By Gareth Vaughan

The year was 1984. Bruce Springsteen was singing "Born in the USA" and Madonna "Like a Virgin." Mullet hairdos were in and the launch of TV series "Miami Vice" made it cool for men to wear pink and have stubble. The Cold War rumbled on whilst Ronald Reagan and Margaret Thatcher trumpeted their economic recipe of small government and free markets.

Here in New Zealand the cantankerous and divisive Robert Muldoon was both our prime minister and finance minister, as he had been for nine years. This was the era of the Bastion Point protest, Springbok tour, price and wage freezes and Think Big. In NZ the free market very much took a back-seat to Muldoon.

That all changed after an inebriated Muldoon called a snap election in June 1984 and lost it a month later to the Labour Party led by David Lange. Lange, and his finance minister Roger Douglas, inherited a weak economy, a NZ dollar whose value was fixed against a basket of other currencies, and rising government debt off the back of the Think Big projects, whose aim had been to gain NZ more energy independence and create jobs after the oil price shocks of the 1970s.

After his defeat Muldoon stayed on in Parliament. And as an opposition MP a few years later, he turned up as narrator in a stage version of the camp musical the Rocky Horror Show. One of the best known songs from the show is "Time Warp." Recently I've been reminded of both Muldoon and the Time Warp song by NZ politicians' attitudes towards government debt during our election campaign.

Because it feels to me as if their attitude towards government debt continues to be framed by a 1980s mindset, and that the ghost of Muldoon still looms large in their thinking. Relitigating the 1980s is not the right approach in 2020 because today we live in a very different, rapidly changing world. I'm going to set out why this is the case and why it matters. But first things first.

Treasury's recently issued Pre-Election Economic and Fiscal Update (PREFU) forecasts government debt will rise 249% over five years. I am comfortable with that but I anticipate many readers aren't. That's not surprising given the prevailing narrative from our politicians, business leaders and media pundits about government debt. Heck, the resurgent ACT, complete with apoplectic leader David Seymour, has even launched a debt destroyer website.

However, I'm going to argue here that our rising government debt is actually a good thing at the moment.

A 249% debt rise

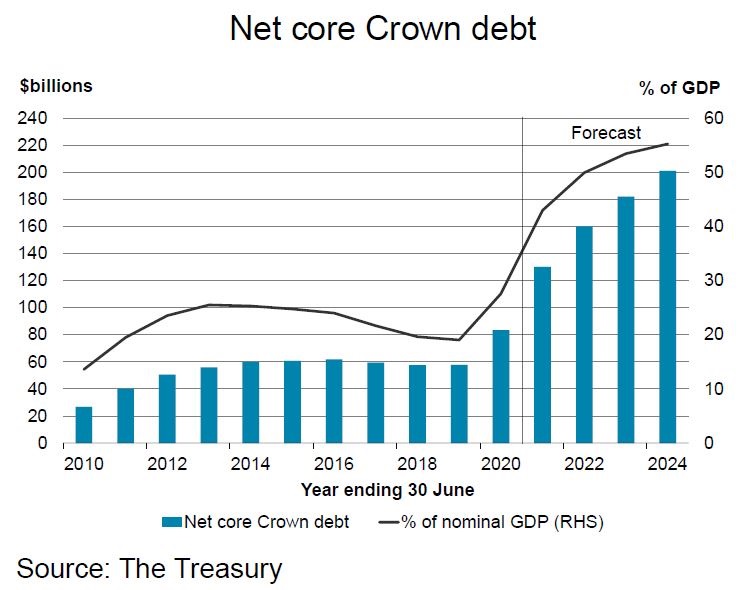

The PREFU has ongoing operating balance before gains and losses (OBEGAL) deficits peaking at $31.7 billion in 2020/21. Net core Crown debt is forecast to rise by $143.4 billion between June 2019 and June 2024 to $201.1 billion. Of course this is primarily related to the COVID-19 pandemic and the government response to it.

In May's Budget Treasury described COVID-19 as a once in a century public health shock causing major disruption to life and economic activity globally, and thus drastically altering the economic outlook both here and overseas. In terms of the impact COVID-19 is having globally that seems a reasonable statement. It also highlights that however the NZ government responded to COVID-19 we were going to have a recession this year.

So just what is our government debt?

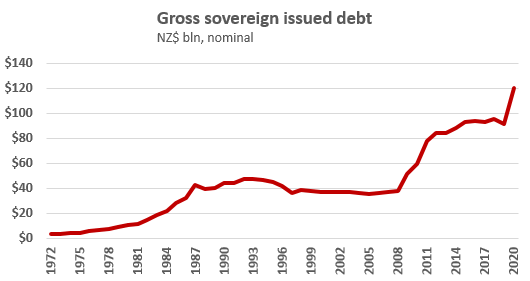

Let's now take a look at what our government debt actually is. New Zealand Debt Management, a unit of Treasury, oversees government borrowing. NZDM issues debt via nominal bonds, inflation-indexed bonds, Treasury bills and Kiwi bonds. These interest paying securities are sold to investors and are all denominated in the NZ dollar. That's important because via the Reserve Bank, the NZ government is the monopoly issuer of the NZ dollar, a sovereign fiat currency.

Fiat money is government-issued currency that is not backed by or convertible into something our government could run out of such as a physical commodity like gold or another country's currency, but by the government that issues it. It's illegal for anyone else to issue the NZ dollar. This means we control our own money supply. And importantly the Labour government that ousted Muldoon floated the NZ dollar, against all currencies, in March 1985. Since then the Kiwi dollar's value has been set by the foreign exchange market.

Treasury bills are wholesale fixed-term debt securities issued for terms of three months, six months and one year. Nominal bonds are wholesale fixed-term debt securities with an initial maturity of more than a year. The longest dated government bond on issue is not due to mature until 2041, that's 21 years from now. The government raised $4.5 billion through this bond issue in July, which is paying investors annual interest of 1.75%. Other countries, however, issue bonds for much longer terms. Austria, for example, recently issued a 100-year bond that's paying investors 0.88% interest.

NZDM also issues inflation-indexed bonds, which are wholesale fixed-term debt securities with an inflation-indexed component. These bonds have an initial maturity of one year or more. A bit like term deposits, Kiwi bonds are the main product offered to individual investors who must be NZ residents.

NZDM also has a euro-commercial paper programme, which issues a type of short term unsecured debt security maturing in less than a year. These can be issued in a range of currencies. The value of debt on issue through this programme is currently equivalent to NZ$1.130 billion.

Additionally NZDM has alternative funding mechanisms available to help meet any short-term Crown cash needs if, and when, they arise. These include an overdraft facility with the Reserve Bank, the Reserve Bank itself, and up-to-date legal documentation for a Euro Medium Term Note programme which is similar to the commercial paper programme, should this be required.

Temporary overdraft increase

The limit on the Crown overdraft facility was temporarily increased to $10 billion from $5 billion for a three month period to July 1 this year, and, according to the Reserve Bank, was utilised for a short period. This coincided with a $5.29 billion government bond maturity in April. Subsequently the account has been replenished following the issuance of additional bonds and Treasury bills. At the end of August the overdraft facility had a positive balance of $23.8 billion.

NZDM generally looks to buy back bonds prior to their maturity to smooth cash flows and to enable investors to recycle their money into new government bonds. Outstanding bonds are typically bought back within 18 months of maturing, with the Reserve Bank taking responsibility for buybacks during the final six month period before a bond matures to ensure overall financial system liquidity.

NZDM says the average weighted maturity of government bonds has increased to 7.9 years from 4.5 years in 2009. The Government has committed to maintaining government bonds on issue at not less than 20% of Gross Domestic Product (GDP) over time to support fiscal resilience and liquidity, and instil confidence in financial market intermediaries and investors.

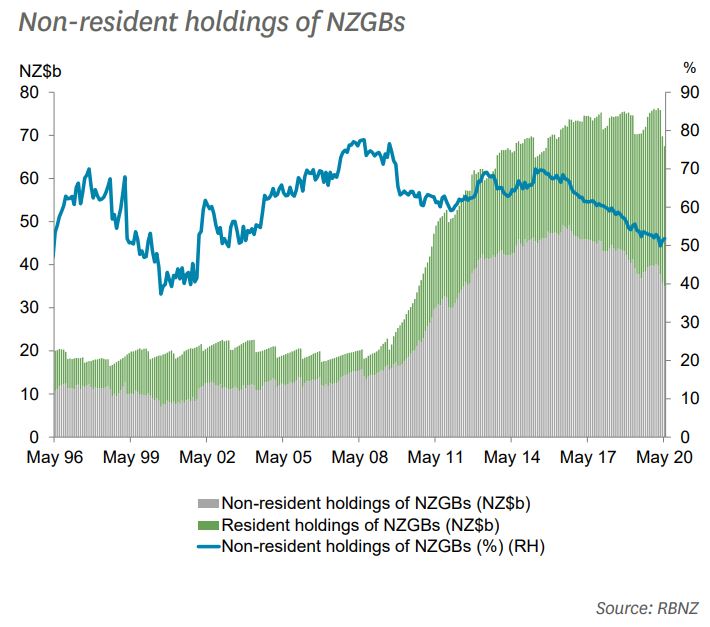

So who holds NZ government debt? Aside from Kiwi bonds, think banks, pension funds and fund managers, or professional investors, here and overseas holding it on behalf of clients. This includes KiwiSaver fund managers, and the likes of the NZ Super Fund and Accident Compensation Corporation. The percentage of NZ government bonds held by non-residents has been falling in recent years, as demonstrated by the chart below, and was at 51.8% at May 31.

