There were no surprises or large movements in currency values over the Christmas/New Year period due to the traditionally reduced liquidity levels in forex markets. The US dollar Dixy Index has remained in a relatively stable 97.50 to 98.30 trading range since mid-December. The EUR/USD exchange rate similarly moving sideways between $1.1700 and $1.1800 over the same period. As a consequence of the calm external international FX market conditions, the Kiwi dollar has oscillated between 0.5750 and 0.5850. The push up in the NZD/USD exchange rate in the week prior to Christmas to 0.5850 could not be sustained as traders took their profits and the US dollar recovered a little in global FX markets.

The most interesting currency related news events over the holiday period related to two currencies not normally commented on in this column: -

- The Brazilian Real appreciated 15% against the US dollar through 2025, from 6.20 Real to USD1.00 at the commencement of the year to 5.25 Real in November. The demand to buy the Real coming from carry-traders attracted by Brazil’s high 15% interest rates against falling interest rates for the US dollar. Other Emerging Market currencies like the Real are forecast to appreciate on inward capital/investment flows in 2026.

- The plunging value of the Iranian Rial currency value to 1.42 million Rial to USD1.00 in late 2025. The Rial was 817,000 to the USD at the start of 2025, therefore it depreciated 74% over the 12-month period. The collapse of the currency instigated shopkeepers and traders in the city bazaars to protest at the rising food prices. Widespread civil unrest in Iran has followed over recent days, culminating with US President Donald Trump threatening interference in internal Iranian affairs if the local military start killing protestors. Alongside the Venezuelan takeover, yet another example of Trump rattling global incidents, when he campaigned on completely the opposite of the US becoming a fortress and not being the world’s policeman under his second term regime. Oil prices seem set to fall further with the US now controlling Venezuelan supply.

The majority of FX rate forecasters still expect further depreciation of the US dollar in 2026 due to changing interest rate differentials, US fiscal deficit risks and the erosion of the Federal Reserve’s independence as Trump appoints his own people onto the Fed’s Board.

The timing of further interest rate cuts by the Fed stands out as the dominant driver of US dollar direction over coming months. The markets are not expecting another interest rate cut at the 28th January Fed meeting; however, the forward interest rate market pricing is for two x 0.25% cuts following that. The timing and speed of US interest rate cuts early next year will depend entirely on US employment data. Weaker than expected new jobs data over coming months will turn the current “hawks” on the Fed (who fret about entrenched inflation at 3.00%) to supporting cuts under the employment side of their mandate.

Everyone will receive the first read on US employment trends over this coming week, with the following economic data being released:

- Monday 5th January: ISM Manufacturing Employment survey results for December – further falls from the 44.00 November result will be negative for the USD.

- Wednesday 7th January:

- ADP Employment Change for December – a +45,000 jobs rebound is expected following the 32,000 contraction in jobs in November.

- ISM Services Employment survey for December – a small decline to 48.7 is forecast from the 48.9 level in November.

- JOLTS Job Openings for November – a stable outcome is expected with 7.70 million, up a fraction on the 7.67 million in October.

- Friday 9th January:

- Non-Farm Payrolls for December – consensus forecasts are for a 45,000 to 55,000 increase in jobs following the +64,000 result for November.

- Unemployment Rate for December – a steady 4.60% number is anticipated following the jump up from 4.40% in September to 4.60% in November.

- Average Hourly Earnings (wages) for December – a 0.20% increase for the month is forecast, leaving the annual increase stable at 3.50%.

The likely FX market reaction to softer than forecast employment data will be a return to selling the US dollar, pushing the USD Dixy Index back below 97.50.

The longer-term technical/chart related picture for the US dollar is very close to turning decidedly negative. The USD uptrend line that has held for the last 15 years since 2011, will be breached to the downside if and when the USD Index trades below 97.00 (refer to the chart below).

Global fund manager investors into the US were net sellers of the US dollar in 2025 as they hedged against the risk of further US depreciation. Whilst some fund managers withdrew physical cash from US equity markets, others bought USD’s as they chased the boom in AI and micro-chip stocks. The question for 2026 is whether global funds will continue to pour into the US listed AI stocks, or do those flows reduce as over-valuation risk issues for the AI companies grow on data centre and electricity supply constraints? We see the latter outcome being more likely.

