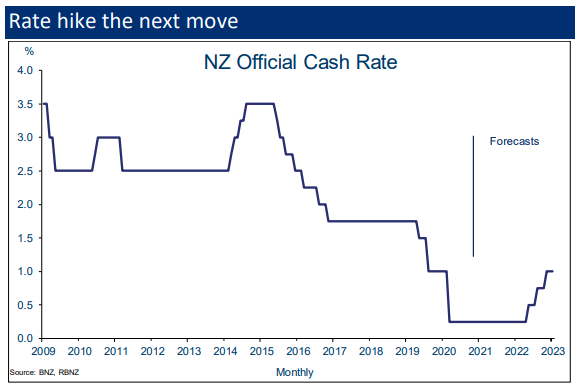

BNZ economists are now forecasting that the Reserve Bank will begin raising interest rates from as soon as May next year.

The change in forecast from the BNZ follows the stunning fall in unemployment for the December quarter to 4.9% from 5.3% in September - a result that went right against market expectations (and the forecast of the RBNZ) that unemployment would rise to 5.6%.

The employment figures have now removed all talk from the marketplace of the possibility of any further interest rate cuts. ANZ economists, who had been forecasting one further cut this year to the Official Cash Rate, taking it down from 0.25% to 0.1%, now say they no longer expect any more cuts.

The Reserve Bank will next publicly be discussing interest rates with the release of its next Monetary Policy Statement (MPS) on February 24. For much of last year it appeared likely that the RBNZ may well take the OCR below zero this year. But market sentiment has changed quickly since towards the end of 2020.

Last week, ahead of the latest unemployment figures being released, global independent economic researchers Capital Economics doubled down on their earlier pick that interest rates would rise from next year.

And Capital's now getting some company, with BNZ forecasting rises from next year, while wholesale interest rate pricing is suggesting increased risk of rising rates from 2022.

BNZ head of research Stephen Toplis said the BNZ economists had been warning for some time that the scene was being set for for the next move in interest rates to be up.

"Indeed, we abandoned the prospect of sub 0.25% rates back in early November last year. As relatively hawkish as we were, we were not prepared to be definitive that rates would rise. Now we are.

"There is still massive uncertainty as to when and by how much but, today, we are formally building in a first rate hike in May 2022.

Toplis says rather than a statement of exactly when, this forecast "should be considered as a placeholder, and a stake in the ground".

"Clearly, there is a mass of water to go under the bridge between now and then and the re-emergence of Covid in New Zealand could again see thoughts of a further rate cut rise to the surface.

"But if the current momentum in the economy is sustained then New Zealand will be in serious risk of overheating if monetary conditions were to remain as stimulatory as they now are."

In terms of whether the RBNZ will adopt "a formal tightening bias" when releasing its February 24 MPS, Toplis says "not necessarily, or even likely".

The dollar is on fire

"It will, no doubt, be very fearful of pouring further fuel on a NZD [New Zealand dollar] that is already on fire. Also, the Bank is on record as saying that it is willing to let things run hot for a while implying that its risk tolerance is to act late and hard rather than early. But the Bank won’t be able to ignore what is going on.

"From a Reserve Bank perspective, the strength in the NZD, which now stands 5.0% above its MPS-assumed level, will be disconcerting. But less disconcerting when seen alongside strong commodity prices, an improving global outlook and an on-fire domestic economy."

Kiwibank economists note that wholesale interest rates are higher "across a far steeper curve".

"Risk of rate cuts have been replaced by risks of rate hikes! And as soon as next year. The Kiwi rates market has gone from pricing in a negative cash rate, just a few months ago, to rate hikes beginning in the middle of next year.

"It all comes down to the RBNZ’s communication on February 24. The RBNZ should remove their ‘optionality’ around negative rate policy, but cap market expectations of rate hikes. A return of the OCR track [the RBNZ removed OCR forecasts from its MPS forecasts last year] will do the trick. We’d expect the RBNZ to signal an unchanged OCR well into 2022 (possibly 2023) at this stage, to restrain the rise in wholesale interest rates.