Government securities pay investors periodic interest payments and are usually considered low-risk investments because the issuing government backs them. NZ currently has strong sovereign credit ratings from key international credit rating agencies. Credit ratings provide investors with an indication of the creditworthiness of an entity in which they are considering investing. NZ's sovereign rating is the highest possible Aaa from Moody's and the second highest possible AA+ from S&P and Fitch.

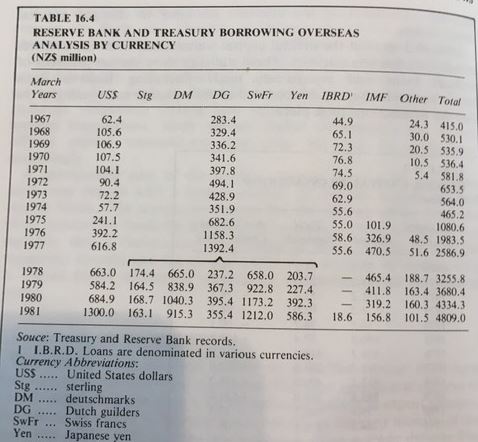

And what was government borrowing comprised of in Muldoon's day?

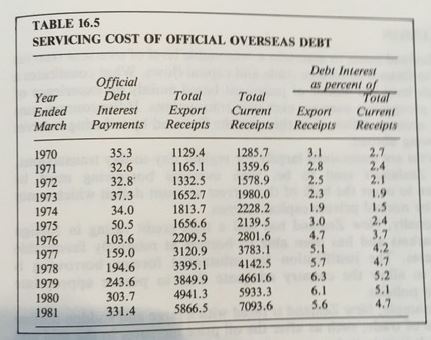

Government borrowing looked very different in Muldoon's day. Prior to the establishment of the NZDM in 1988, government borrowing was handled by a Treasury finance division with support from the High Commission in London, and the embassies in Washington and Tokyo. There was no domestic bond market, so extensive and complex overseas borrowing - where interest rates were typically lower in an era of high interest rates and high inflation following the 1970s oil shocks - was in vogue.

Types of borrowing included direct placements with investors, syndicated loans, private placements with investors and public bond issues. The investors were mostly fund managers and pension funds from a range of countries and the government borrowed in a smorgasbord of currencies including the pound sterling, Deutsche mark, Swiss and French francs, Dutch guilder and Japanese yen. The government also had syndicated standby credit facilities offering short term financing if needed with Lloyds Bank and Citibank.

Shortly after the 1984 election the NZ dollar was devalued by 20%. Given the government borrowing in a range of other currencies, the devaluation immediately increased the country's foreign debt. The average cost of borrowing when exchange rates were factored in ranged from 14% to 18% between 1965 and 1984.

The tables below, taken from the Reserve Bank 1981 book External Economic Structure and Policy, provide some details on NZ's overseas debt in that era.

What QE actually means

As part of its response to the COVID-19 crisis, the Reserve Bank in March launched its Large Scale Asset Programme, or Quantitative Easing (QE). Through this the central bank is buying NZ government bonds from market participants such as banks and pension funds in the secondary market. It's currently planning to buy up to $100 billion worth with new money by June 2022, and could ultimately own around 60% of the outstanding NZ government bonds on issue.

Thus the Reserve Bank is far and away the biggest player in the NZ government bond market. That should keep bond vigilantes, or investors keen to exert power by selling government bonds, or threatening to, and thereby making deficit-spending more expensive, at bay. And through QE the Reserve Bank is siphoning government debt out of the bond market. Sure it remains debt. And the PREFU forecasts the Government effectively buying back its own debt at a premium from banks and pension funds will cost $11.1 billion over three years. But it's debt issued by one arm of government being held by another arm of government.

How does the Reserve Bank exit its bond holdings? As a bond comes to maturity, for example a November 2020 bond issued 10 years ago, the Reserve Bank gets its money back from the Government in November and its holding decreases by the amount of the bond. The Reserve Bank is deliberately buying longer dated bonds, so it takes longer for them to roll off or mature. There has been some speculation the Government could simply write-off government bonds being held by the Reserve Bank. However, both Labour and National say they won't do this.

It's important to remember the key reason the Reserve Bank is undertaking QE is because it believes this will help meet its monetary policy remit. That is: Keep future annual inflation between 1% and 3% over the medium term, with a focus on keeping future inflation near the 2% mid-point, and to support maximum sustainable employment. QE is suppressing interest rates to make borrowing more attractive and encourage economic activity. That means low mortgages rates make housing look more attractive pushing up house prices, and very low bank deposit rates increase the appeal of the share market.

Thus concerns are being raised that, because it benefits asset owners, QE is increasing wealth inequality. In the US, where their experience of QE dates back a decade, a Columbia University report for the Department of the Treasury concludes QE more than likely mitigated income inequality in the US, but just as likely exacerbated wealth inequality and consumption inequality. However, I'll leave a fuller debate over the pros and cons of QE for another article.

What the politicians say

Let's now take a look at what our politicians are saying about government debt.

ACT's Seymour says "our current fiscal track is totally unsustainable." His deputy Brooke van Velden says new government borrowing is equivalent to "$28,000 for each and every New Zealander," and likened the impact of government borrowing on future generations to "fiscal child abuse."

National Party leader Judith Collins says "we cannot continue to have this line of economic morphine in our bloodstreams anymore." NZ First leader Winston Peters wants to "start to pay down debt so that our children are not saddled with the oppressive burden facing them."

Labour's Jacinda Ardern and Grant Robertson, whilst saying increasing government debt on their watch has been necessary to cushion the impact from COVID-19 on households and businesses, are keen to maintain small-c conservative credentials where government borrowing's concerned. Under pressure to implement a short extension to the Wage Subsidy when Auckland returned to COVID-19 Alert Level 3 in August, Ardern said this wasn't going to happen because every dollar borrowed has to be paid back. Post-PREFU Robertson was keen to note that because the Government’s cash position has improved since May's Budget, Treasury has reduced its borrowing programme over the next four years by $10 billion.

And Robertson gave short shrift to pleas for more government support from the struggling central Auckland hospitality sector, where restaurants, bars and cafes have been hard hit by COVID-19 restrictions and office workers working from home. Robertson also says Labour's fiscal plan leaves $12.1 billion of the $50 billion so-called COVID-19 Response and Recovery Fund "protected," which if not needed to combat the health and economic impacts of COVID-19, won't be spent.

Treasury's PREFU has net core Crown debt-to-GDP at 55% by 2024. National wants to bring this down to 36% within 14 years. Either way, the target is an arbitrary one.

By and large business and media attitudes towards government debt are fearful and negative. For example, BusinessNZ says a survey it commissioned shows most businesspeople approve of the Government’s handling of the COVID-19 outbreak, but many are uncomfortable with the resultant debt. BusinessNZ says 60% of the 1,193 businesses surveyed are uncomfortable and 33% comfortable with NZ’s debt reaching 53% of GDP by 2023.

A recent NZ Herald article lumped government debt in with private sector housing, consumer, business and agricultural debt, plus local government debt, saying the combined amount owed is equivalent to about $120,000 for every man, woman and child. Unlike the central government, households, businesses and local government do not issue their own currency.

Argentina, Zimbabwe & Venezuela

Also appearing in a NZ Herald election series are articles by Richard Prebble, a key figure in the Labour government of the 1980s who subsequently became ACT's first leader. Prebble stated that if the Reserve Bank's up to $100 billion QE programme fails, "New Zealand will be another Argentina." And that both National and Labour "have adopted Zimbabwean economics."

"When we are able to travel again, we will find no one wants our money," Prebble claimed.

And Roger Partridge, chairman of think tank the NZ Initiative, reportedly said: "The road from central bank monetisation of government finance leads to Zimbabwe and Venezuela."

As demonstrated above in the explanation of what our government debt actually is, no one's going to come knocking on your door seeking $28,000, or any other sum, from you to pay back the Government's debt.

Virtually all NZ government borrowing is denominated in the NZ dollar today. Argentina defaulted on debt denominated in a currency it had no control over, the US dollar. Zimbabwe's hyperinflation earlier this century had a range of causes including land redistribution, declining economic output, price controls and increased money printing initially to finance a war in the Congo.

