

"In short, we think that the balance of risks around inflation and economic growth are likely to become less one-sided in favour of large OCR hikes over the second half of this year, and that should prompt the RBNZ to move in more considered 25 basis points steps over the second half of the year. But from this starting point, the tolerance for upward inflation surprises is nil."

Zollner expects an OCR peak of 3.5% in the current cycle early next year.

'Inflation is simply bonkers'

ASB Senior Economist Mike Jones also expect a 50 basis points increase. This, he says, is close to fully priced in by financial markets. However, what’s less certain is what the RBNZ does with its interest rate forecasts and forward guidance, which is what will shape Wednesday's market reaction.

"Clouding the picture a little are rising recession risks, both globally and in NZ. These up the difficulty rating on the RBNZ’s future interest rate decisions but, for now, the focus will remain squarely on the problem at hand: inflation. Expect no quarter. The path of ‘least regret’ for the Bank is still to get the OCR to a neutral setting, about 2.0%, quick smart, then adopt a more cautious stance from there."

"This front-loading approach will be enshrined in the Bank’s new OCR forecast track which we expect to show a much steeper ascent than the February Monetary Policy Statement, but not necessarily a much higher peak [of] 3.35% forecast in February. Something around 3.5% perhaps," Jones says.

"There will also be interest in whether the backend of the RBNZ’s OCR forecast bakes in an assumption of an eventual easing cycle. The May Statement will show forecasts out to June 2025 so we think the track will tease eventual cuts. They’ll be modest though. The Bank won’t want the market to get fixated on this aspect and lose some of the tightening baked into the interest rate curve. We still don’t buy into the full extent of this implied tightening given the traction the Bank is already getting over demand, and in particular house prices."

ASB's economists forecast an OCR peak of 3.25% versus market expectations of about 3.75%.

Jones say although it can be argued that much of the inflation the RBNZ is fighting is outside its control because it’s either sourced offshore or reflective of supply shortages, NZ is in the midst of a negative supply shock coming on top of a positive demand shock. Annual inflation is running at 6.9%, the highest it has been since 1990.

"Inflation is simply bonkers and aggressive action is warranted to ensure it does not become embedded in expectations, which would necessitate a longer and more painful tightening cycle. The Bank’s own ‘stitch in time’ analogy remains apt."

If a 50 basis points increase is delivered next week, the OCR will be at a neutral level, meaning the first part of the RBNZ’s job will be complete.

"From there, the least regret’s framework becomes more nuanced, necessitating a more cautious approach as the OCR enters territory on the tighter side of neutral. The Bank will likely move to a more data dependent approach as it seeks to balance restraining inflation expectations against risks of a hard landing down the line. We thus continue to expect the pace of hikes from July to November to slow to the regulation 25 basis points-per-meeting run-rate. Another 50 basis points lift in July remains a reasonable risk though and can’t be ruled out," says Jones.

Bang for buck

Kiwibank Chief Economist Jarrod Kerr also expects a 50 basis points increase to 2%. He then expects 25 basis points hikes until the OCR hits 3% in November.

"And that should be enough. With house prices likely to be off 10% by year end, and most of the mortgage book refixing between now and then, the RBNZ is getting big bang for buck," Kerr says.

According to RBNZ data, $206.5 billion, or 61.5%, of all residential mortgage debt will be affected by any rate increases over the next 12 months. That includes mortgages up for refixing and floating mortgages. As of March 31, there was a total of $335.447 billion worth of home loans outstanding.

Four consecutive 50 basis points hikes

Westpac NZ Acting Chief Economist Michael Gordon this week updated his forecasts, which now include four consecutive 50 basis points OCR hikes. Following the April increase and Wednesday's expected one, Gordon sees additional 50 basis points increases in July and August, taking the OCR to 3%.

"That came out of two considerations. First, monetary policy settings are still a long way from where they need to be. We now expect the OCR to reach a peak of 3.50% for this cycle, from our previous forecast of 3.00%," Gordon says.

"The second consideration was that the RBNZ’s change of tactics in the April review opened the door for larger OCR moves in the future. The April decision was described as 'a stitch in time saves nine' – early action to get on top of inflation would reduce the risk of having to lift interest rates to an even higher level in the longer term."

"We agree with the reasoning behind this. There is understandably a concern about the impact that higher interest rates will have on highly indebted property owners, especially those who got into the market recently when interest rates were at their lows. But the RBNZ would do them no favours by going easy on them at first, then ultimately having to lift interest rates well above what was considered to be the pain threshold," Gordon says.

Westpac notes house prices have now fallen for five consecutive months.

An unemployment headache

As reported earlier in the week, BNZ Head of Research Stephen Toplis believes the RBNZ has little option but to hike the OCR by 50 basis points on Wednesday. Toplis argues the lowest unemployment rate in decades, 3.2%, is a bigger headache for RBNZ monetary policy than the highest inflation in 30 years.

