Ah, now I get it.

I admit to having been mildly perplexed when the Reserve Bank went on a kind of drive to get banks to raise their deposit rates further than they had.

As the RBNZ embarked, in October 2021 on a momentous Official Cash Rate hiking cycle that has seen the OCR go all the way from 0.25% to 5.5%, I guess my focus had been on what would happen to mortgage rates and what the impact would be in terms of dragging money out of pockets.

Well, that has been pretty spectacular.

Rising deposit rates, I suppose I looked on more as, well, nice if you've got some spare cash. And I interpreted the RBNZ's actions in looking for higher deposit rates as a way of our central bank trying to get the country's registered banks to 'lock in' a higher funding structure, IE that by paying more for deposit funds they would need to keep mortgage rates higher for longer. And I think that is valid and part of the plan.

But of course, when you think about it more deeply, central to the RBNZ's drive to take heat out of the economy and inflation is to reduce spending, for people to have less money in their pockets to spend and therefore fuel inflation.

The obvious way we think of that happening is mortgage rates that we pay through the nose - removing money from us. But the more subtle way of taking money out of consumer's pockets is to get them to stick it in the bank - for a long time, where they can't get at it to 'frivolously spend'.

Well, I've been having a bit of a look at the RBNZ's own suite of month-end data releases, compiled by them from information directly supplied to them by the country's banks. We've now got six months worth of these this year, IE the first half of the year.

I was particularly taken with two data sets, the residential mortgage loan reconciliation stats and the deposits by sector stats.

These two data sets together paint a picture of how about $20 billion has been sucked out of consumers' pockets over the past 12 months. Yep, that's right. $20 billion gone from our wallets that we probably didn't know we had.

Working on the basis of a population of 5.2 million in NZ, this $20 billion accounts for around $3846 per man, woman and child.

Or to stretch this across a year, that's about $74 a week of money no longer in pockets.

Ah, the RBNZ's cunning plan. Though shalt not spend.

To look at the mortgage side of the equation, as the RBNZ stats highlighted, the quarterly interest bill topped the $4 billion mark for the first time in the June quarter 2023.

Over the last 12 months to June 2023, the total mortgage interest bill has been $14.8 billion. In the previous 12 months to June 2022 the total interest bill was just $10 billion.

So, the increase over the last 12 months has been $4.8 billion - that's an extra $4.8 billion no longer available to spend.

Right, moving over to the deposits data and this is arguably where it gets even more interesting.

Bizarre as it is to say so, the pandemic was very 'good' for us financially. There's no doubt being locked up in your house can do wonders for the ability to save money.

Prior to the real onset of pandemic conditions here in March 2020 households were not actually saving money very well at all.

As of February 2020 the rate of annual household deposits growth had slowed to just 4.3% - the lowest rate since 2010.

By October 2020 the annual rate of household deposits growth had rocketed to 9.7%. What a difference a pandemic makes.

But of course, at the same time, interest rates had disappeared into the dust. The mattress on your bed was just about offering a better rate of return.

Term deposits were dying the death. Most of the money that had been accumulated during the pandemic was sitting readily available in transaction and savings accounts.

In February 2020 the amount held by households in term deposits was just over $100 billion. By the end of 2021 this had withered to just $83 billon.

But what a difference some 'real' interest rates have made.

In June 2022 there was a bit over $91 billion in TDs held by households.

As of June 2023 the figure was rapidly approaching $117 billion - an all time high.

This rapid ascent of TD balances has had an offset effect on household transaction and savings balances.