The oil dependent Venezuela was hard hit by the falling price of oil. President Nicolas Maduro increased money printing in response to this. Venezuela is now caught in a geopolitical power play, owing billions to China and Russia whilst being hard hit by US sanctions.

NZ's exports have been performing strongly this year. We had a record current account surplus in the June quarter, while the annual current account deficit for the June year fell to just 1.9% of GDP, the lowest for a June year since 2010.

NZ Government debt

NZ Government debt as a percentage of GDP

A year when decades are happening

It was Vladimir Ilyich Lenin, the revolutionary who became the first leader of the Soviet Union, who said; “There are decades where nothing happens; and there are weeks where decades happen.” Lenin may have died 96 years ago but his "weeks where decades happen" reference could’ve easily been about 2020. COVID-19 and its monumental impacts have created the most uncertain world since World War Two. Heck, even the Olympic Games have been postponed for the first time since the Second World War. Literally no one knows when the virus will run its course, or if and exactly when reliable remedies such as anti-virals and vaccines will emerge. If battling COVID-19 itself is a marathon rather than a sprint, then combating the economic impact is likely to be a fully fledged ironman race.

A great example of the uncertainty it's causing is Treasury's PREFU forecast for unemployment to peak at 7.8% in the March 2022 quarter, which is a big shift from Treasury's previous forecast peak of 9.8% in the current September quarter. The reality is no one really knows what's around the corner, or the corner after that.

Tackling the impact of COVID-19 has ushered in the largest government interventions seen since the days of Muldoon. This has included border closures, quarantining people arriving from overseas, lockdowns and the Wage Subsidy Scheme. At its peak in May the Wage Subsidy was supporting more than 1.65 million jobs and by September 18 it had paid out $14 billion. Another example is the Small Business Cashflow Loan Scheme offering interest free loans administered by the Inland Revenue Department to help small businesses hard hit by the COVID crisis. It has seen $1.6 billion lent to small businesses to date. A third example is the COVID Income Relief Payment for people who have lost their job during the COVID crisis, which pays more money than the regular Jobseeker Support benefit.

But NZ, with its Labour-led government, is not alone in having taken such measures. For example, the UK, under a Tory government, has its Furlough Scheme, and Australia's Liberal government the JobKeeper Scheme.

Government debt is surging in other countries too, and in most cases from higher starting points. Credit rating agency Fitch recently forecast Australia's government debt to GDP ratio will hit 60.9% in 2022 up from 41.9% last year, with NZ's reaching 49.4% up from 26.8%. Fitch forecasts Japan's to rise from 232.9% last year to 260.6% in 2022!

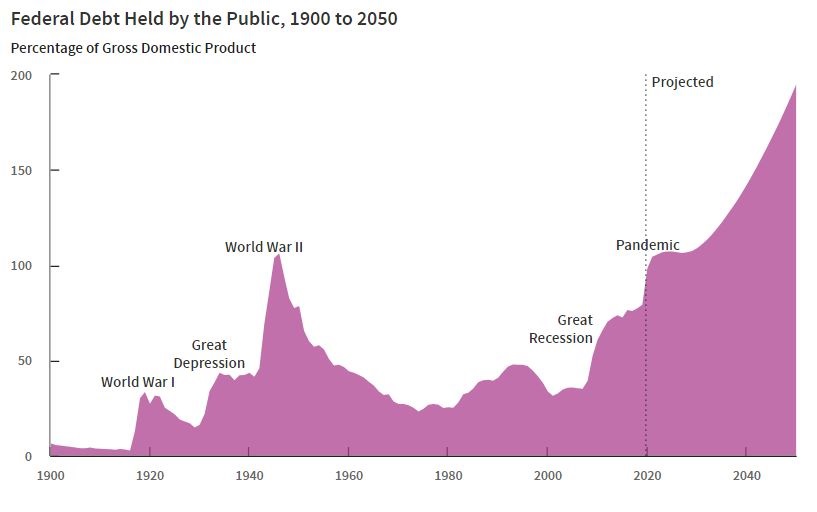

Meanwhile United States government debt will increase from 79% of GDP last year and 98% this year, to 107% of GDP by 2023, the highest in US history, according to the Congressional Budget Office.The previous high was 106% in 1946, right after World War Two. It's forecast to continue increasing, reaching 195% of GDP by 2050, (see chart below). And in the UK public sector net debt had reached 100.9% of GDP by the end of May, the first time it topped 100% since March 1963.

'A delightful moment in history'

Paul McCulley, an economist and the former managing director of high profile investment management firm PIMCO who coined the term "Minsky moment," recently cheered less obsessing over the US government deficit in a Bloomberg podcast , describing this as "a delightful moment in history."

"The budget deficit is quite big enough to take care of itself and needs to be bigger," McCulley told Bloomberg.

McCulley also hailed a sea change from a world where monetary policy has been the dominant, or even sole, economic lever for 40 years with fiscal policy, or government spending, now taking the lead. He spoke of the church and state separation of monetary and fiscal policy in the US in the 1980s, the decade when the same post-Muldoon divorce occurred in NZ with an inflation targeting Reserve Bank independent from government enshrined in law. McCulley said "robust fiscal relief" is required now because of the unique nature of the COVID-19 pandemic, and because monetary policy has largely run its course, having hit "the zero bound."

The US Fed Funds Rate, their equivalent of our Official Cash Rate (OCR) is at 0.00% to 0.25%. Here the OCR's at 0.25%, with the Reserve Bank expected to take it negative next year.

And as McCulley also pointed out, the multi-decade war to slay the inflation ogre "has been over won."

This point was hammered home late last month when US Federal Reserve chairman Jerome Powell announced that whilst the Fed's long-term goal continues to be an inflation rate of 2%, "following periods when inflation has been running below 2%, appropriate monetary policy will likely aim to achieve inflation moderately above 2% for some time."

To most of us that doesn't sound like a big concession. But in central banking it is. And remember the Fed is the world's most important central bank presiding over the biggest economy and the world's reserve currency.

The subtle sounding change means the Fed will be less likely to increase interest rates when the unemployment rate falls, as long as inflation doesn't rise too. Typically central bankers have felt low unemployment will lead to higher inflation, which they’ve preemptively acted against. This is good news in the US where tens of millions of jobs have been lost this year, and official unemployment figures have been as high as 14.7% with 23.1 million people out of work.

NZ CPI inflation since 1977

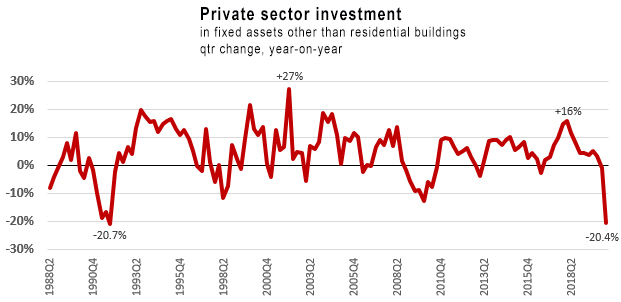

Picking up on McCulley's point about wanting a bigger deficit, private sector investment has fallen sharply in NZ this year (see chart below). This risk aversion hasn't been surprising given the challenging and uncertain world of COVID-19. But it means the private sector has pulled back from investing in the economy. At a time like this the Government is the obvious alternative.

'The expected increase in public debt is entirely manageable and is affordable'

On the theme of monetary policy's limitations when faced with COVID-19, Reserve Bank Governor Adrian Orr acknowledged: "We are first to admit that the front line economic support is fiscal policy." In a recent speech Orr also spoke of: "...the limitation of monetary policy in promoting economic activity when confronted with a pandemic. We can create the environment to spend and invest, but we can’t force it to happen. The outcome instead depends on confidence amongst households and businesses. This also highlights why fiscal policy has been at the forefront to economic support globally – governments are able to directly spend and invest, and ensure resources are mobilised."

Reserve Bank of Australia Governor Philip Lowe has gone further than Orr, specifically making the case for higher government debt in the wake of the global pandemic. Lowe told politicians that fiscal, rather than monetary, policy had provided much of the support to the Australian economy during the pandemic and this was a good thing.

"This is quite a change from how things have worked over recent decades and it is being accompanied by a significant increase in public borrowing as governments work to limit the hit to people's incomes. This shift in fiscal policy is quite a shock for a country that has got used to low budget deficits and low levels of public debt," Lowe said.

He went on to say that by borrowing today to support the economy Australia was avoiding an even bigger loss of output and jobs that would damage its economy and society for years to come, putting an ongoing strain on the budget. Australia's public finances, like NZ's, are in strong shape and public debt is lower than in most other countries, and thanks to staggeringly low interest rates, government financing costs have never been lower.

"This all means that the expected increase in public debt is entirely manageable and is affordable. It is the right thing to do to borrow today to help people, keep them in jobs and boost public investment at a time when private investment is very weak," said Lowe.