"The RBA [in Australia] signalled an unchanged cash rate, into 2024! It’s about time we took out the downside risks. But it’s not yet the time to talk up the upside risks. That’s a game plan for next year (we hope)," the Kiwibank economists said.

'Done the trick'

ASB senior economist Mike Jones said last year’s flood of RBNZ (and fiscal) stimulus "has done the trick, and no more is required" and he agrees with the market pricing "some risk" of a lift in interest rates in 2022.

Jones says that "remarkable as it is to suggest", the unemployment rate may have already peaked.

"There are some chunky implications for the RBNZ here. Achieving the Bank’s two monetary policy objectives is suddenly a goal within reach, from a situation last year in which its inflation and employment projections were a long way from target. Last year’s flood of RBNZ (and fiscal) stimulus has done the trick, and no more is required. By contrast, attention is quickly turning to when the stimulus taps, which are still gushing, might be wound back a little. The market is now factoring in a small (just under 10%) chance of a lift in the OCR by February 2022, which looks about right to us."

Capital Economics Australia & New Zealand economist Ben Udy says he thinks the unemployment rate will fall to near 4% by the end of 2022.

"That’s much more optimistic than the RBNZ’s forecast that the unemployment rate will rise to a peak of 6.4% in Q2 and still be 5.5% by the end of 2022. Our view that the labour market is set to tighten much faster than the RBNZ anticipates is one reason why we expect the Bank to begin raising rates by the end of next year."

'A picture of economic resilience'

ANZ chief economist Sharon Zollner and senior economist Liz Kendall said the latest employment data add to a building picture of economic resilience relative to expectations, which, combined with better inflation data, a strong housing market, resilient business sentiment, and continued good management of our Covid response, should provide some assurance to the RBNZ.

"Their targets look achievable over the medium term, provided downside risks do not materialise. So while easy monetary conditions will be with us for a long while yet, the RBNZ can be patient. We no longer expect the RBNZ to cut the OCR again this cycle."

Westpac senior economist Michael Gordon said the employment results "are of course welcome", but they represent a shot across the bow for policymakers.

"The rebound in the level of GDP, the surging housing market, higher than expected inflation, and now falling unemployment all make it obvious that the combined efforts of the Government and Reserve Bank to support the economy through the Covid shock have had a much more powerful effect than anticipated.

"That calls into question just how much ongoing stimulus is appropriate, particularly over the period when vaccines are rolled out and global travel resumes. It’s becoming increasingly possible that the RBNZ will regret some of the stimulus measures that it put in place last year, and could start to tighten policy sooner than we previously anticipated."

74 Comments

Bond market on the way up.

https://www.rbnz.govt.nz/statistics/b2

https://www.bloomberg.com/markets/rates-bonds - NZ 10 year 1.33% at moment

Rest of the world on the way up also..

I wonder what the chocolate wheel will say next month.......

Goes round and round, round and rou...wrr, khrrk, wobble, akh quick govt & rbnz chorus; the choc wheel on the bus goes..

I don't understand why the banks have been so pessimistic for so long - what data are they actually tracking cause Inflation surprised on the upside, house prices are booming, commodity prices are booming, business confidence back to 2017 levels, stock market at record highs and record low interest rates all point to one way traffic.

Macroeconomist playbook on sentiments:

Negative signs - doom & gloom predictions, rate cuts & mindless printing, fiscal stimulus

Positive signs - adopt Murphy's law and assume cautious optimism

Banker Gangsta's . What do you expect ?

Looks like the silver squeeze might be happening as more wake up to the corrupt scam of the fiat system.

As previously posted numerous times, those with big mortgages need to be prudent and that need seems to be getting a little more likely.

If rolling over a term in the next year, then those 5 year (2.99%) or 7 year rates may provide a bit more certainty and prove less stressful in the longer term so could be worth considering.

As I have said before, pay down your debt boys and girls. Things can change fast.

Karl

I agree totally.

The ability to service the mortgage is of greater importance than short term fluctuations in the market which have few consequences provided on can meet mortgage payments.

