By Gareth Vaughan

As submissions from the banks on the Reserve Bank's proposals to increase their regulatory capital emerge something will become clear. The four Australian owned banks oppose the plans, whilst their smaller New Zealand owned rivals support their regulator's move to level the capital playing field.

With this in mind what would you expect a submission on the proposals from New Zealand's pre-eminent business lobby group, BusinessNZ, to express?

Some reservations about the potential for higher bank capital requirements to flow through to interest rates charged to business borrowers? And perhaps some enthusiasm that the levelling of the playing field aspect of the Reserve Bank's proposals could, even slightly, improve competition in a banking sector almost completely dominated by the Australian owned banks?

BusinessNZ's submission certainly addresses concerns about the potential for the Reserve Bank proposals to cause higher businesses borrowing rates. But it makes no mention of the proposal to improve the competitive position of NZ owned banks against their Aussie owned rivals.

'Your costs are going up'

BusinessNZ CEO Kirk Hope told interest.co.nz the driver behind the lobby group's bank capital submission is concern about the potential impact on business borrowers. With ANZ, ASB, BNZ and Westpac, combined, holding 88% of banking system assets and 88% of banking system liabilities, the reality is they dominate the banking market. And Hope, whose previous job was CEO of bank lobby group the NZ Bankers' Association, doesn't think levelling the capital playing field for the NZ owned banks would make much difference.

"The reality for business borrowers is it's not going to make a more competitive market. Because you're essentially just saying for the bulk of the business banking market share, 'your costs are going up', which is not going to help business borrowers. So our perspective was from the perspective of business borrowers. And the likelihood of it leading to a significant increase in competition, we would like to do some more work on that. But my initial view on it would be unlikely. It really looks to us just like it's going to push costs up," said Hope.

"I'm sure they [NZ owned banks] would welcome a levelling of the playing field. [But] the other consideration for us is we're representing our members and those members are the four large banks, none of the other organisations [banks] are direct members of ours."

How the big 4 have a capital advantage

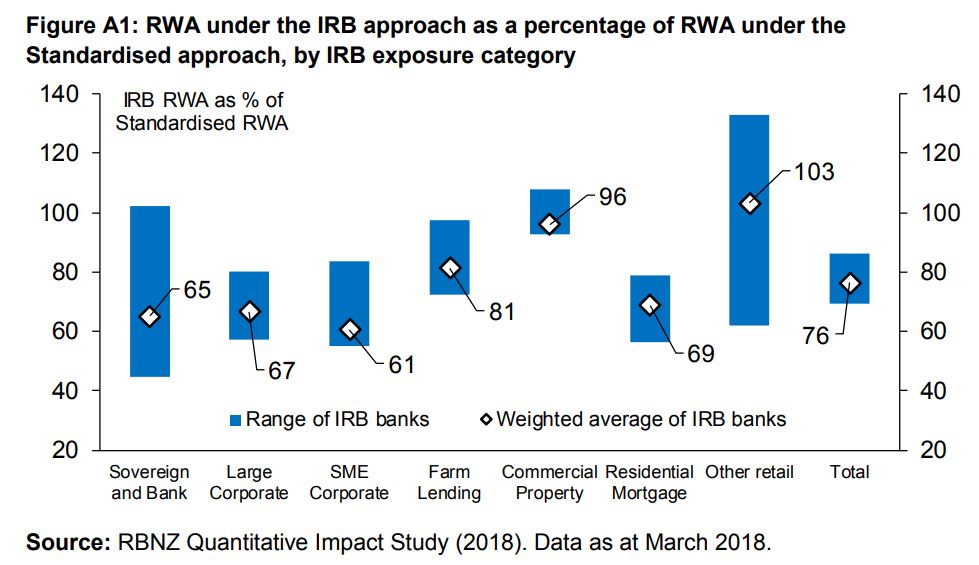

ANZ, ASB, BNZ and Westpac have, since 2008, been using what's known as the Internal Ratings Based (IRB) approach to credit risk measurement. Other NZ banks must use what's known as the standardised approach. This means the big four banks are allowed to set their own models for measuring risk exposure which they must then get approved by the Reserve Bank. In contrast banks using the standardised approach have their credit risk prescribed by the Reserve Bank.