"The Reserve Bank’s task is clear. At its most basic level it has to get current annual inflation of around 7% down to 2% and it will require the unemployment rate, now 3.2%, to rise to around 4.5% to meet its maximum sustainable employment objective."

"The only way the RBNZ can achieve this is to keep raising interest rates until it gets the traction it desires. And so it will," says Toplis.

131 Comments

As of March 31, there was a total of $335.447 billion worth of home loans outstanding.

This figure here was of interest. Apparently the total value of NZ housing stock is 1.5 trillion dollars. So in basic terms there's around 20% debt to value, or prices need to drop 80% for the entire market to be in negative equity.

Perma bears might even wave around a 50 percent decline... to that I say pull the other one

Maybe, if there was a total economic collapse.

It is hard envisaging it otherwise, because you have to relate it back to what goes into a new unit of housing stock. Councils for instance seem to want a hundred grand or thereabouts to make a section. Whether that's a realistic figure of costs or councils padding their fees just to hop on the property bandwagon, hard to say. Regardless, straight away there's a hundred grand you have to factor in, right out the gate.

But doesn't that figure for housing stock include ALL houses? So houses that are no longer under a mortgage, and a significant proportion of old mortgages that have already had 15-30 years of repayments made on them. These properties aren't of any concern re negative equity.

So the vulnerable (mostly newer loans) might represent a third of that 1.5 trillion dollars (500 billion). So now it only takes a drop to about 66% to get a large number of homeowners under deep stress.

exactly, only a miniscule fraction of NZs homes sold in the hot air market of the last 18 months.

I sold one!!!!

Well done, you got top dollar.

Bank ecomomists agree for large interest rate increase. (Would all businesses in an industry agree their prices will go up?) After the new legislation constrains borrowing significantly so many borrowers cannot easily reapply for loans elsewhere. Perfect storm for lenders as what other industry can you increase your price and your customers cannot leave and are forced to pay more. IS this a coincidence? CPI is measured in weighting of a basket of goods, and who knows if this "weighting" is reflective of most hhlds? So as hhlds are paying more for everything ie. inflation, let's resolve this by getting hhlds to pay more for their hhld mortgage payments too. Seriously, people are getting hammered here. If our inflation is imported (as per Finance Minister), then why are Australia's interest rates no where near as high as ours? If our interest rates go sky high tackling inflation, but it is imported inflation, and other countries are not increasing rates like us, then imported inflation will continue no matter how high we make hhld mortgage payments. We are going to get ruined?

yeah that's why a lot of people warned about blowing a housing bubble

We created the housing bubble by dropping interest rates to zero while we imported deflation.

But nobody was complaining when that was happening….

Now quite a few people are complaining when the policy gets paid back in reverse as we import inflation …with interest…

That is an incredible amount of unproductive capital.

Indeed, and given that:

1) the market isn't highly leveraged at an average of 20% D/E. Recent investors and FHB are the most stand out exception.

2) the market is primarily composed of owner-occupiers, who when faced with declines in house values or sales prices, are likely to simply not sell as you always need somewhere to live...

Given that, why would you expect a large correction?

In my age set (40, kids) everyone is slashing spending to make sure they have enough for mortgage and COL increases. Nobody knows how bad it will get, so everyone is assuming the worst. These are all families in pretty decent financial positions who bought before the housing boom and are sensible (on the surface).

This, more than any economists prediction, tells me the OCR raises will falter sooner than expected, much as the increases came sooner than expected.

Exactly!

Maybe bank economists earn too much and only mix in elite circles.

Precisely NKT. Rates are now higher than pre-Covid and home owners are going to be worse off financially now than during Covid due to a supply side price shock. Utter ineptitude from the RBNZ who have been too busy plagiarising Maori symbolism (don't get me started) to do some basic central banking. Maybe they will blame it on Tane Mahuta?

And while they were plagarising Maori symbolism, they saw Maori homeownership rates fall to the lowest ever in history as the bubble expanded.

Exactly. It is essentially brown washing. There seem to be way too many organizations who seem to think sending the CEO to a few Te Reo classes an sprinkling a few words and phrases into their public material somehow makes up for failing to take concrete steps to actually improve things for Maaori staff and/or stakeholders.

I agree, nothing cringier than middle management types blithering on about the great "mahi" after showing no interest in any aspect of Maoridom until they had to.

There in is the key ‘until they felt coerced to’.

we live in surreal times. Those who covet power will act the role the pay masters want.

Tahi rua toru wha... I will be happy to speak maori fulltime when they learn how to behave.

It's not Maori who are enabling the plundering the wealth of younger and coming generations right now.

