By Gareth Vaughan

On Wednesday the Reserve Bank unveiled plans to both reintroduce restrictions on banks' low deposit mortgage lending, and provide the same banks with up to $28 billion of funding priced at the record low 0.25% Official Cash Rate, which they can use to fund home loans.

Against the backdrop of a housing market that's on fire, the Reserve Bank's taking with its left hand and giving with its right hand. On what planet does that make sense?

That would be Planet Conventional Economic Settings.

Reserve Bank Governor Adrian Orr, currently New Zealand's favourite punching bag, was at pains to point out the Reserve Bank's actions are designed to try to meet its mandates.

"I think it is really important to understand that we are doing what we are doing today, and always, for the purpose of the Reserve Bank's mandate and operating within its remit. And that is about making sure the [goods and services] consumer price inflation remains somewhere between 1[%] to 3% per annum on average, and that employment is as best can be near its maximum sustainable level. And that is what's driving our action today," Orr said.

"Around the loan-to-value restrictions...the other mandate is to ensure financial stability. And we have seen a marked acceleration in higher risk loans particularly to investors in the property market."

The high loan-to-value ratio (LVR) restrictions are about higher risk loans and making sure "they don't cause unnecessary long term problems for the [financial] institutions," Orr said.

Reinstating the LVR restrictions on home loans is required because the Reserve Bank's decision to remove them in April with just a weeks notice was a mistake. Obviously the decision came against the backdrop of immense uncertainty caused by COVID-19. But waiting for some evidence the LVR restrictions were gumming up the works in a COVID world might have been advisable, especially given they can be removed so quickly.

What sort of society do we want?

But a bigger issue for me is whether we actually have our economic policy settings right. And this is a really important question because it goes straight to the heart of what sort of society we want.

Do we want a society where the children of renters have little to no chance of becoming a home owner? And one where even some of those whose parents are home owners must wait for their parents to die before they can get an inheritance and afford a home of their own?

In an interview with TVNZ's John Campbell on Friday morning, Orr fingered a lack of housing supply as the problem when questioned by Campbell about young people being priced out of the housing market.

"Inter-generational fairness is something that I would lose sleep over but it's not something that I can intervene with with the tools of monetary policy," Orr said.

"Yes, supply side is absolutely critical, affordable houses. Central government, local government, industry, get together, get it sorted, move on."

However monetary policy settings in the age of COVID have ushered in record low mortgage interest rates meaning for people with job security, the combination of super low borrowing rates and greater capacity for and willingness from banks to offer low deposit lending, means there has never been a better time to buy property. And that's just owner-occupiers. If you're an investor with equity in existing property/properties, with capital gains and wealth taxes ruled out by a popular Prime Minister and miserably low bank deposit rates, fill your boots.

Cheap credit is a key factor spurring on demand for houses in a market where the national median selling price surged 20% in the October year.

Now that's not to downplay the supply shortages. At the end of August 20,385 eligible households were on the waitlist for state or social housing. That's the first time the number has topped 20,000 and this has occurred with the border shut to immigrants. It has also happened despite new dwelling consents rising every year since 2012, and 52% year-on-year in Auckland during September.

What economic settings do we need to achieve the society we want?

Getting back to the question of what sort of society we want, my sense is a comfortable majority of New Zealanders want one that's egalitarian in the sense of housing opportunities. A key question then becomes what economic settings do we need to help achieve this?

In terms of the Reserve Bank's inflation target, arguably this is applying outdated conventional economic thinking in unconventional economic times.

Inflation targeting became all the rage for central banks in the 1980s. And fair enough. High inflation was a problem. But it's not now and hasn't been for some years.

As Orr put it on Wednesday: "One thing we know about central banks globally, they have proved highly effective at fighting inflation from high to low. We don't have a great track record to date of fighting it from very low back to something within their mandate."

Richard Yetsenga, chief economist and head of research at the ANZ Banking Group, recently told me something similar.

"When we adopted conventionally applied inflation targeting three decades ago, nobody even raised the issue about what happens if monetary policy can't get inflation to rise. It wasn't even a question. And clearly we've discovered it's a really important question," Yetsenga said.

Yetsenga suggests against the backdrop of COVID, central banks are effectively targeting "a mixing bowl of objectives" around inflation, unemployment and financial stability, and that this is likely to continue.

With major government fiscal support for the economy, John McDermott, a former Reserve Bank assistant governor and head of economics who is now executive director of public policy researcher Motu, recently told me there's a need to think more holistically about how the economy works. McDermott suggested dusting off the fiscal theory of the price level and the quantitative theory of money and adding them to the monetary policy mix.

The quantity theory of money is a theory that variations in price relate to variations in the money supply. And the fiscal theory of the price level describes fiscal and monetary policy rules such that the price level is determined by government debt and fiscal policy alone, with monetary policy playing at best an indirect role.

There's also the question of whether the Reserve Bank's inflation target could be moved lower to, say, 0% to 2%. And could we be measuring asset price inflation, something that's currently not happening? Remember we now live in a world where capital is no longer scarce, it's oozing in all directions, and technological developments mean human labour isn't required to the extent it used to be. See what author and Macquarie analyst Viktor Shvets has to say on this breakdown of capitalism as we know it here.

What is maximum sustainable employment and is it good enough?

Then there's the Reserve Bank's mandate to target maximum sustainable employment.

Just what is maximum sustainable employment? In February the Reserve Bank said in its estimate employment was "around or slightly above its maximum sustainable level," at a time when the latest Statistics NZ figures had 112,000 people unemployed, giving an unemployment rate of 4%.

Turning once again to the question of what sort of society we want, is 4% unemployment, with more than 100,000 people out of work, something that's acceptable? Or should anyone who wants to work be able to?

Arthur Grimes, former Reserve Bank chairman, chief economist and an inflation-targeting architect, recently told my colleague Jenée Tibshraeny the Government's 2018 decision to add maximum sustainable employment to the Reserve Bank's monetary policy remit alongside inflation was a mistake. Instead, government fiscal policy should address unemployment, Grimes argues.

Concern has been mounting in recent years over future work opportunities against a backdrop of advancing technology, such as artificial intelligence, reducing the need for human labour. Interestingly this week National Party leader Judith Collins named herself as party spokesperson for technology, manufacturing and artificial intelligence.

These fears over dwindling work opportunities have led to the promotion of a universal basic income (UBI), whose most vocal NZ proponent is Geoff Simmons, until recently leader of The Opportunities Party. Another concept with growing support is a government job guarantee. The Tasmanian Greens successfully moved a motion recently calling on the State Government to investigate how a jobs guarantee might be implemented in Tasmania during the COVID-19 recovery.