Effectively what this means is the big four banks are able to hold less capital than if they used the standardised approach giving them a profitability advantage over their Kiwi competitors. Or put another way, the Aussie owned banks can use a smaller portion of equity funding for mortgages than standardised banks, which translates into a funding cost advantage. This is a factor in the significantly higher return on equity the Aussie-owned banks generate than their local rivals. In the December quarter, for example, ASB's return on equity was 15.3%, and ANZ, BNZ and Westpac's ranged from 13.1% to 13.9%. The best of the NZ owned banks was SBS Bank at 10.3%, with the rest in single digits.

A Reserve Bank probe of the big four banks' use of the IRB approach to credit risk shows them with risk weighted assets (RWA) equivalent to 69% of the standardised approach used by all other banks for residential mortgages. Across all types of lending combined, ANZ, ASB, BNZ and Westpac have credit risk RWAs of between 67% and 86% of the comparable standardised calculations, with an average of 76%. Risk-weighted assets are used to determine the minimum amount of capital that must be held by banks to reduce the risk of insolvency. The capital requirement is based on a risk assessment for each type of bank asset.

The Reserve Bank is proposing to make the Aussie owned banks increase the assets they use to determine the minimum amount of regulatory capital they hold to the equivalent of 90% of what's held by other NZ banks, up from 76% now. This follows lobbying from NZ owned banks. For example, In a combined 2017 submission to the Reserve Bank, The Co-operative Bank, SBS Bank and TSB Bank argued the regulator should standardise the measurement of risk weighted exposures across all banks.

"This would result in all banks holding the same level of capital for the same underlying risks, ensuring a level playing field across the banking sector. This will encourage further competition in the banking system, consistent with the Reserve Bank of New Zealand objectives," the three banks argued.

The chart below comes from the Reserve Bank consultation paper. You can see more on the differences between capital requirements for the big four banks and the NZ owned banks, and what the Reserve Bank is proposing to do about this here and here. Overall the Reserve Bank proposals would see banks required to increase their regulatory capital by about $20 billion over a minimum of five years. Submissions on the proposals close on May 17.

'One of the most significant good for NZ Inc outcomes of the proposals'

In Kiwibank's interim results announcement in February, CEO Steve Jurkovich said the state owned bank understood and supported the Reserve Bank's capital philosophy.

"It creates more of an even playing field in several areas, like how capital requirements are calculated, but it is not without implications. We understand and support the Reserve Bank’s philosophy," Jurkovich said.

A former ASB senior executive, Jurkovich also told interest.co.nz narrowing the difference between the internal models and standardised approaches to capital makes a lot of sense.

Asked to comment on the BusinessNZ submission, a spokeswoman said Kiwibank was still working through its own submission, and didn't want to comment until that was finalised and made public. A TSB spokeswoman also declined to comment ahead of TSB making its submission to the Reserve Bank.

Co-operative Bank CEO David Cunningham said he was surprised BusinessNZ had made no mention of the Reserve Bank's proposal to level the capital playing field between banks.

"It is surprising that this doesn’t get a mention. The levelling of the playing field, and therefore robust competition which will be more important than ever with the interest rate impacts of the higher capital proposals, is arguably one of the most significant ‘good for NZ Inc’ outcomes of the proposals," Cunningham said.

SBS Bank's chief financial officer Tim Loan said SBS "obviously" welcomes a closer alignment of the capital ratios.

BusinessNZ says its members are four regional organisations being the Employers' and Manufacturers' Association (EMA) Northern, Business Central, Canterbury Employers' Chamber of Commerce and the Otago Southland Employers' Association. In turn, businesses who are members of the four regional organisations are BusinessNZ's business members.

The four regional organisations do not publicly disclose the names of their members. But according to the EMA, there are more than 14,500 member companies within BusinessNZ, which is "committed to championing a production, export-oriented, competitive business environment in which enterprise can thrive." BusinessNZ's website says the group advocates for enterprise and promoting the voice of thousands of businesses across NZ, working for positive change through new thinking, productivity and innovation.

SBS and TSB are members

In terms of bank members, as Hope noted above, the big four are members. Westpac is also principal sponsor of the Canterbury Employers' Chamber of Commerce and sponsors its annual awards. Westpac also sponsors BusinessNZ’s annual 'back to business party' at the start of the year. An ANZ spokeswoman says ANZ occasionally co-hosts local business and networking events.