It's actually semi-mandated by government that its various entities incorporate more Maori language and custom into their operations and literature. There is some fairly sound logic there given Maori is an official language of NZ, whether people like that or not.

Yes, I should be clear that I've got nothing against that, and in fact think it is a good idea - it just should be done as well as taking more concrete steps to improve things, not as a substitute for, which in my experience it often seems to be. I've seen lots of places make a big song and dance about this sort of thing, while at the same time expecting their Maori staff to do tons of cultural support work to facilitate it when they are not compensated for that kind of work, it's over and above their usual workload, and it's not going to get them any promotions or payrises.

My issue with the RBNZ is a lack of sincerity, their use of Maori symbolism feel's shallow, forced and unnatural. This for example https://www.bis.org/review/r210511a.htm I personally find this offensive because this man would not have shown a blind bit if interest in Maoridom until he had to.

Show me how many Maori you have in the top 50 RBNZ or Treasury employee's by salary. otherwise stop using my culture.

Jesus.

- Firstly your people have been complaining about how the Maori language was "beaten out of them" (caned) at school, even though it was prominent Maori elders in the 1870s that petitioned for it to be banned. https://sites.google.com/site/treaty4dummies/home/maori-forbidden-at-sc…

- Then in 1972 your people started petitioning for the reintroduction/recognition of Maori language. http://teara.govt.nz/en/photograph/35951/maori-language-petition

- Now we're recognizing it and you're still complaining?

i know you're not that dumb, but you're giving it a red hot go changing my mind. Your references are urban myth's to make you feel better - except for the caning part.

Unless you are genuinely interested, I have zero desire to see you use my language because you want to get ahead in your job.

Here's a personal anecdote for you. I have always been genuinely interested in learning about te ao Māori. I reveled in learning te reo Māori at school until I moved overseas to finish schooling. More recently I worked for a kaupapa Māori trust for a number of years, where learning te reo Māori was required. I was excited and dove in; however, whenever I tried to speak with Māori speakers (whom I knew were at least competent, if not fluent) the majority would respond in English looking at me like, how dare you use my language. This became so regular I became too embarrassed to speak it anymore. I worry you may misread people's motivations for wanting to learn/speak te reo.

Just remember ngrrk, that when it's matters maori you will always be wrong. It's a rule, and worse it's a technique.

KH that's just not true and you know it. Nggrk, keep it up, the vast majority of Maori are with you. If you were disrespected I apologise.

You were always going to disagree Te Kooti. Thats ok. Butyou just called me a liar and that"s not

Careful.

Te Kooti doesn’t seem to be arguing that the language is being used but rather that there’s a very real drive in government agencies to incorporate Māori. whether the interpretation of that is to engage in the culture and provide more accessible pathways for Māori or to simply incorporate Koru into a logo and learn the Māori words for their values is the argument. The intention is the former so if that is not being heard then it’s not being done correctly.

Thank you Malamah.

The increased visibility of Te Reo is for Maori, to keep our culture alive and for us to feel a sense of belonging and identity. It's not for Christian Hawkesby to use to signal his virtuousness on the world stage when he almost certainly has no connection to it.

Can I also add that Te Reo is for all of us. Pakeha are always welcome to learn this, kapa haka etc, always welcome in our wharenui tipuna to learn and understand. I draw the line at it being used in a corporate environment to advance careers - that's my issue.

As for NZD's points, how miserable do you think thing's were for Maori that they had to consider walking away from their language? Google how the Maori Battalion were treated when they returned (and they volunteered),

Fair points. Apologies for going off on you, I love how we are embracing Te Reo in this country and it irks me when I read about people putting it down or questioning people's motives.

I've been passively learning Te Reo for a couple of years, starting off with integrating key words into English sentences when conversing with my now 5 year old daughter, now we're focusing more on complete phrases. She's attending a school with a heavy vision in Te Reo, Tikanga and Kawa. I was fortunate to attend her school Powhiri a couple of weeks back, where the "pale stale male" Principal stood infront of the school and spoke fluent Te Reo without referring to notes.

Seems no matter what society does to embrace Maori language and culture, you get chronic moaners like Te Kooti going into conspiracy mode and questioning people's motives. Telling people when they can and cannot use "Te Kooti's" language etc.

And then people wonder why stereotypes exist....

I absolutely question the RBNZ motives in appropriating Maori symbolism.

We are to judge each tree by the fruit it bears. The RBNZ has overseen the biggest fall in Maori home ownership rates ever. Maori are literally becoming tenants in their own land.

A very strong case could be made to say that it has been over 100 years since NZ had a high-ranking beaurocrat that was as destructive to Maori interests as Adrian Orr. We may all be too busy tied up in the hurly-burly and distractions of everyday life to notice such things. But I feel confident that the historians will judge Orr very poorly for what he has done to Maori. The whole "Tane Mahuta" appropriation thing is just adding insult to injury.