"The impacts of the pandemic on Australians and Tasmanians is devastating and it will have generational impacts. The power of having employment, of having a job and the dignity of work, cannot be overstated," Cassy O'Connor, the leader of Tasmania's Greens, said.

Steven Hail, lecturer at the University of Adelaide School of Economics, describes a job guarantee as offering a government job to everyone who would like to take such a job. Hail also describes the concept of a job bank, through which jobs are available for people to draw on in local communities, depending on each community's needs.

In the September quarter New Zealand's unemployment rose to 5.3%, or 151,000 people. In last week's monetary policy statement the Reserve Bank said this rise suggests employment has fallen below its maximum sustainable level. Unemployment is expected to rise further next year as the full impacts of the COVID crisis take effect. Is it thus not an opportune moment to consider whether targeting maximum sustainable employment is acceptable in the type of society we want?

And then there's QE, and housing...

In a further effort to meet its monetary policy mandate the Reserve Bank is running a Large Scale Asset Programme, or Quantitative Easing (QE). Through this it's buying government and local government bonds from banks and pension funds in the secondary market. It's currently planning to buy up to $100 billion worth with new money by June 2022 with the aim of pushing down interest rates.

Evidence from overseas, notably the United States over the past decade, suggests QE benefits asset owners, especially owners of property and shares, over non-asset owners and thus increases wealth inequality. A Columbia University report for the Department of the Treasury concluded QE more than likely mitigated income inequality in the US, but just as likely exacerbated wealth inequality and consumption inequality. Once again, is this the sort of society we want?

Back to housing, the newly minted Labour-alone government has pledged to overhaul a long-term bugbear of those decrying a lack of housing supply, the Resource Management Act, and have the Commerce Commission probe the competitiveness of the building supplies sector. There are other housing market bugbears that interest.co.nz readers are familiar with such as local government consenting costs, land prices, and banks' regulatory capital settings through which housing loans require less capital to be held against them than loans to businesses.

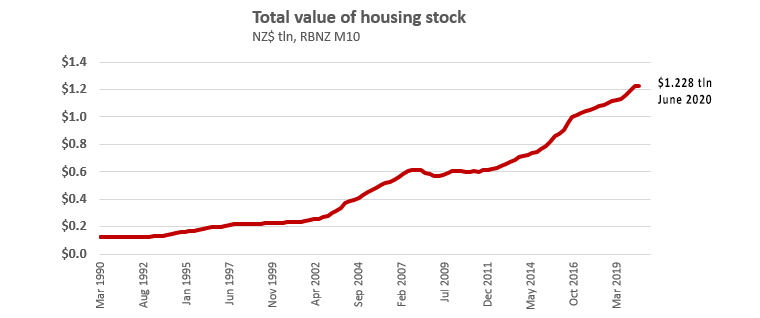

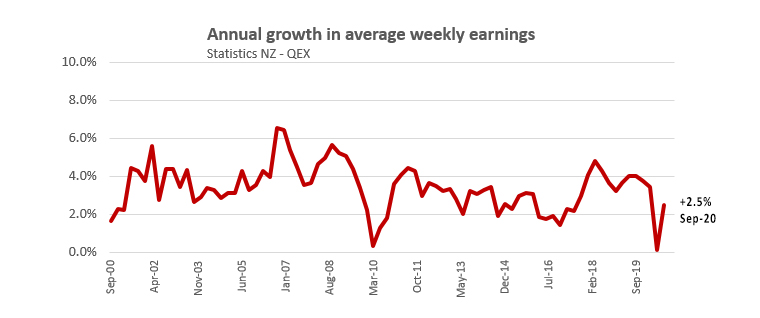

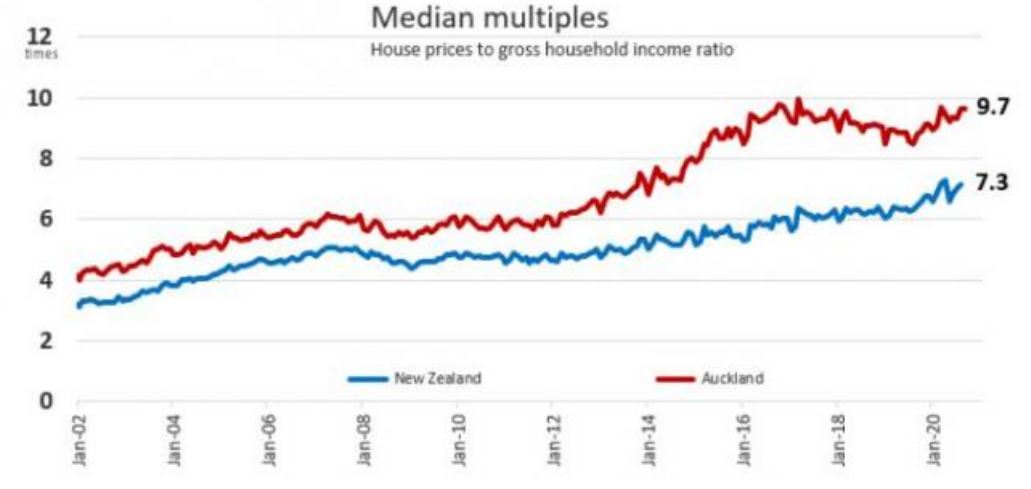

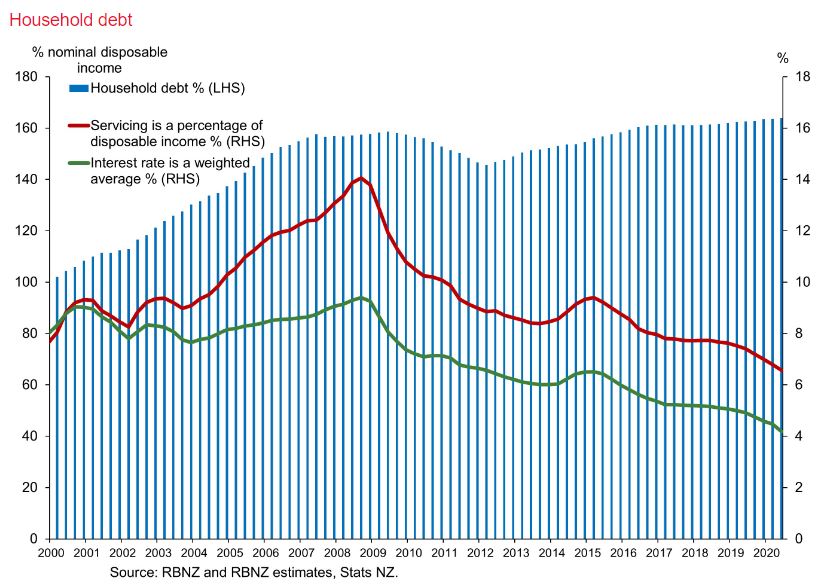

The reality is New Zealand's housing market is broken and has been for a long time. Statistics NZ figures show 65% of households owned their own home in the third quarter this year, down from 74% in 1991. Wage growth has lagged the soaring growth of housing values, sending house price to income ratios higher, leading to high household debt levels, as demonstrated in the charts below. All this means a significant rise in mortgage rates, should it ever occur, would cause significant economic pain to homeowners with big mortgages.