Printer8

Haven't people made glorious amount of money taking out debt to buy additonal homes? People who have been paying down loans have missed out.

Hi Nifty

A comment not of meaningful substance worthy of a response.

Cheers

Wow that's 'high and mighty'!

Fritz

It was simply an obtuse comment in the context of the discussion and Nifty knows it.

Not at all. Pay down your debts has been terrible advice for a long time now. Of course that may change very soon.

Depends what kind of debt, pay down your consumable debt like credit card, holidays, hire purchase, cars is great advice. Pay down debt on assets that increase in value is not so good advice. Unfortunately many people don't make the difference and were taught "all debt is bad, period" which is bad advice

Yeah true, although better to never take on those debts at all if at all possible.

The reality is that - provided no major Covid event - the economy has feared far better than expected and as BNZ point out there is increasing likelihood that we may see RBNZ raising rather reducing the OCR in the next year onwards.

For recent FHB with a $600,000 mortgage; a 0.5% increase will mean a $3,000pa increase in interest payments - that is equivalent to around $4,000 pre tax annual earnings (there goes that annual salary step/ bonus) or fortnightly $120 after tax out of the pocket.

In the near future that could easily be 1% or 2% or $240 or $480 a fortnight - feeling comfortable?

When taking out a mortgage the bank stress tested one’s affordability for around 6%; that’s not meaning affordability for usual luxuries, domestic holidays and updating the car.

While one should pay down high interest debt - e.g. credit card - as a priority, mortgages although low interest, the principal is far, far larger and even small increases in interest rates can be significant and crippling.

Banks stress tests 6% +/- with a person's existing expenditure. If the person has been spending 'luxuriously', a responsible lender i.e all main banks will take that into account at time of application. You can't deny that people have made alot of money by increasing their housing debt and taking advantage of increasing house values by buying additional property and/renovating. Your blanket statement is not applicable to everyone, and is misleading.

Jimbo

When you want to see where you are going look ahead not behind you.

I don't regret paying off my mortgage early. Does anyone?

Potentially. You may regret it if you don't have the ability to borrow against your house again due to a change income, bank policy changes etc. Your money is fully tied up in the house and can't be utilised anywhere else.

Nifty

Your comment shows you really don't understand.

In the vast majority of instances, when people have "paid their mortgage off", they may have a zero balance but do not have the mortgage lifted from their title. The mortgage most commonly continues to be registered against the title and is not addressed until the property is sold - the mortgage is simply dormant.

It makes total sense as a borrower. If there is a further desire for a loan - for what ever purpose such as a new car - then one is not paying far higher interest rates for an unsecured loan and of course there is not the cost in first paying to have the mortgage to be lifted from the title, and then the cost in re-establishing a mortgage.

The number of people retiring with a "mortgage" is surprisingly high but in many instances these are dormant mortgages. I am one; I paid my "mortgage off" some fifteen years ago but still have a mortgage registered against the title of my home; this provides the bank ongoing security at no cost me and they have given me a considerable overdraft facility (which I currently have no need to use) at no cost. If I so wished, I could walk into the bank tomorrow and leverage of my home to buy a rental property without it costing to re-establish a mortgage.

Printer 8

I didn't say anything about what you're going on about? You paid your off your home loan but you still have a mortgage secured with the bank...well done.

The bank doesn't really care how much equity you have if you have no income or very little income to make the repayments - eg. NZ super. Good luck borrowing against your owner occupied home if you're in that situation, it wont be anywhere near as easy as you allude it to be.

Well technically I didn't pay it off yet, I have just been sitting on 100% offset for almost 3 years now. Best of both worlds, unless there's an OBR event of course...

I'm looking forward to having the mortgage paid off, at the current rate, 13 years of ownership. Payments increase as pay goes up.

Sure, "opportunity cost" etc etc but i'm risk averse.

but you responded anyway...

Printer8: "Hi Nifty A comment not of meaningful substance worthy of a response. Cheers"

Haha yeah classic

Nifty

Your 12.31pm posting is incorrect, misleading and shows a lack of understanding.

