By Gareth Vaughan

The Reserve Bank (RBNZ) has once again raised the old chestnut of having a tool to restrict high debt-to-income ratio mortgage lending included in its macro-prudential toolkit.

The latest request of the Government, whose acquiescence is required, comes in the RBNZ's response to Finance Minister Grant Robertson, released on Friday, over his concerns about soaring house prices.

"We have also previously consulted on introducing debt serviceability restrictions, such as debt-to-income (DTI) limits, on mortgage lending. Although we consider that restrictions on high-DTI lending could complement the current LVR [loan-to-value ratio] policy, we note that this tool is not currently part of the Reserve Bank’s Memorandum of Understanding with the Minister of Finance. We request that the Government gives consideration to adding restrictions on debt serviceability (that would include DTI limits) to the permitted tools in 2021," the RBNZ said.

That Memorandum of Understanding (MoU), signed by Finance Minister Bill English and RBNZ Governor Graeme Wheeler in 2013, includes four so-called macro-prudential tools the RBNZ can use to dampen excessive growth in credit and asset prices and strengthen the financial system. LVR restrictions, removed this year after being in use since 2013 but now on their way back, are among these tools. DTI ratio limits are not. The RBNZ has regretted not having a DTI tool in the MoU since at least 2016, when it formally asked English for such a tool.

Steven Joyce, English's successor as Finance Minister, parked the idea in the 2017 election year by telling the RBNZ to conduct a full cost-benefit analysis on DTI ratio restrictions and consult publicly before he would consider giving the RBNZ access to such a tool. Opposition politicians Grant Robertson and Jacinda Ardern were also unenthusiastic about a DTI tool in 2017, but more on this later.

Despite being knocked back in 2017, the RBNZ's desire for a DTI tool has never gone away.

Current Governor Adrian Orr reiterated this desire soon after taking the helm in 2018. And last year a RBNZ paper said: "The Reserve Bank’s view is that a serviceability restriction, eg, a debt-to-income threshold limit for borrowers, at which banks can only make a certain percentage of new lending, would be a useful addition."

Robertson and Ardern's opposition in opposition

But to get its treasured DTI tool the RBNZ will need the backing of Robertson, its current political master. And this is not certain with politicians reluctant to prevent first home buyers from loading up on debt so they can get into the housing market.

In 2017, as opposition finance spokesman, Robertson issued a press release saying, “Labour does not support debt to income ratios for first home buyers."

"The introduction of across the board debt to income ratios for home lending would punish first home buyers struggling to get into the housing market," said Robertson. "Thousands of young New Zealanders would be shut out of the security of home ownership."

And in 2017 Ardern said of DTI ratio restrictions: "We’ve never favoured them."

The RBNZ cost-benefit work requested by Joyce wouldn't have eased Robertson and Ardern's political concerns. It concluded that restricting the DTI ratio of some mortgage borrowers could prevent about 10,000 borrowers from buying a house, reduce house sales volumes by about 9%, trim house prices and credit growth by up to 5%, and shave 0.1%, or $260 million, off Gross Domestic Product.

On Friday Robertson would only say: “I thank the Governor for his response and will consider it, along with the advice I have requested from the Treasury. The Government will make announcements in the New Year.”

What is a DTI ratio tool?

So just what is a DTI ratio tool, and when might one be used?

As the RBNZ puts it, borrowers with elevated DTI ratios may be vulnerable if their income falls or interest rates rise, potentially presenting a risk to the banking system and the wider economy.

"A macro-prudential DTI policy would enable the Reserve Bank to limit the degree to which banks can reduce mortgage lending standards during periods of rising housing market risks, in order to protect financial system soundness. This may be desirable in some periods as (i) banks are not incentivised to adequately take account of the impact their lending can have on the overall financial system and (ii) the economy can suffer if too many borrowers take on more debt than they are able to service," the RBNZ said.

"DTI policies can support financial stability by reducing the scale of mortgage defaults during a severe economic downturn. All else equal, borrowers with higher DTI ratios have less disposable income to draw on as a buffer to avoid defaulting on their mortgage, without selling their home, in a period of lost income or higher mortgage rates. Loan serviceability is a crucial determinant of probability of default, reflecting that many borrowers will attempt to service loans even if they are in a position of negative equity."