The salutary tale of Francis Fukuyama

Back in 1989, the same year the Reserve Bank of New Zealand Act was passed enshrining the central bank's independence and inflation targeting mandate in law, American political scientist Francis Fukuyama famously proclaimed the end of history. Fukuyama made this call after the fall of the Berlin Wall hastened the demise of communism in Eastern Europe. Thus, he argued, free-market liberal democracy had won and would become the world's "final form of human government."

In 2018 Fukuyama issued a mea culpa via an article entitled, Against Identity Politics The New Tribalism and the Crisis of Democracy. He noted democracy had retreated in virtually all regions of the world with authoritarian countries, led by China and Russia, becoming more assertive.

The tale of Fukuyama is a good lesson that finality is a very big concept. And that dogmatic positions can come back to haunt you. I hope that as we New Zealanders continue to debate the short comings of our property market, our Reserve Bank's mandate, key economic settings and the sort of society we want, we remember that the world is always changing and what was the right approach once might not be anymore.

131 Comments

RBNZ keeps missing inflation target,

and employment is not at the max sustainable level (going by their commentary)

So their objectives are being missed.

Were they impossible/impractical? Then they are the wrong objectives and should be changed.

Were they possible/practical?

Then Adrian should be rolled.

It's strange how the price of oil is rarely mentioned as a factor in inflation. Oil is a major cost in the production of everything we buy, so just maybe its price might have something to do with inflation - high oil price in the '70s, very low price now.

Also very interesting to review this interview from early June with Jenee and James Shaw. At 2.55, Mr. Shaw talks about QE and asset bubbles:

https://www.interest.co.nz/news/105399/central-banks-money-printers-fir…

And David Seymour's suggestions that government require the Monetary Policy Committee consider asset price inflation targetting:

https://www.interest.co.nz/news/107565/david-seymour-suggests-governmen…

Inflation is between 1-3 range (1.4%) so he is doing his job. He is 100 times better than Wheeler who missed range for several years.

Inflation @2% should have been abolished with the gold standard, it was a target because thats how much more gold entered the system each year. We dont need it now , and god knows those whose wages have been stagnant for years dont need it

What would you set it at then? 0,5,25%? Wages have been stagnant due to a stagnant dysfunctional CPI measure. Core inflation is different (although linked) There needs to be control for core inflation and for that there needs to be a target.

Agreed - but is it not sensible to have a moderate inflation rate as a buffer to deflation, which would cause havoc?

Demographic driven?

https://www.bis.org/publ/work722.pdf

Who cares if he's meeting his target or not if he's destroying this country to do it. He's totally lost his moral compass. Its the same as a company polluting rivers and destroying forests to meet its target of maximizing profit.

It may not be in his remit, but he has to take responsibility for his actions.

Great article Gareth. What we want has been lost amongst a bunch of economic mumbo jumbo and acronyms.

For example: Some say the way to raise GDP is to keep wages down. That's a contradiction and it's stupid. GDP has become our master.

GDP or GDP per capita? Raising GDP is easy, open the immigration floodgates. Raising GDP per capita is the measure of efficiency and what I’d like to see used.

Even though I think GDP is a dumb measure in the first place, it should be at least Real GDP per capita and with inflation including all inflation that includes house prices. Orr just caused inflation in houses to go up 20%, that's excluded form his inflation target but people still have to pay for housing. From https://www.hud.govt.nz/news-and-resources/statistics-and-research/hous… about 75% of people spend over 30% lets say 30% of the average house hold expenditure is housing that means inflation just when up by 6% on housing alone. Yeah inflation is 2% what a bunch of nonsense. Its much easier to manipulate the number than actually fix the economy.

Great article. Sadly these questions aren’t openly discussed and lead by our leaders...they remain private talks around the BBQ

The political parties have lost their way. "What New Zealanders want" is what they should be talking about.

Judging from the hysteria about Greens tax proposals, what New Zealanders want seems to be endless untaxed capital gains on property assets. So it is not just our leaders who are the problem. This may end badly...

Agreed. All the do-gooders crying for change but just don’t take their money for nothing capital gains from them. Can’t have it both ways

Capital Gains tax is a red herring, it will do nothing, you also pay 0 capital gains on shares, (you pay tax on dividends, but you also pay tax on rent - expenses). The share market has outperformed property prices consistently and no dealing with tenants. The reason I think we have high property prices is, 1 you can borrow to invest in housing but not in shares (negative gearing). 2. People do not believe that property will ever go down, so have gone crazy with the amount they will spend. Look at bitcoin, a currency that uses 482,000 times more power per transaction than visa (https://digiconomist.net/bitcoin-energy-consumption) and is so unstable that it could never be used as a real currency but enough people still invest to make go up. It is human nature and a system that is fundamentally based on greed.

I believe that capital gains tax on house prices would actually make things worse, currently this and previous governments have not been willing to do what it takes make property prices come down, do you seriously think they will if that means that they will if they have to give tax refunds to all the people who own property that have lost money. In my opinion not a chance in hell.

Bitcoin is not supposed to be used to buy coffees and other daily transactions. It is a final settlement layer that will be used ultimately to settle balance of accounts between central banks. What you need to be comparing it to is the settlement price that central banks pay to transfer gold between themselves. https://money.cnn.com/2017/08/23/investing/germany-gold-reserves-new-yo…

Bitcoin is pristine collateral. You hold the keys no one else can own them.

The on-chain transactions (which you are referring to) is the base layer of the network, second layer networks like the lightning Network will be the daily transactions layer. These are then batched together for one on chain transaction.

the Reserve Bank's decision to remove them in April with just a weeks notice was a mistake.

If can be removed within a weeks notice WHY can it not be introduced again within a weeks notice SPECIALLY now when it is accepted that it is and was a misyake.

WHY MR ORR.?

It can, 3 of the major 4 banks have come out and done it.

Orr is being disingenuous saying it cannot be applied. He is clearly trying to leave it late as possible to try and pump the market more. Why is he pumping the market as much as he can? Time people started looking into his own interests, how many properties does he have...

For some reason he is looking after property investors at the expense of everyone else. Orr is blaming everyone else except himself for the housing problem when he says it is not his business. If the law has to be changed to include housing in the CPI then so be it.