In Canada's recent Speech from the Throne Governor General Julie Payette outlined the direction and goals of prime minister Justin Trudeau's government.

"This COVID-19 emergency has had huge costs. But Canada would have had a deeper recession and a bigger long-term deficit if the Government had done less," Payette said.

"With interest rates so low, central banks can only do so much to help. There is a global consensus that governments must do more. Government can do so while also locking in the low cost of borrowing for decades to come. This Government will preserve Canada’s fiscal advantage and continue to be guided by values of sustainability and prudence." (Canada's government debt to GDP ratio was 53.3% in March. Fitch forecasts it will top 120% in 2022).

Turning Japanese as the cost of capital falls to zero

Rather than scaremongering over Argentina, Zimbabwe and Venezuela, Prebble & Co would do better to look to Japan. Rising government debt, low inflation and weak economic growth have been features there since Japan's finance and real estate bubbles burst. Japan's government debt has been steadily climbing since 1990. Its government debt to GDP ratio pushed through 100% in the late 1990s, breached 200% in 2010 just before the massive earthquake and tsunami of 2011, and has continued rising since. After more than two decades of low interest rates, Japan's debt-servicing cost is approximately zero with the Bank of Japan buying up Japanese Government Bonds by the bucket load.

Raf Manji, a strategy and risk consultant and former Christchurch City Councillor, told me in May of his experiences trading the yen and Japanese government bonds (JGBs) in a previous life. Holding a short position in JGBs led to a big losing trade for him. The Japanese were "printing money like crazy" and Manji expected JGBs to go down when they just kept going up. Manji was one of many traders who lost by betting against Japanese sovereign debt in what became known as the widow maker trade.

With little inflation or growth, Manji describes Japan as a highly advanced but post-consumer society. This may not be an ideal scenario, but nor is it a worst case one.

Someone else I've interviewed this year is the Hong Kong-based Macquarie strategist and author Viktor Shvets. He argues that technological disruption and financialization started creating a new world in the 1970s, and the COVID-19 pandemic is a dislocation that's accelerating change. The financialization began when US President Richard Nixon ended the post-World War Two collective international currency exchange regime, or Bretton Woods Agreement, in 1971. This had seen other currencies pegged to the US dollar, which was itself pegged to the price of gold. Shvets argues Nixon's move ushered in an era of leverage and strong asset price inflation.

In this world the role of capital and labour are different to how they're traditionally viewed in capitalism. Rather than being scarce and allocated carefully, capital is now abundant. In fact in a world of QE we're drowning in it, Shvets says, although it's not evenly or fairly distributed. And as technology develops in this information age, led by artificial intelligence, human labour is becoming less relevant.

Thus generating more capital than we need is required to support asset prices, which have become the backbone of the economy. And as we generate more capital than we need, the cost of capital, or the cost of a company's funding, falls to zero. The lower the cost of capital gets, the faster technology proliferates, Shvets argues, because with the cost of capital so cheap, almost any idea can be funded.

Probability that #Automation will lead to job losses in next decade or two. pic.twitter.com/Ii9coIlns2

— HumanVSMachine (@HumanVsMachine) September 20, 2020

An inflation comeback?

The Shvets thesis is that capitalism as we know it is irreparably broken and will be replaced by something else in coming years. But of course there are other views.

There are pundits who believe the scale of the global monetary and fiscal stimulus being splashed around to combat COVID-19 could lead to rising inflation after three decades of deflation. Such a situation could see a sharp spike in interest rates. Chetan Ahya, Morgan Stanley's chief economist and global head of economics, is one of them. Ahya argues the monetary and fiscal policy easing underway around the world is essential to get out of the low-growth, low-inflation loop of recent years, and will disrupt the three key deflationary forces of the past three decades, being technology advances, trade rules and corporate titans.

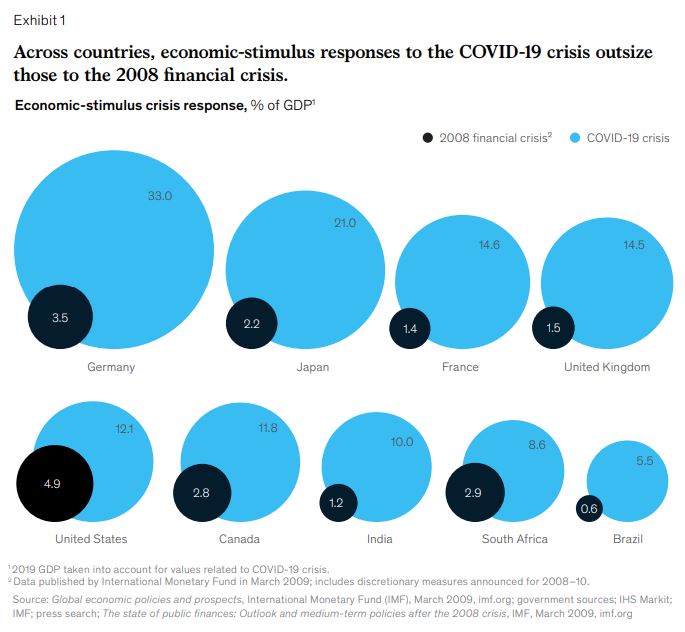

Ahya says inflation may emerges from 2022 onwards, and overshoot central banks’ targets. Bernstein analysts also suggest the public policy response to the COVID-19 pandemic will be inflationary because of its scale, the social impact of the pandemic highlighted by high unemployment, and government debt among OECD countries in line with levels reached at the end of World War Two. The diagram below from McKinsey and Company shows the scale of COVID-related economic stimulus from several countries. Note, this dates from June.

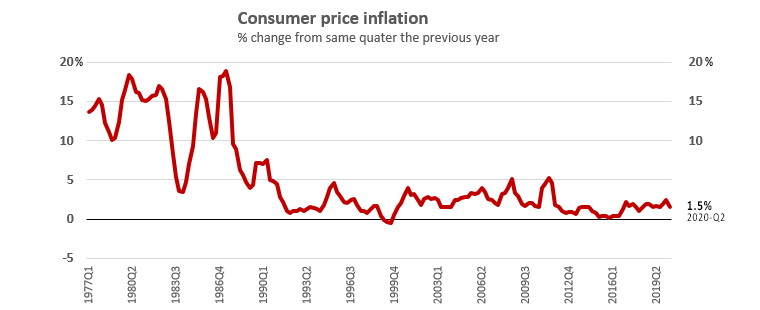

But right now central banks are worried about deflation, not inflation. In its August Monetary Policy Statement the Reserve Bank forecast consumer price inflation of just 0.4% next year, 0.8% in 2022 and 1.5% in 2023. If the inflation ogre does re-emerge surely we will know what to do, we can draw on our experience of the past 30 plus years.

In the meantime NZ government bonds were recently issued with a negative yield for the first time. That means an investor receives less money when the bond matures than what they originally paid for the bond. And as I recently pointed out, despite NZ government bond issuance surging since COVID-19's emergence, the interest bill on the debt isn't following suit. In fact despite having borrowed almost four times as much money via bond issues this year to date as in all of 2018, the government's interest bill is $21 million lower.

In the tweet below Martin Whetton, head of fixed income and foreign exchange strategy at ASB's parent Commonwealth Bank of Australia, points out a significant volume of the NZ government bond market is now in negative yield land.

A good chunk of the NZGB market is now in negative yielding territory. pic.twitter.com/pTCOLsSXW7

— Martin Whetton (@martin_whetton) September 21, 2020

Post-Muldoon Parliament passed the Public Finance Act in 1989. It sets out principles of responsible fiscal management.

Under the Act, the Government must reduce total debt to prudent levels. This is to provide a buffer against anything that might impact adversely on the level of total debt in the future by ensuring that, until those levels have been achieved, total operating expenses in each financial year are less than total operating revenues in the same financial year. Additionally once prudent levels of total debt have been achieved, they must be maintained by ensuring that, on average, over a reasonable period of time, total operating expenses don't exceed total operating revenues.

The Act also says when formulating fiscal strategy the Government should have regard to its likely impact on present and future generations. There is some wriggle room, however. The Government may depart from the principles of responsible fiscal management temporarily, if the Minister of Finance states the reasons for the departure from those principles, the approach the Government plans to take to return to those principles, and the period of time the Government expects to take to return to those principles.

At risk of being burnt at the stake as a heretic, in the world Shvets describes would the principles of responsible fiscal management in the Public Finance Act still be relevant?

Awash with debt

According to the Institute of International Finance, global debt to GDP reached a new record high in the first quarter of 2020 at US$258 trillion, or 331% of GDP.

If the inflation hawks are right and inflation makes a comeback with interest rates rising significantly in this debt sodden world, how many borrowers holding a slice of that US$258 trillion will simply not be able to continue servicing their debts, or pay back the principal borrowed? How many of NZ's home owners with mortgages would face severe financial stress, especially if unemployment was also high?