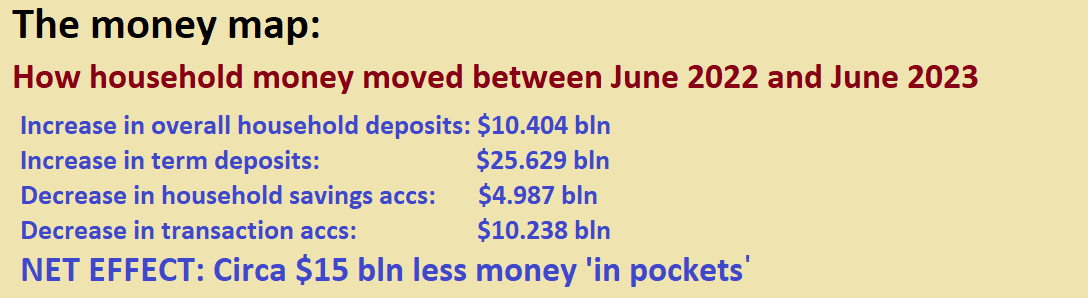

As of June 2022 household transaction account balances were $51.564 billion. By June 2023 they had dropped to $41.326 billion.

As of June 2022 household savings balances were $79.69 billion. By June 2023 they had fallen to $74.703 billion.

The significant part of all that of course is that it means households that were awash with extra cash available to spend post-pandemic, now have less money in the pockets. Less spending.

Here's a summary of what's happened in the past 12 months:

So, the upshot of all that is even though total household deposits have increased by over $10 billion in the past 12 months, more than $25 billion has been sucked away into term deposits, which is a lot of money.

And it means that $15 billion that was previously swimming around and available for spending in savings and transaction accounts has now been vacuumed up (into TDs) and is not burning a hole in pockets.

Of course that extra $25-plus billion that's gone into term deposits is not 'gone' as such, it's sitting there attracting interest and waiting to be grabbed later. But it's not being spent now and it's not fuelling inflation.

So, between the somewhat more than $15 billion 'taken out' through re-direction into TDs and the approaching $5 billion extra for mortgage interest costs, there's $20 billion less hanging around looking for things to buy. Fascinating.

I would think that given the fact that both mortgage rates and term deposit rates have edged up again recently would be giving the RBNZ some comfort at the moment. The plan IS working. Money IS being sucked out of circulation. Now all we need is for inflation to play ball.

In the meantime it looks increasingly as though interest rates - both for deposits and for loans may well be 'higher for longer'.

28 Comments

"In the meantime it looks increasingly as though interest rates - both for deposits and for loans may well be 'higher for longer'."

Page 1 of the Scroll

by Future | 7th Oct 22, 2:34pm

The Seal has been Broken. This is how the Scroll reads.

Interest Rates will continue to go Up from here and Stay Up for a Long Time.

Until something breaks... and something will break

Not at current interest rates it won't. Rates need to hit double digits before the SHTF.

Maybe in NZ, but someone systemically important overseas will be found to be swimming naked before then, and then global rates will drop. It is just a matter of time

Huh! You younguns know nothing. Back in 1982 the finance company I worked for paid 24% at one stage for deposits, and lent out at 29-31%. Nothing broke. House mortgage rates were also at some ungodly rate as well. We bought our first house and 2 investment properties in the '80s and survived. Short term hardship, and taking a bit of a risk, and working hard were all part of the deal. Those 3 paid off in Spades.

I got about 20% return on my deposit from the Post Bank.

Houses were selling for about 45K in fancy locations. Does not take much of an interest rise to make a big difference to a family now.

Ok, Boomer.

This BOOMER spent 30 years paying off our mortgage borrowings for our family home and are still living in it, we saved for our retirement, the wife was earning $9 per hour less Tax, I being a Tradie was earning $15 p/hr, us BOOMERS that did that are now spending our savings at incredible rates, we had a Plumber recently at $80 p/hr $350 to replace a hot water cylinder element, our savings that were hard earned are now exiting our bank accounts just like the bath water exiting the plug hole, you are the next BOOMER in waiting! so make sure your home is freehold and you have numbers in your bank account resembling a telephone number, because believe me you will need it, depending on your age but your $50 per hour maybe a loaf of bread.

Cheers.

A labeled BOOMER at 74 years of age.

Why did it take you 30 years to pay off a mortgage that would have been at most 2 x your annual income? Did your wife continue to earn $9 per hour over that period?