As he said the other day, it’s house prices increases or depression. He’s avoiding the depression option. I feel a bit sorry for the guy - he has literally been made captain of the titanic at the moment the watch starts yelling ‘iceberg’. He’s pulling levers to try and avoid the iceberg but it’s too late, you need to show caution before it gets to late to avoid the iceberg - we’ve had that the last 10 years but we decided it was full steam ahead so the rich in first class feel special and to hell with those with the cheap tickets in the decks below.

There response needed to be more targeted. Instead they left it up to commercial banks to decide which have then gone on to have a party. The banks come out now with tweaks to placate political fallout but it’s not enough and far to late.

Depression/ recession should be viewed as natural process of over exuberant capitalism. The phenomena is too complex for man to control. Every action has a consequential action that Govt and Central Banks view as collateral damage

Change the CPI to include housing. .. A nice practical and instant solution that won't take the government too much more than 3 years to introduce. They will campaign in 2023 on the idea and policy, no hold on, the new way is not discuss any policies as thats boring for the voters and the govt can be held to account later

blobbes

You serious?

"Time people started looking into his own interests, how many properties does he have..."

For a start the decision is made by a RBNZ committee.

Simply a conspiracy theory with no intellect that adds nothing and distracts from a serious issue.

Then let's look at the interests of everyone on the committee. The result of the reserves banks actions were completely predictable. Why did they do it. Why are they waiting 5 months to fix it.. Answer these questions. Questioning the motives of the reserve bank is what everyone should be doing.

The inflation measure is loopy. How can they say it's now low, when people who could once afford to buy a house no longer can. Calculate inflation correctly.

For some reason house prices are NOT included in the Consumer Price Index. That is why the CPI is irrelevant .

Yip our OCR might be in the 5-10% range right now if house prices were included - and if you look at M3, then you will see there is inflation in terms of money supply - but it’s not in consumption, it’s been moving into assets.

Yeah this is crazy. If we agree that decreases in interested rates effect house prices now more than anything else, surely that has to be factored in. Housing is most consumers biggest weekly outlay.

It always seems to me that RBNZs actions, in using its preferred policy tools and interest rate settings, are likely to actually be deflationary over the medium and long term. We don't really hear them talk about longer term management of price stability but if they remain reactionary they'll likely perpetuate the same approaches that lead them to where they are today.

Media helping create FOMO

https://www.newshub.co.nz/home/money/2020/11/skyrocketing-house-prices-…

They should be required to state that these articles are an advertisement. Maybe a #AD in the headline. Maybe chuck in a #FOMO too.

The article quoted ardern saying "Labour will continue to improve the availability of land for housing through better-integrated planning and investment in urban development, infrastructure and transport, and set standards for quality urban design," she said in a statement."

She does speak double-speak, over complicated twaddle doesn't she. She plans to "improve availability" at the same time as raising "urban design standards" ... does she even know anything or what she is saying? A big NO

Agreed Fh, Central Govt can't force LG to increase the supply of land nor can they directly steer the planning process. Her last three years have proven what the "improvements" to infrastructure and transport look like and, as you say, improvements in "quality urban design" is simply a vacuous, immeasurable commitment to more mediocrity. She IS the master of waffle

The PM will solve all these issues with the Build Back Better programme which she is following. (Note her election victory speech).

https://www.weforum.org/agenda/2020/07/to-build-back-better-we-must-rei…

BBB will usher in a new utopian socialist controlled ‘capitalism’ where private property, small business ownership etc may need to be reconfigured.

The voters have spoken

Did they have any choice?

Yes. Or are you suggesting all are the same

I think MB is suggesting - quite rightly - that there wasn't much in the way of viable alternatives

Do we follow the Argentine path of decline or the Yugoslavian one? This seems to be coming to something of an head in the US at the moment, if we follow the BBC we will not be far behind.

That’s in the eye of the voter.

I submit the reason is more to do with popularism trumping policy.

NZ is far too conservative at times.

What sort of society do kiwis want? Sadly I think alot want what we already have. Try talking to your average boomer about the issues - you'll likely get a blank stare followed by a lecture on how hard it was in their day & how smart they've been to accumalte their wealth. Ain't no body going to take that way from them.

I am a boomer, so I gained significantly from these assets booms (in virtually all asset classes) in the last 20 years or so, but I am disgusted by the type of society that the likes of Orr are causing to come into existence. I am also alarmed by the potentially catastrophic effects to the soundness and stability of the NZ financial system that this ultra-loose monetary policy is potentially causing, together with the eye-watering amount of landlord welfare subsidized by the productive economy.

Me must tax heavily all forms of speculative housing, increase LVR limits to at least 50% minimum for all speculators, remove landlord welfare and immediately increase interest rates: all of these actions combined will balance the NZ economy and make it healthier in the medium term. Pity that no government will have the balls to do it, unless really forced to do so.

I am a boomer like you, having, with my wife, earned very ordinary incomes for most of our lives. We are now in a comfortable position due to careful money management, a modest lifestyle and a bit of luck with a one house property investment. It is immeasurely harder now for young people to get ahead and own their own dwelling, certainly in Auckland. I am very disappointed that high LVRs are not on new investor mortgages. I continue to be disappointed by the successions of Labour governments that profess to be for more equitable economic outcomes yet enact policies that essentially do the opposite. Sure, they tinker with industrial relations legislation and slight improvements to health and education but little else.

I find it ironic that the last government stuck to keeping public debt to around 20% of GDP during a time of a massive housing problem and worsening poverty levels yet happily take on more debt as a way to lessen the impact of Covid and continue to allow home ownership levels to drop. Their 'vision' for NZ society seems to be little different to National's. I wish Ms Adern would stop the hand-wringing and do something effective.

Don't knock us Boomers Nifty. Speaking as a Boomer who has done very well, mostly accidently, out of ridiculous house price rises, I can also say I am seriously alarmed at what this is doing to young people. Including my ownchildren.

No blank stare here, and from time to time I have posted that (by comparison) , how easy it was for me as a low income worker 50 years ago.

Virtually guarantee that the boomers above however voted for status quo government, either Nats or Labour. Because they are going to fix it...

They (as did most of the country) voted for the established mainstream parties because we didn't want a bunch of untested unproven idealistic crackpots anywhere near Parliament - seems to have worked (thankfully)

How do they become tested if nobody gives them a shot? I reckon MMP is a stupid system and proportional representation would at least allow a more diverse parliament. This might let the majority hear and see a fringe group and what they stand for in parliament, then when they go voting they could make a relatively informed decision. It would also mean all MPs are accountable to an electorate and not a party.