Thanks Fitz, NZD is missing subtle difference that this is more about Orr and the RBNZ using Maori mythology than helping Maori. I'm less concerned about home ownership because that affects all of us, but why can we not have a senior Maori banker talking to the BIS or our mythology? That's the issue.

We are certainly being a bit more cautious.

we front loaded buying quite a few things mid to late last year, which helps.

we aren’t really cutting back on cafe visits etc. still want to have a bit of a life.

I am certainly focussed on paying down a loan or two by late 2022.

Ok but if NZ slows faster than other countries and they stop raising rates, then our currency will fall, introducing higher import prices including petrol, and more inflation. The path will probably a be a combination of weak economy, lower dollar, and still high inflation.

correct, thats why RBNZ has to increase the OCR, but some things are out of their control. The strength of the spiral is strong...........

That's outdated orthodoxy. The NZ$ is weak despite us having a higher OCR track than all other Western economies. It will actually fall harder as the smart money knows higher rates will cause our economy to bleed out. It's not the interest rate differential.

The RBNZ are just going to have to suck up the current inflation and do nothing about it. They caused it, as long as wage rises are subdued the factors NKT discussed are already sending us into recession.

Sooo. It is a good point. But, even if you are right, things never go that way, unless it is unavoidable.

Those peps, the ones that decide... the only thing they want is to have a good salary, and that good salary keeps going as much as possible.

They don't want any accountability.

To avoid that anybody can point a finger to you, in big corporations, the only thing you have to do is to follow protocols. The older the better.

I have been there.

It doesn't matter if you are right or wrong. If what you are suggesting will actually have better or worse outcomes.

It doesn't matter how sensible (or not) your thinking is.

All it matters is that you can demonstrate that you followed what is considered common sense.

Being consistently wrong is better than being sporadicaly right.

You are always going to be blamed for Actions, rarely for Inactions.

TL:DR;

There are a subset of people (like me), without specific ethic or moral, that are just wired to make things work well. soooo... those peps are never ever going to be in the command chain. That is how democracy works.

Higher rates relate to higher risk and opportunity cost. Obviously there are better nations to hold one’s money in these times.

... which is why the brainiacs at the RBNZ need to be held account for behaving so recklessly with the OCR ... ... we were dealing with a nasty flu virus , not in the midst of a war or a depression ...

You only know that in hindsight…

No ... there were manifold economists , radio commentators , regular bloggers here , lots of voices piping up that the Reverse Bank's behaviour was reckless , foolhardy ... and , they were proven correct !

Yeah same here, even some of the tradies I know are starting to get a little nervous as their previous policy of just raising their rate as they wish is starting to run into less people looking to start renovations or new builds.... who knows they may even find their yearly earnings matching their declared earnings

Four or five consecutive 50 basis points hikes is what is required, I have little confidence that this will occur.

Required to do what?

Drive a stake thru the heart of the economy.

Precisely! What we have here is failure to communicate…. Nah…

Tis what open free market economies require is a reset.. to cut the rot out

By rot do you mean our remaining cafes?

Still a fundamental and ridiculous mismatch within the economists’ views. The views over at Macrobusiness in Australia accord with my own in this respect.

Taking the OCR to 3.5% will cause a deep, deep recession, large increases in unemployment and house price falls from peak of at least 30%. Yet none of the economists are forecasting this.

Go figure!!!

... as painful as a deep recession can be , sometimes an economy needs one to expose those who have been swimming naked ... to reset on a sounder footing ...

The housing market in NZ is wildly overvalued , and has unbalanced the entire economy ...

... we need that recession ... and a new RBNZ board !

yes in the states it was their stock markets that needed a considerable correction (which we already have -20% to date), but in NZ its mainly the housing market that requires the most correction. Happening slowly now as borrowers qualify for less under 7.2% stress tests. Auckland median down about 7% to date and falling.

I respect a lot of what Jeremy Grantham says. According to Grantham, a house price crash will be much more impactful for the economy than a stock market crash.

Impactful, yes. You wont have to borrow as much and sign away the next 30 years of your life to buy a house. I would say very impactful. Then go on, what about all the job losses in related industries.... We'll I say it's well imbalanced, obscenely imbalanced.

30 year mortgages have been the norm for decades now.

I'm not sure why there's so many people expecting that to suddenly not be the case.

Prices may drop but affordability, that being people's ability to pay for a house, only looks to worsen.

If they can overbuild Auckland over the next decade, maybe things might be different then.

30-year loan terms may have been the norm (well, 25-year was probably the norm), but it seemed the norm of them being fully paid off was far, far shorter and many were able to spend more in their 50s having paid off the house.