"An important feature of a DTI policy is that the borrowing capacity of constrained borrowers grows in line with their incomes," the RBNZ said.

What's a high DTI ratio?

So just what constitutes a high DTI ratio? Back in 2017 the then RBNZ Deputy Governor Grant Spencer described a DTI ratio above five as "pretty high."

"We think if we get up over five that's pretty high. And it tends to be the area where potential stresses are going to emerge if there's a shock to interest rates or incomes," Spencer said in 2017.

Around the same time bank executives told KPMG's annual Financial Institutions Performance Survey an ideal DTI restriction set by any Reserve Bank DTI tool should be between five and seven. Albeit they added most borrowers were at levels of nine to 12 at that stage.

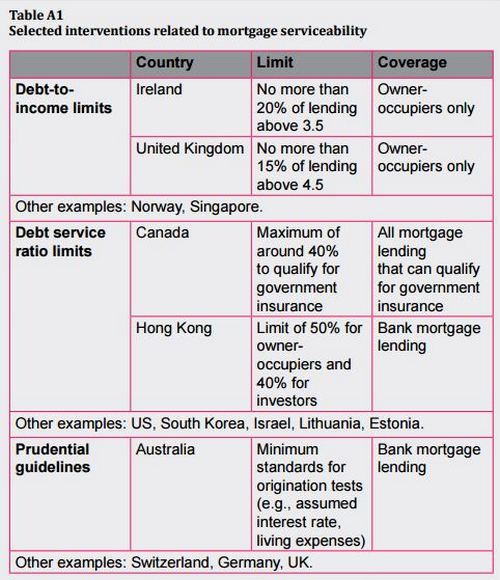

In terms of overseas use of DTI ratio restrictions, the RBNZ included the table below in its November 2016 Financial Stability Report. The Bank of England's DTI ratio of 4.5 featuring in the table applies to no more than 15% of the total number of a bank's new mortgage loans for owner-occupiers. And for Irish banks the DTI limit of 3.5 isn't to be exceeded by more than 20% of the value of housing loans for owner-occupier homes during an annual period.

'Banks willing to grant higher DTI loans to comparable borrowers than in 2018'

In last month's Financial Stability Report the RBNZ said it had recently completed a hypothetical mortgage borrower survey of mortgage lending banks.

"Results suggested that banks are willing to grant higher DTI loans to comparable borrowers than in 2018, with the average DTI for the stylised owner-occupier borrowers increasing from 4.8 to 5.3. Despite this, average debt servicing as a share of the borrowers’ incomes has fallen on average, from 39% to 35%, reflecting the decline in mortgage lending rates over the past two years," the RBNZ said.

"A lower debt-servicing ratio implies borrowers would have a higher capacity to absorb declines in income or increases in expenses, after making their loan repayments."

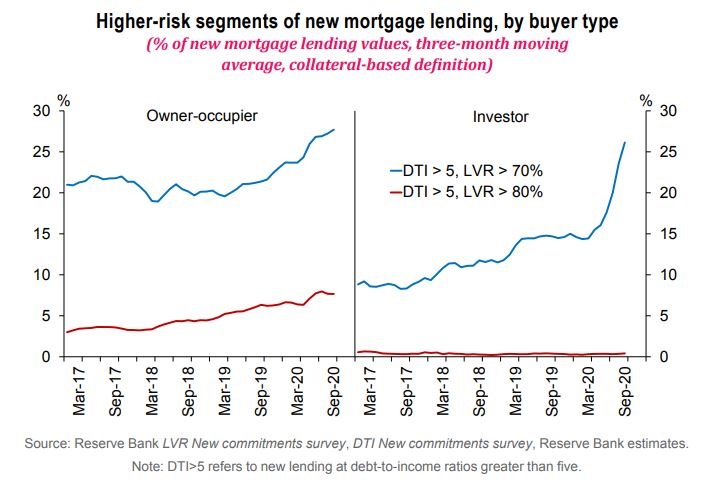

The charts below, also from the latest RBNZ Financial Stability Report, show a recent spike in new lending to investors at DTI ratios greater than five. This, of course, coincides with the RBNZ's removal of LVR restrictions on high mortgage lending in April.