Your comment bemuses me. So NZ votes instead for idealistic establishment parties that support a failing crackpot system!?

Also, how do 'untested' and 'unproven' parties become 'proven' in your mental construct if they never get a turn in power?

I certainly wouldn't want any social or economic experiments run at a time such as what we find ourselves in now. Obviously with circa 1% of the vote gained by each of these fringe parties neither did the rest of the electorate. If you're referring to TOP as a candidate then it's interesting both their leaders tossed their toys after being shown the door. When their theories are tested and ratified by the IMF, the World Bank the G20 or another reputable organisation then perhaps they'll be more acceptable - until then.. no thanks.

Ok, so basically you're saying stick with the status quo because you feel it is working well and the establishment and elite support it. Gotcha.

I'm saying stick with what has been accepted and is mainstream, tweak it where necessary.

If you're in a speeding car you apply the brakes to slow down - you don't slam it into reverse and hope that'll work.

Depends, what if the car's about to go off a cliff?

Well Nifty what would you do? Accepting that slamming the vehicle into reverse would shred the gearbox/transmission and not slow you down one iota. You could slam the handbrake on, but that would step you sideways and you'd go over the cliff sideways instead of front first

Indicate, pump the brakes and turn hard.

Impressed with your defensive driving skills - especially the indicate bit.. lol Glad you opted for the brakes rather than the "slam into reverse" option.

Then do not come on here and complain that house prices are too high, wage growth pitiful, FHBs are getting a raw deal or that the system is rigged toward property investors. Because none of that will change while we keep voting in the parties that were responsible for making all of that happen.

If you can't recognise that the housing crisis exists because of the actions/inaction of Labour and National over the past few decades, there isn't much hope for you. It's clear a lot of people are suffering from a cognitive dissonance, they keep voting in the same people who promise to keep the system the same, then whinge about how the system is broken.

I think your reply is aimed at the wrong person blobbles.. I'm not complaining or whingeing about house prices but I do acknowledge there's an issue, as there is with wage growth. For the record I own (freehold) my property (40 acres) and have absolutely no interest in rental or any other form of housing investment.

I do however have an issue with unproven theoretical experiments proposed by fringe parties lead by comparatively unqualified idealists. The current Govt has the tools via MP and the RBNZ to alleviate some of the issues - whether they do so remains to be seen.

Do you want things to change? If your answer is "YES!", then there is no way that will happen under Labour and National, going off their track records. That includes lifting wages, they have zero idea how to go about making our economies more productive. They promised last election to build 100k houses (to fix the housing crisis) and failed miserably. Then they won the election even after their failures, by a landslide. The current government has no motivation to change anything, they haven't changed anything for decades and still keep getting into power. Why would they do anything different now?

In the 1980s inflation rate targeting by a central bank was called by many to be a fringe idea that had zero historical evidence that it would work. NZ adopted it in the 1990's, which worked sensationally. It then spread around the rest of the world with most major economies now doing it. Actually now it seems like a balmy idea to come across a central bank that doesn't do it. The point here is that if you are looking for evidence that something will work before implementing it, you are being extremely conservative. There is a whole host of ideas out there by very well respected people who have recognised the limitations of our current monetary and economic systems. You just have to be bold enough to change, just like we were in the 90's.

Are you seriously suggesting that NZ was a forerunner in inflation targeting by a central bank which the rest of the world then followed?? I think there's a few people who might disagree. As for being conservative - some would call it being cautious, others prudent and still others reasonable and measured, which is as you would expect when dealing with a country's economic future.

As for the respected people - who are they and who are they respected by? If it's M3 theory you're talking about then I'm afraid the people that actually count and are in a decision making roles the world over are far more respectable and reasoned than a bunch of economic academics playing with untested theories in their lecture halls

Ahhh, we were the first country to fully implement inflation targeting, so yes, we were definitely the forerunner. Was when Don Brash was RB governor, don't you remember? https://en.wikipedia.org/wiki/Inflation_targeting

" I'm afraid the people that actually count and are in a decision making roles the world over are far more respectable and reasoned than a bunch of economic academics playing with untested theories in their lecture halls"

Then why are they making the economic situation dramatically worse on all counts? Do you not recognise that we are pushing on multiple strings now. Negative interest rates and deflation/stagflation are just around the corner, that is where the current "experts" are taking us. They are like lemmings running off a cliff because their models said there was no cliff. These are the people we should listen to?

Yep! We need people to be strategic, analytical and bold...unfortunately the older one gets the more risk adverse and conservative they are (on the whole)

Risk averse or more measured and critical?

It’s a proven evolutionary phenomena. Not rocket science.

I find it perplexing that the shifting in DTI metrics is being portrayed as a result primarily of new speculative "high risk " lending , when clearly the removal of the LVRs, by the RBNZ was from concern about the end of the first six month deferred mortgage period. Clearly with a significant amount of mortgages on six month deferral, any refinancing at the end of the first six month period, of those mortgages would be met by a higher debt, and with the potential/ actual loss of income , including rental income, shifting the bell curve of all mortgages . Clearly a significant proportion and for obvious reasons has been shifted to the investor category, from the RBNZ data

As an aside ,over the next year , approximately 50 percent of all mortgages will be refinanced, for the majority, they will reset cerca 200bps lower.

Why not keep the LVR as it is now and move to DTI ratios? I know the RBNZ was calling out for this under the Key govt but haven’t heard anything lately

With wage growth so pitiful in NZ DTIs may not achieve anything material in helping FHBs. Maybe the conversation around housing should begin with WHO should have the smoothest and most equitable path to ownership, and then actually design some policy to achieve that. For example if FHBs are the preferred sector then perhaps mandating cash deposits and refusing equity, maybe DTIs coupled with LVRs, and refusal of all loans with < 25% deposit.

Bang on. The ability to leverage equity is really what gives existing property owners an unassailable advantage over those trying to buy with actual money that they have to earn by working.

Exactly. A property can be purchased with zero actual cash deposit once sufficient equity is built, which isn't difficult if an investor had bought about 5 years ago, in fact even 1 year ago would give them sufficient equity now. The RB and FM will never do this though which begs the question - WHY NOT?? Are they actually scared of the Aussie banks? or worried about their future career prospects?? Is the Illuminati really controlling everything after all (had to throw that in - I'm getting depressed)

This is why I think housing here has ponzi characteristics - you benefit by getting in early but for the system to survive it needs new entrants on a continued basis who can’t see they’re being robbed by those who got in before them.

The greatest challenge New Zealand is going to face is retaining its best and brightest moving forward.

It's been a challenge for years and is unlikely to change until wages lift. Also NZ doesn't always offer the opportunities that some seek - it's too small. Besides we've survived happily enough up till now.