Think what happens when the stress tests are at 8%

HouseMouse I think we can both agree on the fact that we are all about to see what is more important to the RBNZ, is it house prices or is it inflation ? I see a couple more 50bps rises for certain, we are a long way off from smashing house prices yet. Orr is about to find out what the market will tolerate, no need to "Wait and Watch" on this one, the results kick in very fast.

... as I recall , it is written in law that the RBNZ's mandate is to maintain an inflation band of 1 - 3 % ... perhaps , Adrian Orr has forgotten that ...

The smoke we're seeing is Orr's overcooking of the economy ... the housing market ...

Its whether RBNZ protects employers or housing investors. I suspect the former dont want to give 15% pay rises and will apply heat on RBNZ behind the scenes.

Employers may not be able to give employees a 15% pay rise, on top of paying 15% more for the supplies and expenses… This only works if the employer can charge 15% more for his/her service or product! With customer's discretionary income evaporating (being sucked up by higher inflation and higher interest rates), it will be hard for many business owners, to pass on the increased cost of doing business...

This only works if the employer can charge 15% more for his/her service or product!

Why would you think this? There are plenty of ways an employer could increase wages without increasing the price of the product. Reduce staff hours. Increase efficiencies elsewhere. Accept a reduction in profits.

"Why would you think this?"

Because I'm an employer

And as an employer, you can't imagine any possible way to increase staff wages by X% without also increasing the price you charge for the goods and services you provide by exactly X%? If that's the case, then if your wage bill drops by a certain percentage, do you also immediately reduce the price of the good or service you provide by the same percentage?

I have increased my staff's wages by 5% on the 1st of April this year and I have done the same the year before. The wage bill NEVER drops.

On top of wages, there is also supplies, rates, insurance, power, petrol, accounting, legal, advertising, repairs and maintenance and other expenses which are also rising significantly.

If you think it's that easy, Al, may I suggest you take out a big loan, start your own business, work evenings and weekends for a few years so that you don't end up like the 80% of businesses which fail in the first 5 years. Then, when you grow, learn about employment contracts, hire some staff, good ones I hope, and then you will see how much excess profit you have left to give your people 15% wage rises

Calm down. I didn't say anything was easy. I just challenged the idea that an increase in wage rises automatically forces an equivalent rise in the cost of goods and services. It clearly doesn't. It's like when landlords argue that they 'have' to increase rents when their costs go up, but of course they never decrease rents if and when their costs go down. Employers and landlords both don't get to appeal to supply and demand when setting prices and wages when it suits them but cite costs when it doesn't, regardless of how hard they work.

Who says employers set prices, there are plenty of industries in NZ that are price takers, thanks to weak government watch dogs

dont forget Labours gifts of additional public holidays, an extra 5 days sick leave, dramatic minimum wage increases, and oh year the cold thats been going around

Minimum wage went up 5% didn't it?

None of my staff are on minimum wages

We really do need an LVT coupled with lower company income taxes. We should be incentivising and rewarding business builders like yourself, not speculators on land. When you build a business you contribute to the country and to improving living standards.

To be fair Yvil has cited a 15% rise in all expenses, not just labour. In such an environment you'd need to pass some if not all of those costs on.

If a business is able to reduce costs then it's their decision to reduce prices or absorb the increased profits, or a bit of both.

Sure - but it's not like there is some one-to-one correlation whereby if all your costs increase 15% you simply must increase prices by 15% (and if you don't, you simply can't increase wages).

It depends what the business is.

A distributor or retailer will usually adjust prices in line with what replacement stock costs fairly inline with cost increases. You would more likely see a price decrease in such a business.

A business with more moving parts might absorb costs over shorter terms in favour of less frequent rises. It's unlikely such a business will lower prices.

Usually a business has a profit imperative to shareholders so usually you pass on increased costs.

Yes, and that profit imperative means that the incentive is to keep wage costs as low as possible while still keeping sufficient staff of good enough quality to keep the business running. And businesses have had a pretty easy time keeping wages low up until very recently, given the immigration settings and what are essentially taxpayer-funded wage subsidies in the form of accommodation supplements, WFF, etc. They might not for much longer - what's happening in Queenstown at the moment is a good demonstration of that fact that supply and demand is what has the most impact on wages. If an employer in Queenstown at the moment told their staff that the simply couldn't increase wages because there is not sufficient customer demand to support an increase in price, then they would just end up with no staff. But that's exactly what is supposed to happen in a market economy - there isn't a god-given right to keep a business running.. If you can't provide a service at a price point people are willing to pay for while also paying wages high enough to keep the staff you need to keep the business running, then you go out of business. Tony Alexander had a good piece along these lines recently in the Herald (if I remember rightly).