In this scenario is it against the realms of possibility that something will simply have to give? Could it be some sort of debt jubilee, or debt forgiveness, as proposed by Australian economist Steve Keen, or the Great Reset that US pundit John Mauldin talks about? Or will the days of fiat currencies come to an end, with a return to something like the Gold Standard, or perhaps something completely different?

I don't have the answers to that. But what I do know is that in a 2020 world I'm not going to lose any sleep over our government debt-to-GDP ratio whether it's 35%, 55% or 75%.

And that $12.1 billion that Robertson's keen not to spend? Couldn't we actually put some of it to good use?

At the onset of the COVID-19 health crisis NZ wasn't as well prepared as it could have been despite warnings stretching back at least as far as SARS in 2003 that a major global pandemic was on the cards. The Global Health Security Index, issued last November, ranked us 35th out of 195 countries with a score of 54 out of 100. In contrast Australia came in fourth with a score of 75.5. Writing at the time the University of Otago's Matt Boyd, Michael Baker and Nick Wilson said: "This poor result suggests that the NZ Government needs to act promptly to upgrade the country’s defences against pandemic threats."

What about building some proper quarantine facilities outside our cities so we're better prepared for the next pandemic? In normal times they could be used for the likes of school camps and conferences. Meanwhile, the Government is tipping $180 million into the Canterbury District Health Board basically to keep the lights on after a decade featuring earthquakes and a terrorist attack on the city's mosques. That's even though Treasury acknowledges underfunding is one reason for the DHB' s deficit. Wouldn't a bigger contribution help bolster core services?

Then there's education. An RNZ story last week highlighted Auckland's five year-old Ormiston Primary School, which is converting its boardroom, staff room, principal's office and library into classrooms as a school designed for 700 students sees its roll approach 1000.

Our politicians passed the Zero Carbon Act last year, with the support of all parties in Parliament except ACT. Under the Act, the Government must strive to meet the target of zero net carbon emissions by 2050, with the Climate Change Commission established to advise and monitor the Government. Climate Change Commissioner Rod Carr told me that electrification is a significant opportunity for NZ to reduce its emissions, as long as the electrification is powered by renewable energy sources.

Achieving this is a major undertaking, requiring significant investment in increasing renewable energy production, upgrading how we move energy from where it's produced to where it's used, and incentivising the uptake of electric vehicles. Carr also says we need a national energy plan for the next 30 years.

Then there's the tourism industry, hit by the loss of overseas tourists. In a report last December Simon Upton, Parliamentary Commissioner for the Environment, noted international visitor numbers were approaching four million and could rise as high as 13 million annually by 2050. The sheer numbers of people are eroding the sense of isolation, tranquillity and access to nature that many overseas tourists seek when visiting NZ, Upton added, questioning whether we were in danger of killing the goose that laid the golden egg. Thus surely now is the perfect time to work out a preferred post-COVID approach to tourism for NZ.

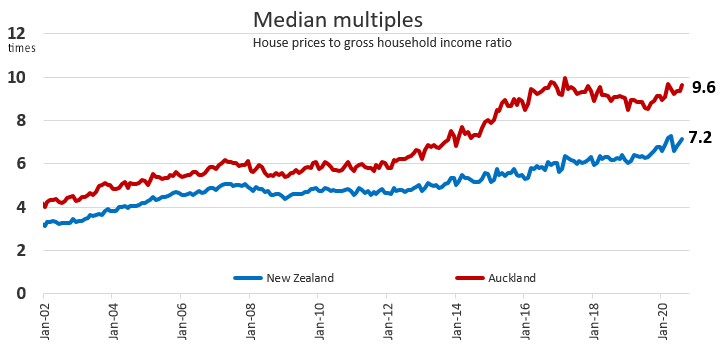

I am a parent. Leaving government debt for my kids and grandchildren is not something that worries me. There are many other issues I would prefer to see us focus on. These include what sort of housing is going to be affordable and available for them. Just look at the house price to income multiples in the chart below. Additionally will they be able to find fulfilling work, what state will the planet be in, what state will our infrastructure be in, how fractured along social media bubble lines and haves and have nots might society be, and what type of world leaders and regimes will be ruling the roost?

Muldoon's ghost as the marshmallow man

The original "Ghostbusters" film, about a group of ghost catchers in New York City, came out in 1984, the year of Muldoon's electoral Waterloo. There's a famous scene in the film where the heroes successfully battle a giant ghost marshmallow man. Muldoon's political demise ushered in a sea change, ultimately right across NZ society. But our understanding of government debt has not evolved. In NZ's fiscal version of "Ghostbusters," Muldoon is the marshmallow man. Now, 36 years after his political demise and against the backdrop of COVID-19, the time is again ripe for some major changes. Moving on from 1980s style thinking about government debt, and focusing on issues that really matter for New Zealand, would be a good start.

(This article is part of Interest.co.nz's Election Series).

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

102 Comments

I strive to talk to my bank about being in the 21st century as well, why can't they be an adult about my debt levels Vaughan ?

Why can't we bring them into the 21st century and me not have to pay back any money I borrow.....why Vaughan

I am in the same boat, I would be much better off if the bank would lend me 2m and all I had to do was pay the interest. I could make a lot more money, hire more staff and focus on the important issues instead of worrying about debt.

Well I thought this was a very informative article about keeping the country economy together. Comparisons with the rest of world shows we will survive and the future is not lost. It certainly was not about any one's individual economic situation. As individuals we all have to strive within our own parameters.

If you were a currency issuer and not just a currency user then your debt would not be a problem for you. if you wish to have money to save then only the government can create this money by running deficits. A government deficit must equal a private sector surplus. (Sectoral Balances). https://gimms.org.uk/fact-sheets/sectoral-balances/

Good theory I'm sure. Where does trade balance and balance of payments come in to it.

look at the link that I posted. NZ runs consistent current account deficits that must be funded by additional currency or the private sector will become even more indebted.

The logic behind Modern Monetary Theory is sound as a lens through which government fiat currency and its role can be viewed. To a large extent it simply describes money's role. But leftists invariably look to abuse this to justify vast government spending restrained only by inflation. Inflation will become a problem and we'll look like a banana republic. They also totally disregard the fact that government is not the best allocator of resources. For the time being I think government should continue to try balance its books with funding via debt (bonds with the banks as an intermediary) and tax.

I don't think you get it either DD, or you've over simplified too far. MMT simply changes a basic fundamental principle the we've been sold for too long that is simply wrong, and Gareth is trying to get people to understand and importantly, debate.

By recognising that a Government can issue all the money it needs changes a lot of things, and importantly significantly increases risk in some areas while solving issues in others. The risk of inflation is one of those risks which would lead us to become a third world country with a valueless currency. the solution to this is taxation.

With recognition that the Government can issue all the money it needs, then the rationale and vectors for taxation shift significantly. Until now, including the upcoming election, we have been and are being told that the Government must tax to raise the money to pay for it's policies, and the money it cannot get from taxation must be borrowed. And it is this borrowing that Gareth has written about. Is it really necessary? Under MMT the answer is NO.

Taxation is the means by which the Government manages the total amount of money that is in the economy, and therefore through this it's value against other currencies, as well as other things like the performance of parts of the economy as well as behaviours of business's and people. But even then it is not this simple.

We need to consider how we as a nation make our money. Do we produce anything of value, or is our focus on doing stuff for others - products/commodities v services. These aspects also impact the value of our currency. But there is more - how resilient are we? Are we overly reliant on others for what we consume as opposed being able to survive on our own if the world shuts down? These are all important parts of the debate that need to be understood and recognised. The majority of the economy would not change significantly for most people, but the rationales behind a lot of what happens does. Properly understood MMT does offer a solution, but as Venezuela shows, great opportunity for abuse too.

Disagree, MMT changes nothing

Its not a solution to anything

We can make as much DEBT as we like and we always could

the question as always is FAITH in your ability to service that debt ...

And for that you need some output (which is ultimately valued in the reserve currency of Debt = the petrodollar)

MMT doesn't change a "basic fundamental principle". It acknowledges the pre-existing principles of money and describes the lens through which it can be viewed accordingly. But when leftists get hold of it they extrapolate it into something it was never meant to be.

Government can't "issue all the money it needs" because this would be inflationary. Not only that, but Government expenditure very rarely represents most efficient allocation of capital, so free rein isn't a good idea. It is important to make a distinction between Treasury and RBNZ, instead of lumping both into "government".

Taxation is not the means by which the Government manages the total amount of money that is in the economy. This is a side effect, but the primary function of tax is a revenue stream for Treasury. Changes to RBNZ's balance sheet is a better way manage the total amount of money that is in the economy. Case in point, there is currently lots of new money being put into the system, but tax has remained the same, because more/less tax is not the primary tool used to get more/less money into the system.

What is 'the most efficient allocation of capital'? You seem to present as fact that government spending - whatever that means - is not efficient. If that is the case, then what is?