What about just targeting property investors?

In terms of the RBNZ request of Robertson, he may agree to a DTI tool being added to the regulator's macro-prudential toolkit. And he may not. If he does, there's no cast iron certainty of exactly when the RBNZ would use it, whether it would be used alongside LVR restrictions, or whether it would apply to all or just some of first home buyers, other owner-occupiers, and residential property investors.

Given Robertson's publicly stated opposition to applying the tool to first home buyers, could DTI restrictions be applied only to property investors?

In the 2017 consultation the RBNZ did float the idea of a DTI ratio tool that distinguished between housing investors and owner-occupiers, or debt serviceability limits that focus on owner-occupiers and investors separately.

"Based on the feedback received, the Reserve Bank will consider alternatives to the hypothetical calibration example provided in the consultation paper if a serviceability limit is used in the future. These alternatives could include a DTI limit that distinguishes more between investors and owner-occupiers, or serviceability limits that focus on owner-occupiers and investors separately," the RBNZ said in 2017.

Incidently that hypothetical calibration example described the possible use of a DTI tool in a scenario where it was assumed house prices would rise nationwide by about 15% in 2018, with interest rates static and the share of mortgages originated at high DTIs staying the same. This, the RBNZ said, would mean house prices rising even further relative to income, having already reached overstretched levels.

Interestingly Friday's Real Estate Institute of New Zealand figures showed the national median house sale price up 19% in the year to November.

In its 2017 consultation response the RBNZ acknowledged banks make serviceability assessments and allow for the risk of rising interest rates. However, it said individual bank lending decisions don't necessarily take account of their impact on systemic risk during periods of intense competition for mortgage loans, nor that there can be a role for limits on banks’ serviceability practices during these periods.

"The Reserve Bank accepts that DTI is not a perfect indicator of risk. The attraction of DTI is that it is easy to compute and understand, and should be fairly well correlated with affordability. However, the Reserve Bank agrees that if serviceability restrictions were added to the MoU, this should be written in a more general way that would also allow a DSR [debt service ratio restriction] or other related restriction to be deployed if supported by subsequent analysis," the Reserve Bank said.

Overseas DTI ratio restrictions aren't always used for investors. In the 2017 consultation submitters pointed out to the RBNZ that, given fairly low rental yields, a large investor with quite a low LVR - say 40% - would likely be a high DTI borrower and thus subject to a DTI limit. In response the RBNZ noted other serviceability policies, such as DSR restrictions, were applied to investors in Canada, Hong Kong and Singapore, and the Bank of England had suggested a macro-prudential “interest coverage ratio” could be applied to investor lending.

"This would limit the debt on rental properties to a level where, even at a stressed interest rate, the investor could comfortably service the debt with rental income from those properties," the RBNZ said.

Challenges

In its consultation response the RBNZ said analysis of rental income scenarios suggests it might be difficult to calibrate a DTI limit that appropriately restricts DTIs for owner-occupiers without being overly restrictive for investors.

"For example, an investor could have a DTI of five assuming a 4% net rental yield, an LVR of just 20%, and no other income servicing their loan. Even if that investor lost rental income for a long period, it seems likely they would be able to get further finance, e.g. push the LVR up to 25%, to cover interest payments in that period, so they do not appear high risk."

"Furthermore, the Reserve Bank’s current LVR restrictions on investment property already effectively limit debt on rental properties, unless they have a very low yield, to a level where the rental property income should cover the debt servicing. For example, using a stressed servicing rate of 7.5% and assuming a property yield of 4.5%, a rule that required debt to be limited to that serviceable with rental income would effectively limit the investor’s LVR to 60%," the RBNZ said in 2017.