Tony Alexander does love to wax lyrical about this stuff. I'm pretty sure he won't have to fire anyone in the next 6 months because revenue craters, he will just write about it.

What's happening everywhere is a good example. We just don't have a large enough working population to support the economy in its current configuration.

So costs will rise or some services will die.

exactly, but if your staff leave and you cant get any more.....thats why RBNZ will priortise inflation quickly by increasing the OCR, to lower inflation, so the employers dont have to give 15 % pay rises....and so it goes

Exactly this.

Why? Because non property speculating businesses generate tax. Lots of tax. Paye, gst, company tax. Not intending this to be a trick question but how much do leveraged property speculators create...?

Last time inflation was at this level rates were a lot higher. The RBNZ have no choice just have to follow FED and I don’t see anyone dropping rates for years

So hey bingo, first sign of a recession we drop the OCR to near zero again, print money like there’s no tomorrow to avoid any pain and in 2 years we are paying 4.4M for a 2 bedroom crap box in Hamilton? Repeating the same thing over and over again is not improving our situation.

No printing money like before can only happen when inflation is low. It's just not an option now. Inflation is more important than the economy especially when unemployment is so low. More and more people are realising the central banks aren't about to pump money into the system when things get worse, and this is why stock markets keep falling and will continue for a while yet.

...and this is why stock markets keep falling and will continue for a while yet.

Because everyone is cashing out?

Bailing out because there is no more easy credit.

Also damn hard to do your share buybacks when you input prices have gone up ten percent and your shareholders still expect a dividend...

And pretty hard to get people to take on the risk of buying a share with a divided of 2% when they can get that in the bank soon...

Theres going to be some real carnage.

What would NZ look like with a fifty percent fall in everyones kiwi saver?

And a fifty percent fall in houses?

We might be about to find out...and more

Interest rates are in theory supposed to be above inflation. So rates to the moon, and prices back to reality is very possible. Leveraged "property only goes up" believers will continue to preach, untill they realise their debt is an inward facing suicide vest.

To reposition someones quote. "Lots of room for upward (rate) movement, be quick (to exit debt)..."

Popcorn.

Depends if Orr sticks to the line at last meeting, go hard early (ie 2 x 50 point rises to start, then 25 each meeting rest of year to try and get things under control in 2 years instead of 4 or 5. Will he flip flop, unlikely on his recent strong reslove. My pick, 50 points next week, 25 each meeting until we get OCR starting with a 3

So you don’t think he will stop before 3, as the economy sinks?

If he goes to 3.5% what do you think that will mean for the economy, employment and house prices?

And then, what is the path for the OCR over 2023, assuming a big slump?

I think many, including RBNZ (for sustainability), RE industry (for turnover), and banks (for turnover), do not have a problem with a 10 to 15% house price correction. A 'crash' for NZ housing market would need to be 25%, I dont think that will happen even with 6% mortgages. Hopefully we can engineer a stable 2.5% OCR by 2024.

I think it will. 10-15% already and the pain only just started.

Agree. If the OCR goes to 3% or more I see at least 25-30% house price falls and a decimated economy.

which is why I still don’t think it will get to 3%.

A 25 % fall in house prices only takes them back to where they started in 2021 ... and , they were already wildly overvalued then , when the RBNZ decided to pour petrol on the raging inferno ...

I'm still going for a 100bps on the 25th May.

good to have a laugh in these times Carlos lol

This should be funny. Sadly there is a case to be made for that after the overreaction downwards during Covid.

You are joking, right?

Why would I be joking ? its going to move 100bps. Whats the real world difference if it moves 50bps in 3 days then another 50bps in 6 weeks ? its going up at least another 100bps in the very short term. RBNZ appears to have a 50bps limit on the way up. If it moves 50 now and 50 in 6 weeks I'm still right.

Oh dear, you aren’t joking…

and no you won’t be right if it goes up in two 50 BP increments, you were talking about it going up by 100 BPs on 25 May. VERY different things - one x 100 BP rise would shock the markets.

weird

Good we now know it will be 50

If there will be Four consecutive 50 basis points hikes, then at least we can say Orr has tried to rectify his mistake of unnecessary 75 basis cut and LVR removal.

Ad commented in the article Orr is presuming a neutral rate of 2% if the neutral rate turns out to be higher then this is all smoke and mirrors. Personally I believe inflation will go quite a bit higher than he expects and he will be too little to late again .

Beware the unemployment rate. It is actually the unemployable rate. The job seekers (also unemployed) double that number & some. Lies, damn lies & statistics.

"However, we wouldn’t be too surprised if estimates of the neutral interest rate start to edge upwards, given the sharp rise in inflation expectations here and overseas. And it really matters what the RBNZ thinks neutral is, because they need to lift the OCR one for one with any increase in their estimate of neutral, otherwise interest rates can become more stimulatory, even if the OCR remains unchanged," ANZ's economists say.