Erroneous postings are not only embarrassing for you but need to be corrected and that I will continue to do.

Make sure you know about what you post.

Wrong on my income also. :)

Cheers

Printer8

You're delusional, time and time again you get proven wrong but can't see it or admit it. I guess that comes with age...

Cheers

Very few would have predicted the OCR would be .25% a few years ago.

have you not heard , debt is GOOD, i know of a farmer that has more cash in a TD than their loan for the farm and the bank trying to convince them to use an offset mortgage to cut the interest rate to no joy , as they have always been told by accountants to keep the debt level at max

I’ve always said that rising interest rates shouldn’t be an issue for most people on a salary as interest rates normally rise when there are inflation and pay rises. But for investors with low cashflow I doubt we will see enough rent inflation to cover the interest increases, could get interesting.

Is this financial advice??

Banks cartel already prudent remember? - ouh look March last year LVR gone, let's boogey, and even at gossip level if rbnz going to put it back again.. the cartel already put it all back.. hmn.. it seems that 'prudent' word is in the eye of beholders (tobacco, alcohol, gambling Co.s etc).

So much of the commentary -- both for and against rate changes is based on huge assumptions - not least that we wont have another lockdown due to Covid.

It would take only one real outbreak and a 6 week L4 lockdown across Auckland for all teh pixie dust to be blown away! -- there are still a huge number of businesses and jobs out there -- that are hanging on by a thread -- many that are only just starting to recover and very few with any reasonable reserves -- it will take a lot longer for resilience to be built into those businesses-

all decisions should include a weighting for another severe lockdown -

Exactly. Everything being rosy - which it *generally* is - is predicated on no further lockdowns.

More lockdowns and things could change dramatically.

Not that dramatically. We've had shorter, sharper lockdowns since last March and the economy adapted better every time.

Hospitality does it tough, but there tends to be little contagion from failures - hardly any capital tied up in it and no barriers to entry means that it's a high turnover industry anyway.

The capital tied up in Hospitality is all in the property lending, its not a problem, until it is.....

So far the lockdowns have been short

Looking at the rapid fall in the unemployment rate to pre covid levels, it should be a hell of a lot quicker than that or else we are going to have a even bigger mess on our hands.

may be a good time to fix long here

Hmmm. Been thinking about that.

Since NOBODY really knows where rates are going the sensible thing for most with high mortgages would be to chunk it up into maybe 3 parts and fix 1/3 short term (eg 1 year), 1/3 medium term (2 or 3 years) and a third long term (5 years). Kind of a reverse gamble or hedging, which is probably more sensible than playing a guessing game.

"The rebound in the level of GDP, the surging housing market, higher than expected inflation, and now falling unemployment all make it obvious that the combined efforts of the Government and Reserve Bank to support the economy through the Covid shock have had a much more powerful effect than anticipated."

That's the best summary, well done Westpac

And well done RBNZ and NZ govt. pity about the massive increase in house prices but I’m fairly certain that will change if interest rates go back up so should only be a short term issue.

Hmmmm, mixed feelings. The runaway house prices are a tragedy, but on the other hand we have come through the economic headwinds very robustly....

The govt deserves some credit for sure, the right always lambasts the left on the economy, well here we are with lowering unemployment etc etc.

Good luck with "I’m fairly certain that [house prices] will change...". Hope is not a strategy, and asset prices in illiquid commodities such as housing are notoriously sticky on the downside.

Imagine, if you can, a scenario where interest rates are 5-6%, RV is $1m, and you've advertised the shack for $1.3m. The sole offer after 90 days on market is $900K. Are you gonna accept That, or just sit tight and Hope for a better offer?

That will be determined by the market. It's the market decides the price.

There will be plenty of people who can sit tight. There will also no doubt be plenty of people who cannot sit tight.

Always best to increase the OCR prior to the next disaster or you have no powder to burn as a Central Bank. The increased noise of increasing rates seems to indicate imminent disaster in the financial sector.