My understanding of the recent emergence of MMT as a point of discussion outside of academic circles is just that we need to stop fixating on debt as a zero-sum mechanism and more as a fluid allocation mechanism. I don't care if QE is inflationary if it produces real-world benefits. Equally, I don't care about debt if holding debt produces more wealth than it costs to service - if you can borrow at 2%, grow your economy at 5%, and introduce 1% in additional inflation, then it seems irresponsible not to borrow. As we issue debt in our own sovereign currency, the power to relieve or cancel debt, weighws against the inflationary pressure, is ours and ours alone.

OTOH, I don't want see debt or QE used without careful consideration of its negative consequences. My reading of this article is that in the political and popular realms, Gareth is arguing that the dialectic focuses on debt as a necessary evil without due consideration of the benefits. Whereas in economic and financial academia this perception is less so.

I think rushing to dismiss the entire concept in terms of 'left' and 'right' is reductive.

What pre-existing principles of money are your referring to that are in use under the current 'Tax and Borrowing then Spend' model? MMT essentially changes that to Spend, then tax.

And, at least theoretically, a Government that is the sovereign owner of it's own free floating currency can issue all the money it needs. However as i have indicated there are risks when it does that, that cannot be ignored without dire consequences. I have not ever suggested free reing for a Government, but that is about functioning democracy, not economic control.

Under MMT, if you recognise the principles of MMT (Sovereign owner and all that) then the rationale for tax does change, because a Government no longer has to tax to spend. It does so for other reasons.

Core pre-existing principles like government can’t go bankrupt or default due to debt denominated in its own fiat currency, and unemployment or idle productive capacity generally indicates there isn’t enough currency in the system, with the shortfall being an unnecessary impediment analogous to a runner with a plastic bag over their head. This is the core thinking of people like Warren Mosler.

But we don’t currently operate our monetary/fiscal system according to the approach that leftists like Stephanie Kelton advocate using MMT as justification. For example, the approach that government spending should be paid for by the creation of money with no regard for balancing its budget, with the purpose of taxes being to limit inflation instead of funding government. This clearly isn’t how we operate today - NZ government aims to balance its books and is funded by debt and tax.

Of the principles in the first two I agree, but for unemployment I don't. Existing economic models contain a concept of maximum employment level that essentially means that unemployment is an essential to an economy. There is no basis of fact to this, and it can be argued to be demonstrably wrong quite easily. Indeed the principle is based on a perspective of perpetual growth which as we know now is quite wrong as we live in a finite system. So in this area many of the early theorists are wrong, but it is easy to understand why. They lived in a world where the physical limits of our world from an economic perspective were not apparent as they are now.

I disagree and don't like your labelling of Kelton as a leftist. I think it marks you as someone who doesn't understand what she and the other economists with her are advocating, so you're falling back on name calling as a defence. Stephanie Kelton does not argue that the only purpose of taxation is to limit inflation, but it is a primary reason for taxation. When or if you read her book (and I have) you need to be able to see past the idiosyncratic Americanisms and find the basis of her perspective.

And you are right, the NZ Government doesn't currently operate that way, but that doesn't mean it can't. The current system has not served the people of NZ well, so it is time for a change and MMT offers an opportunity for that.

Kelton is a leftist. This is a fact, not “name calling”. It isn’t a coincidence that she was Bernie Sanders's economic adviser.

You sound like someone that doesn’t really understand MMT but is persuaded by the too good to be true promises that some people on the left have bastardised it to support.

Guilt by political predilection?

Spare us the comment, perhaps.

This nothing to do with left or right - this is about the growth-requiring system hitting the wall, and a section who can see this coming (which is never conservative thinkers - those who don't think fast/change) but who don't want to address the issues. So they've cooked up a formula, but it is the same as the old one - fails to address real depletion.

As i said, when you resort to name calling it is more about you than the person you are deriding. Kelton is not a 'leftist' she was advising Sanders because she was presenting a different perspective and approach to managing the economy that changed some fundamental rationales around why things are done.

MMT in some respects offers more for the right than the left. Your view of unlimited money is what the right wants for their own purses. But as i have stated, while it looks like unlimited money, it is not without cost, so cannot be treated as such. For MMT to be effective a strongly functioning democracy must be in place where the Government is fully accountable to the people. Here in NZ the electoral term has again surfaced during the current campaigning, but nowhere in the debate is there any mention that increasing the term undermines democracy unless there is some additional means to ensure the Government is accountable to the people. A big part of the current mess is due to Governments not really being accountable to the people.

MMT does mean that the Government's source of funding for it's policies is not sourced from taxes and borrowing, but it also means that the rationales for taxes change as well. If the Government does not need to tax to raise money, it does need to tax to control the value of the dollar and inflation, manage corporate and individual behaviour, support employment, grow industry and resilience, preserve the environment and so on. In the current system we have been, and continue to be sold a myth that can be proven to be not true. This myth has been damaging to most of the population and is used to preserve and protect power and privilege.

An example. During the Clark/Labour Government they delivered multi-billion$ surpluses. Indeed I well remember one occasion when Michael Cullen was asked about the possibility tax cuts which would cost about $1.5 billion, when the Government was trumpeting a $12 - $13 billion surplus. MCs retort was that if people wanted a tax cut then the budgets for Health and Education would need to be cut. So they were protecting their own interests at the cost of the people, while they could have still fully funded those areas. This position also shows some flaws in Kelton's perspective. Over their tenure that Labour Government report $billions in surpluses over a number of years, but Kelton suggests that to do so that would have significantly impacted inflation and the value of the dollar. I don't think either happened. But during that time the economy did start to spiral into the mess it is now.

No there are other factors that drive the value of the dollar as well, and they may be stronger, but the Government, any Government must understand these and be prepared to manage them.

National Party leader Judith Collins says "we cannot continue to have this line of economic morphine in our bloodstreams anymore."

So what's the plan you ask?

National has just announced a plan to create at least 10k new jobs a month with a 'cash-for-jobs' scheme, among other things.

· Supporting businesses with $10,000 to hire new staff and provide modern, flexible working practices

· Encourage high skilled migrants including surgeons, rocket-engineers and scientist to choose a life in New Zealand to help grow the economy and create more jobs.

http://business.scoop.co.nz/2020/10/06/national-focused-on-creating-at-…

National continues down the road of denial its loss of centre-right votes to a minor party has now come down to bribing cafes to hire baristas and citing the term "rocket-engineers" in grown-up conversations.

Instead of the economic morphine of borrowing, National is offering a short term sugar hit.

I could live with more debt if we had something to show for it. Yet we're about to re-elect a government that has achieved very little and abandoned almost all of its key election platforms that saw it be in a position to form a government in the first place without any real consequence. There's considerable irony in raising the specter of Muldoon to defend this particular Labour government, which promised lashings of state intervention but was too incompetent to deliver, and would be facing a tough election justifying having achieved practically nothing were it not for Covid. Think Big? More like Think Kind - and about as effective.

Well JA paid someone in NY $50k with the Covid money to "think about art" through $16M art grants.

Surely thats value for money and a high achievement.

Policy for the real challenges is already here...

There are better ways to waste your vote than on these illogical Marxists

The only wasted vote is for Labour or National who wasted every bit of political capital on nothing...

If everyone that would’ve voted for TOP stayed in bed instead, the election result in terms of parliamentary seats will be exactly the same. TOP votes are discarded for all intents and purposes.

2017 votes increased electoral funding for this election...

You've just added wasted taxpayer money to the list

If you’re completely satisfied with the status quo I have nothing to offer you unfortunately

I’m not satisfied with the status quo, which is why I won’t be wasting my vote. Speaking of wasted, the leader of TOP is a self-confessed regular and ongoing user of illegal drugs.

You sound pretty determined to keep the status quo (asset speculation anyone), you wouldn't be lying to us about your voting intent would you?

Also, what drugs has Geoff used and why is it relevant to the discussion? Or are you trying to stir up some 1950 style moral panic to appeal to other dinosaurs? I hope it's not 'reefer' he's using, I've heard if you have one toke you'll turn in to a Mexican and then go crazy and murder all of your neighbours!

The drug of choice aside, don't you think one's willingness to routinely break the law is a reflection of moral character?

That said, I raise the issue because it appears most of Geoff's policy proposals were conjured up while high as a kite. LeT'S TaX ASsEts BaSED oN THe iMagIONary INcome They ARe eArniNG!!??

The law is not a moral code, its a legal one

Yes, but I don't break the speed limit even if I know I can travel safely while exceeding it. And I pay the amount of tax I am legally obligated to even though I think the rate should be lower.

Wouldn't it be nice if everyone towed the official line just like you do, what an obedient citizen. So what are you doing mixing with all of the 'radicals' here!?

Oh, you're here to defend the status quo.

Yes, it would be nice if everyone obeyed the law. I get the impression you’re a delinquent. Seems like this may be a common theme among the TOP folks.