Hmmmm ..Liquidity preferences are simply opportunity from the opposite perspective. Falling interest rates outside of the short run are an expression of economic (which might include financial) pessimism.

I would put a lot more faith in the current flat NZ sovereign 5yr vs 10yr spread as an indication of heightened liquidity preferences. The extraordinary low yield demand by one bidder for the most recent 15/04/2027 NZ government stock tender is further evidence.

This is what Milton Friedman called the interest rate fallacy, and it indeed refuses to die. We can tell what monetary conditions are in the real economy, as opposed to financial liquidity, though the two can be linked, by the general level of interest rates. When money is plentiful, interest rates will be high not low; and when money is restricted, interest rates will be low not high. The reason is as Wicksell described more than a century ago:

[The natural rate] is never high or low in itself, but only in relation to the profit which people can make with the money in their hands, and this, of course, varies. In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low.

When nominal profits are expected to be robust, holders of money must be compensated for lending it out by higher interest rates. Thus, the same holds for inflationary circumstances, where nominal profits follow the rate of consumer prices. During the Great Inflation, interest rates weren’t low at all, they were through the roof well into double digits and higher by 1980. At the opposite end in the Great Depression, interest rates were low and stayed there because, as Wicksell wrote, the rate of profit was low and was expected to be low well into the future. High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar. Link

"Toplis argues the lowest unemployment rate in decades, 3.2%, is a bigger headache for RBNZ monetary policy than the highest inflation in 30 years." Yes, it seems the heat from employers to avoid 10 to 15% pay increases has more clout now than protecting housing investors. Interesting.

It’s assumed that if increasing interest rates cause a recession the OCR will come back down again and quickly.

I would have thought there’s a very strong argument that high interest rates will not tame inflation and we are facing the real prospect of high interest rates, recession, increasing unemployment and decreasing asset values all at once while still facing untameable inflation. What a concoction!

Exceptional external factors right now mean we are not facing “normal” economic fundamentals. I find it extraordinary that these economists are so inward thinking when it comes to their expectations. New Zealand doesn’t live in a bubble. We sit down here at the mercy of decisions made by Russia, China and USA.

I'm going to pretend I didn't read your post, look at the nice sunny day outside, and tell myself that, it's beautiful day. LOL

Swingtrader yep reminds me of the eighties all of the above seems familiar.

That is an excellent post. NZ rode a Globalisation wave that hugely benefitted a country normally hamstrung by its isolation. This could be the beginning of the end of Globalisation. What does that mean for the Chinese economy, our biggest trading partner, and Australia, our second biggest trading partner. This is what the currency markets are seeing. NZ could be particularly hard hit in the next few years.

Will Reserve Banks be able to redeem themselves after a major goof up.

https://finance.yahoo.com/news/the-fed-overshot-dramatically-on-inflati…

The views expressed are interesting but I don't think we'll see RBNZ slow the rate of increases until we see inflation dislodged and CPI registers a fall. We've been running hot for more than a year so inflation expectations may need to be reset.

It astounds me that most here seem to think it's a given that the RBNZ are going keep dealing to inflation over the next 1.5 to 2 years.

They didn't for so long last year, and furthermore inflation is not the only part of their mandate.

So, past record PLUS their mandate would suggest it certainly is not a given.

And do people *really* think the RBNZ is truly independent and that the election next year won't have any influence???

It’s surprised me that Powell has more or less one out and said I don’t care about the markets or necessarily a bad recession because getting inflation under control is the number 1 goal.

I think RBNZ being the puppet of the Fed will simply mimic that sentiment/stance/action.

And given how they completely overcooked the response to avoid deflation, it won’t be surprising if they overcook things completely to get inflation under control - at least if they are consistent in the size of the errors that they make.

The cause of inflation was from all the money printing, stimulating demand massively. Supply was constrained due to covid, disruptions and hence 18mths later we are seeing prices increase. Economics 101 supply or demand problem, central bankers globally overcooked.

Inflation is extremely damaging as it dents confidence in the economy. But what’s more dangerous it creates massive social upheaval for the masses who are on min wages 46k to 70k, as they struggle to make ends meet.

Thats why they need to hit OCR hard or there will be serious social issues in a year or two. Not to mention more inflationary pressures from food and fuel are yet to flow into more price increases, it’s just beginning. Expect Arab Spring 2.0 in the 3rd world this November.

With eliminating child poverty in mind, do you think middle NZ hhlds can cope with higher prices for everything and sky high interest rates on their mge too?