Once again highlighting the frivolous nature of the Boomer generation, rushed out to take out 3 very modest at best mortgages at ridiculous interest rates and still took 30 years to pay off? LOL

...and there you have it, the effects of monetary policy are working exactly how they should be, interest rates rise.

People with cash save more with higher returns on savings, debtors pay more in interest and mortgage repayments- net effect less disposable cash to slosh around in the economy.

A very pertinent article David!

Imagine if that $20b was instead sucked out of consumer's pockets into their Kiwisaver accounts.

It's an interesting point. At ~$120billion just in transaction and savings accounts, that's ~$23K on average for everyone in the country. (Seems a lot for a rainy day fund). And this doesn't include TDs.

More likely $119 billion for the top 1% and $1 billion for everyone else.

And apart from an emergency savings account, anyone with a mortgage should be paying off the principle rather than putting extra money into savings.

The reason people are in the top 1% is because they don't have $119billion in under-performing transactional and savings accounts.

Is there somewhat of a misinterpretation here? That $20 billion will have gone to private bank profits, not the RBNZ surely? At least the banks will claim it as their profits. Is Mr Orr getting a private commission?

Its $20 billion not in circulation. Much will be in term deposits, only to reappear at a later date.

This is not how retail banking works. The money we pay to banks in interest for our mortgages gets paid out straight away to term deposit holders. The difference is a spread but in the current climate banks keep less of it than previously as the RBNZ is 'encouraging' banks to keep increasing the deposit rates and thus decreasing the spread. As a result, and also because of shrinking number of home loans, the banks have not been making as much money in this high-interest environment.

On the other hand, the cash you and I have sitting in non-interest paying bank accounts like your current account, gets transferred to the RBZ each night where the RBNZ earns high interest on it.

One lesson for you and me - put your money into term deposits and don't let it sit in cash accounts!

Does anyone know what happens to customers’ savings accounts in an insolvency situation? Are customers treated as unsecured creditors? Is the benefit compared to term deposits that it is easier to get your money out once warning signs begin to flash?

Not sure I believe that. Look at the total loan portfolios and the interest income from them v the amount held in term deposits. I'm pretty sure you'd find a significant discrepancy between the two totals in favour of the banks. If they paid at least the OCR in non-term deposits then you be closer to the truth. Fundamentally i simply don't believe the banks can be trusted.

Great information, thanks David for the analysis.

Not sure how completely wasted money in higher mortgage rates actual "Helps" the economy. This is 100% wasted money as it has zero productivity. It appears the RBNZ needs to treat everyone like a 5 year old standing in the chocolate isle in the supermarket, it steals your pocket money so you cannot buy that bar of chocolate. I guess 5 year olds don't buy houses however and when you give adults cheap money in this country all they do is rush out and buy another house.

It's interesting you say that money sitting around is wasted money. I'm of the opinion that people are losing their trust in money as a store of value. People only see it now as a means of exchange, not as a store of value. I think it's what's causing the current market volatility and asset bubbles. And inflation.

I am not at all sorry to keep banging on about it, but money kept and looked after by a Kiwi firm at least has the profit staying in NZ instead of being syphoned offshore as quickly as possible.

And of course higher term deposit rates means more interest for depositors as well as more tax for the Govt to play with....

Government get 15% from GST ... So, nah.

Also, job losses and economic recession will - actually already has - slash govt receipts.

Quite surprised you're surprised by this.

Now you see why many of us are furious at the RBNZ? They should never have been raising rates in 0.25% increments over such a long period. It literally encouraged spending and inflationary spending at that.

Instead it should have been, "Right. Covid shock is over. Back to some degree of normality. The OCR will be 4.5% to stifle demand while global supply chains sort themselves out."

Sure, there would have been some howls from money markets. But, quite frankly, they had to way too good through covid.

The obvious issue is that mortgagees will never see their money again whereas the term depositors will see theirs and them some.

Or put bluntly - another massive transferal of wealth. The RBNZ has much to answer for. More so given how slow they've been to instigate more effective inflation fighting tools when the seriously inequitable effects of the OCR are well known.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.