We need inflation for wages to lift. But in theory if we have inflation all costs go up (destroying any realised benefit of the wage increase) so the increases in wages doesn’t help does it?

I remember when wage increases used to exceed inflation by 1 or 2%, sadly those days are gone. Even when wage earners are told on one hand there is a labour/skills shortage, monetary increases barely match inflation or in some cases hours are reduced but the wages are maintained thereby providing the illusion of an increase. Truly a sad state of affairs which seems to be getting more and more entrenched. Indexing wages to the CPI is a failed exercise and has been for a long time - time unions woke up to it.

Exactly. Wages are crap, house prices are crazy, consequently rent is too. Why would they stay?

ultimately, that is the reason why IMMIGRATION happens

True, there is always somewhere that APPEARS better, NZ had mass migration from the Islands to work our textile and car assembly factories in the 60's and 70's. Some found it wasn't that crash hot but couldn't leave.

What no reference to immigration at the ridiculous rate we as a small economy cannot successfully absorb or afford. This is a people problem. We took in too many people and tourists and we couldn’t keep pace with the infrastructure. We need a population plan.

All this hand-wringing about the inability to meet inflation targets, and yet, when there is a sniff of wage inflation, business goes crying to media about massive skills shortages, and the government of the day, not wanting to be seen in any way anti-business, opens the immigration flood gates.

There is a real class system when it comes to wage inflation. It seems we have decided certain industries should be immune to supply and demand forces, whereas in other industries the argument is we need massive salaries to attract the right caliber of person.

It would be interesting to run a "physicality" filter over the areas of skill shortage in NZ, the results might be embarrassing but educational. Also some industries burdened by current labour shortages could quite readily be replaced by imports - not ideal from a long term security view, especially food

Totally agree. I've been saying this for months. We need immigration capped at a reasonable number, I don't really have that number, maybe 10k a year for a decade so we can get on top of everything as you mention.

Has there even been a population target set? NZs population growth as a percentage seems to be a lot higher than other countries like the UK. Yet we haven't built the infrastructure. Not building enough houses is one thing, but also not building enough hospitals, roads, public transpot, wastewater treatment plants, water storage, power stations etc the list goes on. These are all very expensive to provide, yet governments have only looked at the short terms gains that immigration provides. But someone has to also look after these people as they age etc. They are trying to now put up the age of super to try and cope with it, but that isn't popular. We are all going to pay for the high levels of immigration that have occurred. It is not a mtter of if, by when. We are already partly paying for it with high house prices.

The reasons are simple WI - it's called self interest. No one wants higher taxes or rates and what money there is available gets subverted by the "crisis of the day" All designed to calm the masses and get reelected - Local or Central Govt positions and bureaucracy seem to be the only burgeoning sector with little or no true accountability for their failings. Look at the satisfaction ratings (skewed and self serving as they are) of most of NZs councils. I think Rotorua DC (Lakes District Council) didn't even make 50% compliance with their own feeble KPIs

"I think it is really important to understand that we are doing what we are doing today, and always, for the purpose of the Reserve Bank's mandate and operating within its remit. And that is about making sure the [goods and services] consumer price inflation remains somewhere between 1[%] to 3% per annum on average, and that employment is as best can be near its maximum sustainable level. And that is what's driving our action today," Orr said.

Working for wages while inflation, taxation & currency debasement dissolves your purchasing power.Link

Great article. Pity our 'transformational' PM (cough, splutter) isn't listening.

She will just pull out another Concerned Jacinda Frown (TM)

Wage growth has lagged the soaring growth of housing values, sending house price to income ratios higher, leading to high household debt levels, as demonstrated in the charts below.

It's unmanageable when those without mortgages are excluded, according to the RBNZ.

{kind=link}

All this means a significant rise in mortgage rates, should it ever occur, would cause significant economic pain to homeowners with big mortgages

The capital commitment of an Auckland median house price set at $955,000 is out of reach for a median NZ household income set around $68.000. Banks don't entertain DTIs around 14. Too much shareholder risk.

Maybe as suggested above the DTIs would be a viable handbrake. Although a dual income HH would drop the DTI below 10 so would probably still get approved. Imv there needs to be a comprehensive suite of controls applied together - not in a piecemeal fashion, nor left up to banks voluntary compliance. This has to come from the top - PM and FM.

I was not clear - the median $~68.000 wage income I claimed is a household estimate.

Except, it's not, is it. Let's unpack this comment...

NZ Household income - this should be Auckland median income, given that we're talking about the Auckland market. Using the same source you have, this is $94,465. After tax, the median household disposable income for Auckland is $78,461.

Auckland median house price - are you suggesting that first home buyers go out and get themselves a 'median house'? How very aspirational of you. How about a starter home, for $600,000. Seems a little more reasonable, and there are plenty of them around.

Let's assume that our hypothetical couple have a 20% deposit, and buy a $600,000 home. That's a mortgage of $480,000. Fix for 1 year at 3.09% (the current available rate, based on 80% equity) and you have repayments of $472 a week, with a DTI of around 5

While your argument is certainly attention grabbing, it doesn't hold water, nor is it based in reality. Do your homework before you stand up in front of the class & make a fool of yourself.

Find me a $600,000 home in Auckland then. That would be 'cheapest available', not lower quartile.

The Fee-orhetical value of a house, is inflated by lowering the interest rates to make mugs buy into the theory that houses never go down, because we is different. I understand the stupidty is caused by certain individuals who would be broke, if their highly leveraged portfolio sank by even a tiny percent.

I think they do not understand that funny munny has to be bloated by fat cats in banks, who also own real estate and have riden the dead horse they have been flogging for years, but now see the under takers will leave our so called Fair Isles, for somewhere, where a house is still a home and as cheap as chips....

Mortgages in this country are now slave labour factors, as though interest rates are low by banks stealing from savers to fund their ill gotten gains, that some of us will also be not amused by this crime and you cannot flog a dead horse on a market, where funds dissapear into the woodwork, the mattress, the safe havens to indulge our sensibilities. Funding thieves is never been my intention, just like paying Peter to fund Paul, by devious means, means our Capital System is broke, if ya cannot leverage it up, another notch. Proven by the Govt and banking policy of not defaulting loans during Covid.

I could explain, but I have to take some more cash out of the wall and sock it to the Banks, who have stolen my deposits and shuved them up shit creek, in more ways than one. Oh and by the way, Savings for a deposit of shite Houses is as stupid as tossing the tossers more munny to fund a less than Capital Idea. Our rotten and leaky home status, on a shaky island or two is a fund a mental idea, especially when coming into this country, that is more over priced and debt ridden than others per head of population.