Lol. Well, I have toked a 'reefer' once or twice in my life so I guess I'm basically a terrorist in your eyes!

I’ll be voting yes in the referendum. Won’t however be voting for the party lead by a habitual user of illegal drugs with a tenuous grasp on reality. But you go ahead and waste your vote.

I look forward to seeing your precious vote make a tangible difference to the election outcome. It isn't often a party wins by one vote. If that doesn't happen you might as well have stayed in bed, your voting was a waste of time as it changed nothing.

Seriously though pushing the 'wasted vote' theory is stupid and anti-democratic in my opinion.

You’re not making any sense. A vote for any party that achieves the 5% threshold or wins an electorate seat isn’t wasted because that vote is counted towards their parliamentary seats. If neither of these criteria are met, your vote is discarded for all intents and purposes. What part don’t you understand?

I disagree with the concept of a wasted vote. We all have a vote. Each one is counted and there is a system for apportioning power based on the count. Each vote by itself doesnt change anything. The idea of a wasted vote to me is simply trying to scare people into voting for the status quo. Your vote by itself doesn't really matter, why not use it how you really want to rather than worrying about how it might be used once the votes are all tallied up? If everyone thought like that we would get a more representative democracy. Instead of everyone voting for the major party they hate the least. Banning polls close to elections would help.

Not necessarily, especially when a law isn't based on actual evidence of risk / harm.

Regarding point two, is their policy any worse than the current policy of taxing productive workers and/or the savings of these people? Shouldn't we want to lessen the tax burden on those doing the productive work?

I don’t break the speed limit even if I know I can do it safely. Anyone that does is not cool. If everyone broke laws that they disagree with the country would be a mess.

There is no tax policy more unjust than to tax income that doesn’t exist (like TOP’s asset tax proposal). A flat poll tax is far more efficient than any other tax and doesn’t punish human labour at all, but it is very much immoral. Why don’t you people advocate that - probably because it doesn’t satisfy your illogical contempt for landowners and property investors.

Really, you never break the speed limit?

Not intentionally. Do you?

Nor do I run red lights even if I know I can do so without causing a crash.

Sometimes, on the open road, to pass someone I might go to 110 kph. Obviously in the right circumstances.

You never do that? I congratulate you for your 100% law abiding nature.

Again, not purposefully or internationally - no doubt it happens on occasion whether I’m passing or not. What Geoff is doing is much more purposeful and pre-meditated illegal activity. The guy has a drug dealer. He participates covert illegal transactions. Not the sort of character that should be in parliament. Knowing how illogical TOP’s policies are, it came as no surprise to me when Geoff came out as a stoner.

Interesting how you twist things...going above 100 kph to pass someone is clearly intentional, you know exactly what you are doing...

I am not satisfied by the status quo, which is why I will be voting for the status quo.

Hmmm... does not compute. Maybe voting for the Advance NZ party? Oh no, I think it was ACT DD was going to vote for, because they are able to sometimes get a members bill in and can sometimes shout across the floor at people. In reality they are just the right hand side of National, so a vote for ACT is a vote for National policy, i.e. the status quo.

With all the free money, why doesn’t the government purchase 100ha+ in every town & city and build houses just like the 1950s?

Much of NZ infrastructure was built in the post WW2 era and during the Muldoon era with hydro schemes etc. Time to Think Big.

Instead of frittering away all the helicopter money on subsidies & RDFs etc

why doesn’t the government purchase 100ha+ in every town & city and build houses

That's exactly what the Urban Development Act 2020 intends to do i.e. provide powers to the HUD ministry and Kainga Ora to cut through the bureaucracy of 10 different acts so as to ramp up social and market housing supply quickly and on a larger scale.

https://www.hud.govt.nz/urban-development/urban-development-act/

That's exactly what the Urban Development Act 2020 intends to do ....

What you explained sounds like something from a Franz Kafka novel or from the public sector in Japan post-bubble. Nightmarish.

There is no winning against the DGMs in these comment sections with their poetic analogies.

Scroll above to see how commentators have managed to criticise both the government's inaction and its excessive action in the same reply thread!

I reckon we all are policy champs until the time we enter public office or the polling booth.

"With all the free money, why doesn’t the government....." And that is the problem with people who can't think. MMT does not produce 'free money'. Issuing money by a government comes at significant cost, and if that is not recognised and addressed, the consequences are dire for the country.

You're arguing against ideology. People have been indoctrinated that the current system is the only one possible. I personally don't think MMT will solve all of the wider issues but our current system certainly won't and I respect that you're trying to progress this conversation.

You're arguing against ideology.

No. MMT is a new kid on the block. Most of the ruling elite and people on the street think that MMT is nuts. Most people believe in balanced public accounts as the be all and end all. It makes instinctive sense to them.

MMT IS nuts.

The problem is the amount of planet left, and MMT doesn't measure that any better than OMT.

The were/are both a collection of bets on a dwindling-chip table.

Rogernomics in the 80s destroyed NZs ability or desire for public spending on infrastructure or public good projects. Everything became a private good and individual private cost.

Even this past week see the discussion on charging power users based on their distance from generation.

Look at the shonky fibre optic installations into homes - poor workmanship that the Post Office technicians of the 60/70s would be shocked at. Now it’s impossible to build new hydro power sites, Govt housing, nation-wide anything, just piece-meal shonky privately funded sub-projects.

.. and that is exactly was the neo-liberalism capitalism of Roger and ACT did, detroyed the very fabric of kiwi society, the individual over the collective good

Rogernomics in the 80s destroyed NZs ability or desire for public spending on infrastructure or public good projects. Everything became a private good and individual private cost.

A basic constraint in MMT is the level of available resources. That should factor in planetary limits. Much of what I read about MMT does not recognise the importance of this.

So, all forms of Taxation are going to be abandoned. The Cash-Job society brought out into the open and run by The Central Banks..

" Manji describes Japan as a .... post-consumer society." Quite right. And Post-Consumer Societies; ones that most Western countries are set on becoming - including us, won't levy tax. Neither will they Consume, as we are currently conditioned to.

What's the purpose of tax if Inflation isn't a problem and isn't coming back? (It isn't, regardless)

Tax has been An Option for some, forever; many for 40 years or less, and now it will become a relic of the past for all.

The government doesn't need to raise revenue to run the country. It just maneuvers funds around on several spreadsheets.

We will all be paid in what was net-of-tax terms; Cash if you like; (and nominally lower?) and the rest will be done for us. Easy.

The only drawback? Those who benefit from tax-avoidance; be it Cayman Island stuff or plain ol' Negative Gearing, are going to squeal when their special rights to enhance their net income, disappear!. No tax? No lurks....

" Manji describes Japan as a .... post-consumer society." Quite right. And Post-Consumer Societies; ones that most Western countries are set on becoming - including us, won't levy tax.

What is a 'post-consumer society'? Consumerism is very much at the heart of modern Japanese culture (but not nearly as rampant as Westerners think). Furthermore, tax is still very much part of Japanese individual's / h'holds' lives. Manji needs to rethink his descriptors.

I've taken issue with some of Manji's writings before; so agree with your comment.

And the thrust of my post is "What's the point of taxation if money/liquidity can just be conjured up at the stroke of a key?"

None!

Tax is to keep the mass of the population compliant; make them feel that they are 'doing their bit' and paying for the necessities of any society. It's always been that way (Think the 10% Tithe that applied in pre-Christian times etc). But as the past chairman of a tax committee, where the first point on the agenda each year used to be "Ok, chaps! How much tax should we pay this year?" It was 'just enough to keep the tax authorities 'happy', and we figured 10% over the rate of inflation in any given year ought to do the trick; it did!

So tax; tax avoidance; tax evasion etc all disappear with the scrapping of taxation.

If we can run The System and keep it alive without the need to ask for a contribution from every soul, I reckon that what's coming next.

Negative Interest rates were an unthinkable thought 10 years ago. So is 'Scrapping Tax', today.

Tax is to keep the mass of the population compliant; make them feel that they are 'doing their bit' and paying for the necessities of any society.

OK. I think there is an idea that NZ can do what Japan has done. Japan easily has the best infrastructure in the world in my opinion. I'm skeptical NZ can simply do what Japan has done for 2 reasons: 1. Japan is a creditor nation; and 2. The scale of industrial output is on a completely different scale in Japan's economic profile.

Does your assertion that all forms of taxation are going to be abandoned include taxing bads? using income and capital/wealth taxes for reducing inequality?

Or is it just a throw away statement?