Whilst none of Kiwibank, The Co-operative Bank or Heartland Bank are members of any of the regional business groups that make up BusinessNZ, spokespeople for both SBS and TSB say their banks are members.

Meanwhile, the BusinessNZ submission says; "BusinessNZ does not support any increase in bank capital requirements." This is a similar view to Westpac, whose CEO David McLean told interest.co.nz this week; "the need for an increase in capital is hard to justify." ANZ CEO David Hisco suggested the Reserve Bank proposals could leave New Zealanders facing additional annual costs of $2.4 billion based on a return on equity of 12% for the big banks. Whilst BNZ CEO Angela Mentis and ASB CEO Vittoria Shortt have both said higher mortgage rates, lower deposit rates and credit rationing are possible in response to the Reserve Bank proposals.

Fears for SMEs

BusinessNZ's submission also raises concerns about the potential impact on small and medium sized businesses, SMEs, from the Reserve Bank capital proposals. Given SMEs source much of their funding through banks, the lobby group argues it wouldn't like to see such borrowers pay "unnecessary additional capital or borrowing costs where this is not commensurate with risk."

"Many small business owners use housing mortgage finance to partially fund business activities. They may do this for a variety of reasons including, but not limited to, the fact that housing mortgage finance is generally less costly than business finance. By in effect restricting this source of finance, the ability of many small business ventures to get off the ground could be unnecessarily restricted," BusinessNZ says.

"According to the Ministry of Business, Innovation and Employment, 97% of New Zealand businesses employ fewer than 20 people. Many small businesses have little in the way of assets to offer as collateral for loans, so often personal housing is used as security."

Interest.co.nz recently wrote about floating mortgage rates, arguing they were too high to justify and banks should cut them. We noted such rates apply to some SME owners who use property as loan security. Asked whether there was scope for banks to reduce these rates, Hope said this was a good question.

"You're quite correct to point out that a lot of small and medium sized enterprises will use their property as security, [and] there's a case to make that that's a fairly low risk lend for a bank. So are those rates as competitive as they could be? What are the features of the lending, ie the business risk plus the home loan risk, if you like, that are leading to those higher rates? And are they valid for the risk that bank is taking in that particular business?"

"I think there's always opportunity for scrutiny of those rates. And bear in mind when you look at a headline rate there's always going to be a whole lot of other things going on like competition in the market and so on and so forth," said Hope.

The key point, he added, is if there's reasonable competition in the market, which he believes there is, borrowers should be able to take advantage of it, and should be able to "hold their banks to account to ensure they are getting the best rate they can."

Reserve Bank data shows the weighted average new overdraft interest rate paid by SMEs was 9.45% in April.

Comprehensive cost/benefit analysis sought

Ultimately Hope said BusinessNZ's key point is the Reserve Bank should undertake a comprehensive cost/benefit analysis of its proposals before taking any further steps.

"We've said on the face of it this looks to be pretty challenging and to have some pretty significant impact for New Zealand businesses. That was the basis on which we said the Reserve Bank needs to have a deeper think about the cost/benefits," Hope said.

"We take them [the Reserve Bank] at their word it's a genuine consultation, they want to understand a range of perspectives, and they'll have a think about it. That's what our hope about this would be. The voice of a business borrower is an important voice, [which is] why we thought it was important to have the view of a business borrower in there. This has some potentially pretty significant impacts for businesses," Hope said.

In a video interview with interest.co.nz in February Reserve Bank Governor Adrian Orr said the fact the consultation paper details the potential for higher mortgage rates, lower deposit rates, credit rationing by banks and an impact on Gross Domestic Product, shows benefit/cost analysis work.

Typically Reserve Bank policy development sees the estimated costs of the proposal considered when the policy proposal is being developed, and when decisions have been made about what part of a proposal to implement, and what to alter in response to feedback, a final cost/benefit analysis is done. A full cost/benefit analysis is then published with the Regulatory Impact Statement.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

13 Comments

We should have a level playing field. People don’t seem to realise that many monopolies or market dominance comes about because of governmental and regulatory advantages. Let’s sort it out.

This won't only level the playing field but as importantly will reduce the risk of a public funded bailout if there is a significant event and one of these lenders takes more losses than their model predicts. That in itself is reason enough to support the RBNZ proposal.