Sections in this country are more expensive than a farm in Europe. Go figure, some people are dreaming, just google a section in the USA, they have a cheaper lot than ours......by far. Even Trump does not Buy into NZ....what does that tell you, when the biggest mug in the World, will not let his hair down and come to the Golden Land of the rising 400sqm Gold Mine. .....Awkland, plus floating away on beachfronts, with their multi-million dollar houses, in a few years time, at this rate of storm in a tea cup, Napier, not with standing....on the side of bloody hills and flood plains to the Sea.

See ya..........A Chateau in France is as cheap as chips....and reduced..................INTO the Bargain.

https://www.frenchestateagents.com/french-property-for-sale/view/77983A…

Love it ;)

Easy to post AE, but your posting history demonstrates that you will continue to complain and take no action. Classic DGM.

Being aware and pointing out the obvious to our so-called Financial Ex-sperts is how we can all work together to right the wrongs perpetuated by those with vested interests. I am not poor, but I do hate to see others being screwed by the system. Just ignore what I say in future, but quite a few people do agree with my Tantrums about the screwed side of things and the Ponzi systems we endure to our eternal cost. My intention is to reach many people who read items on this site. We all have different opinions....we ain't regimented like some countries, it is a free world, but not cheap........here in NZ.

Do have a pleasant day. B737......Keep flying high and freely.

It’s interesting to note the sudden enlightenment going on that we might be in serious trouble. It looks like the horse has bolted now and I can’t see a balanced way to restore equilibrium to our markets/functioning society without significant pain for one part or the other of society. Short term pleasure seeking could well now cause long term pain in equal quantity to the pleasure that has been derived from asset price increases that were unjustified - look at any housing market in the world over time that has done what we’ve done - it doesn’t work out well.

"It's out of control. Robertson and Treasury and RBNZ have got themselves into a mess that is NOW beyond their control. Nothing they can do about it. Anything they do from here on in will only make matters worse" by iconoclast 4 days ago - I agree

It may sound discouraging to some people, but until we have COVID under control so that we can open the border and let (lots of) people in, RBNZ can't do much except keeping the show going. NZ needs immigrants to absorb the high housing price and support the running of the economy with a low wage. You will know what I mean if you check the immigration from 3rd world countries since 2000. We had the Chinese and their money during the past two decades, and dare I say - there will be our Indian sisters and brothers' turn from now on.

I'm not sure you could call China and India 3rd world NZC, and we've had meaningful immigration from India for a long while - a lot of hi skilled ones too. Doctors, engineers, IT workers to name a few. It's not immigration per se that's the issue - it's the quality and skills matching that needs addressing.

The mass immigration influx began in 1998 from Hong Kong then exploded from 2001 onward. Why did the Clark-Cullen Government introduce Accommodation Supplements? Was the pressure starting to show

Our 'one immigrant for every new born' immigration settings have been the greatest social experiment since Soharto's transmigrasi policy. Gareth asks what sort of society NZer's want like we have a say in it. The political and media class decide these great social experiments not the NZ voter.

https://www.interest.co.nz/charts/population

Do you really think the "media class" get any traction?

Personally I don't think so

I think the government regard the media as useful fools

Otherwise give us some examples

An article here in the Independent Australia today on the real cost of immigration to Australia. Would NZ be any different?

https://independentaustralia.net/politics/politics-display/population-g…

However monetary policy settings in the age of COVID have ushered in record low mortgage interest rates meaning for people with job security, the combination of super low borrowing rates and greater capacity for and willingness from banks to offer low deposit lending, means there has never been a better time to buy property. And that's just owner-occupiers. If you're an investor with equity in existing property/properties, with capital gains and wealth taxes ruled out by a popular Prime Minister and miserably low bank deposit rates, fill your boots.

Hmmmm...

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion. Link

As economist Prof Bill Mitchell say's here, "Reliance on monetary policy is mindless, ideological nonsense". "The claim by mainstream economists that the lower interest rates will boost spending is flawed". " A sole reliance on monetary policy to boost aggregate spending at a time the non-government sector is resolutely trying not to spend (bar exports growth) is the hallmark of the stupidity of neoliberalism".

http://bilbo.economicoutlook.net/blog/?p=42647

Is another way of framing the discussion that we have been forced to reduce interest rates and buy our own debt because the productive economy has been weakened past the point where it can support the government and financial system overhead?

One very notable aspect is that government jobs tend to survive downturns fairly well, the private sector takes the losses. They are far from equally distributed. This is another part of the inequality generating mechanism.

What has weakened the private sector, I wonder? Over regulation is part of it, but I suspect it is a second order effect. My sense is it is partly immigration diverting resources to house building and infrastructure rather than more productive endeavours, too.

The likeliest culprit seems to me to be excess capital inflows (mainly to fund house price inflation) causing the exchange rate to rise and thus reducing private sector profitability in the export and import substituting sectors. We have scored an own goal from globalisation, using it to borrow and spend in the cities, rather than increase productive capacity and competitive advantage.

Why have we chosen to become New Argentina?

Short term self interest view is why.

Give them what they want now... don’t discuss future problems they are not upon us... yet.

This is the dilemma of democracy vs authoritarianism

Yes. Spot on. The process has been ongoing for 20 years. Enlightenment is happening. Stampeeds can happen in reverse.

Best case scenario is 10 years of very average to no capital asset growth whilst General productivity and wages rebalance.

"average to no capital asset growth"

20 years of mass immigration bringing in liquid assets pushing up house prices, plus all the High Net Worth immigrant Visas, plus all that Foreign investment - where has it gone - cant be right

Immigrants buy existing houses - they dont "build new" out in the outer suburbs

What's to say the vendors don't go and build new houses? Someone is building them obviously so what does it matter who builds them, as long as they're being built

Current account deficits that have to be financed by selling the family silver have been endemic for forty years.

Decay starts slowly, then it speeds up.

By the end of August 20,385 eligible households were on the waitlist for state or social housing, with over 18,000 ranked as “priority A” – the most needy.

This compared to 19,438 the month before and 13,167 in August 2019. The waitlist has more than trebled since 2017.

https://www.stuff.co.nz/national/politics/300144823/public-housing-wait…

Congratulations Gareth for an outstanding article that lays out the issues very nicely.

A key issue is that Orr is saying that he is simply responding to his mandate.

That takes the responsibility back to the political leaders who set the mandate.

I have previously argued that reducing the inflation target to between zero and 2% would be a start.

There is also a good argument that employment generation is best left to fiscal policy.

KeithW

Thanks Keith.