Yeah I will be far from surprised if there's a financial crisis in the next two years. I have been calling it to occur in 2022 for a couple of years, but it could be this year.

I put my KiwiSaver into cash a year or so ago expecting a meltdown and of course the opposite happened. If you want I can give you a heads up on when I tire of waiting and put it back in growth, the share market will no doubt crash that night.

Jimbo.. I am the same with property. Have been saying there could easily be a big correction (and warning readers to be careful) for a year now. Started looking at rentals last week and would have to laugh at the irony if I bought and a huge correction followed. Who knows.

Kiwi saver is another Govt sponsored scam where money is transferred from the average Kiwi to huge financial institutions by way of extortionate commission that nobody can avoid. Almost in the league of RE charging over 30K to sell your house.

First time ever someone will try to wind down a ponzi.

A question for the economists: Is the govt stimulus being included in the GDP figures? How would a person find out?

analysis from UK probably relevant...

... money created through QE was used to buy government bonds from the financial markets (pension funds and insurance companies). The newly created money therefore went directly into the financial markets, boosting bond and stock markets nearly to their highest level in history. The Bank of England estimates that QE boosted bond and share prices by around 20%. In theory, this should make people owning shares feel wealthier so that they spend more but... very little of the money created through QE boosted the real (non-financial) economy. The Bank of England estimates that the first £375 billion of QE led to 1.5-2% growth in GDP. In other words, through QE it takes £375 billion of new money just to create £23-28bn billion of extra spending in the real economy. It’s incredibly ineffective, because it relies on boosting the wealth of the already-wealthy and hoping that they increase their spending. In other words, it relies on a ‘trickle down’ theory of wealth.

Yes. Trickle down BS v Keynes re propensity to consume.

By far the biggest benefit of QE went to the share market and property through asset price inflation. The rich got (a lot) richer last year.

This is not govt stimulus. This is the dividing of existing wealth into smaller and smaller pieces and redistributing it. Most of the redistribution has gone into consumption or increasing asset prices. B-all has been directed into anything productive.

In the depression we planted forests and built highways. This time round we have splurged it into nothing.

And we celebrate how well we are doing? BS. We have squandered the future for a quick high.

It's going to be an interesting 12 months. The employment data that's just been released by stats.govt.nz in my opinion isn't fully formed because the wage subsidy extension has only just finished, and EOY is looming when struggling businesses will decide whether to chuck it in or soldier on. If the RBNZ are forced to raise the OCR, we could be in for a double dip of austerity as the true employment figures start to percolate, and the squeeze goes on people who were foolish enough to max out their leverage on a 2% mortgage. Not to mention the international economic environment, which will blow any RBNZ policy out of the water one way or another whatever they do.

Crux here is WILL the RB in fact raise rates when inflation supposedly requires them to?

10 year bond market rates already double hat they were at the bottom of cycle when they were around 0.5 in NZ and USA and of course negative in Japan and Germany.

That which cannot continue will end, as I have quoted repeatedly, as have others.

Interest rate cuts cycle, with minor alterations in world, has been downwards since 1987 roughly.

As Steve Keen has written many times and been ignored, when debt ceases to grow exponentially, the debt induced house price growth will end. Exponential growth in debt and credit requires rates to go down continually. Now they cannot go down further because of inflation. I called this 6 months ago at least, ie asked what would happen when inflation arrived and stated that it would. Now people are expressing surprise and still in denial. As usual economics profession is 6-9 months behind because their views are based on daft models.

House prices rise not because supply is lower than demand but due to price of debt falling.

So, when price of debt ceases to fall, game is over for asset bubbles.

QE does not boost house prices of course, esp at the middl to higher end.

Except, IT DOES

https://wolfstreet.com/2021/02/02/the-feds-monetary-punchbowl-is-fuelin…

Fortunately I sold most of my bonds 2-3 months ago, and I was left with only 3% of my investments in bonds. But gosh it still hurts. I see a bleak future in bond prices, with interest rates that will go up in NZ and internationally, within the next 18 months.