Other issues were also raised in the 2017 consultation. These included that in order to apply DTI restrictions in an equitable manner across lenders, it would be necessary to tightly harmonise bank definitions, such as those covering what is permitted to count as income, and specific haircuts that would apply with a lower-than-market value placed on an asset being used as collateral for a loan. As with LVR restrictions an exemption for new construction was touted.

"Concerns were raised around more complex customer scenarios, e.g. where a home loan was combined with a business loan, or guarantees were issued by one family member in favour of another. Some submitters raised the idea of shared data services that would allow banks to gather information about customer income and/or debts at other banks more easily than at present," the RBNZ said.

What about a uniform serviceability interest rate for all banks?

In its response to the 2017 consultation, bank lobby group the New Zealand Bankers' Association (NZBA) argued the evidence linking high-DTI loans and default was weak, with job loss having the most significant impact on the likelihood of loan default. NZBA suggested a serviceability interest rate as a potential alternative.

A serviceability interest rate would be based on a notional interest rate set above current market rates to incorporate a level of interest rate sensitivity. Determined by the RBNZ, all banks would apply this rate to their affordability assessment calculation as a minimum affordability measure for borrowers.

Individual banks do already build in a serviceability buffer at an interest rate higher than current mortgage rates to get a feel for what repayments borrowers could afford if interest rates rise. This time last year for example, ANZ, the country's biggest bank, had a mortgage servicing sensitivity, or test, rate of 6.65% per annum.

NZBA argued a serviceability interest rate would have advantages over a DTI framework because; It's better able to respond to a rapidly changing market environment as it can be adjusted quickly and easily, banks will be able retain their current serviceability assessment frameworks, and it would enable a consistent approach for both owner-occupiers and residential property investors.

Undoubtedly there are challenges in developing a DTI macro-prudential tool. Apart from the politics of it, doing so for first home buyers would be simpler than for investors. The typical first home buyer scenario is pretty straight forward with salaries and just one property.

In contrast investors may have multiple properties, mortgages with different banks, rental income plus other income, and there will be a range of ownership structures including companies and trusts.

But similar issues have been overcome in the development of LVR restrictions, will little reported avoidance. And in terms of first home buyers, banks can favour them with an over sized proportion of the percentage of lending they're allowed to offer outside the restrictions.

*Interest.co.nz has a DTI ratio calculator here.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

21 Comments

Those graphs should scare everyone. Over 50% of all new lending is DTI >5 and LVR>70. It looks like in a major downturn it will be quite bad for quite a few people. Meaning the effects would be wide ranging. The solution being chased by everyone at the moment is to just try and inflate it all away with higher house prices (a grand game of musical chairs, it seems).

That'd be true but our approach to any downturn has been to rescue residential borrowers, this is because house price growth is now a large part of our economy.

The arguments about preventing home ownership are specious. Putting the DTI limits on will just curtail the collective amount that FHBs can spend on property (to some extent saving them from themselves). In the same way that every benefit to FHB borrowing power over the last few years has just been capitalized upwards into existing house prices, the reverse should apply. The net result will be more FHB in homes, if the rules are applied properly, as well as cheaper homes.

As for the effect on current house prices, we have to toss this idea that every time house prices go up we use the ratchet and try to lock in the current level. A healthy market will involve some level of correction and everyone should plan for the possibility.

Cool. Maybe the ones who made the massive gains at the expense of everyone else's standards of living should be chipping in. Fair is fair, after all.

Did you not know it's their right to become wealthy at other peoples expense because they've worked hard for it by using risky leverage that the bank made by typing some numbers on a keyboard?

As the RBNZ puts it, borrowers with elevated DTI ratios may be vulnerable if their income falls or interest rates rise, potentially presenting a risk to the banking system and the wider economy.

Until banks are precluded from over exposing their balance sheets to asset bubbles because of RBNZ sponsored capital incentives, all else is tantamount to navel gazing.

Hence, I cannot emphasise this dilemma enough:

Banks extending 60 % of their lending to one third of already wealthy households to speculate in the residential property market because the RBNZ offers them an RWA capital reduction incentive, to do so.

{kind=link}

Or this:

RBNZ cutting OCR in half five times since July 2008, causing the rich to capitalise rising discounted present values of future asset cash flows.