The Humphrey–Hawkins Full Employment Act in the US, mandating the twin objectives of low inflation and full employment, was enacted in 1978. The Fed has used the act to justify unlimited money printing and, due to the resulting asset price inflation 10% of the US population now owns 90% of the assets. NZ is heading in the same direction after adopting the same dual mandate. Another interesting fact, almost simultaneously US workers stopped benefiting from increased productivity and the majority of Americans started saying that the country's economy was heading in the wrong direction. The end result was Trump winning the 2016 election. Unless Jacinda's government rescinds the full employment mandate at once, then the wailing and knashing of teeth in the face of an asset price bubble will become ever louder.

The fact is, examples from Argentina to Zimbabwe prove that money printing does not lead to sustainable employment growth,

Are you not mixing up the money that the banks create for housing ((credit money) with the money that the government creates (currency) for public services, they are two entirely different things with different economic outcomes. We can only store up the governments currency as savings for instance, a non inflationary outcome, all other government created money will eventually be taxed back again and cancelled.

The private sector will never provide jobs for all and this is where the government can step in and use its own fiscal powers and where there is unused capacity in the economy and unmet demand then this is not inflationary.

Zimbabwe had its own set of problems relating to an economic collapse in food production after farms were seized by Mugabe.

I think you're conflating several different drivers into your argument. US worker's rampant unionism and ensuing lack of productivity was one of the key drivers behind outsourcing. Trump winning was a direct result of disaffection with the political establishment and Trump's propaganda regarding bringing back jobs - the same jobs that were offshored due to workers intransigence in the first place

In NZ we have an interesting comparison between Port of Tauranga (high productivity, workplace flexibility, relatively low union membership and public ownership) vs Ports of Auckland (lower productivity, inflexible workforce, comparatively high union membership and effectively state (LG) ownership) speaks volumes imo

Refreshing article - thank you. It's almost like it has taken a global pandemic to get many economists to realise that monetary policy is (and was) pretty impotent. Unfortunately, in NZ we are still pulling at the same ineffective monetary levers... the 'low interest rates' lever might actually be *deflationary* in the current climate and it definitely drives property price inflation (landlords will always buy big when rental yield is so much higher than interest rates). The 'QE' lever makes no difference at all when there is no shortage of capital - it's just Govt welfare for bond owners.

If Govt want to drive economic growth they need to increase aggregate demand. They should cut to the chase and inject funding directly - focusing on activities that give the most bang for the buck economically (and present the lowest inflation risk). They could start by employing some of the 100,000+ souls that are currently being used as a buffer against a non-existent inflation risk.

Deflation is bad because it stops people buying; why buy it when it will be cheaper next year. But that theory doesn’t apply to essentials; no one will stop buying food and petrol if it was going to be cheaper next year. And it doesn’t seem to apply to consumables either; I know that TV will be cheaper next year, but I want it now. So is it possible that deflation is only really bad for assets? The very thing we don’t measure in the CPI!

That seems right to me. Especially given that consumables like TVs etc are a lot cheaper than they used to be. The kind of people who buy 1000 dollar TVs will buy them now because they want them, even if they are cheaper next year. The kind of people who buy $250 tvs will buy them now even if they are cheaper next year, because why wait a year to get a TV when the saving is likely to be small in the scheme of things.

I don't think Gareth Vaughn has read the Reserve Bank Act or the charter or the remit. A torch is being held to Orr and I agree with that. Unfortunately following hard on the heels of Orr is the RBNZ board as well as the Minister of Finance who finds it convenient to keep quiet while the torch is being held to Orr. He has the ability to have a far greater input than he is letting on. The MPC (Monetary Policy Committee) chaired by Orr with a few externals on the MPC having some say. Unfortunately it appears to me that the MPC is a mutual admiration society.

Raise productivity. End of story.

Ha ha.. that's a good one, that's what NZ did the past 15yrs.. in case you've missing the regular GDP figures. NZ is a neat established place for hardworking past generations, is just that.. if you are a new recent graduate with heaps of debt and happened to be catagorised as essential workers? start from rubbish collector, engineer, teachers, police, technician, nurses, doctors, pharmacist, physiotherapist, dentist etc. want to start family? - your best bet is actually across the ditch, I suggest to start from: Adelaide, Perth, Melbourne & Brisbane. Put Sydney as a quick stepping stone, bit expensive but for sure it's not as expensive as AKL though.

Book the flight or quit complaining Mrs Pusheen! Different story, same post.

@JLM. Wrong. There is more to the story, it's called "Ownership". No matter how productive you are, if a country or and individual does not have ownership, they are just working the treadmill.

RBNZ is in unison with the new govt. - majority voting at play finally, Govt should announce the flexi-wages subsidy/supplement extension for out of work Kiwis and soon abolish the RMA & Bright line test. Close sparing partner RBNZ, should open the increased FLPs into property investor, put down negative OCR quickly to at least -2.5%. Vaccine news is here, border to open soon for Tourist, Student, Seasonal worker. NZ will be mad to insert some sort of regulatory measures into this flourish economy. By the way to Ed, that flogging dead horse cartoon is very insensitive, demonized individual. Be fair, please. With the current result surely that dead horse sketch can be transformed into at least a silhouette of strong unicorn?

Unfortunately in the vacuum of courageous transformational leadership NZ is part of the global cancer that is in its final metastasis. There is no solution if it is focused on neoliberalism and capitalism as the engine. MMT is being used the wrong way, because in the cancer there is no other way than to provide more and more money as pallitive care. 'We' are addicted to the fruits of money, as its the path to the Americanism success that's at the source of 'our global' cancer. The Climate Tragedy is another symotom of that same cancer: http://www.one-point-zero.com/a-new-world/changing-societys-architectur… I have solutions but they are of a revlutionary nature, and sadly not for leaders seeking popularity and celebrity....

Borrowing at low rates does not impact on fact that the higher the purchase price of housing then the more you have to pay back. So, if house prices rise 3-5 times more pa than incomes then more of a lifetime's earnings are paying the debt rather than being spent on anything else, more productive or enjoyable (like not working)

"What we want as a society" - never covered in election "debate" not in "policies" neither of which were present in NZ in 2020. Adults I am afraid, in the misty middle, want more services, more debt and not to have to pay more taxes. This innumeracy is encouraged by government failure to talk reality and by private capital love of indebtedness to pull forward spending.

And yet Labour just announced that 1 out of 10 quarantine places are now reserved for foreign workers coming in. And that the parent visa requirements will be relaxed so more immigrants can import their elderly parents. How can any Govt in a time of high unemployment and a spiralling housing crisis, open the floodgates to even more immigrants?

To your last sentence, I agree, it beggars belief.

I don't understand why the government doesn't put a 2-5% tax on housing property investor's mortgages.

Does the Government have the ability to override Reserve bank decisions on monetary policy or any other policy of theirs???

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.