Maybe we need a radical approach along the lines of what the Australian NLP are proposing:

A Monetary Reset [that]would:

- Give every Australian adult an identical sum of government-created money;

- Require those who had debt to use that money to pay down their debt;

- Sell Treasury Bonds to banks, precisely as is currently done in deficit financing; and

- Require those with less debt than the amount issued to purchase Treasury Bonds from banks, from which they will earn interest income.

This would not create any additional money and put inflationary pressure on the economy, but rather, it would change the asset backing the money from private debt, to reserves and government bonds.

Now everyone is blaming central banks, where were everyone when biggest lie of Transitory Inflation was been played to manipulate and support the ponzi be it house price or stock market.

Mr Orr had the audacity to say that they are not responsible for housing ponzi...where does this arrogance comes from....

https://www.kitco.com/news/2022-05-20/Real-estate-slowdown-starts-in-20…

Why are governor of reserve bank not held accountable or asked hard questions.

Mr Orr's arrogance is outstanding. He lowered TD interest to less than 1% and couldn't understand why savers had to move their money to property. Rather than admit that he got things wrong, he kept the tap of cheap money on too long.

Yep and more than a couple of people on here that are shaking in their shoes and said rates couldn't possibly go up and that it was impossible only 6 months ago, well now its happening and everyone else could see it coming, most certainly in the last couple of months it was a given. The only thing we don't know now for certain is the size of the coming train wreck.

Indeed. Did Mr Orr turn property into the finance companies of the GFC...?

Of course it was interest rates, proven simply by whats happening right now.

I do recall David Clarke apologising early on in the Covid fiasco due to riding his bicycle during the first lock down. After much attention he owned up to his lapse of judgement. Taking ownership took guts and I for one admired that!

Has anyone in the echelons of power and or the reserve bank subsequently admitted that maybe decisions were made with unintended consequences??

The failures are spun as wins, the outright economic destruction will be Putin’s fault and oh, we are still better off than anywhere else in the world hahaha.

Accountability, no no no no, that’s an outdated value for the rest of you to concerns yourselves with, especially in your relationship with IRD, Human Rights Commission, Ministry for a-zz and all our other minions.

I see fantastic consulting jobs for our architects to replicate this madness in Australia under their new government. Rinse and Repeat. Never admit to failure. Let the good times roll lol

it's questionable RBNZ need to do anything. Imported inflation is causing such an erosion of disposable income that a slow down is inevitable OCR rise or not.

As house prices rose RBNZ cut rates and added jet fuel to a hot market, now they are doing the direct opposite.

There is also contradictory fiscal and monetary policy at work. What on earth is the point of govt cutting fuel duty and offering households free cash to alleviate the burden of price rises if at exactly the same time RBNZ are hiking rates ?

Check this article on inflation and how high interest rate have gone in 1970 to tame the inflation.

https://www.dailymail.co.uk/news/article-10832437/How-1970s-inflation-c…

If anything remotely like that happens everyone will hear the 80s song...

Hold tight, wait 'til the party's over

Hold tight, we're in for nasty weather

There has got to be a way

Burning down the house

Well I'll admit I'm not an expert but as everyone it putting out there opinions I'll have a go. Personally I think they (RBNZ) want to tank the housing market by more that 25%. They can't say it out loud and both the RBNZ and the banks are being are cautious with how it's being drip fed, but the New Zealand housing market is and has been for many years incredibly overpriced and unsustainable. It has been a drag on the real economy and the negative externalities have been massive. The housing market has been held up by faith in ever-increasing prices. In order to reset the economy onto a more sustainable path this faith has to be broken and that means that a whole lot of people, including owner occupiers who bought years ago, before the Covid madness, also need to experience negative equity and real losses. And the argument that if they let this happen it will smash the overall economy? There is no wider economy, it's all housing baby. It's not going to be pretty.

Its pretty obvious you are wrong. The RBNZ has already had a year to "Tank" the market and they sat on their hands while house prices when through historic price increases. The RBNZ are now trying to very reluctantly raise rates and will do so until current home owners start to squeal loudly and then they will stop. Given a choice people would pay an extra hundred bucks a week due to inflation than have their house lose a couple of hundred thousand.

It was not the right time to tank it, before. Now is the right time when everything is tanking. Gives them and government cover.

With the indebtedness of our economy, it's possible (even likely) that the neutral rate is much lower than 2%. Which has to be the main reason they will slow down the rate increases. Basically keep prodding with 0.25% increases until something breaks.

Isn't it a shame that it is in the Reserve Bank's interests for unemployment to rise to bring down inflation. That more people should be on the dole/Job Seekers benefit rather than in work, so that there are more people looking for work, therefore leading to the flattening off of wages.

I really hate the link between employment rates and inflation, it basically says that the poorer people and their families on less stable jobs are collateral damage in the country's quest to reduce inflation for everyone else. And it is the poorer people that lose their jobs as a result that pay for lower inflation for the wealthier amongst us.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.