Yeah it's weird this isn't mentioned anywhere as it is one of the major benefits. I guess when the OBR policy was pushed through, the big banks were pretty happy the government gave them a get out of jail free card so modified their internal risk models to take advantage. Next should be replacement of the OBR for something more sensible...

The cause and effect chain of increase bank capital is interesting, and poorly understood. It includes a lower OCR (as ANZ Economist Sharon Zollner said last year and we saw this week), and not higher business borrowing rates as OCR reduces to reducing business activity. Standardised Risk models may also reduce currently high bank risk aversion, while at the same time limiting bank failure risk in adverse parts of the cycle.

Borrowing cost isn’t the main issue, it’s the currently high risk aversion, which limits business investment in innovation and succession. Banks now measure risk very accurately, and internal models drive them to avoid it.

The other interesting thing is where capital will come from. Banks have high earnings, but not the scope to accumulate required capital at the rate implied by RBNZ, and maintain earnings to attract this capital. Nz partial listings, NZSF Investment ?

I'm with Orr on this one. He had a pansy attack last week, but he is right to require all banks to behave in a manner consistent with the stability of the whole system in mind (that's NZ Inc). Too much cream has been disappearing across the ditch for too long in my mind, & now I learn that, by the way, they had an advantage over the other banks by deciding themselves on their gearing & lending ratios & God knows what else, required. They're pissed it'll lose them market share & so they should be. But they've had it too good for too long & it's nice to see NZ Inc fighting back on this. Go Orr.

'deciding for themselves their gearing and lending ratios'... my god, please pick up a book. They have demonstrated to the RBNZ that their internal models operate more efficiently than the standard approach the RBNZ applies to other banks. The RBNZ must approve the banks use of internal models.

Their RBNZ-approved models drive the capital requirements of each bank. The issue is here the RBNZ have by in large announced they neither have the skills or inclination to try and understand these models and in doing so are reducing every bank to the lowest common denominator... the standard model.

Banks will have no reason to proactively manage their own risks and capital and will simply pivot to arb'ing the RBNZ standard model. It will make banks more risky.. not less... as all banks will simply run risks the standard model misprices.

At a time when every other regulator is investing in its skills and resources shouldn't we be asking why the RBNZ are going to other way and seeking to dumb down their oversight?

NZers need to voice their opinion on this.... do we want a supervisor who is engaged and actively challenges the banks models and inherent risks.. Orr do we want one that is seeking the easy road because he cant be bothered understanding how banks actually manage their risk?

"Banks will have no reason to proactively manage their own risks." That's an extraordinary statement. Which bank do you work for, and is this the in-house view?

yea.. ok .. fair call... but no more outlandish that many of the other comments whining on about increasing capital.

The debate is not about (nor was it ever about) the banks having to raise the capital levels. They know they do and are expecting to globally and domestically. The debate is to how much is prudent. I think the NZ public deserve a little better from the RBNZ than a blindfolded throw at a dartboard in establishing a prudent amount to raise capital by.

By their own admission... no cost-benefit analysis has been conducted. The consultation paper is woefully below what is normally a very high standard of work from the RBNZ. Orr and Bascand should be embarrassed over what has been produced.

The ability to use the Internal Model is a tailwind however there are other factors at play. The 4 Australian banks are some of the highest rated financial institutions (AA-) globally and can fund themselves at lower rates than the local NZ banks. That funding advantage opens up a lot of doors. Also there are scale returns in operations, tech, systems, reporting etc.

That's funny - you asked a "very good question" and instead of answering it - Hope came back with a whole set of questions instead. I had to smile.

Point is, why did you have to raise it - isn't he supposed to be raising these very issues with the big four banks on behalf of his SME members (who are indeed getting fleeced)?

What I took from that exchange is that in BusinessNZ terms: "all animals are equal, but some animals are more equal than others".

BusinessNZ has a very vested interest. All the big banks are members. They dont represent SMEs at all, look to me to be a nice lobby group for all the big boys.

Removing the capital advantage sounds great. But this does not necessarily mean that it has to come with increased capital ratios across the board. As a commentator mentioned, the scale/credit ratings/cost efficiencies of the big 4 contribute a lot to the cheaper cost of funding.

As if it's not clear enough in the article I'll pull out the key part: "we're representing our members and those members are the four large banks" So the Aussie banks are using BusinessNZ as lobbyists, that's all this article needs to say.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.