In any case, a moderate increase to the OCR should happen now, otherwise a bigger increase will be required later on. The sooner the better for the economy in the longer term. Current monetary settings should be revised with urgency. If an increase to OCR deflates the NZ housing Ponzi, all the better.

Lies, damned lies and statistics

"The change in forecast from the BNZ follows the stunning fall in unemployment for the December quarter to 4.9% from 5.3% in September - a result that went right against market expectations (and the forecast of the RBNZ) that unemployment would rise to 5.6%.

The employment figures have now removed all talk from the marketplace of the possibility of any further interest rate cuts. ANZ economists, who had been forecasting one further cut this year to the Official Cash Rate, taking it down from 0.25% to 0.1%, now say they no longer expect any more cuts"

However...

"As at the end of December 2020, the number of working-age people on

Jobseeker Support increased by 44.1 percent, compared with the December

2019 quarter. The proportion of working-age people receiving JS has been

increasing since the December 2017 quarter."

"6.8 percent of the working-age

population receiving JS as at the end of

December 2020"

https://www.msd.govt.nz/documents/about-msd-and-our-work/publications-r…

The unemployment stats only count those who want to be in work. Those happy enough to be depressed whilst on a main benefit will increase beneficiary numbers whilst not impacting unemployment figures.

How can the underutilisation rate decrease by 2% but the people on the Jobseeker increase by 40%. It doesn't add up.

According to Stats NZ the jobseeker % increase figure should be included in the underutilisation numbers:

Underutilisation reflects people who: do not have a job, but are available to work and are actively seeking employment – unemployed - link

The criteria on workandincome.co.nz is identical to the criteria outlined in the underutilisation measure:

To get Jobseeker Support, you generally need to either: not be in employment and looking for a job; be in part-time employment seeking more work;

have a health condition or disability which affects your ability to work.- link

If the number of people on Jobseeker support in April 2020 was 174,630 when lock-down started (source RNZ), then that's an increase of 70k people. No small amount and something seems off.

MSD obviously didnt get the memo.....suspect theres considerable jawboning going on.

There will be justification no doubt for the discrepancy if required but along with CPI the measures are selected for the desired purpose.

best to keep some powder dry till the everything bubble bursts, which cant be too far off now.

Interesting how AAA rated companies can default on their bonds

https://www.chinabusinessreview.com/podcast/a-look-at-chinas-recent-spa…

Does it cross a residential property investors mind they are "devaluing" all major FIAT currencies, all the time (primarily the US dollar) - that is why house and other asset prices are rising.

What is going to happen when wages and salaries get left further and further behind, as landlords interest payments increase, along with the new regulations for rental properties etc. These costs will no doubt be passed onto the tenants, who increasingly won't be able to afford them ....so they will go to Jacinda who will smile and give them an accommodation supplement top up.

So the government gets more and more into debt ...and debt that they can't pay.

But in the meantime the tax payer is forking the bill......

It's such a sh*tfest ....I'm all in to Cryptocurrencies - at least I can get something back for my money !

It's happening right through the western world. Fiat might take a while to go under, but it's time has come. There's thousands of incoming DeFi solutions to replace and improve every sector of the currently centralised financial ecosystem. Only a few have to succeed to completely up end the whole banking apple cart.

As for government taxation right now - sorry but I lost my crypto wallet on a USB stick in a boating mishap.

@Ezy ....it sure is ...all western currencies are just buying less and less whether its a USD NZD AUD EUR CAD GBP ...as you said, it will only take a well thought out and cleverly executed DeFi solution for a very small market like NZ and the banks will be left wondering what happened, as currently them, the MSM, stockmarkets, RE and its "hangers on" think the current status quo is just going to carry on "ad infinitum" .........

Indeed. Take a look at $COTI. Thank me later :)

me too; PMs, crypto, macadamia trees...

This is all going to make a great fireside story some day.

It's a bull in the making by all participants.. we called herding the sheep slowly, BNZ just over fear of the unknown - nothing will happen bro, keep on lending into housing the more and steep the ups, the better.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.