The risks that the alternative scenario to further USD depreciation in 2026, i.e. USD appreciation occurs, centres around two main factors: -

- US inflation remains entrenched above 3.00%, therefore not allowing further Fed cuts in US interest rates. The recent reductions in oil prices to below US$58/barrel looks more likely to push US headline inflation lower over coming months. The impact of import tariffs on inflation has been less than expected over the last nine months and housing costs (Shelter CPI) continue to decline. The risk seems well contained.

- Global geo-political events causes investors to keep funds in US dollars. Venezuela and Iran are the current hotspots for US intervention, however the probability of an end to the Ukraine/Russian war is somewhat improved and if it happened the Euro would certainly appreciate against the US dollar.

More confidence around a resurging NZ economy in 2026

All the indications are there that the New Zealand economy is poised for positive GDP growth close to 3.00% in 2026. Certainly, business and consumer confidence has picked up since interest rates were cut to 2.25% in November. The household de-leveraging cycle over the last two to three years, that diverted cash from retail consumption to repaying mortgage debt, appears to be coming to an end. What is most encouraging about the export-led expansion in economic activity over the second half of 2025 was that it was not caused by immigration/population growth or a residential property market boom. It can be done!

There has been a dramatic U-turn from the majority of economic forecasters in New Zealand over the last three months. In September, continuing doom and gloom was their depressing outlook. However, stronger than expected economic data from July onwards and the interest rate cuts have transformed their outlook to a much more positive vibe today. The NZIER Business Confidence survey results for the December quarter being released on Tuesday 13th January should confirm the improved expectations for the economy in 2026.

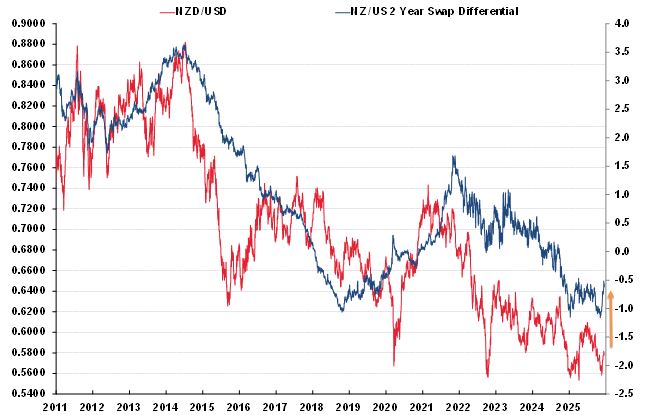

The most significant impact on the NZ dollar value from the New Zealand side of the currency equation with the US dollar, will be the direction of our inflation rate over the first six months of the year. Inflation outcomes will determine whether the RBNZ hold the OCR interest rate at 2.25% throughout the year or whether the are forced to increase the OCR later in the year. In a potential environment of lower US short-term interest rates and increasing NZ interest rates, the differential closes right up and lifts the NZD/USD exchange rate.

The RBNZ are forecasting the CPI inflation rate to only increase by 0.20% in the December 2025 quarter and increase by 0.50% in both the March and June 2026 quarters. Under their forecast the annual rate of inflation decreases abruptly from the current 3.00% level to 2.20% by 30th June 2026. It is hard to fathom what prices will be decreasing or staying at the same level over the next six months to offset the ongoing price increase to produce such a rapid decline in the annual inflation rate. The RBNZ have stated that they see the 1.00% increase in the inflation rate in the September 2025 quarter is largely due to one-off/temporary factors. In an expanding economy this year with increased consumer demand we are unlikely to see large-scale discounting by retailers. The stronger consumer demand may also lead to local producers seeking to recoup compressed profit margins over recent years with price increases.

The December 2025 quarter’s CPI inflation figures will be released on Friday 23rd January and in increase as low as 0.20% as the RBNZ forecast seems unlikely against the 0.50% December quarter increases in both 2023 and 2024. The current local interest rate market pricing of the OCR increasing in the second half of 2026 looks closer to reality than RBNZ Governor Anna’s stated position that the market has got ahead of itself.

Closing interest rate differentials and continuing Chinese Yuan strength against the US dollar stand out as two current positives for the NZD/USD exchange rate to return to above 0.6000 over the coming period (refer to the charts below).

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

1 Comments

Jolly Roger sees a resurgent NZ economy and NZ dollar ✔️

He'll make no friends here with these positive well-argued thought pieces!

Cheers Roger!🥂

What is most encouraging about the export-led expansion in economic activity over the second half of 2025 was that it was not caused by immigration/population growth or a residential property market boom. It can be done!

What's he talking about? None of this has materialised.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.