{kind=link}

You would have thought everyone would have noted the necessary lessons from 2008 - but if anything, its made people more ignorant to real risk.

I agree. The best way to sort this out is to require banks to allocate significantly more capital to residential mortgages viz. other lending (which the banks should be doing anyway as the bubble grows but probably aren't).

repeat

Robertson has already buggered first home buyers by letting the DTI ratios get so high to start with.

Introducing them now at any sane level would likely trigger a price correction so we can expect the teeth lady to come along in the new year and rule them out for as long as she is prime minister.

Incomes just need to catch up to house prices for the next hundred years you see and then everything will work out just fine.

Aroha BeKind.

If a strict & low DTI is introduced - how can a young FHB purchase in Auckland? Is this 'tool' being considered too late in the piece? Is it just going to benefit those with wealthy parents who can supply large gifting towards a deposit...

Yes, it's too late for cities now.

Those FHBs would (ideally) have less competition from investors -- and any other FHBs would be in the same boat, too. It should push prices down, or at least stop them rising.

Prices aren't going to decrease straight away though right... so if you've currently been able to purchase a $850k property, with DTI you may only be able to buy a $700k property. Basically this could rule you out of the game in Auckland unless you can get a gift from parents.

My initial guess would be the market would lock up while those with housing investments battle those without, to see what their political clout is and if this can be reversed.

Then if DTI's are obviously permanent your $850k property will come down to $700k because you were the demographic (income and age/savings) that was intended to buy it, all things being equal. The higher income buyers that can borrow and therefore pay more will still be getting the better house they were before just at a cheaper price. This change wont be smooth or overnight though.

In NZ house prices primarily controlled by what people can borrow.

Sharon Zollner on twitter:

Housing unaffordability is an enormous problem in New Zealand. It requires big, bold, urgent policy action. Engineering an orderly response that leads to better outcomes is absolutely possible.

https://twitter.com/sharon_zollner/status/1338614445124308994?s=20

We have the highest level of homelessness in the OECD, nearly twice the rate than Australia that is number 2. And now 15 years average to save a deposit for a house! So typical young person starts saving at 22 (after gap-year/s and tertiary training), so will be 37 by the time they're in a position to buy a house!

For those that say NZ is the bright light, well I'm not so sure. Perhaps it was.

Before RBNZ, ASB and ANZ may come out with such rules, first for rentals and gradually for FHBs.

Watch this space.

Meanwhile the posturing on both sides over this - essentially some high level finger pointing over the state of the housing market - is just fueling the FOMO. Your average FHB doesn't have any context, and mainstream media version they are hearing is "prices rocketing, LVRs ending, DTIs coming, quick buy now!".

"The RBNZ has regretted not having a DTI tool in the MoU since at least 2016, when it formally asked English for such a tool."

Started with BE then to "Steven Joyce, English's successor as Finance Minister, parked the idea in the 2017 election year by telling the RBNZ to conduct a full cost-benefit analysis on DTI ratio restrictions and consult publicly before he would consider giving the RBNZ access to such a tool."

Stalling tactic probably knowing that this would be well nigh impossible to quantify easily and public consultation. Consultation another stalling tactic. Get real.

The fiasco continues with Robertson (won't include Adern as she is just a mouthpiece).

"Opposition politicians Grant Robertson and Jacinda Ardern were also unenthusiastic about a DTI tool in 2017"

Orr must have realised he was dragging up old coals and wouldn't have any success

but covering himself if the financial system hits some serious wobbles.

Between National and Labour we're sunk.

DTI's will never be implemented. The Govt who brings them in would be voted out next election. Simple as that.

DTI should never been considered again, it's proven that housing cost is got nothing to do with income and immigration - the myth already been discussed several times in this website, C'mon. This debate, ideas of tinkering is not much more than like a desire to regulate the tobacco, alcohol & gambling industries. Housing is carry that 'intrinsic things' should never need regulation, it's solely a 'self regulated balance system of supply and demand' - but I guess tinkering with the idea is good enough for popularity contest, in the end .. just skip it.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.