Great piece, thanks, a lot to digest. The debt may be ok (especially if directed towards future productive value not just more 80's think big eg Tiwai bail out which seems to be most of the 80's style thinking from all parties without applying much critical/imaginative thinking for today's environment), but as you say as a parent & what leaving them re: house price from 3-4x to 10x income, isn't the form taken (QE, near zero interest rate) and its impact (inflating share & house asset bubbles, increasing wealth inequality, whilst seemingly not having intended effect that it is 'supposed to have' (and used to have at higher rates, likely why the bureaucrats advised it would work at low rates too, and are stuck trying to defend even when clearly its not, now entering magical thinking phase) - instead causing more saving, companies and households cutting debt, not investing, & not spending, all very logical even if not foreseen & now maybe driving into a decade of stagflation (perhaps after a quick burst of deflation) and/or bursting of the now massively inflated bubble & it's more widespread harm - cause you concern Gareth?

That (presumably) is why even Fed (which led the QE & we all followed like economic sheep) is investigating sending digital money direct to households rather than the QE bond buying via banks (which they now see just inflated bubbles, expanded wealth inequality, & didn't have intended consumption/inflationary impact) to actually reach ordinary people and spark consumption.

New Zealand has low levels of public debt but the net results has been very high levels of private debt (driven in large part by the constraints on realestate development), infrastructure development falling far behind comparable OECD countries, productivity stagnation and growing wealth inequality.

Overall I would describe this as a right pickle.

Yes. NZ (and Aussie) h'holds have among the highest h'hold debt to GDP in the world. H'holds are the mules. The debt load has been contracted out to the private sector in the form of a housing bubble.

You see Akl prices are ratioed to HOUSEHOLD income = 9 so per individual income approx = 18. Beautiful numbers.

Most households don't have people earning equal amounts.

It seems to me that our indebted households have been forced to lever up so as to maintain high living standards despite a sustained drop in productive employment and wages back in the 90s when we began offshoring higher value-add activities such as manufacturing.

Countries that held on to manufacturing (Austria and Germany) seem to have relatively lower levels of household debt to GDP.

https://www.imf.org/external/datamapper/HH_LS@GDD/NZL/DEU/AUT/CAN/AUS

Most would look at Germany and Austria with a degree of envy in what they have achieved over the last three decades. I suppose what you are seeing is an increasing divergence between the industrious and highly productive economies and, um, ...the rest of us.

It takes the some of us 6 years discussing "acute" skill shortages and special visas in industries critical to socioeconomic wellbeing and are pushed into action by a virus-induced border closure in reintroducing a subsidised trades apprenticeship programme.

I did my apprenticeship in 2001 and we were crying about a skills shortage then. Almost 2 decades later, soaring youth unemployment, and the polys are stumbling around blindly. Sigh.

It seems to me that our indebted households have been forced to lever up so as to maintain high living standards despite a sustained drop in productive employment and wages back in the 90s when we began offshoring higher value-add activities such as manufacturing.

Housing bubbles are easy on the way up (and a no-brainer for the self-absorbed members of the ruling elite). They can become a nightmare to untangle on the way down. Personally I think NZ is woefully under-prepared. The concept of a rainy day didn't exist until Covid hit.

Overall I would describe this as a right pickle.

That's very generously described ;-)

It's all fun and games until the Pied Piper turns up

Recently I've been reminded of both Muldoon and the Time Warp song by NZ politicians' attitudes towards government debt during our election campaign. Because it feels to me as if their attitude towards government debt continues to be framed by a 1980s mindset, and that the ghost of Muldoon still looms large in their thinking. Relitigating the 1980s is not the right approach in 2020 because today we live in a very different, rapidly changing world.

Indeed: A high level of liquidity preference, the low level even lack of economic growth to provide opportunity causes investors to seek refuge in what they consider to be safe liquid assets. The consequential rise in sovereign bond prices reduces term interest rates, which in turn increases the discounted present value of cash flows associated with all assets and liabilities, but not much else.

This is what Milton Friedman called the interest rate fallacy, and it indeed refuses to die. We can tell what monetary conditions are in the real economy, as opposed to financial liquidity, though the two can be linked, by the general level of interest rates. When money is plentiful, interest rates will be high not low; and when money is restricted, interest rates will be low not high. The reason is as Wicksell described more than a century ago:

"[The natural rate] is never high or low in itself, but only in relation to the profit which people can make with the money in their hands, and this, of course, varies. In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low.

When nominal profits are expected to be robust, holders of money must be compensated for lending it out by higher interest rates. Thus, the same holds for inflationary circumstances, where nominal profits follow the rate of consumer prices. During the Great Inflation, interest rates weren’t low at all, they were through the roof well into double digits and higher by 1980. At the opposite end in the Great Depression, interest rates were low and stayed there because, as Wicksell wrote, the rate of profit was low and was expected to be low well into the future. High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar.

Friedman pointed out the basic, non-trivial distinction between a liquidity effect and an income effect. Low rates can be stimulative in the short run (the liquidity effect), but over the long run their persistence means something far different. A yield curve is supposed to be upward sloping given the core time value of money and investing. That arises from opportunity cost, meaning the more plentiful the opportunities the greater the time value and the steeper the curve (the income effect). Yield and/or money curves (the eurodollar curve and even the history of the OIS curve) that collapse and remain that way unambiguously demonstrate that "stimulus" deserves only the quotation marks.

The more only the government can borrow, the more only the government does borrow. And the more the government does borrow, the harder it is to get the economy growing The more difficult it is for meaningful growth, the more banks will only lend to the government. courtesy of Alhambra Investments

It is never about the debt, it is about the spending. The problem with Muldoon wasn't the debt, it was the abysmal quality of the spending on mostly a junk grade petrochemical industry. In the 1970s/80s the idiot in charge was politically committed to keep saving us from the oil crisis, even after the world had moved on and the oil crisis resolved.

So here we are in the 2020s, trying to isolate the country from the rest of the world to prevent the spread of COVID19. This isolation plan was formulated in March on the best info available at the time, but now we are in October and have subsequently found the disease to be much less lethal than originally feared. Our policy will not change to reflect the new understanding of the disease.

Our policy will not change to reflect the new understanding of the disease.

Except it already has. Jacinda has said she won't consider a travel bubble with Australia until they have 28 days without community transmission. Similarly it looks like there is going to be a bubble with Rarotonga by the end of the year.

Both these are distinct changes in stance from her, as previously she'd never given any concrete criteria by which bubbles would be opened.

Likely this is due to an increasing confidence in our border, quarantine, testing and tracing capacity. The entire point of standing these systems up -and then continuing to improve them - is that it allows you to then do things that were previously judged as being too risky.

How does the Reserve Bank exit its bond holdings? As a bond comes to maturity, for example a November 2020 bond issued 10 years ago, the Reserve Bank gets its money back from the Government in November and its holding decreases by the amount of the bond.

Which begs the question how do banks extinguish the deposits they create when they initially monetise government IOUs, other than the RBNZ passing the government bond redemption proceeds to them to do so?

Audaxes,

If the Govt repays the money thru its accts with Private Banking system ( westpac ), then the reserve Bank would simply take the money from Westpacs' reserve acct with the RBNZ ( payment settlement system ). Reserve Banks asset/liability would diminish by the equal amounts.

I'm guessing that Govt would repay the Loan by either reborrowing or from Tax income. In both Cases it is inside money ( credit money.)

Does that make sense..?? I'm thinking it thru as I type.

The LSAP/QE counterparty banks are many and varied.

Government borrows inside money and repays inside money - not outside RBNZ created bank reserves. Bond redemption liquidation costs are financed by prior syndicated issuance and reopening tenders.The government claims it has reserved around $14.00 billion over borrowing to accommodate unforeseen covid-19 liabilities, but there is an $11.309bn May 2021 issue in need of liquidation proceeds.

you can't escape the fact that govt spending sucks up resources for their pet projects...and not projects that the market requests.

A bureaucrat or politician driven choice...verse market demand. Malinvestments galore. Limited resources wasted.

I wonder if the solution here could be introducing a direct democratic process. I am thinking along the lines of eligible voters being able to raise and sign petitions publicly.

Under Swiss law, once a petition receives a certain number of signatures, the relevant ministry drafts up a policy initiative, and the independent electoral body holds a referendum on it.

That's one way to push meaningful reforms in areas where our major parties would dare not go (migration, tax on speculative investments, etc.) although the last 3 Swiss referendums attracted less than 42% voter participation.

And therein lies one of the problems with MMT. While Governments already direct funds towards their pet projects/policy objectives, under MMT with proper understanding of being a currency issuer the pollies could run amok if not constrained. The only real solution for this that I can see is by having a properly functional democracy, where the Government are accountable to the people, not just at the electoral term, but all the time. The pollies hate this and would not agree to it.

Australia : Is government helping FHB or in guise of helping FHB keeping the ponzi alive :

Yes lets talk less about important topics and more about housing please.

I'm all for a reasonable amount of fiscal support, but make it to people and their businesses, not to corporate and government bureaucracy. Capital is desperately hard to come by if you are a person, or a small or medium sized business, because you have to actually earn it.

The current finance, taxation and regulatory system is socio-pathic. It channels resources to where they are least needed, to large bureaucracies. It erects endless obstacles for all others.